Can there be anyone left who hasn’t helpfully uttered or been the red-faced recipient of that phrase over the course of the last year? It captures not only the extraordinary and unexpected change we have all experienced but also the remarkable speed and resolve with which we have adapted since last March. Forced to substitute the physical world for the digital, plenty of old dogs have proven very capable of learning new tricks.

James Beck, Head of Investments

The ability of society to find solutions through technology and medical science has meant that following the initial fear of the unknown, those parts of society and industry not rooted in the need for physical interaction have been able to find a way. Even though much of the Northern Hemisphere has succumbed to new waves of lockdowns at the coldest and darkest period of the year, ingenuity and innovation in the world of vaccines has provided hope of a brighter social and economic reality in the future.

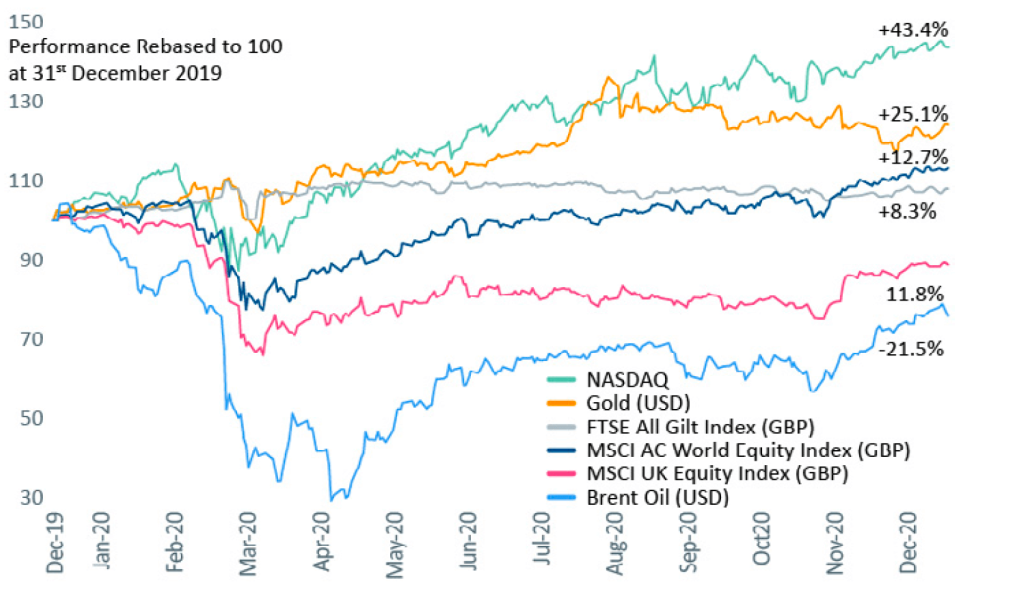

Markets predict a recovery

Given the real-world events of 2020, the headline returns across asset classes have proven extremely resilient – remarkable given the scale of market falls in the first quarter of the year and the economic damage as a consequence of measures to fight the pandemic. As recently as October, many markets remained in losing territory as a patchwork economic recovery was disrupted by second waves of the virus. The US election brought a change in The White House bringing with it fresh hope that was immediately burnished by the news of not one but three effective vaccines. Markets surged in November, delivering one of the strongest months on record and the best for the Dow Jones since 1987. This ebullience was sustained through to the end of a tumultuous year.

In local currency terms the MSCI All Country World Index ended the year up 14% while UK and US government bonds returned 8%. Gold rose by 25%, bolstered by its role both as a safe-haven and potential inflation hedge in a world of zero interest rates. There were areas of weakness, with oil declining by over 20% and the dollar falling by nearly 7% on a trade-weighted basis as investors digested the swelling of the Federal Reserve’s balance sheet, a rising US budget deficit and the fall in US real (inflation-adjusted) interest rates to levels closer to those in the Eurozone and Japan.

Regionally, China was the strongest major equity market rising by nearly 30%. Its economy rebounded so successfully that it is projected to grow by over 2% in 2020, whilst the world in aggregate will contract by more than 4%. Asian markets in general delivered strong returns, supported by their more adroit handling of Covid-19 given previous experience of airborne viruses SARS, swine flu and avian flu. The US, too, proved resilient, with the technology-focused NASDAQ index rising by a phenomenal 45%. This success was driven not just by the likes of Apple, Google and Facebook but also a raft of companies that benefited from both the necessity of staying or working from home and a forced acceleration of the transition to a digital economy in retail, entertainment, payments and enterprise.

