CALMER WATERS BUT NOT YET CLEAR SKIES

The calmer waters we anticipated three months ago have largely materialised, allowing asset markets to chart a steady course through the summer as turbulence subsided. The capacity for political dynamics to shock has proven much reduced, particularly as to date they have shown few signs of blowing the economy off course or causing lasting damage. The feared economic squall of stagflation has seemingly been avoided.

Markets have responded positively, buoyed by robust corporate earnings and renewed enthusiasm for artificial intelligence (Al), where the initial existential concerns around DeepSeek have given way to a snowball of spending one-upmanship.

Yet, beneath this surface calm, many of the underlying issues remain unresolved. Trade tensions persist, geopolitical flashpoints have intensified, and political dysfunction continues to plague major economies, from Japan and France to the increasingly polarised United States.

In the face of this, the US economy remains a testament to resilience, growing at an annualised rate of nearly 4% in the three months to July and showing strong momentum into the second half of the year. This pace could continue, particularly if major geopolitical and policy risks recede, allowing already announced interest rate reductions and fiscal stimulus to take effect by 2026.

Markets are increasingly pricing in such a benign outcome. We think that they could very well be right, but things could change quickly given the unpredictable nature of policy, the spectre of tariffs and signs of exuberance in the technology sector.

Looking further ahead, events this year continue to reinforce our conviction in the structural trends shaping the post-COVID investment landscape. These themes remain central to our long-term portfolio strategy and asset allocation thinking.

THE SORT OF CALM AFTER THE STORM

Results for the third quarter were broadly positive, delivering a sense of much needed stability. The market narrative followed a well-established pattern: equities outperformed, while government bonds offered minimal excitement, and the diversifying benefits of gold shone through. Regional and sector leadership remained consistent. The US market continued its dominant run over Europe, with technology stocks well ahead of more defensive areas like staples, healthcare and utilities.

The notable exception was a resurgent Chinese stock market. This follows a moribund five years in which it was largely shunned by foreign investors, frightened off by poor economic performance and rising government interference in the private sector.

With many investors’ nerves shredded by the events of March and April, the summer months were always likely to prove important for setting the direction for markets for the rest of the year. They provided the first hard data to assess the real-world effects of the Trump Administration’s trade and economic policies.

”Tariff wars are good and easy to win” or so was the opinion of your favourite President. The jury remains out on both statements. What is clear, however, is that the direst predictions of economic fallout have not materialised. The anticipated stagflationary shock has failed to emerge as growth has rebounded, consumer spending remains resilient and inflation has been largely contained.

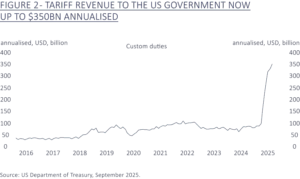

Meanwhile, US budgetary coffers have begun to swell with tariff receipts, providing a degree of fiscal cover for the impending tax cuts and domestic support programs enshrined in the flagship ”One Big Beautiful Bill Act” that passed through Congress in July.

Corporate earnings, in the US at least, have also proven more resilient than many feared. Company earnings reports through July and August revealed aggregate earnings grew at 11% on the prior year, with the sharp fall in the dollar proving a tailwind for the profits of US multi nationals. Projections for 2025 and 2026 are that US company profits will grow by more than 10% in both years, a healthy rate consistent with a still thriving economic and business environment.

With each positive data point, the trauma of ”Liberation Day” has faded further in the memory. The US dollar has stabilised, government bond yields have moderated and predictions of the end of US exceptionalism have become fewer and further between.

March’s hopes of a European resurgence have faded, undermined by flatlining growth, more political dysfunction in France and a realisation that recent promises of fiscal activism still remain more rhetoric than action. Reports of the death of US exceptional ism now look premature; as we pointed out, the structural advantages the US possesses will not be ceded quickly.

