29.11.2016

Is it time to shelve bond proxies?

Rosie Bullard, Partner, Portfolio Manager

Rosie Bullard

Bond proxy stocks have had a great run but have faltered lately. Is it time for a return to value? Portfolio manager Rosie Bullard looks at the numbers and offers some warnings for investors tempted to over-react.

They’re some of the world’s best known brands – Guinness, Gordon’s, Dove, Hellmann’s, Fairy and Gillette. The companies behind them have a reputation for delivering predictable and stable returns with attractive, growing dividends to shareholders – characteristics similar to those of bonds. As a consequence these stocks have earned the soubriquet “bond proxies”.

In the wake of quantitative easing, as returns on bonds have become squeezed, investors have turned for comfort to these shares, which at one point were offering something like five times the yield.

For those who bought early and rode the wave (and we count ourselves among that group), the results have been impressive. Yields have compressed subsequently – the average price to earnings ratio for the MSCI UK Consumer Staples Index (representing one of the key bond proxy sectors) has risen to 25x with a yield of 3.0%.

More recently however, the mood has changed. Economic recovery appears to be gaining pace and the recent move in the bond market shows that interest rates are expected to rise (and, as we said last week, Trump’s victory makes rising inflation and interest rates more likely still). With bond prices falling as investors get possibly over-excited by the prospect of Trump bringing growth, inflation and faster normalisation of rates, then bond proxy stocks have shown signs of selling off.

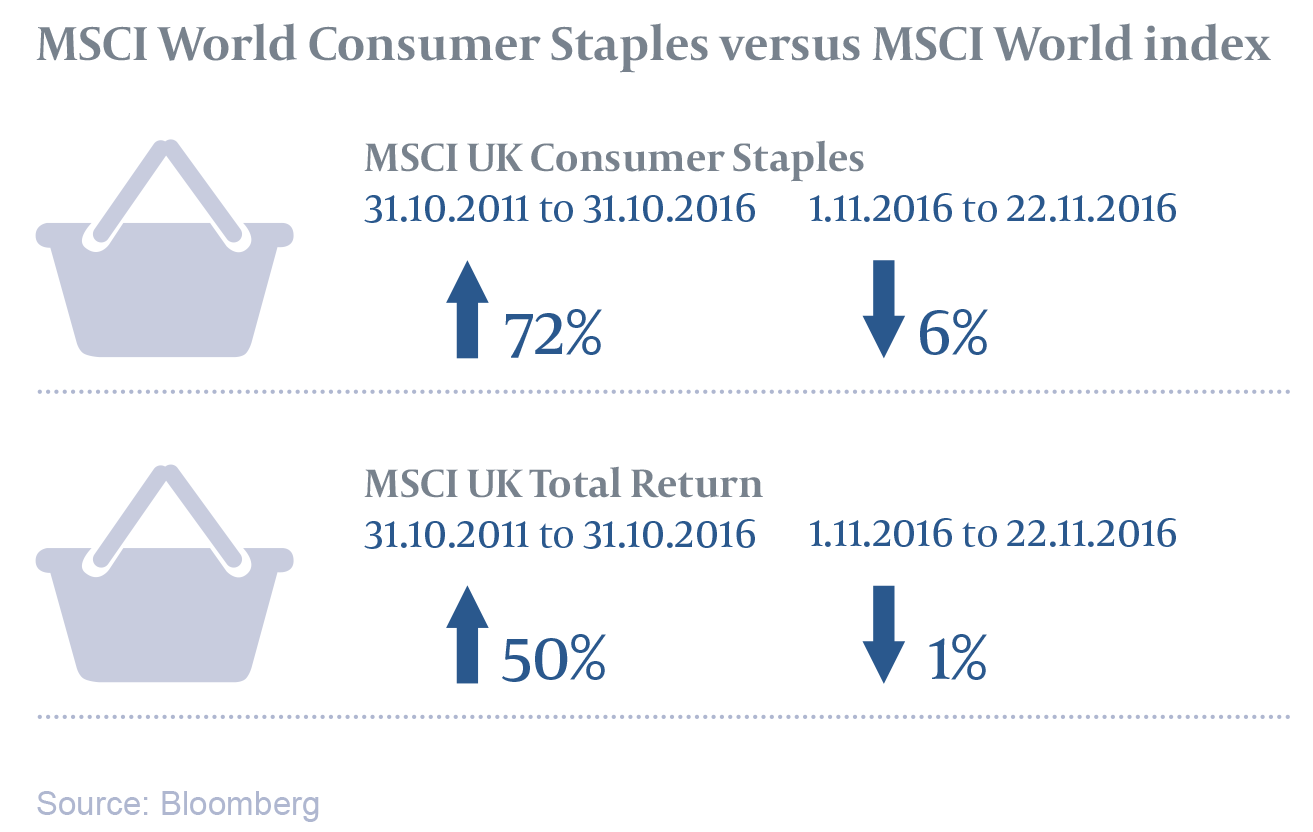

For the five-year period to 31 October 2016, the MSCI World Consumer Staples index total return was 72% versus the MSCI World index total return of 59%. For the UK, this was even more pronounced with the MSCI UK Consumer Staples index returning 82% compared with the MSCI UK Total Return Local index of 50% over the same period. However, since 1November 2016 to date (22 November 2016), the MSCI Consumer Staples sector has fallen 5% versus the wider market up marginally. Meanwhile in the UK, the MSCI UK Consumer Staples index return was down 6% vs the market off just over 1%.