At the other end of the spectrum were the UK and Europe, as the FTSE 100 fell 11% in 2020. It could be tempting to attribute this to Brexit, but the UK economy has materially underperformed its G8 peers, with UK GDP forecast to contract by more than -11% in 2020 (the largest drop in annual output since the great frost of 1709), well behind the Euro area (-7%), US (-4%) and OECD expectations for the world (-4%). The FTSE has also been exposed by its composition, with a high exposure to the three poorest performing sectors in 2020 – Oil, Financials and Real Estate – and limited exposure to the Covid winners of technology.

Asset returns 2020

One for the record books

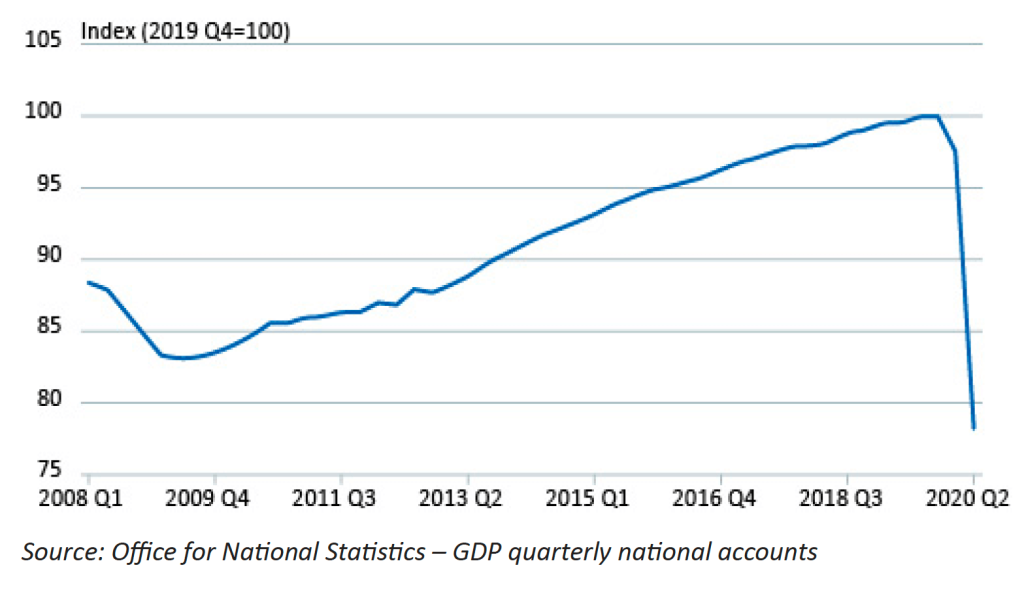

The dramatic changes wrought by the global pandemic and measures to contain it continue to dominate the day-to-day more than twelve months since reports began to surface from China. The scale of economic damage will have enduring implications for the nature of the anticipated recovery and beyond.

The abrupt shutdown of much of the global economy in March caused a colossal reduction in activity. Real GDP in the US fell in the second quarter by 31.4% on an annualised basis whilst UK GDP fell by 19.8% – in both cases the worst on record. Global trade fell by 12% in April, twice the contraction of the depths of the 2008 global financial crisis. US unemployment, having reached a 50-year low of 3.5% in February 2020, only two months later had rocketed to an all-time high of 14.7% as shutdowns led to lay-offs. Whilst this spike proved temporary, with the rate having moderated to around half the February peak, new unemployment claims continue to run at 700,000 per week and there are more than 3.5 million additional people claiming unemployment benefits in the US as compared to a year ago.

UK, Quarter 1 (Jan to Mar) 2008 to Quarter 2 (Apr to June) 2020

In a typical downturn, the economy slows before falling into recession, allowing investors to adjust to the deteriorating conditions. 2020 began with the global economy a decade into the slow expansion following the financial crisis and most economies showing few signs of either strain or excess. Stock market indices were near record highs, bond yields near lows and inflation expectations depressed.

The overnight recession forced markets and investors to tear up their projections whilst scrabbling for any indication as to the trajectory, impact and virulence of the pandemic, all at a time when they were being sent home from their desks – the result was a 37% fall in the venerable Dow Jones Industrial Average in just 40 days and the fastest bear market on record (the ‘Dow’ is a longstanding index of leading US companies). Only the crashes of 1987 and 1929 come anywhere near comparable in terms of depth and speed.

Market volatility exploded having lain dormant for much of the preceding decade, with a disorderly unwind of leveraged positions and evaporation of liquidity that briefly infected even safe-havens such as gold and US treasuries. Of the 17 biggest daily falls in the Dow over the last 124 years, 14 occurred in 2020.

