26.07.2021

As we reach escape velocity, jobs hold the key – Q2 Comment

James Beck, Partner, Head of Investments

Global markets have continued their impressive run, buoyed by confirmation of the effectiveness of vaccines, the steady inoculation of populations and impressive economic indicators as we lap the economic paralysis of 2020. The touch paper lit by the vaccine announcements of November last year has burned through to ignite economic lift-off, just as some of the world’s more flamboyant billionaires competed to be the first galactic tourist – with Richard Branson having stolen a march on Jeff Bezos and Elon Musk. However, for investors, the real excitement came in the aftermath of the most recent pronouncement of the Federal Reserve, which saw sharp moves in government bonds with ramifications across asset classes. Inflation and employment are set to be the dominant narratives for the second half of the year.

Source: Official data collated by Our World in Data

The scores at half-time

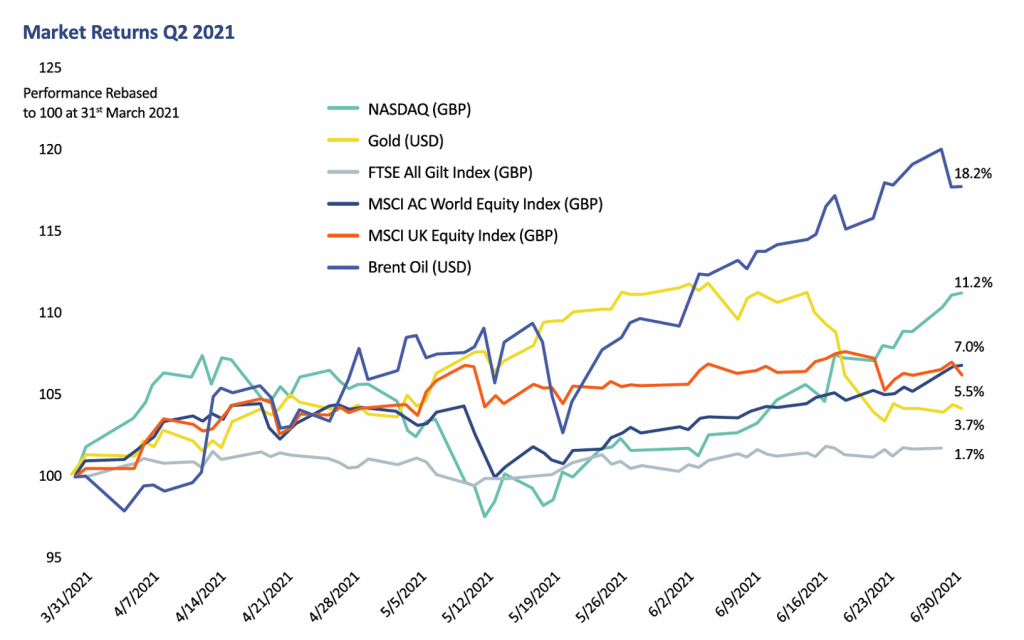

The previous quarter was one for traders rather than investors, characterised by sharp moves in many of the most economically cyclical and previously depressed sectors of the market alongside rampant speculation in cryptocurrencies, speculative tech and so called ‘blank cheque’ companies or SPACs. With the spring came April’s corporate reporting season and a chance to focus on the fundamentals. This provided confirmation of a more widespread recovery across companies and sectors. With earnings growing a whopping 60%, some 15% ahead of already upgraded analyst forecasts, markets saw a broadening out of returns as those areas previously left behind regained ground.

Global equities delivered another healthy quarter of returns with the MSCI All Companies World Index rising 6.9% in local currency terms. However, the positive momentum was evident in most asset classes as Gilts (+1.7%), US Inflation-linked bonds (+3.2%) and Hedge Funds (+1.7%) made steady progress. Commodities led the way with S&P Commodity Index up 15.7% driven by oil which continued its ascent as Brent Crude ended the quarter at $75/barrel (barely a year after a technical absurdity led it to price briefly in negative territory. Gold, too, reversed the decline of Q1, rising by 3.7% as the predicted acceleration in inflation revealed itself.

Global equities delivered another healthy quarter of returns with the MSCI All Companies World Index rising 6.9% in local currency terms. However, the positive momentum was evident in most asset classes as Gilts (+1.7%), US Inflation-linked bonds (+3.2%) and Hedge Funds (+1.7%) made steady progress. Commodities led the way with S&P Commodity Index up 15.7% driven by oil which continued its ascent as Brent Crude ended the quarter at $75/barrel (barely a year after a technical absurdity led it to price briefly in negative territory. Gold, too, reversed the decline of Q1, rising by 3.7% as the predicted acceleration in inflation revealed itself.

Underlying the strong move in global equities was a positive return from all major geographical regions with the leaderboard reflecting the stage of vaccination success. The US led the way (S&P 500 +8.5%) setting several record highs through the quarter, followed by Europe (+7.3%). Asia (+4.3%), Emerging Markets (+4.1%) and Japan (+0.1%) lagged as they suffered from further waves of Covid whilst the associated restrictions undermined the prospects for growth. China, too, acted as a brake on Asia as the government tightened policy to reduce heat from an economy which has already largely recovered. With the Communist Party celebrating its centenary on the 1st July, the change in leadership in the US has done little to diffuse the simmering strategic tensions that have punctuated recent years.