So it may now be the turn of value stocks to shine and suddenly investors are spotting bargains.

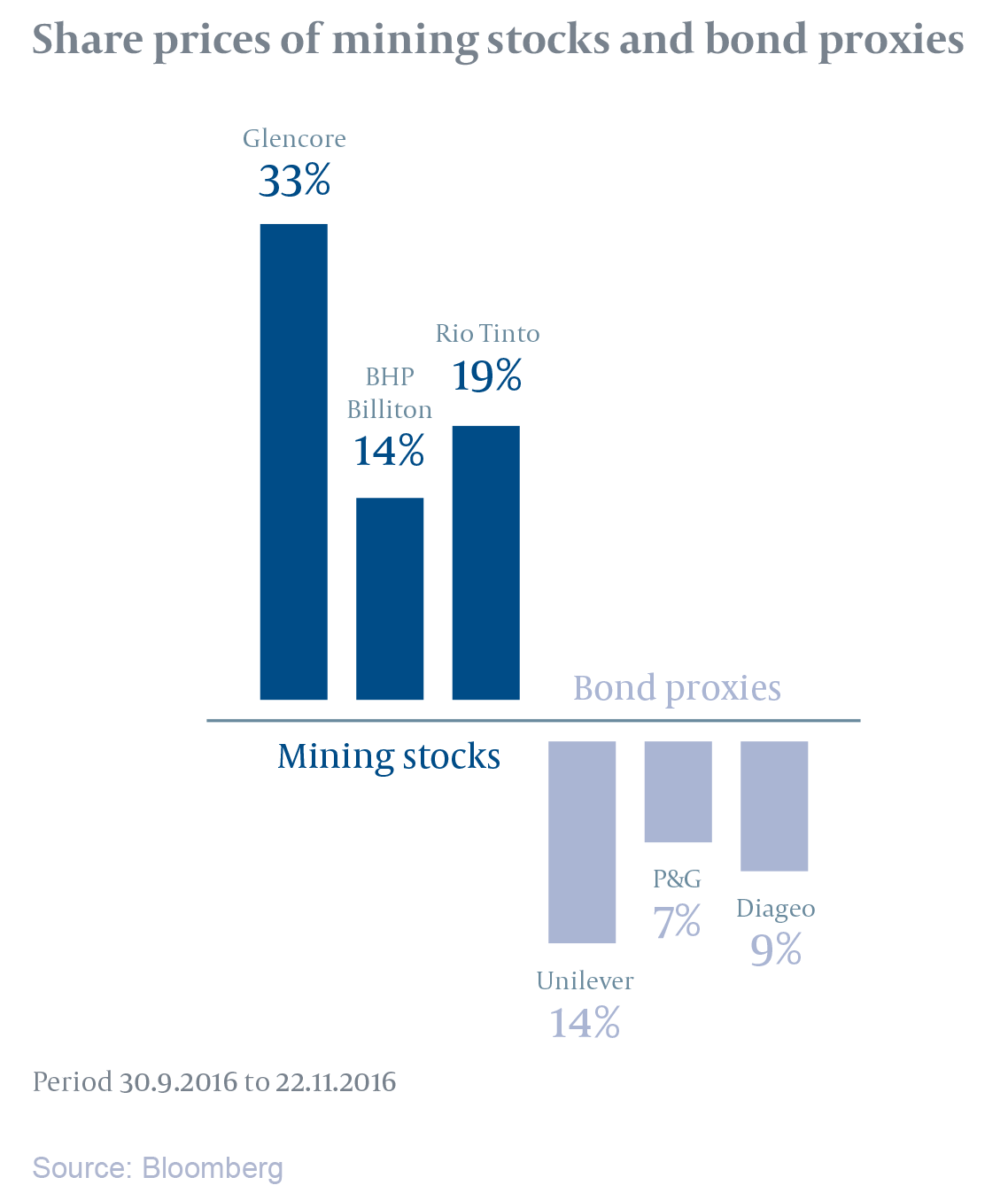

Since the end of September mining companies Glencore (up 33%), BHP Billiton (up 14%) and Rio Tinto (up 19%) have seen their share price rise. Financials like HSBC, JPMorgan and Prudential have all enjoyed post-Trump rallies too. Meanwhile, Unilever (Dove and Hellmann’s) is down 14%, P&G (Fairy and Gillette) is down 7% and Diageo (Guinness and Gordon’s) down 9% in local currency terms over the same period.

Where does this leave investors? We had begun tilting towards value some months ago and portfolios have benefited.

Does that mean abandoning bond proxies? Far from it. If this year has taught us anything it is to expect the unexpected. A good portfolio is a balanced portfolio.

We are long-term investors and many bond proxies have all the characteristics you want in a company – visible cash flows, balance sheet stability, attractive products and good management teams. They remain good defensive holdings.

Remember two things: “markets have a tendency to overshoot” and “it’s all about the entry price”. Keep your eye on those bond proxies. There may be some buying opportunities in the weeks to come.

Image: Graham Corney/Alamy Stock Photo

You should not act on this content without taking professional advice. Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made of given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions.

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. Fluctuations in interest rates may affect the value of your investment. The levels of taxations and tax reliefs depend on individual circumstances and may change. You should be aware that past performance is no guarantee of future performance.