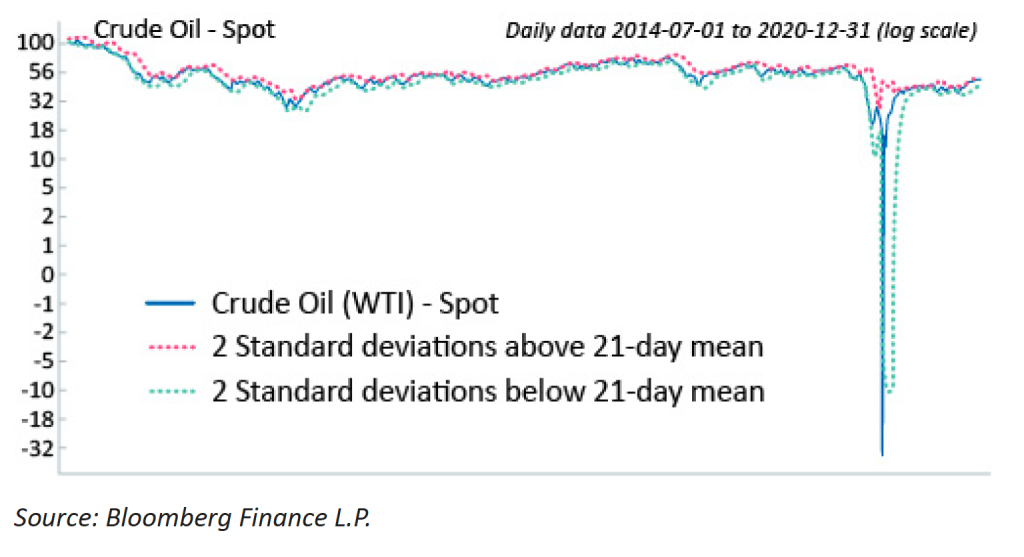

The disruption across markets prompted a complete breakdown in some areas. Nowhere was this dysfunction more evident than in the energy market. The collapse in trade, industry and travel destroyed demand, causing a glut in crude oil, with storage facilities filled to the brim. On the 20th April, the day before the settlement of oil future contracts, the already weak oil price fell to minus $37.63/barrel with counterparties scrabbling to avoid taking delivery of oil they neither wanted nor were able to store.

NY spot crude oil closed at -$37/barrel on April 20

Central bankers to the rescue again

Central bankers, led by Jay Powell and the US Federal Reserve, acted as first responders to underpin the operation of the financial system. They slashed rates to zero or below and flooded the financial system with liquidity to ensure markets and banks continued to function and have access to capital. Central banks showed their ability to adapt and to do so quickly. Financial support was stretched to companies and credit markets through a series of programmes that allowed them to buy not only government bonds but also investment-grade and even high-yield (junk) corporate debt. Through these actions central banks were able to prevent a government-induced economic demand shock evolving into a financial crisis, but it has also created an environment that will have longer-term implications for government policy and investment. They cannot have much more fuel left in the tank!

This response pushed the already low yields available on cash and bonds to trough levels as the value of bonds yielding less than zero surged above $18 trillion. This may in time prove to be the pandemic-charged end to the bull market in government bonds that started in 1980 after the late Chair of the Federal Reserve Paul Volcker’s waged war on inflation by raising interest rates to 20%. With rates now nearer zero, anyone looking to make a material long-term real return from government bonds today will need a particularly bleak view of the future.

