MAJOR RECESSION, MILD SLOWDOWN OR SOMETHING IN BETWEEN?

James Beck, Head of Investments

“If you are not confused, you don´t know what is going on.” Jack Welch, Chairman and CEO General Electric 1981 – 2001

The first half of 2022 was one of the most challenging for markets in 50 years with a balanced 60:40 equity:bond portfolio performing worse than at any time outside the financial crisis. Almost all asset classes suffered as markets raced to adjust to high inflation and rising interest rates.

Valuations are now more in-line with long-run averages, suggesting market direction for the remainder of the year will be tied to the progress of corporate earnings and outlooks. These have been surprisingly healthy to date but, with signs of a slowdown already evident, this strength looks set to be tested.

Investor confidence is low with good reason – a range of growth and inflation combinations are possible, each with quite different implications for portfolios. Inflation is at record levels but longer-term price expectations are sinking. Consumers are flush with cash but more pessimistic than ever. Job markets are booming but housing markets stalling. If we are entering a recession, it is unlikely to look like any other on record.

We maintain a cautious approach with a focus on ensuring portfolios are resilient in most scenarios.

One of the toughest 6 months on record

Weak performance across almost all assets accelerated in the second quarter as inflation showed few signs of moderating, interest rate expectations moved ever higher and future estimates of economic growth began to include mentions of recession.

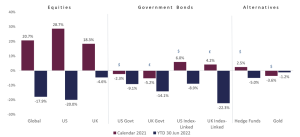

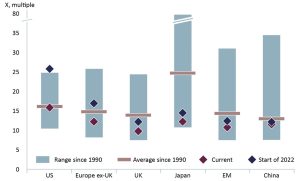

FOLLOWING A STRONG 2021 – FEW PLACES TO HIDE THIS YEAR

Asset class returns in local currency

Source: Bloomberg

Equity markets, as measured by the MSCI All Countries World Index, fell 17.9% (in US dollars). The US led the declines with the S&P 500 down 20% and the technology focused Nasdaq falling by almost 30%. The picture was similar, if not as pronounced, across most regions. The UK proved most resilient, with the FTSE All Share falling only 4.6%, buoyed by its exposure to energy and utilities. Despite this, the UK market remains a laggard over the last five years.

For the last thirty years sharp falls in equity markets have been accompanied by a counterbalancing stability in bonds, particularly government bonds in the US, UK and EU. The experience this year has been quite the opposite. Bond markets have fallen in lockstep with equities as prices have adjusted to the accelerating regime shift associated with inflation and rising global rates. The FTA All Gilt Index in the UK fell 14.1% from the 1st of January to 30th June, whilst US Treasuries dropped by more than 9%. These represent the worst first half return from bonds in fifty years.

The collapse of the bond market represents a colossal unwind of a decade of loose policy culminating in the response to the COVID pandemic in 2020. The bursting of the bond-market bubble has seen the outstanding stock of negative yielding bonds fall from a peak of $18 trillion to less than $1 trillion according to Bloomberg; a much more rational state of affairs. Buying bonds no longer means guaranteed losses.

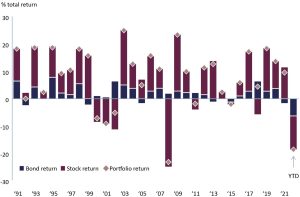

BONDS ON COURSE FOR THE BIGGEST LOSS SINCE 1920

World govt bond GDP weighted return index (annual returns)

Source: BofA Global Investment Strategy, GFD, *2022 is YTD annualised

The combined impact of simultaneous falls in both assets has meant that the traditional balanced portfolio of 60% equities and 40% bonds is now on track for its worst annual return since 1990. It is already second only to the fall seen in 2008 at the height of the global financial crisis.

60:40 portfolios on track for their worst year since the financial crisis

Annual returns in a 60:40 stock-bond portfolio

Source: Bloomberg Barclays, MSCI, Refinitiv Datastream, J.P. Morgan Asset Management Stock returns are calculated using MSCI All-Country World Index and bond returns using Bloomberg Barclays Global Aggregate. All returns shown are in USD. Data as of 14 June 2022.

There were few shelters from the storm, with commodities the only bright spot, rising 35.8%. This reflected strength in oil and gas prices which rose nearly 50%, whilst many industrial commodities such as copper fell given the COVID-induced shutdowns in China and slowing industrial demand.

