The importance of a long-term mindset

The good old days

It is intriguing how some things don’t change, like the human tendency to reminisce on better times. As far back as the ninth century, Alfred the Great, complained of how much better England was in the good old days.

“It very often comes to my mind what wise men there formerly were throughout England both of sacred and secular orders, and how happy the times were then throughout England and how the kings who then had power over the people obeyed God and his ministers.”

Looking back, events in the past appear easier, less intense, and more benign than they do in the present. If we are honest with ourselves, such nostalgia is misguided. If transported back to that moment, we would realise that we were experiencing concerns and anxieties then as well. Politicians were disappointing, our financial security felt threatened, and we craved a more certain existence. Humans are predisposed to feel anxious and dissatisfied; there is always something to worry about, always more we want.

Daniel Kahneman wrote: “nothing in life is as important as you think it is while you are thinking about it.” In investing, we tend to myopically focus on the challenges of the present, shortening our investment time horizon just at a point when the opposite is ordinarily the right course of action.

It’s always different this time

The tragedy unfolding in Ukraine has brought the horror of war to mainland Europe for the first time in a generation. The scenes of women and children being loaded onto trains to unknown destinations leaving their husbands and fathers behind, forced to stay and fight, are heart-breaking.

It is not surprising, therefore, given Russia’s invasion of Ukraine, that people are saying, “no but this time it really is different”. And perhaps it is but, the specific risks are always different. True risk is what is left over when everything else has been considered. Investment literature is full of benign statements like markets hate uncertainty but, given we are not capable of predicting the future, uncertainty is a fact of life; risk is a constant.

Stanley McChrystal, the US military general best known for his command of Joint Special Operations in the mid-2000s, described risk as an equation: “risk equals vulnerabilities times threats”. This is an observation particularly relevant to investment management. Threats are unknown but inevitable, vulnerabilities are known and manageable. When we invest, we need to focus on the things we can control; we need to minimise our vulnerabilities. The more limited our vulnerabilities, the less of an impact the threats will have when they inevitably surface.

Time matters more than returns

How can we limit our vulnerabilities and prepare ourselves for the inevitable threats as they emerge? The first is by having a long-term mindset. The author Naved Abdali wrote, “A modest rate-of-return can accumulate a fortune over time. You don’t need to beat the market, do over-leveraging, or pick the best stock to be rich. You just need to earn a decent rate-of return and let your money compound over time.”1

Compounding is such a simple concept but is rarely properly understood. The investment writer Morgan Housel describes compounding as simply returns to the power of time. The problem is that too much focus is given to returns and too little attention to time.

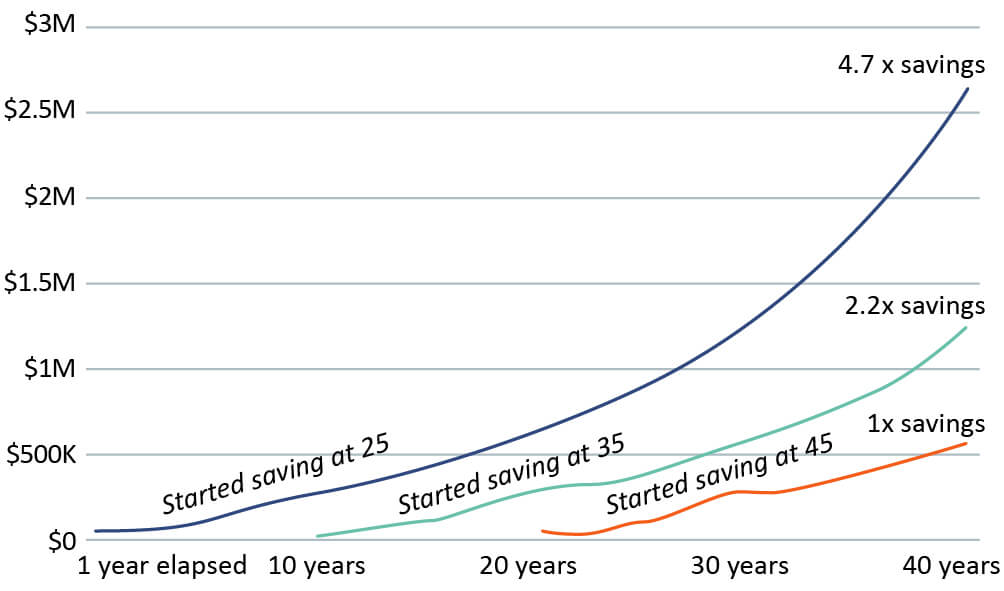

Power of compound interest

Savings = $12,000 a year for ten years at 8% p.a.

Source: https://www.profgalloway.com/the-algebra-of-wealth/

Some individuals can produce phenomenal investment returns in short periods of time but how many can produce those returns consistently year after year? Very few. Warren Buffet is not one of the world’s richest people because he was able to produce extraordinary annual returns. His returns are very good but there are many that have done better. The reason Buffet has amassed a fortune is because of the consistency and length of time he has been generating good returns. 99% of his wealth was accumulated after his 50th birthday and 97% after his 65th birthday. If you can produce attractive returns for a very long time, the impact can be remarkable.