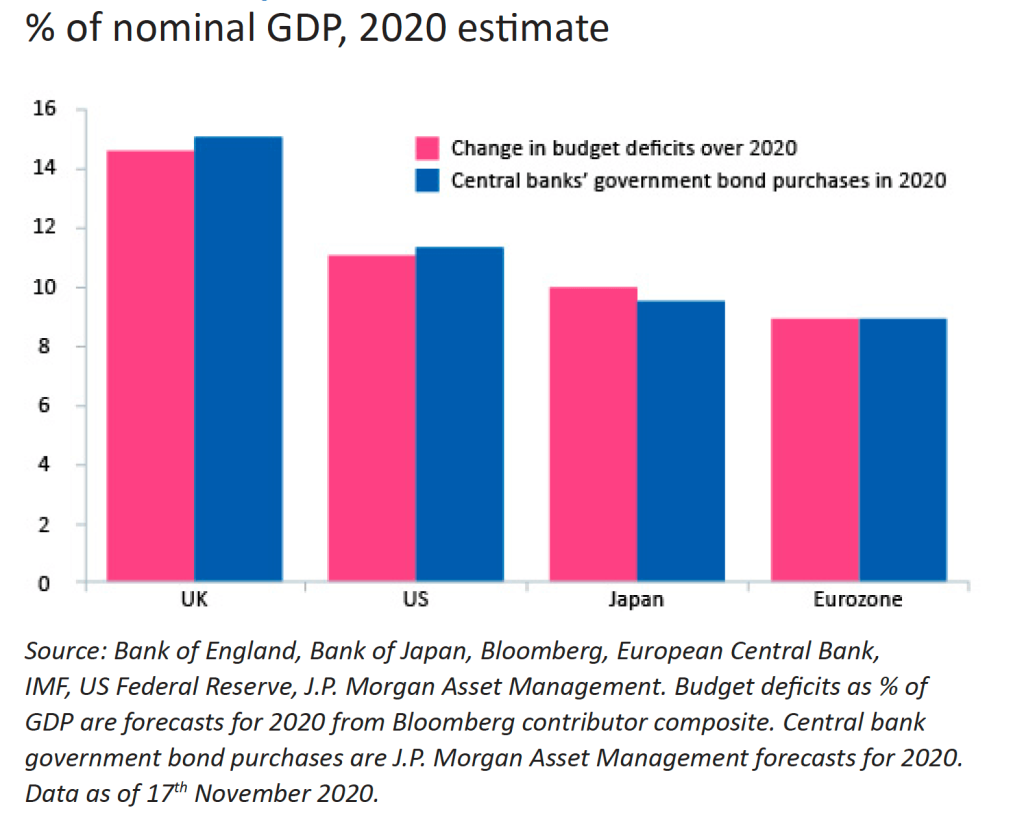

Crossing the fiscal Rubicon

If the monetary response was a dose of more of the same but on steroids, the government response represented a change in the approach of the post-financial crisis era. The mantra for much of that period was one of austerity and fiscal conservatism. Having effectively caused a recession through quarantining economic activity, governments acted quickly providing disaster relief through fiscal programmes to protect the people and businesses most affected. With every new wave and lockdown, governments have responded with additional support; in the US support programmes totalled more than $3 trillion or 15% of GDP, even before the announcement by Joe Biden that he would push for an additional $1.9 trillion in his first 100 days.

Europe has also thrown off the spending shackles with even fiscally conservative Germany providing stimulus equivalent to nearly 30% of GDP and the virus proving the catalyst for a €750 billion pan-European recovery fund borrowed at the EU rather than state level; a significant moment for the European Union as a step towards a fiscal as well as a monetary union.

Even before the crisis there were calls for governments to spend on infrastructure to stimulate tepid growth and drive a levelling-up of societies, given that the post-financial-crisis years had driven financial inequality to extremes. This explosion in spending has so far been achieved without loud cries for a balancing of the books, signs of any significant increase in long-term interest rates or the return of inflation. Almost the entire expansion in government spending last year has been funded by central banks buying government bonds. In effect a form of central bank funded government spending or what some might call Modern Monetary Theory.