AI: BUBBLING AWAY BUT NOT YET BUBBLING OVER

The relative calm of the past few months has allowed technology, specifically Al, to resume its place at the apex of investor excitement.

Technology is now operating at a trillion-dollar scale, with the largest firms increasingly measured in thirteen digit valuations. Ten companies have surpassed the $1 trillion mark, and the market capitalisations of giants such as Nvidia, Microsoft, Alphabet, and Amazon now rival – or exceed – the annual GDP of most G10 economies. For context, the UK’s GDP stood at $3.6 trillion last year.

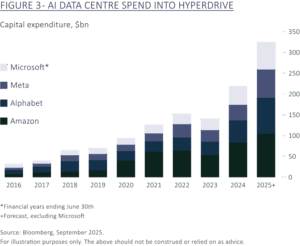

Words of caution following the revelation that China’s Deepseek had managed to match American Al models on a relative shoestring have been drowned out by a crescendo of escalating capex announcements from leading technology companies.

Data centres now sit at the heart of the AI investment cycle, providing the critical infrastructure needed to train, deploy, and operate increasingly advanced AI systems. Realising AI’s full potential will depend on the continued expansion of this backbone.

There is little sign of a slowdown. Capital commitments to data infrastructure have grown steadily throughout the quarter, culminating in Oracle’s results, which included over $300 billion in new data centre contracts signed with just three partners. The announcement sent Oracle’s shares up 40% in a single day, adding more than $100 billion to the net worth of founder Larry Ellison.

The scale of investment is unprecedented. In fact, in the first half of this year it is estimated that Al spending will have been a larger contributor to US GDP growth than even the powerhouse US consumer. According to economic and strategy house TS Lombard, capital expenditure by Apple, Amazon, Meta and Alphabet in Q2 alone was the equivalent of 1.2% of US GDP, placing it alongside historic investing booms such as US shale oil, the 1990s fibre network build out and the railroad expansion of the 19th century.

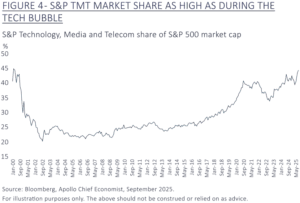

This tsunami of spending has been mirrored in a sharp rise in the share prices of technology companies, particularly those with direct exposure to AI. Technology, Media and Telecoms (TMT) companies now represent as much of the US stock market as they did at the peak of the technology and telecoms bubble in 2000.

The rapid acceleration in Al infrastructure investment – alongside soaring share prices and increasingly interlinked commitments among dominant players – has understandably raised concerns about a potential bubble. Valuations are certainly high, leaving little room for disappointment, and Al remains in its early stages, with the commercial returns and productivity gains from this wave of investment still largely unproven.

We acknowledge and share these concerns regarding the path to sustainable returns on investment. While we maintain meaningful exposure to this dynamic and potentially transformative area, we have been careful not to let it dominate portfolios. Diversification remains a core principle of our investment approach.

Comparisons with the late-1990s dotcom bubble are inevitable, but there are important distinctions. The first is that valuations, whilst high, remain below the extremes of March 2000 when Qualcomm traded at over 500x earnings and Cisco at 200x, nearly four times that of Nvidia today.

Much of today’s investment is also internally funded by the sector’s largest and most profitable companies. Nvidia, for example, has no net debt, and many of its peers are in net cash positions. This contrasts sharply with the highly leveraged telecom and fibre buildouts of the early 2000s.

Finally whilst spending on Al has surged, it has not yet reached the sustained, multi-year deployment seen in the late 1990s, when tech capital expenditure rose by over 20% annually for five consecutive years.

Sentiment and enthusiasm for AI are undoubtedly extended and valuations look full. Signs of excess are emerging, although today these are more akin to the speculative venture capital environment of 2021 than the dotcom mania of 1999. This leaves the technology sector, and by extension the broader equity market, vulnerable to disappointment. However, vulnerability to a setback is not the same as the systemic risk of a full-blown bubble imploding.