Given the globalised nature of most industries and wide geographical reach of companies, sectors now matter as much as geography. Here, too, it was a story of positive performance in nearly all areas with technology (+10.6%) and healthcare (+9.5%) leading having lagged in January and February. The long-term structural attractions of these two sectors are hard to ignore even when short-term attention favours industries that are more cyclically exposed. Companies operating in these industries are a core component of our portfolios given their underlying quality and sustainable growth.

Source: JH&P, Bloomberg data to 30th June 2021.

A simple twist of F.A.I.T.

The most hotly anticipated event of the quarter, other than the resumption of an old rivalry in the Euro 2020 Football Championships, was the June meeting of the US interest rate setting body, the Federal Open Market Committee (the Fed).

Participants in investment markets, particularly those with a shorter time horizon, have developed an obsession with every utterance of the Fed. This is not without good reason given that ultra-low interest rates have helped drive investment and asset flows.

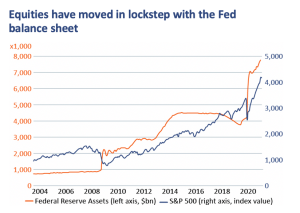

Since March last year the Fed has underwritten liquidity in the financial system, whilst its monthly purchase of $120 billion of US treasuries, corporate bonds and mortgage securities have suppressed yields and mortgage rates. As confidence has improved, this has provided a platform for strength in the US housing market and for excess savings to flow into stock markets. The recent correlation between the Fed’s balance sheet and the US equity market is striking.

Source: Refinitiv Datastream

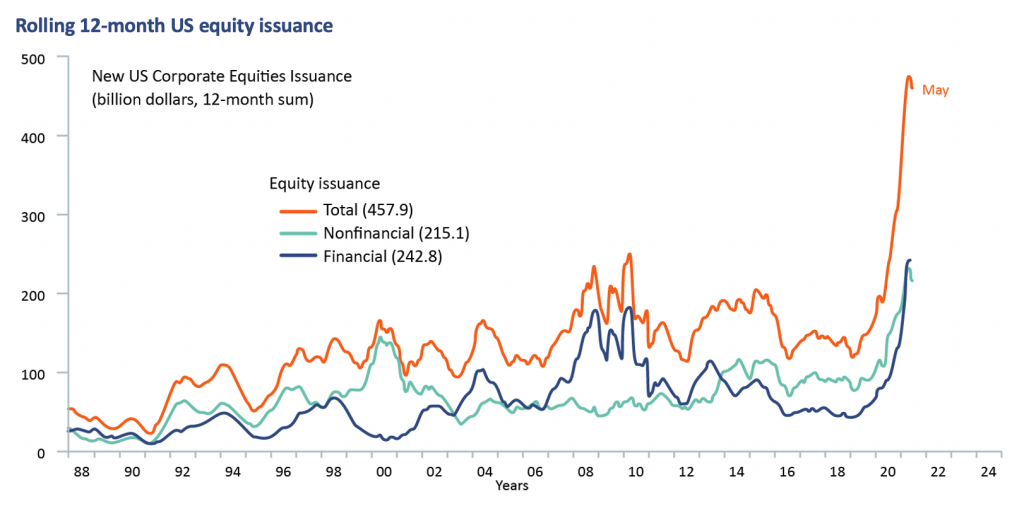

The combination of confidence, investor demand and ultra-low rates have propelled Olympic levels of bond and equity issuance. US companies have successfully issued more than $4.2 trillion of debt, nearly a quarter of all that outstanding. Similarly, many have taken advantage of record index levels and lofty share prices to issue equity at astonishing rates. The corporate sector has never been so flush with cash.

Source: Federal Reserve Board. Financial Accounts of the United States

Much of the confidence of companies and investors is built on the belief that Chairman Jerome Powell has the markets back. To this point he has given them every reason to believe he does.

In September 2020, a technical change in the Fed’s approach to embrace Average Inflation Targeting (F.A.I.T.) was another shot in the arm for investors. For those worried about interest rates going up, it effectively said that the Fed was no longer worried about short-term inflation – this could run hot – but concerned only with restoring the economy to full employment.

Yet in June, with more than 7 million jobs lost in 2020 still to be recovered, it came as something of a surprise to markets that the Fed made a subtle change in its forecasts. A majority of members now expected interest rates to begin rising in 2023 having seen 2024 as lift-off only one month earlier. Both dates seem a long way off!

With a May headline inflation rate of 5% fresh in the mind, markets interpreted this as the Fed returning to its inflation-fighting roots. Bond markets priced in even earlier rate rises in 2022 and with them lower growth in the future. Equity markets took their lead from the expectation of lower growth to return to their pre-pandemic predilection for the growth-orientated technology heavyweights. This added impetus to sector moves already in place.

Long-term bond yields now point to an economic environment of even slower growth than that which prevailed in the period of austerity and secular stagnation before the pandemic. Given the trillions of dollars injected into the world economy by governments, and the digital corporate revolution of the last 12 months, this seems a pessimistic projection.