Government budget deficits and central bank purchases

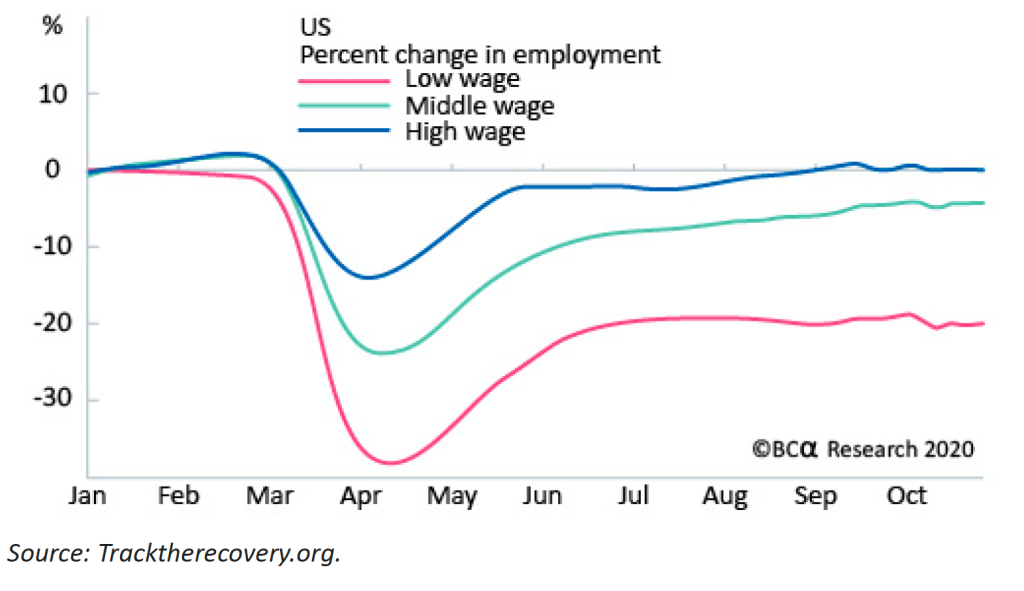

With Pandora’s box now open and the pandemic having further exacerbated inequality in society due to the outsized impact on lower-wage jobs, governments seem likely to resort to further spending to fuel the recovery once we exit this period of economic restrictions. Whilst there are valid worries around the scale of deficits and their longer-term implications, austerity is unlikely to prove palatable for some time which will have long-term implications for currencies, inflation and rates.

Unemployment still high among the poorest

“with interest rates at historic lows, the smartest thing we can do is act big”

Janet Yellen, new US Secretary of the Treasury and former Chair of the Federal Reserve

The acceleration of the electric revolution

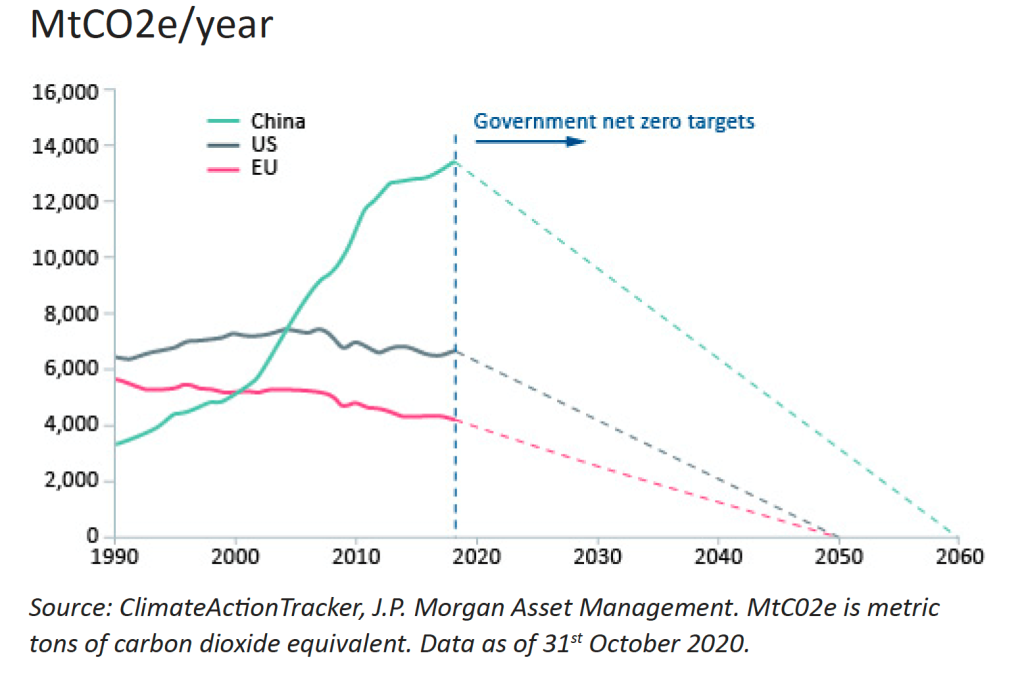

A fair proportion of any post-crisis spending is likely to find its way into infrastructure projects, particularly those targeted towards reducing carbon intensity and a transition towards an electric economy. The momentum established in 2020 as part of the response to the pandemic looks set to accelerate in 2021 as international cooperation is buoyed by the US re-joining the Paris Climate Accord and the Democrats’ stated ambition to address climate change at home. The UK is likely to be at the vanguard, at least publicly, as the host of the UN’s 26th Climate Change Conference – or COP 26 – in November. Even China surprised many by announcing at the UN a target to achieve carbon-neutrality by 2060, a vital step given China’s status as the greatest contributor to carbon emissions.

Substantial investment will be needed to achieve even these very long-term targets and efforts will have to intensify. With funding rates so low there is an opportunity for governments to use climate change policies as a means to stimulate their economies by both investing their own funds and also using the regulatory levers to incentivise private capital. 30% of the European Commission’s €750 billion flagship recovery fund is mandated to be spent on green initiatives. Likewise, 2020 saw considerable inflows to green bonds and equities focused on the transition towards an electric economy. This is likely to prove only the start of a multi-year trend that will draw in trillions of dollars in capital.