However, saying you are a long-term investor and consistently acting like one are very different, particularly when circumstances become more challenging. The zeitgeist of modern investing is the antithesis of a long-term mindset. Second-by-second pricing, constant news flow, and daily research from brokers who are incentivised to drive action, not inaction. Bad news sells, optimism is in short supply. When our fears reach a crescendo and our fight or flight instinct takes over the easy thing to do is sell; staying the course is very hard to do in the face of an always uncertain future. Yet good assets can only provide compound returns if we allow time to work its magic. It is hard to do nothing, but if we have selected our companies well and believe in their true ability to generate attractive returns on a persistent basis, then doing nothing makes sense.

Putting this approach in some historical perspective. Since the trough of the market in March 2009, during the financial crisis, the MSCI All World Index has returned 14.8% per annum to 31/03/22 in sterling terms. £1 million compounded for 13 years at 14.8% equates to £6m today.2 During that time, we have endured peak to trough declines of more than 20% on three separate occasions and all for very different, largely unpredictable reasons. Unfortunately, such attractive long-term returns are only achieved by accepting significant volatility over shorter periods of time.

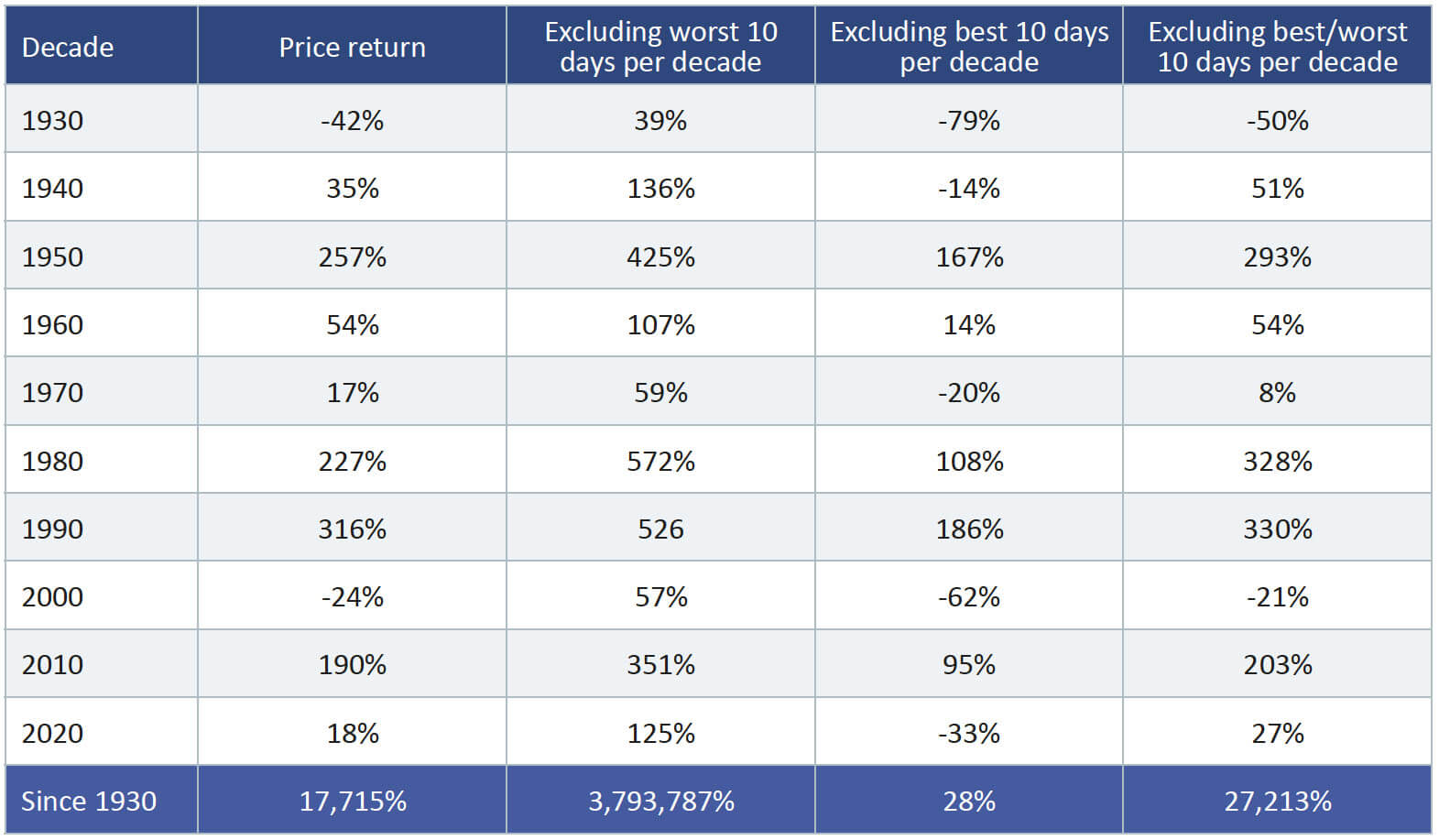

As illustrated in the table below, missing the ten best days in any decade can lead to significantly lower returns than if we hold on and ride out the harder times. In fact, between 1990 and 2022 a compound annual return of 8.3% falls to -4% if the 90 best days are missed. The very worst periods are always followed by the very best. Trying to time markets is a dangerous game.3