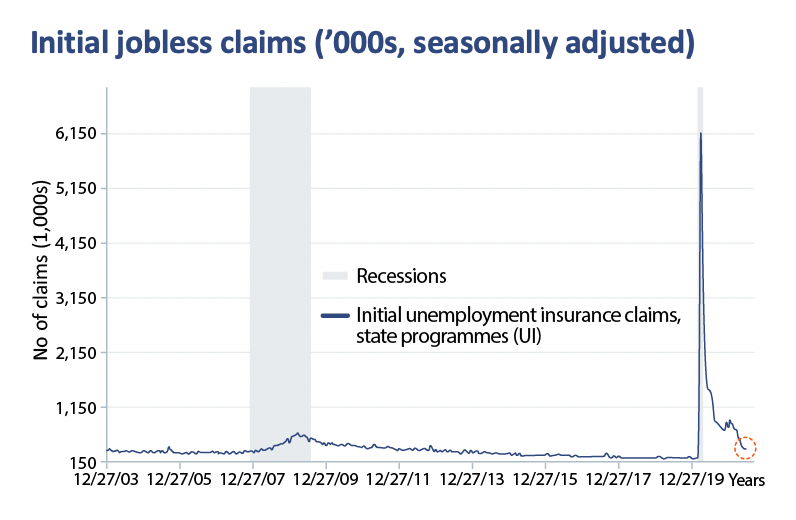

A lack of jobs is not the issue for unemployment

Coronavirus had a devastating impact on employment, particularly in the services sectors that dominate western economies. Unemployment rates across the West surged to depression levels even given the masking impact of furloughs.

The recovery has been equally impressive as befits what will be the shortest recession on record. Already 16 million of the 22.6 million jobs lost in the US have been recovered and an unemployment rate that flirted with the teens has dropped to 5.8%, albeit still above the 3% to 3.5% associated with full employment.

Source: Department of Labour, Bloomberg. William Blair equity research.

In Europe the situation is less rosy with the leisure and hospitality sectors still some way from returning to normal. Thanks to furlough, the UK is engaged in a guessing game as to what the real position is. However, at 4.7% UK headline unemployment is nowhere near the level of 8.5% reached following the financial crisis.

In the US, unemployment appears at odds with the number of available jobs. In May, the job openings rate reached 6.4%, a record, whilst business surveys report that 48% of firms are facing hiring difficulties with 22% planning to raise compensation to attract staff. Major employers such as Amazon, Walmart and Costco are already paying $15/hour, having raised wages this year, well above the Federal minimum wage. The likes of McDonald’s have resorted to increasingly desperate measures to attract workers.

A Pennsylvania McDonald’s is offering a hiring bonus. Keith Srakocic/Associated Press

If jobs are so plentiful, why is unemployment not falling faster? One possible answer is that unemployment benefits and stimulus cheques remain generous. For lower-wage workers current benefits are often better than potential earnings and so labour shortages remain pronounced in low-pay sectors such as leisure and hospitality. With the special measures rolling off through the summer, it should begin to pay to work.

Labour mobility, too, has been undermined by the pandemic and there are some who still feel nervous about venturing back into the workforce given the lingering health risks; many Americans have voluntarily eschewed the opportunity to be vaccinated. Parents have also been kept out of the market by school closures and the difficulty in finding childcare. All these factors should ebb away through the balance of the year.

As the focus of government spending moves from filling the Covid void to ‘levelling up’ and infrastructure spending, further growth in the jobs market should be forthcoming.

With the US adding an average of more than 500,000 jobs a month this year, a continuation of this rate would mean that full employment should be reached in the second half of next year.

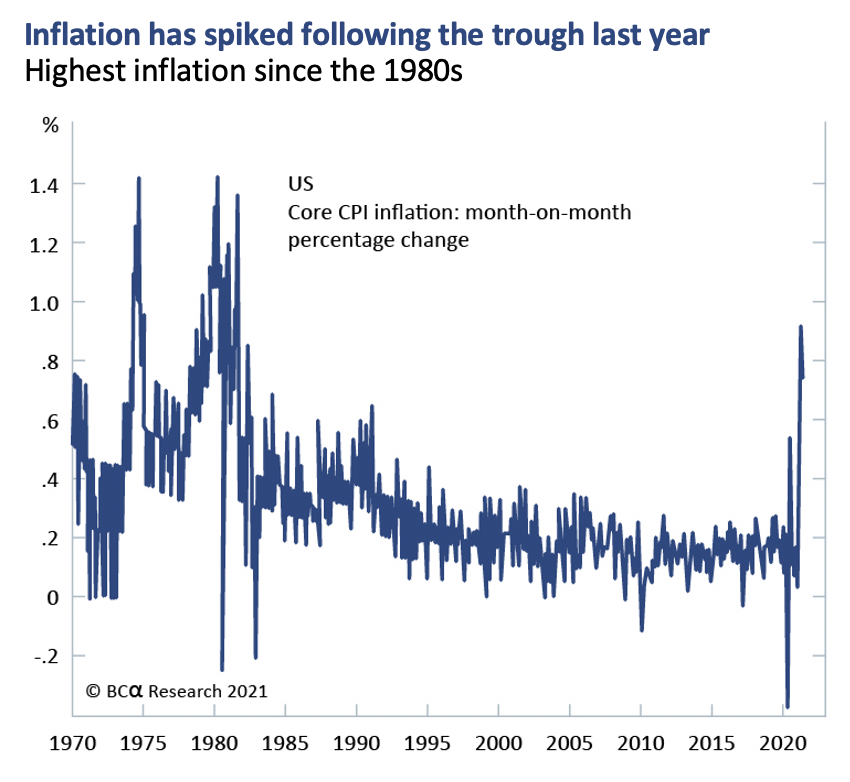

Inflation – when does transitory become intransigent

“I’m going to make a prediction – it could go either way” Champagne Ron Atkinson (Former Manchester United Football Manager and Television commentator)

While the prospects for employment look good, inflation remains more of a conundrum. As we expected in April we have seen inflation rates rise through April, May and June to levels not seen for decades.