This will provide fantastic opportunities for growth, adding further structural demand to already buoyant industries such as semiconductors, which will benefit from the increased demand across the electric infrastructure. For example, electric vehicles require as much as five times more semiconductors than the petrol-powered alternative. The mining industry, which understandably sits low on many environmental scorecards, will have a fundamental role to play in the infrastructure necessary to see renewable energy supersede carbon production. We see scope for investment in established industries essential to the acceleration in growth, alongside specialist investment to gain exposure to the new technologies and companies that will naturally emerge as part of the electric revolution.

Emissions targets

Vaccinating our way to freedom

The nearer direction of markets will be dominated by the extent to which the rollout of vaccines allows a progressive reopening of economies and borders. This is essential for the economic recovery to continue beyond the initial snapback seen last year. Risks remain around the vaccines, namely their efficacy, side-effects and ability to address mutated strains, whilst the immediate outlook for economies is hampered by second and third waves of the disease. However, it is increasingly clear that a path to reopening and economic normalisation in the second half of 2021 lies ahead.

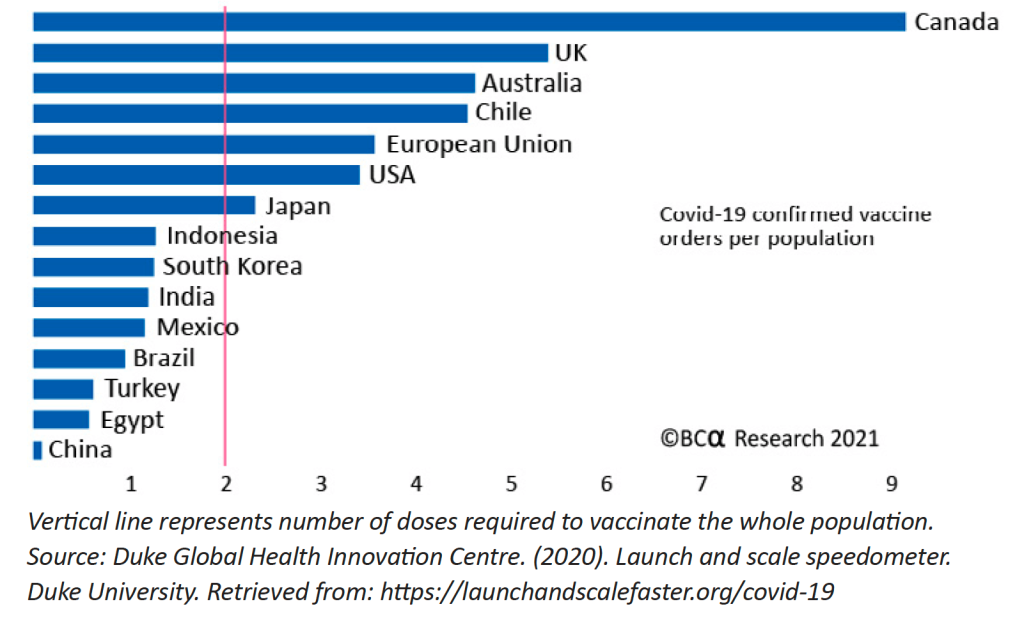

…and there are plenty of doses to go around (at least in rich countries)