At an equity sector level energy proved the only positive in the first half of 2022 rising by +15.4% in US dollars. All other sectors were in the red, with technology and consumer sectors the worst performing (-29%). Even supposed inflation linked sectors such as materials (-17.4%) and real estate (-18.5%) fell with the market. More defensive sectors such as utilities and healthcare did better than the broad market but still fell between -5% and -10%.

MORE ATTRACTIVE VALUATIONS ACROSS THE BOARD

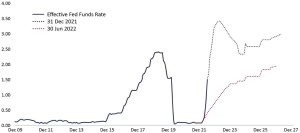

Market expectations of US interest rates have surged and are now expected to reach 3.5% by the end of the year, more than double that forecast in January. Government bond yields have followed with US 10- year bonds yielding 3% whilst 10-year gilts yield 2.3%. The pace and scale of interest rate rises look increasingly well reflected in government bond markets. They now offer some defensive attractions.

Fed Funds Rate & Futures Market Expectations, %

Interest Rate expectations have more than doubled since January

Source: Bloomberg. William Blair Equity Research

Corporate credit markets have also been subject to a substantial reset with the additional return offered over and above government bonds now more reflective of the risks, particularly if we see a recession. US High Yield bonds now yield 8%, 5% more than treasuries and more than twice as attractive as late last year.

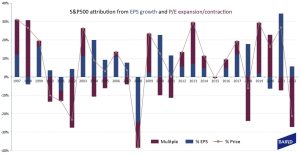

In equities, the sell off this year so far reflects a downward adjustment to valuations rather than a material reset in growth or earnings. The chart below illustrates that whilst last year’s market return reflected strong growth in earnings, 2022’s market declines have been driven by lower P/E ratings, with prices falling even as earnings have held positive. The last time we saw such a contraction in valuation was in 2018, which was also the last time the Federal Reserve (the Fed)raised interest rates. The Fed ultimately backed off in 2019 prompting a rapid recovery in equities.

The fall in markets this year is entirely due to a fall in valuation

The reset in the price of everything this year has left most assets trading at much more balanced levels. Equity valuations are now in line with long-term averages, if not cheaper, while 10-year inflation adjusted yields are positive and corporate credit is paying a more normal premium for risk.

If the first six months were about valuation, the next six months will be about growth and earnings, the ‘E’ in P/E. Whilst economists have been competing to downgrade their economic forecasts this year from over 4% to nearer 2%, we have yet to see a similar impact on estimations of company earnings. The direction of earnings will prove the key driver of market returns in the second half.

The crucial determinants of those earnings will be the intertwined forces of inflation, interest rates and growth.

Valuations are now In-Line WITH long-term averages

Source: JP Morgan Asset Management

A Not So simple matter of Inflation, Rates and Growth

Inflation is ultimately a symptom of an economy in transition and out of equilibrium, where supply and demand are misaligned and prices move to try and re-establish that balance. The fiscal response to COVID was $11 trillion, four times that to the global financial crisis. Add a further $10 trillion of central bank liquidity and is it little surprise that we are seeing big swings in prices. The COVID experience has thrown the world off balance.

With the Russian invasion of Ukraine adding an energy shock into the mix, US headline inflation reached 8.6% in May, shocking bankers and markets in equal measure.

Fed Chairman Jay Powell has left little doubt that he is more concerned about fighting inflation than protecting markets or growth. For the first time in thirty years, he is willing to risk a recession and falling markets to bring prices back under control. The outlook for growth and markets therefore depend on how quickly inflation stabilises allowing central bankers to ease off the brakes.

Passing the peak in Inflation?

For those of us filling up the car ahead of a holiday drive (or for those at the vanguard of the energy transition, running up electricity bills to charge an electric car) the idea that inflation may be nearing a peak is hard to believe.

However, there are reasons to believe that inflation may begin to roll over as the year progresses even if it may not come back to levels that persisted pre-pandemic. The Fed’s own forecasts expect US inflation to fall back to 4.5% by the year end.

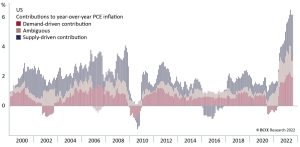

Supply factors explain half of the increase in prices over the past year

Source: Federal Reserve Bank of San Francisco.

Data from the Federal Reserve Bank of San Francisco estimates that nearly half of the increase in prices is due to supply constraints, particularly the ability to source and transport goods.