Much of this spike is seen in the prices of products or resources that are in high demand as the world exits lockdown and where supply constraints, such as shipping bottlenecks, have limited the ability of suppliers to respond to rising demand. For example, lumber prices surged, not due to a lack of wood to support US housing demand, but due to capacity limitations at saw mills in Canada. Used car prices have risen as rental companies rebuild fleets in the face of a shortage of new cars – itself due to a shortage in semiconductors which is also impacting the world of consumer electronics bolstered by the demand shock of working from home.

These will pass in time as supply and demand adjust, lending credence to the central bank view that inflationary spikes will prove transitory. But there are risks to this narrative, particularly as inflation contains a psychological element that can prove self-enforcing.

In the near term, goods inflation will give way to services inflation as demand for flights, hotels and events surges when the blinking-eyed masses emerge from social hibernation. There is also a risk that disruptions persist longer than expected. Alongside these supply-side factors are the prospects that strong demand gives pricing power to labour and companies creating wage growth and price spirals.

Given the complexity of the moving parts, it is deeply uncertain as to how things will progress and how long central bankers will hold their transitory line. Ultimately, central bankers see inflation as a foe that they have the weapons to fight, unlike deflation. So, it will require some big surprises for them to be deterred from their glacial approach to the removal of stimulus this year.

“There are only three ways to meet the unpaid bills of a nation. The first is taxation. The second is repudiation. The third is inflation” Herbert Hoover

The longer-term inflation debate requires more time than we have here, but in a world of soaring government debt, the words of Herbert Hoover and precedent of the period after the Second World War suggest that there are plenty of politicians who might welcome some inflation to help erode deficits. Their friends at central banks may well oblige.

As good as it gets?

As we move past year-on-year comparisons against the most severe Covid impacts of 2020, there are early signs we may have reached the point of peak growth, peak policy, peak stimulus and peak sentiment. The US economy could grow by as much as 10% in the second quarter before slowing through the rest of the year. The UK and Europe are likely to be close behind. We have seen some leading economic indicators begin to roll over but we remain firmly in growth mode.

Even as the rate decelerates, pent-up demand and stimulus should help sustain an above-average growth rate well into 2022 as consumption patterns migrate from goods to services. Government infrastructure spending, whether through President Biden’s $1 trillion infrastructure bill or the delayed disbursement of the €750 billion European Recovery Fund, should plump corporate investment as well.

![]() A combination of government handouts and lockdown-enforced frugality has seen household savings rates rise materially. US consumers have increased their savings by $2.6 trillion dollars, with excess resources estimated at 12% GDP in the US, 7% in the Eurozone and 10% in the UK. This provides plenty of firepower for them to get out and spend.

A combination of government handouts and lockdown-enforced frugality has seen household savings rates rise materially. US consumers have increased their savings by $2.6 trillion dollars, with excess resources estimated at 12% GDP in the US, 7% in the Eurozone and 10% in the UK. This provides plenty of firepower for them to get out and spend.

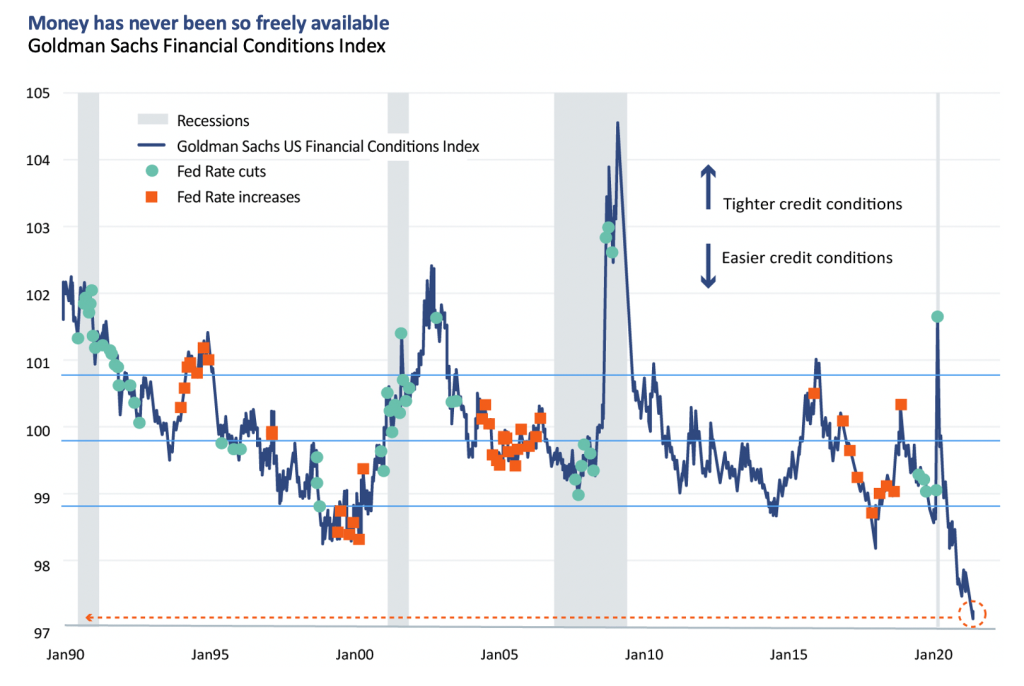

Renewed consumer spending will provide a bridge to an acceleration in capital spending by companies. Companies are extremely well funded having tapped bond and equity markets at rock-bottom borrowing rates. Financial conditions are looser than at any point in the last 30 years and, with plans having been on hold last year given the understandable caution of management teams, corporate spending is now on the up. This is already apparent in the record-breaking level of M&A.