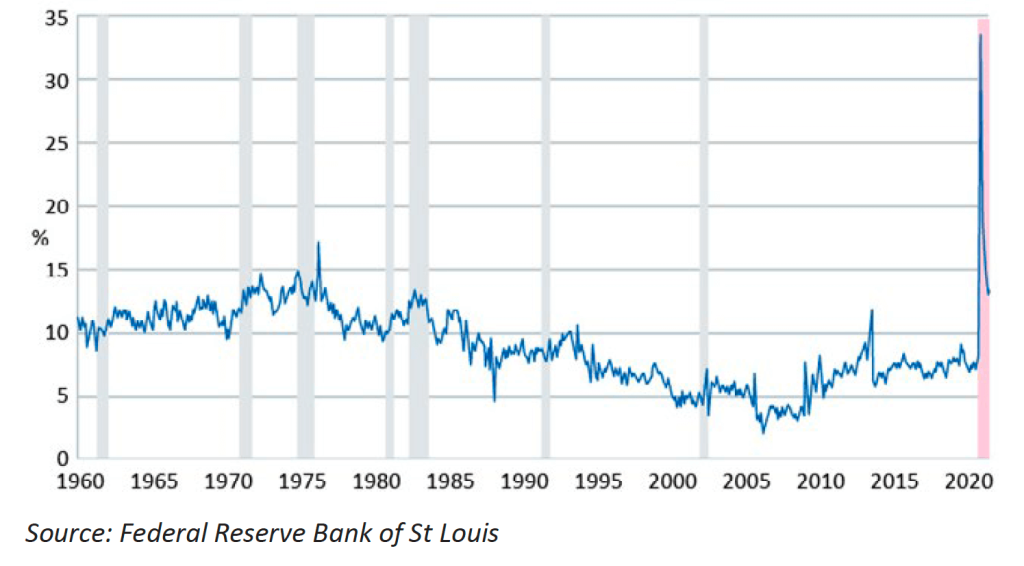

The state of consumer finances provides particular hope for the future. Household savings have jumped as both the large transfers and income support provided by governments and a reduced ability and propensity to spend have bolstered balance sheets. US households were financially healthy heading into the crisis, with debt-to-disposable-income at an 18-year low and servicing costs near generational lows. These metrics have improved further as The Fed cut interest rates and long-term yields plumbed new depths, allowing for the refinancing of mortgages and fall in interest payments. Consumer spending remains the most important constituent of US GDP, and by extension a major determinant of global growth. There is plenty of firepower to be unleashed as confidence returns and people emerge from hibernation.

FRED – Personal saving rate

T.O.W.I.E. (The only way is equities)

These dynamics of low interest rates, supportive governments and strong consumer balance sheets are likely to dictate the direction of both economies and investment markets this year and beyond. Whilst the unpredictability of the trajectory of the virus cautions against complacency, it seems likely that pent-up consumer spending power should be set free as economies open up and provide the impetus for strong economic performance as we enter the second half of the year.

A recovery in the global economy should be mirrored in corporate earnings; consensus analyst estimates forecast a 26% increase in global equity earnings this year following a likely 14% contraction in 2020. Expectations of this recovery are already partially reflected in the recent moves with share prices in many of the more economically sensitive sectors and companies having risen since the vaccines were announced in November. It is difficult to argue that equity markets are cheap in aggregate; global equities currently trade on 20 times 2021 earnings, well above the long-term median of 15 times. However, equities look much more reasonably priced when compared to the other asset classes, specifically bonds. In the US whilst the earnings yield on equities is at the lower end of its 30-year average, the difference between it and the 10-year treasury yield has rarely been wider, and, as pointed out, earnings will grow whilst bond yields will not.

For anyone looking to generate long-term growth in their investments, equities represent one of the more attractive options.

Equities look cheap – at least relative to bonds

For many companies that form the nexus of the digital economy, including the big technology behemoths, events in 2020 served to turbo-charge trends already firmly in place; proponents of the shift to the digital economy benefiting from “two years’ worth of digital transformation in two months” as Satya Nadella, CEO of Microsoft, said in April. These companies have led the market higher over recent years and remain dominant businesses still growing at incredible rates given their size. However, this is part of the challenge as they are now competing more directly with each other and their scale and dominance is attracting an increasing amount of regulatory scrutiny which will intensify as the Democrats settle into government and Europe is able to focus on something other than Covid and Brexit.

It would be extremely brave to bet against the innovation and ingenuity of Amazon, Google, Microsoft and co. but with the primary beneficiaries of economic recovery likely to be those industries that were most severely impacted by Covid, such as the leisure, travel and services sectors, 2021 could see the market leadership swing from the lockdown winners to those more geared towards an accelerating economic cycle.

Asia to take the lead?

Should we see leadership move from technology to other sectors, it is possible that we could also see change in geographical leadership from the US to Asia. The north Asian economies have been more successful in controlling the virus. Their economies are still heavily exposed to global trade and, after several years of turbulence in the shadow of US/China trade conflict, have seen a huge boost from the manufacturing disruption in the rest of the world and a global consumer who switched their spending from services to goods. China’s economic performance has been remarkable, with real GDP growing in 2020 and the economy running at an annualised rate of +6.5% in the fourth quarter.

Real GDP growth

Due to their success in controlling the outbreak, the fiscal and monetary response to the crisis was smaller across Asia, leaving central bank balance sheets less bloated and bond yields higher across Asia. China’s onshore bond market, at $16 trillion, is second only to that of the US in size, and for yield-hungry investors, their sovereign bonds, yielding above 3%, offer a real return from an A+ rated country; something available nowhere in the financially constrained developed markets.