The difficulties of trying to time the market

Bank of America looked at the impact of missing the market’s best and worst days each decade

Source: Bank of America, S&P 500 returns.

Ecosystem control

“The chief task in life is simply this: to identify and separate matters so that I can say clearly to myself which are externals not under my control, and which have to do with the choices I actually control. Where then do I look for good and evil? Not to uncontrollable externals, but within myself to the choices that are my own…” — Epictetus, Discourses, 2.5.4–5

So how do we maintain a long-term approach and how can we minimise our vulnerabilities to allow the assets we own to do the work for us through the power of compounding? The ecosystem in which we, as investors, choose to operate can go a long way to creating a foundation for long-term thinking. Our partnership structure, the team we have built, and the long-term focus of our management provide an essential foundation.

It is also you, our clients, and the owners of the capital we manage, who have a time horizon aligned with our principles and approach to investment; enabling success to accrue over time.

Being uncompromising on the quality of the assets we own will protect us when threats emerge. Our quality threshold for asset selection means we apply the same principles that we apply to ourselves to the companies and funds we buy – a culture of alignment that favours long term strategic capital allocation and an investor base supportive of these principles.

We look for business models that have the opportunity for sustainable growth and competitive advantages that will endure. We avoid companies with leverage or whose success is dependent on exogenous forces. We favour businesses with recurring revenue and limited capital intensity giving them the opportunity to invest for growth in the bad times as well as the good; allowing them to emerge from more troubled times in better shape than their peers. We think about returns from a probabilistic viewpoint, preferring a high probability of an attractive return over a low probability of a very high return. A resilient portfolio of companies built on being owners of businesses not renters of names on a screen.

Staying in the game

“Diversification is the Kevlar that protects you — with it, bad decisions will still hurt, but they won’t prove fatal. Diversification, in other words, is your bulletproof vest.”4 Scott Galloway

But being dogmatic about the companies we own requires a sensible level of pragmatism about how we build portfolios. Being pragmatic means we are honest enough to admit we can be wrong or that we too are human and can get emotionally drawn into the terror of the short term. Diversification is the tool we use to save us from ourselves, to protect us from capitulating when it is most irrational to do so – it is always darkest before the dawn.

Building protection into the portfolio by adjusting what we own is vital to staying invested and reaping the long-term rewards. It is likely that the dual impacts of the pandemic and the war have changed the investment landscape for the foreseeable future. Inflation, which has been close to non-existent for many years, has risen precipitously. Central banks now have their sights firmly trained on fighting inflation, which means economic growth in the medium term is likely to slow. Will slowing demand bring inflation back to more comfortable levels? Will higher interest rates slow consumer demand and cause a recession? Has inflation now taken hold so that it will remain higher for longer? These questions are very important, the answer to them is unknown – the future is uncertain.

Whatever the future path of the economy, we firmly believe that our companies have the ability to navigate this successfully. High levels of pricing power and limited capital intensity will provide some protection in a backdrop of higher inflation. Secular demand and recurring revenues will limit downside should growth begin to slow. Recognising this changing landscape, our equity exposure has already been adjusted since the trough of the pandemic. A greater level of exposure to the banking system provides some protection for rising interest rates. Resources exposure has given us cover for the backdrop of rising materials prices already evident before the war but exacerbated by it. There could be more we can do here; we are working hard to find the right solutions.

Around our core group of equities, we continue to use a set of diversifying assets that can provide greater levels of protection from inflation and are uncorrelated to equity returns. These assets should smooth the ride and give us the strength to hold onto the companies that we believe have the right attributes to exit any storm stronger than they entered it. The world is risky, riskier today than it was six months ago. We will continue to watch the situation closely adjusting as the facts change, so that we can hold our nerve and allow our assets to compound thanks to the wonderful power of time.

1 Investing – Hopes, Hypes, & Heartbreaks: The Game is Rigged and is Rigged in Your Favour, Naved Abdali

2 For completeness, taking the top of the market in October 2007 as the starting point reduces the annual return to 9.8% per annum. £1m invested for 15 years at 9.8% equates to £4m today.

3 https://www.cnbc.com/2021/03/24/this-chart-shows-why-investors-should-never-try-to-time-the-stock-market.html

4 https://www.profgalloway.com/the-algebra-of-wealth/