Source: Bloomberg, William Blair Equity Research

With inventory restocking and infrastructure investment on the horizon, it is possible that spending will allow growth to endure at high rates well into next year. With a sequential recovery rippling east from the US to the UK and Continental Europe, and interest rates on hold for the rest of this year, there seems little prospect of recession in the next 12 to 18 months. The OECD is forecasting global GDP growth of 6% in 2021 and 4%–5% in 2022 as against the average of 2.1% in the 10 years preceding the pandemic.

Equities are well placed for growth and inflation

The robust economic backdrop should provide a healthy environment for continuing growth in corporate earnings, underpinning our confidence in equities as an asset class.

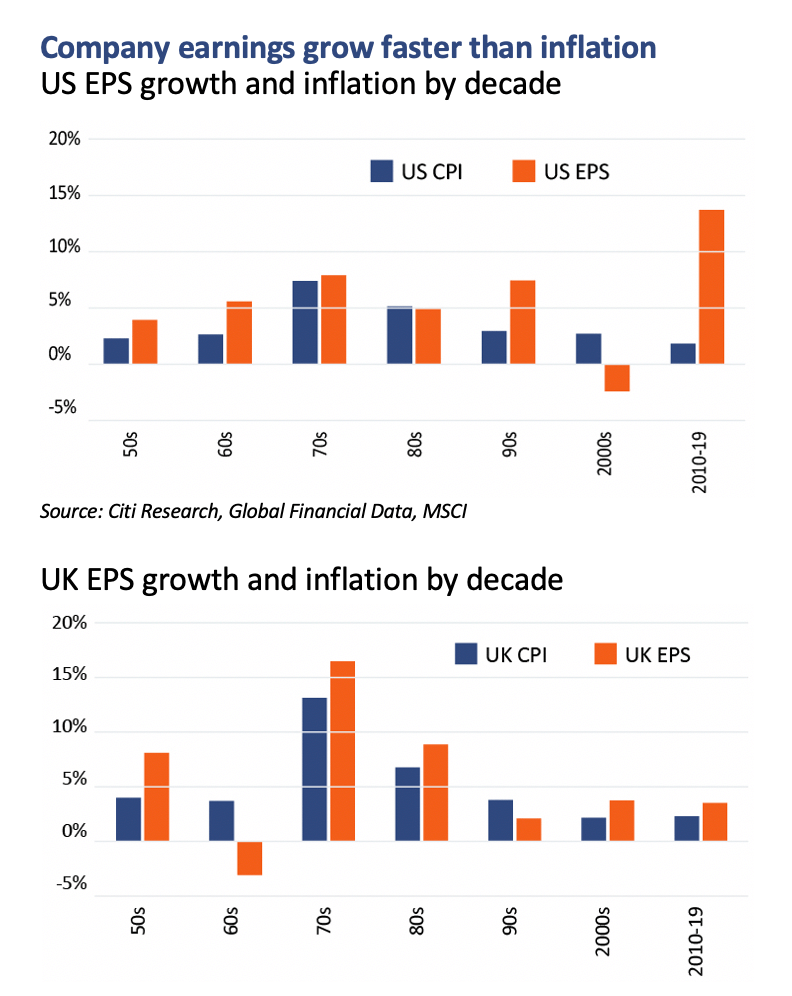

Equities have historically proven a good asset to own during periods of modest inflation, as companies with pricing power are able to increase revenues ahead of costs, a key area of focus for us in our own analysis. Even in the inflationary decades of the 1960s and 1970s aggregate equity earnings outstripped inflation. The notable exception was the US in the early 2000s following the collapse in the technology sector and notable bankruptcies from Enron and Worldcom.

Equities have historically proven a good asset to own during periods of modest inflation, as companies with pricing power are able to increase revenues ahead of costs, a key area of focus for us in our own analysis. Even in the inflationary decades of the 1960s and 1970s aggregate equity earnings outstripped inflation. The notable exception was the US in the early 2000s following the collapse in the technology sector and notable bankruptcies from Enron and Worldcom.

With demand underpinned by economic growth, companies look well placed to retain pricing power this time too. With the outlook for inflation in the balance, our view is that equities are better placed than other asset classes and have a considerable advantage over bonds.

The only obstacle to our taking a more constructive view on equities now is their strong performance this year and valuations which are full by historic standards, particularly in the US. Prices reflect much of the expected good news. With sentiment verging on complacent and positioning buoyed by a record inflow of $600 billion into equities so far this year, it would be no surprise were we to see bouts of profit taking as we move through the mid-cycle transition from recovery to a steadier economic state.