THERE ARE ALWAYS RISKS, AT TIMES THEY ARE BETTER MANAGED THAN AVOIDED

The relentless news cycle, unpredictable policy shifts, and Al-driven valuations represent shorter term portfolio risks. We seek to mitigate these through a combination of tactical asset allocation and robust diversification. This is risk management in real time.

That said, constantly focusing on short-term risks can obscure some of the more enduring structural shifts underway. We continue to look beyond the next quarter, focusing on the long-term forces shaping government policy, corporate strategy, and ultimately, portfolio construction. In these, we feel increasingly confident.

CHARTING A COURSE FOR THE FUTURE

”Skate to where the puck is going to be, not where it has been” – Wayne Gretzky

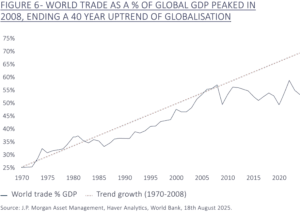

As we’ve noted in previous updates, COVID-19 served as a catalyst for a structural reset in the global investment environment. After decades of globalisation and relatively stable policy frameworks, the pandemic ushered in a new era marked by heightened volatility, disrupted supply chains, and shifting geopolitical dynamics.

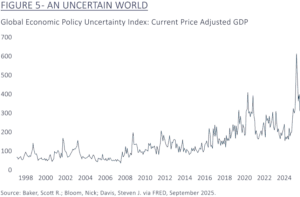

From 1990 to 2019, markets benefited from a backdrop of multilateral cooperation, low inflation, and steady growth. The major disruptions, the dotcom crash and the Global Financial Crisis, were largely the result of private sector excess. In contrast, the post-pandemic period has been defined by a sharp rise in policy unpredictability.

According to the Federal Reserve Bank of St Louis, global uncertainty reached record highs in 2020 before setting a new record earlier this year. It remains elevated. Today’s investment environment is shaped not just by market forces, but by rapidly evolving government interventions, trade policies, and regulatory shifts, with significant implications for asset allocation and capital flows.

DISCONTENT DRIVING A CHANGE IN DIRECTION

While globalisation was long associated with economic growth and geopolitical stability, its benefits were not evenly distributed. The seeds of structural change were sown well before COVID-19, with the pandemic acting as an accelerant for discontent to bloom. Since the Global Financial Crisis (ironically the high-water mark of global trade cooperation) public dissatisfaction with economic outcomes and disillusionment with political leadership have steadily increased, fuelling a broader shift in sentiment and policy direction.

This disaffection found its basis in a coalition of the economically discontent and culturally disillusioned, whose influence can be seen in a building rejection of the status quo from Brexit to the election of Donald Trump. More recently, we have seen a surge in support for more nakedly nationalist parties on the left and right which are increasingly part of the mainstream. Reform in the UK, the AfD in Germany and Rassemblement National in France each now command significant levels of popular support.

The political response, from both incumbent and disruptive parties, has been to turn inward. This shift coincides with a renewed focus on domestic security and resilience, brought into sharp relief by the supply chain disruptions of COVID-19 and the energy shocks following Russia’s invasion of Ukraine.

These forces appear deeply embedded and are giving rise to four broad, interlinked structural themes that transcend national borders:

- Economic nationalism

- Fiscal activism

- Rising capital investment

- A new technological cycle

Together, these themes are reshaping the global investment landscape. They offer a framework for understanding how capital flows, risks, and opportunities may evolve and they underpin our long term strategic approach to portfolio construction.

ECONOMIC NATIONALISM – CHARITY BEGINS AT HOME

Economic nationalism has gained significant momentum, with countries prioritising domestic industries and national security over global integration. Protectionism has found a new lease of life.

These protectionist policies disrupt global supply chains and alter capital flows. For example, foreign direct investment (FDI) inflows fell by 11% in 2024 for the second consecutive year, with advanced economies experiencing the sharpest declines. Investors face new risks, such as regulatory intervention and retaliatory measures, but also new opportunities in sectors favoured by national policy, such as domestic manufacturing and critical infrastructure.