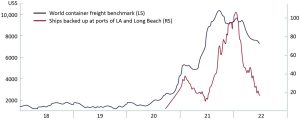

Here there are encouraging signs with freight indicators easing from their 2021 peaks and backlogs at key ports falling. Evidence from many companies suggest that inventories and stock levels have been rebuilt, whilst recent warnings in the retail sector from Walmart and Target suggest that pandemic trends were over-extrapolated leading to over-ordering in some sectors. Even Amazon has admitted to overinvestment in logistics and distribution, sending shockwaves through the listed logistics sector.

Supply logjams are beginning to clear

*Source: Drewry Shipping consultants; shown in US$ per forty foot container

** Source: Marine Exchange Southern California. Includes ships at anchor in ports as well as those waiting beyond the ports safety and air quality area following queuing regulation implemented on 16 Nov 2021.

Prices for many commodities have rolled over from their peaks. Industrial metals have fallen over the year while soft commodities and even oil have seen their prices moderate in recent weeks (although with refining capacity limited, we are unlikely to see much benefit from the latter move at the petrol pump soon).

The demand driven components of inflation are still significant but the combination of a fading fiscal stimulus, particularly the “free money” of stimulus cheques, and liquidity withdrawal as quantitative easing gives way to quantitative tightening should take some of the heat out of demand even before interest rate rises begin to bite.

The extraordinary stimulus is being rapidly drained

*Annual change in federal deficits as % of GDP, shown inverted

Despite the current highs, longer-term inflation expectations in the US, amongst both consumers and institutional investors, are still relatively well anchored at between 2% and 3%.

Whilst inflation may continue to rise through the summer there are good reasons to expect some respite towards year end providing policymakers with more flexibility of action. Comparisons with the 1970s are premature.

Rates have to rise further but could peak by the end of the year

It is now clear that central banks are willing to risk recession to tame inflation before it becomes embedded. With most countries targeting long-term inflation of only 2%, current levels of nearer 10% means there is no option but to slam hard on the monetary brakes.

Only eighteen months on from when they were contemplating cutting rates into negative territory, the Federal Reserve has signalled it is aiming to raise rates to nearly 4% in the early part of next year whilst the Bank of England is expected to hike rates to nearly 3% over the same period. Even the Eurozone may see interest rates top 1%.

This pivot to a pro-cyclical policy, tightening interest rates into a slowdown, represents a regime shift from that which has persisted for over thirty years. Ever since Alan Greenspan became Chair in 1987 the Fed’s response to every period of economic or market weakness has been the application of soothing interest rate cuts; the eponymous “Greenspan Put”.

Policy makers will continue to talk and act tough until there are clear signs that inflation is being tamed. Rising rates act as a headwind for markets and growth, the question is whether applying the brakes brings the economy to a halt.

We expect bankers to be able to pause around the end of the year as inflation rolls over but that may come too late for the economy.

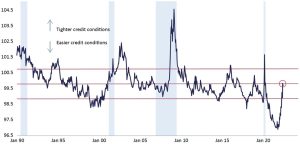

Financial conditions have swung from the loosest on history back to normal in 6 months

Source: Bloomberg. William Blair Equity Research

“Whenever I am asked whether there is going to be a recession, I always answer yes” – Howard Marks founder of Oaktree Capital

RECESSIONS ARE AN INEVITABILITY – THE IMPORTANT QUESTION IS WHEN AND HOW DEEP

Growth expectations have been swiftly reset after the breakneck speed of growth seen in 2021. The IMF and World Bank now expect global growth to be 2.9% in 2022, reduced from an expected 4.1% on the 1st January.

Economic data has weakened quickly

Note: Blue shaded areas are first half of each year.

Source: Citigroup

It is not too hard to see why. Consumers are facing a surge in the cost of basic needs such as electricity, food and fuel rather than fitness equipment and consumer electronics. Rises in interest rates have doubled the cost of mortgages in the US from a year ago impacting housing affordability.

Combined with an increasingly polarised and impotent political backdrop, consumer sentiment has plumbed record depths beyond the troughs associated with the major recessions, crises, and depressions of the last forty years.

Confidence is worse than at the depths of the financial crisis

Note: Seasonally adjusted; 1Q 1966=100. Source: University of Michigan

The data is clear. Growth is slowing across the economy whether it is consumers, services, or manufacturing. The risk of recession this year, or more likely early next, has risen even if not yet a foregone conclusion.

Irrespective of timing, downturns are not all equal. Recessions usually turn nasty when there is too much debt, particularly in private hands. That is not the case now; the ratio of US household debt to disposable income has fallen by a third since 2008.