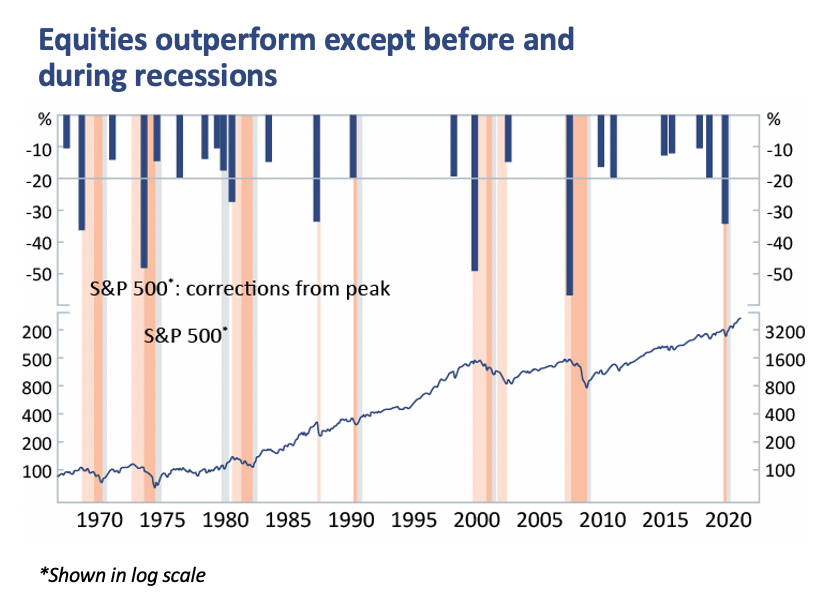

Factset[1] estimates that profits will grow by 42% this year given the recovery, and that growth earnings will be sustained into 2022. Should equity valuations drift lower, earnings will cushion the impact and should sustain share prices. Indeed, it is rare for equities to underperform outside of a recession, particularly without any rise in interest rates. With no recessionary signs on the immediate horizon and rates on hold for the rest of this year and into next, there is little reason to change our view for the remainder of the year.

Factset[1] estimates that profits will grow by 42% this year given the recovery, and that growth earnings will be sustained into 2022. Should equity valuations drift lower, earnings will cushion the impact and should sustain share prices. Indeed, it is rare for equities to underperform outside of a recession, particularly without any rise in interest rates. With no recessionary signs on the immediate horizon and rates on hold for the rest of this year and into next, there is little reason to change our view for the remainder of the year.

The curious case of bonds

Given the accelerating narratives around both inflation and growth in the US, the positive returns for bonds last quarter as well as the current level of yields are proving something of a conundrum. In the US, 10-year yields have fallen below 1.4% from 1.7%, pushing inflation-adjusted yields even further into negative territory as inflation has moved higher.

Part of the explanation may be technical. With US government bonds having just experienced their worst quarter since the early 1980s, positioning provided fertile conditions for a snap back. Other justification can be found in the negligible or negative yields offered by the alternatives of Japanese and German bonds. With the ability to hedge the currency cheaply with interest rates near zero across the world, risk averse institutional investors can achieve higher levels of income by buying US government bonds, thereby keeping demand elevated even if real yields are negative. It is also easy to forget that the Fed is still active in the market.

Whatever the reasons, the fact is that government bonds offer little attraction to investors looking to generate either absolute or real return over the long term. For the long-term investor their only role is to provide some offset against heightened volatility in other assets and protection against unforeseen risks.

We expect yields to rise again in the second half of the year given our views on both growth and inflation. With rising yields translating to falling prices, our current exposure remains low with our only holdings in the highest quality government bonds as protective assets where we favour inflation-protected securities in case current views prove too benign.

The crypto-chickens come home to roost

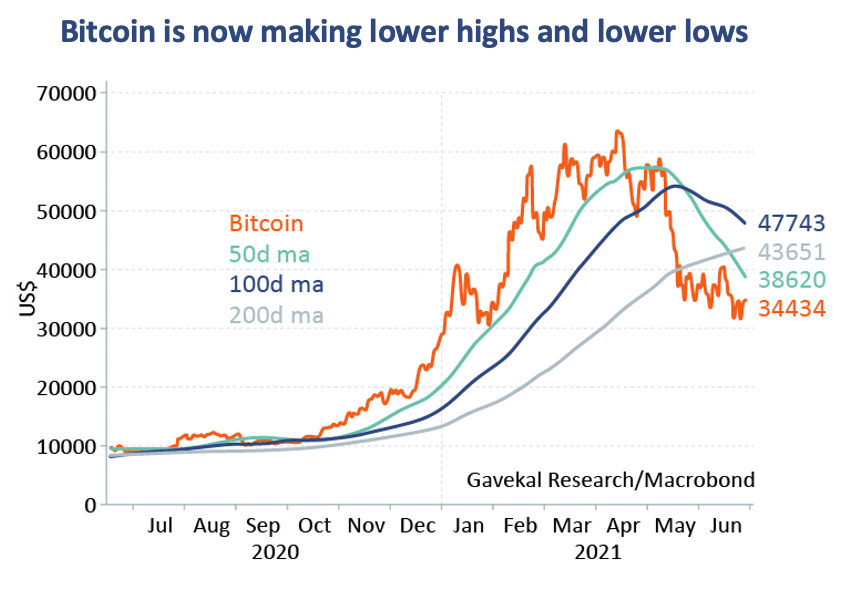

We were inundated with questions about cryptocurrencies earlier in the year and wrote last time of our preference for the tried-and-tested protection of gold given the speculation and volatility that seemed worryingly present in Bitcoin et al. Cryptocurrencies have since come back to earth with a bang, although they remain a topic that evokes primal responses from champions and critics alike.

The mania around digital currencies had spread from Bitcoin to Ethereum to Dogecoin and into the world of Non-Fungible Tokens (NFTs) which have allowed for the auction of digital art, avatars and even an invisible sculpture (sold for $18,000) at stratospheric prices. The levels of euphoria had many of the characteristics of a bubble which peaked, coincidentally, on the day before the $85 billion flotation of Coinbase, the leading crypto trading exchange.