Asian markets outperformed many developed world indices in 2020 given their economic resilience. With longer-term structural growth supported by urbanisation, a growing middle class and a transition towards more consumer-based economies, the region’s recently agreed free trade agreement should provide further impetus (the Regional Comprehensive Economic Partnership covers China, Japan, Korea, Australia as well as the ASEAN nations – which when combined are responsible for a third of global GDP). With President Trump having withdrawn the US from President Obama’s Trans-Pacific partnership, China has stepped into the breach to establish a trade zone that will eliminate 90% of tariffs on goods manufactured within the free trade area. This could deepen supply chains, and whilst China will undoubtedly benefit there may be other winners such as the world’s third largest economy, Japan, given its strong credentials in specialist manufacturing and factory automation.

One enduring legacy of the Trump presidency will be the overt expression of the strategic tensions between China and the US. Trump’s trade policy has revealed to China its vulnerability to US sanctions around technology, capital markets and the risk of holding their reserves in US-controlled dollar assets. This has prompted a drive in the development of domestic technology, semiconductor and pharmaceutical industries in a push for self-sufficiency, and may lead to an increasingly polarised world between Washington and Beijing. There will be attempts by China to develop further their capital markets and to establish the renminbi as a challenger to the dollar. An increasing share of the benefits of China’s growth and development seems likely to accrue to companies based in China and Asia, rather than those established in the West. It is a region that cannot be ignored.

First Biden then Brexit

Two big political hurdles have been cleared.

The Biden administration has been greeted with wide acclaim and relief in many areas. The return of a more conventional US to the international community is to be welcomed by those involved in trade and longer-term planning of business investment. The wafer-thin Democratic majority in both Chambers should mean a more centrist approach but also a zeal to achieve as much as possible before the mid-term elections in two years. The immediate focus will be on ensuring economic recovery, green initiatives and infrastructure, all of which have cheered markets. However, further down the line taxation and regulation are likely to rise up the agenda with negative implications.

Closer to home the eleventh-hour trade deal with the EU was greeted with understandable relief and it is at least behind us. Now begins the hard work of agreeing a route forward for the bigger services sector. There are nascent signs that the UK, having been substantially overlooked by global investors for a long time, may begin to attract more international investment. Nonetheless, with the economic situation remaining worst in class and the potential constitutional spanner of rising calls for a second Scottish Independence Referendum from May, it may be too early to sound the clarion call for the FTSE and sterling.

A return for inflation?

Given all the changes we have seen and the crossing of the fiscal Rubicon, the thoughts of some have turned to the return of inflation.

Inflationistas have been predicting its return for years, with many seeing the introduction of quantitative easing in 2009 as the catalyst. However, for those waiting for the inflation bogeyman to return, it has been more a case of waiting for Godot up until now.

Inflation is important for the direction of markets and economies, given bond yields are on their knees and much of the system and recovery founded on current ultra-low rates.

A combination of increased spending boosting demand and the subtle change in September by the Federal Reserve in their approach to allow inflation to run at higher rates before they need to begin hiking interest rates has understandably generated excitement. However, current indicators are yet to show much sign of an increase and the Fed’s move suggests they are more concerned about too little rather than too much.

It is likely that we will see a rise in short-term inflationary readings as we lap the low oil prices of last year and supply bottlenecks cause a temporary shortage of some goods. This may spook the horses but should prove temporary.

It is too early to predict whether the changes in policy will ultimately overwhelm the disinflationary forces of debt, demographics, globalisation and technology that have prevailed over the last decade. Nor do we know how much permanent economic scarring the pandemic may leave.

We have not seen inflation for a generation and investors have adapted to that reality. However, the risk is that the ultimate outcome of all the policy support is that inflation rather than growth returns with gusto. This would have major negative implications for bonds and could force bankers to raise rates too early.

For now, we are comforted by the words of the dark-suited sheriff of financial markets:

“The time to raise rates is no time soon”

Jay Powell (Chair of the US Federal Reserve

By James Beck, Partner, Head of Investments

Posted on 30 January 2021

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.

James Hambro & Partners LLP is a Limited Liability Partnership incorporated in England and Wales under the Limited Liability Partnerships Act 2000 under Partnership No: OC350134. James Hambro & Partners LLP is authorised & regulated by the Financial Conduct Authority and is a SEC Registered Investment Adviser. Registered office: 45 Pall Mall, London, SW1Y 5JG. A full list of partners is available at the Partnership’s Registered Office.