Whilst not as buoyant as they were six months ago, consumer balance sheets are neither unhealthy nor heavily leveraged compared to previous recessions. It is still estimated that US consumers have $2 trillion in additional savings which at the very least should provide a buffer against rising costs and slowing growth.

Unemployment is near a record low of 3.6% and the jobs market is showing a significant surplus of job openings to those looking for work. This should support wage growth particularly amongst the lowest skilled.

Whilst companies carry more aggregate debt, their assets are also larger and balance sheets are in decent shape. Leverage is low and interest cover is high meaning that businesses should be able to weather a more difficult economic environment and higher rates.

A recession does not automatically mean a depression and the absence of the structural imbalances evident in prior deep drawdowns means that there is reason to believe any slowdown ahead could prove shallow.

China offers a potential positive surprise. The Zero COVID policy has been a huge headwind for the world’s second biggest economy. With President Xi Jinping recently reiterating the 5.5% growth target for his economy this year, to get there will require substantial support and stimulus. With low inflation and interest rates higher than in the west there is scope for action. A resurgent China would be an economic bonus for the rest of the world.

IT’S All about earnings

With valuations having adjusted down to more attractive levels the future direction of equity markets will be determined by the outlook for and delivery on corporate earnings.

Despite the upheaval of the last six months, analyst expectations have remained resilient and still point to growth this year and next. This seems optimistic and the coming corporate earnings season will be vital in underpinning the benign view of analysts or otherwise.

We are more cautious. The combination of rising input costs and slowing growth suggests that aggregate earnings estimates are too high. Even in the event of an economic soft-landing we would expect to see management teams guiding down estimates as historically high profit margins come under pressure and outlook statements are laced with caution.

Falling earnings expectations and heightened risk aversion means that the immediate outlook for equities is challenging and current volatility will persist. However, we have already seen a significant move lower.

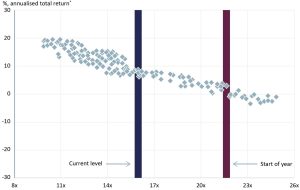

With valuations having already reset, JP Morgan’s analysis suggests markets may not have substantially further to fall even in a recession. If policy makers succeed in slowing rather than stalling the economy, then this is a reasonable level to buy. In either event, for those looking to invest for a longer period annualised returns from the current valuation level have been between 6% and 9% over the subsequent 10 years. A pretty good starting point.

Historically markets have delivered good long-term returns from here

Source: (All charts) IBES, Refinitiv Datastream, Standard & Poor’s, J.P. Morgan Asset Management.

*Dots represent monthly data points since 1988, which is earliest available. Past performance is not a reliable indicator of current and future results. Guide to the Markets – UK. Data as of 30 June 2022.

As focus moves from macro-economic headlines to corporate earnings, we expect to see individual company fundamentals have a greater determination on share prices and with it the potential for better businesses to deliver better returns. Whilst no company is immune to a recession, we have targeted businesses with characteristics that should allow them to navigate any economic troubles ahead:

- Pricing power born of market dominance, mission critical products or high switching costs.

- High margins that enable companies to protect earnings and more easily pass on rising costs

- Strong balance sheets that provide the financial resilience and ability to invest through the cycle

We have great confidence in the quality of the businesses in which we invest and the management teams that lead them. They are proven survivors through multiple environments.

Looking beyond the storm on the horizon

Markets have experienced a tumultuous start to the year with investment returns amongst the poorest on record. The potential outcome from here is far from clear, with a soft landing, recession or a period of recession with high inflation (stagflation) all possible over the next twelve months. We lean towards a recession but not a deep one, with the stagflationary outcome still the least likely.

We are still living with the reverberations of the COVID crisis even if they are less apparent which leaves the world vulnerable to shocks. With global energy markets particularly fragile, any further disruption would be damaging.

Given that vulnerability, diversification is vital to ensure portfolio resilience. We have been busier than usual over the past six months, with changes aimed at building a degree of insurance into portfolios against the twin risks that inflation proves more persistent, or that economic growth proves less robust. Gold, index-linked bonds, commodities, and real assets such as infrastructure all proved helpful in the high inflation/volatile growth environment of the 1970s.

Importantly, market challenges bring opportunities as well as risks. With asset prices having materially reset, prospective returns are now more attractive across equities, bonds and corporate credit. This gives us greater confidence in returns over the next five years even as there remains little visibility over the coming months.

For illustrative purposes only and should not be construed or relied upon as advice.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.