The anticipated resurgence in European defence spending will now be more closely targeted at domestic suppliers and national champions than in the past. The likes of Safran, Rheinmetall and BAE Systems will be preferred over the large US providers such as Lockheed. European air carriers will lean towards Airbus rather than Boeing, with more engines manufactured by a regional leader such as Rolls Royce or the aforementioned Safran.

State capitalism is on the rise, from the US government taking a strategic stake in the beleaguered but strategically important Intel to China’s support for the rapid development of Huawei’s Al chips as an alternative to US rival Nvidia. Businesses will be encouraged to collaborate with domestic partners over international peers.

Economic nationalism is increasingly evident in consumer behaviour. See the collapse in the European sales of Tesla following Elon Musk’s intervention in European politics or the challenges faced by luxury European and American skincare brands in China as revealed in the slowing sales at L’Oreal and Estee Lauder.

Considerations of competing strategic national interests and economic nationalism are now an important component in any investment analysis and growth thesis.

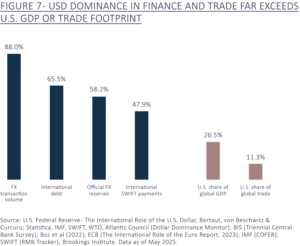

Economic Nationalism could have particularly important ramifications for the US, its bond market and the dollar. Having dominated finance and trade beyond its geographical or economic footprint even small shifts could prove profound for the US.

FROM FAMINE TO FEAST – THE REVIVAL OF FISCAL ACTIVISM

After a decade of frugality and austerity following the financial crisis, governments worldwide are now taking matters into their own hands. They have forsaken Adam Smith’s ‘invisible hand’ of capitalism and have shifted towards fiscal activism, deploying large scale stimulus and industrial policy to support economic recovery and strategic sectors.

This structural shift is evident in rising debt levels. According to the IMF, global government debt reached 93% of GDP in 2024, up from 84% in 2019, reflecting extensive spending on pandemic measures, infrastructure, and energy security. The numbers in the US and Europe look even more extreme.

Emblematic programmes like the US Inflation Reduction Act (IRA) and the EU’s NextGenerationEU fund are channelling hundreds of billions into climate initiatives, digital infrastructure, and innovation. Even Germany, historically the West’s most fiscally recalcitrant nation, has eased its constraints, signifying a widespread capitulation to activism. The US transactional trade policy serves as another mechanism to channel investment domestically, using strategic pressure rather than direct funding. Big government is back.

These programmes carry significant macroeconomic implications. While many companies stand to benefit from large-scale infrastructure renewal, the erosion of budgetary discipline raises questions about long-term fiscal sustainability and inflationary pressures. Government bonds, once a reliable portfolio diversifier, now face heightened risk.

Gold has proven a primary beneficiary of flagging confidence in government bonds, whilst other sources of balance for portfolios will be needed beyond the traditional 60% equities, 40% bonds approach. It may be that the bonds of the world’s biggest companies are seen as safer assets than those of the biggest countries.

A CAPEX SUPERCYCLE ON TECH BRO STEROIDS

The resurgence of fiscal activism is fuelling a new wave of capital investment, particularly in infrastructure, clean energy, and advanced manufacturing. According to the International Energy Agency (IEA), global investment in clean energy surpassed $2 trillion in 2024, up from $1.3 trillion in 2020. China leads in renewable deployment, accounting for nearly half of global solar and wind investment and a majority of small modular nuclear reactors, while the US and Europe accelerate their own transitions. Even as political attention shifts, the imperative for domestic energy security ensures continued investment across wind, solar, and nuclear technologies.

Infrastructure spending is also rising. The G20’s Global Infrastructure Hub projects a cumulative $94 trillion in investment needs by 2040. This extends beyond physical assets to include digital infrastructure and supply chain resilience – areas prioritised in response to recent global disruptions.