Whilst we do not rule out that Bitcoin or another token may have an important role to play in the future of finance, they do not yet meet the requirements of a currency and remain the domain of the speculator; they are not a store of value, medium of exchange or unit of account.

Many of the perceived risks came home to roost, as Bitcoin’s environmental footprint, criminal association and vulnerability to regulation mounted against it.

It was widely reported that the energy usage of mining and transacting in bitcoin approximated to that of a medium-sized country. Proponents such as Elon Musk moved to dial back their support, whilst the ESG credentials of some institutional investors compelled them to temper their views.

It was widely reported that the energy usage of mining and transacting in bitcoin approximated to that of a medium-sized country. Proponents such as Elon Musk moved to dial back their support, whilst the ESG credentials of some institutional investors compelled them to temper their views.

China, the source of much cryptocurrency mining, undertook a large crackdown on the mining and trading of bitcoin, motivated in no small part by its plans to launch its own government-backed digital currency. The regulatory noose has tightened worldwide with the Bank for International Settlements, FCA and SEC all either proposing or implementing further restrictions on the use and regulation of cryptocurrencies.

Finally, we were concerned by Bitcoin’s use in criminal enterprise, by its association with a number of high profile ransomware and cyber-attacks. Having been used as the ransom of choice in a series of cyber-attacks, notably shutting down the Colonial oil pipeline in the US, confidence in Bitcoin was further rocked by the FBI’s success in tracing and recovering half of the $4.4 million ransom paid – the success by a federal law-enforcement agency in tracking movements was a further mark against it.

Greatest threat to Goldilocks is that she gets the virus

“There are known knowns; these are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns – the ones we don’t know we don’t know.” Donald Rumsfeld, former US Secretary of Defense

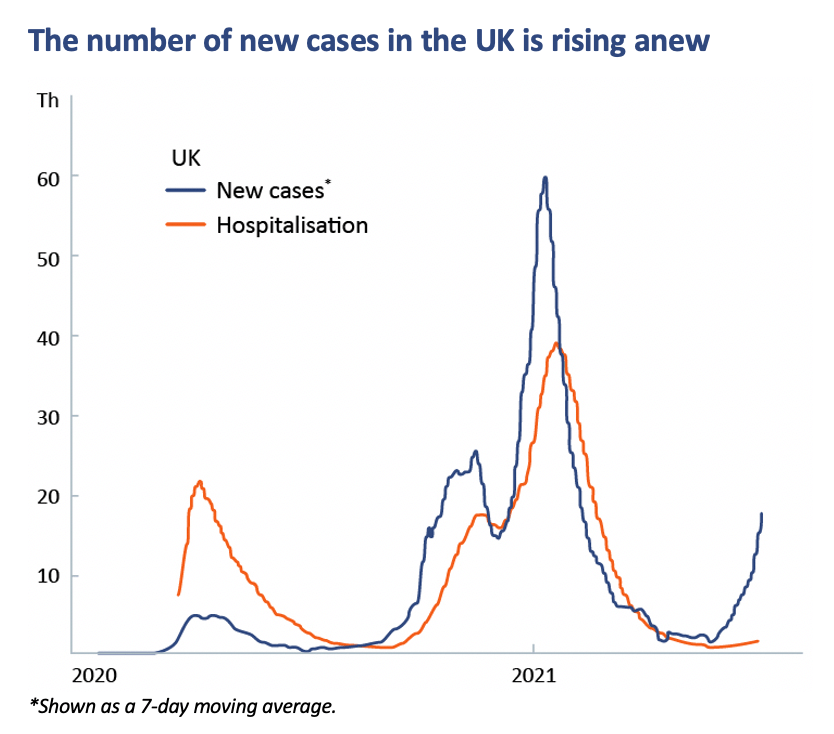

This oft-quoted statement from Donald Rumsfeld elegantly encapsulates the current risks, perhaps poignantly so given his recent death. We have already referenced the known risks of inflation, yet cyber-attacks are a growing threat to the present harmony in markets. However, the most obvious known unknown remains the virus, given its potential to derail the reopening and economic progress to date.