This government-led investment push coincides with a historic capital expenditure cycle by the world’s largest technology firms. These companies – effectively operating at quasi-sovereign scale – are deploying capital at levels unseen in over two decades. Their investment is reshaping energy and digital infrastructure and creating a halo effect across multiple sectors, with implications likely to extend well into the next decade.

A NEW TECHNOLOGICAL CYCLE: AI, INVESTMENT AND PRODUCTIVITY

Technological innovation is entering a new cycle, driven by Al, automation, and digital transformation. According to IDC, global spending on digital transformation is projected to reach $3.4 trillion by 2026, up from $1.8 trillion in 2022. Al adoption is accelerating, with PwC estimating that Al could contribute up to $15.7 trillion to global GDP by 2030.

The race for technological leadership is intensifying, spurring heavy public and corporate investment in R&D, semiconductors, and next-generation networks. In the first quarter of 2025, global venture capital investment in AI and automation exceeded $80 billion, nearly double that invested across all of 2023. These advances are reshaping productivity, labour markets, and the competitive landscape across sectors.

Whilst the focus is currently on Al, adoption extends much further to automation, robotics and a new productivity era. This transformation will inevitably create disruption, but it will also generate significant new opportunities, driving fresh demand for leading incumbents that control data, or are at the vanguard of automation and precision robotics.

Crucially, a sustained productivity uplift could provide the economic momentum needed to address the underlying causes of broader social dissatisfaction and political friction. Innovation is not just a source of growth; it may also be part of the solution.

NAVIGATING A NEW INVESTMENT ERA

These four structural themes – economic nationalism, fiscal activism, rising capital investment, and a new technological cycle – are deeply interconnected and global in scope. Economic nationalism is driving fiscal intervention, which in turn is fuelling investment in infrastructure and innovation. Technological advancement both enables and accelerates these shifts, as nations compete for strategic advantage.

Capital flows are increasingly shaped by these dynamics. Policy driven incentives and restrictions are influencing cross-border investment, while supply chains are being restructured for resilience and technological capability. This interplay creates a powerful feedback loop, amplifying both risks and opportunities.

The resulting investment landscape is complex. Policy volatility, regulatory shifts, trade tensions, and fiscal reversals can disrupt markets and valuations. Inflation, currency fluctuations, and geopolitical uncertainty add further layers of risk.

Yet these same forces are creating compelling opportunities. Sectors aligned with government priorities – such as clean energy, digital infrastructure, and advanced manufacturing – are well positioned for long-term growth. Investors who can identify and access these themes stand to benefit from powerful structural tailwinds.

Inevitably progress will not be smooth and events will force us to adjust course. Diversification, active management and adaptability will be important tools in protecting our clients from the growing number of extreme events and increasing risks at both tails of the economic cycle, recession and stagflation now present equal threats. By ensuring portfolios are robust and resilient we believe we give ourselves and our clients the best chance of navigating the uncertainty to take advantage of the wealth of new and different opportunities that the shifting regime will offer.

Article written by James Beck, Partner, Head of Investments.

This document is a Financial Promotion for UK regulatory purposes and is directed only at investors resident in the United Kingdom.

This document does not constitute investment advice or a recommendation.

Past performance is not a reliable indicator of future performance. The value of investments, and the income from them, may go down as well as up, so you could get back less than you invested.

This material has been issued and approved in the UK by James Hambro & Partners LLP, which is authorised and regulated by the Financial Conduct Authority and is a registered investment adviser of the Securities and Exchange Commission. It is listed in the Financial Services Register with reference number 513246. James Hambro & Partners LLP is a limited liability partnership registered in England & Wales with number OC350134 and registered office at 45 Pall Mall, London SW1Y 5JG. A list of members is available on request. The registered mark James Hambro® is the property of Mr J D Hambro and is used under licence.