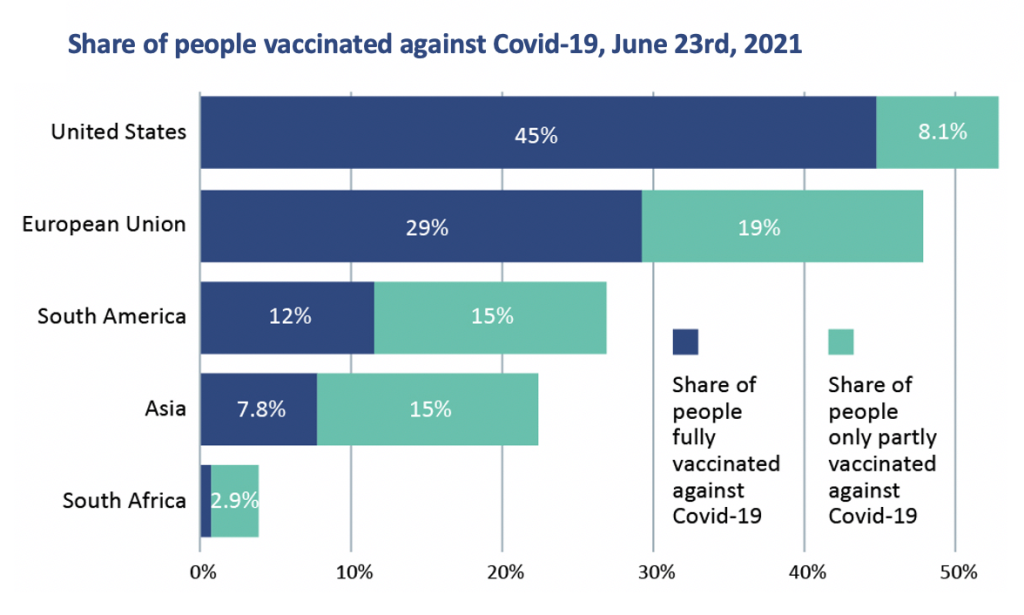

The Delta variant in the UK has surged as social distancing measures have been rolled back. However, even with case numbers having returned to similar levels to those experienced in early January, hospitalisations have not followed. Whilst the increasing numbers are a concern, the lack of hospitalisations adds credence to the belief that vaccines would provide a means of limiting the danger of Covid to life, allowing society to learn to live with the virus.

Cases are rising but hospitalisations are not

Source: the center for systems science and engineering (CSSE) at Johns Hopkins University, and our world data.

Encouragingly a nascent UK study has shown that two doses of the Oxford-Astrazeneca vaccine have been 92% effective against hospitalisations from the Delta variant and the Pfizer-BioNTech 96%.

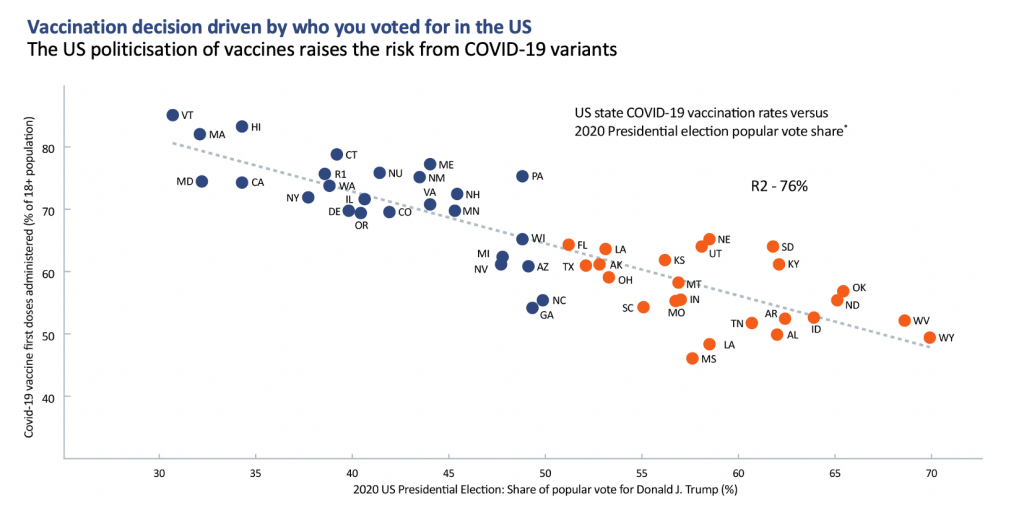

Should the US be beset by the Delta variant too, with economic activity nearing normal after the 4th July holiday, it seems unlikely that there will be a reduction in freedoms. However, with one third of US adults yet to receive a single dose, the risk of disruption is higher. That the lack of vaccination is due to choice (split strongly along political lines) makes the likelihood of further lockdowns more remote. There is a determination to find a way to live with the virus.

* Source: US centers for disease control and prevention and the Cook political report. **As of June 30th, 2021

The future is brightening but…

Conditions are buoyant and the outlook is brightening. Should the US economy continue to grow as anticipated, it is inevitable that stimulus will begin to be withdrawn from the economy. With the volume of fiscal support announced by the US government, $6 trillion and counting, the Fed’s asset buying programme would be simply too generous for the circumstances. It is reasonable to assume that, barring any shocks, the Fed will announce its intention to reduce stimulus and ‘taper’ its asset purchases. This could come as early as the annual central bankers’ jamboree at Jackson Hole; we know they are ‘talking about talking about’ tapering.

Given the perceived reliance of asset prices on both abundant liquidity and low yields then, there is every chance that this causes jitters through markets that have benefited from both fiscal and monetary largesse. The velocity of change means the next six months are sure to be riddled with mixed messages.

Short-term forecasting, a flawed and imprecise enterprise at the best of times, is likely to prove more challenging than ever.

The strength of returns so far this year mean that aggregate returns are likely to prove more muted in the second half even if the news remains benign. Within portfolios we remain focused on building a resilient collection of businesses and funds that can prosper over the longer term irrespective of the current economic backdrop, whether through the ability to pass on price increases during a period of accelerating inflation, or exposure to growing structural trends in a period of lower economic growth. Companies that offer ‘sustainable growth’ reduce the requirement to predict and react to the latest economic data. Trying to chase or anticipate short-term trends in a period of such rapid change has as much chance of success as the English football team in a penalty shootout. The fewer kicks we take the better!

………………

[1] Factset, Financial Data, Analytics & Trading Solutions, factset.com

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.

James Hambro & Partners LLP is a Limited Liability Partnership incorporated in England and Wales under the Limited Liability Partnerships Act 2000 under Partnership No: OC350134. James Hambro & Partners LLP is authorised & regulated by the Financial Conduct Authority and is a SEC Registered Investment Adviser. Registered office: 45 Pall Mall, London, SW1Y 5JG. A full list of partners is available at the Partnership’s Registered Office.