“To get there, I wouldn’t start from here.” Anon

Daniel Zegleman

There’s no place like home

When it comes to investing, people often prefer to remain close to home. This “home bias”— the tendency for investors to overweight their portfolios to their own country relative to global benchmarks – was somewhat understandable in the past when company information was not as readily available, accounting standards were less consistent and foreign transaction costs more prohibitive.

However, over time these arguments have become less convincing and, by constraining themselves to a smaller pool of potential ideas, investors risk missing out on some of the best opportunities elsewhere. The UK investment community has arguably been guilty of this in the past, with traditional portfolio allocations heavily weighted towards homegrown stalwarts at the expense of international heavyweights and faster growing developing markets.

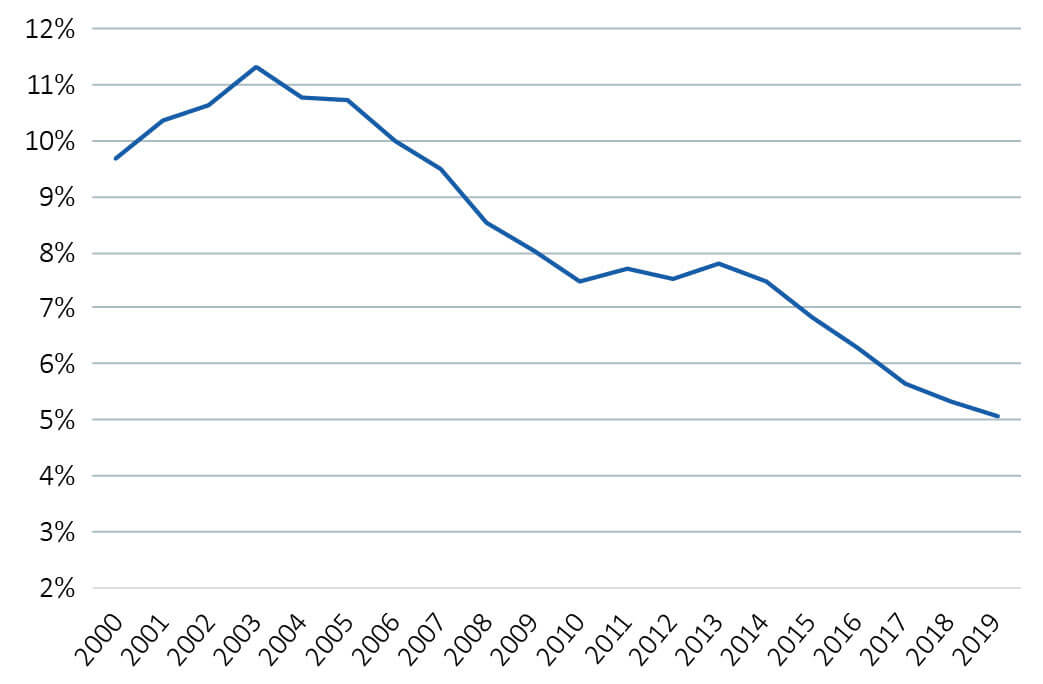

Overseas investors have been less forgiving. While remaining an important market, Figure one shows UK equities currently account for just 5% of the global index, down from over 11% in the early 2000s.

Figure one – UK weight within MSCI All Country World Index

Source: MSCI; Bloomberg

On a global scale the numbers are stark: of the 8,880 companies included in the MSCI All-Country World Investable Market Index, which covers 99% of the world’s publicly-listed companies by value, only 363 are British. The UK undoubtedly boasts some fantastic firms, but basic probability would argue there may be a few more in the remaining 8,517.

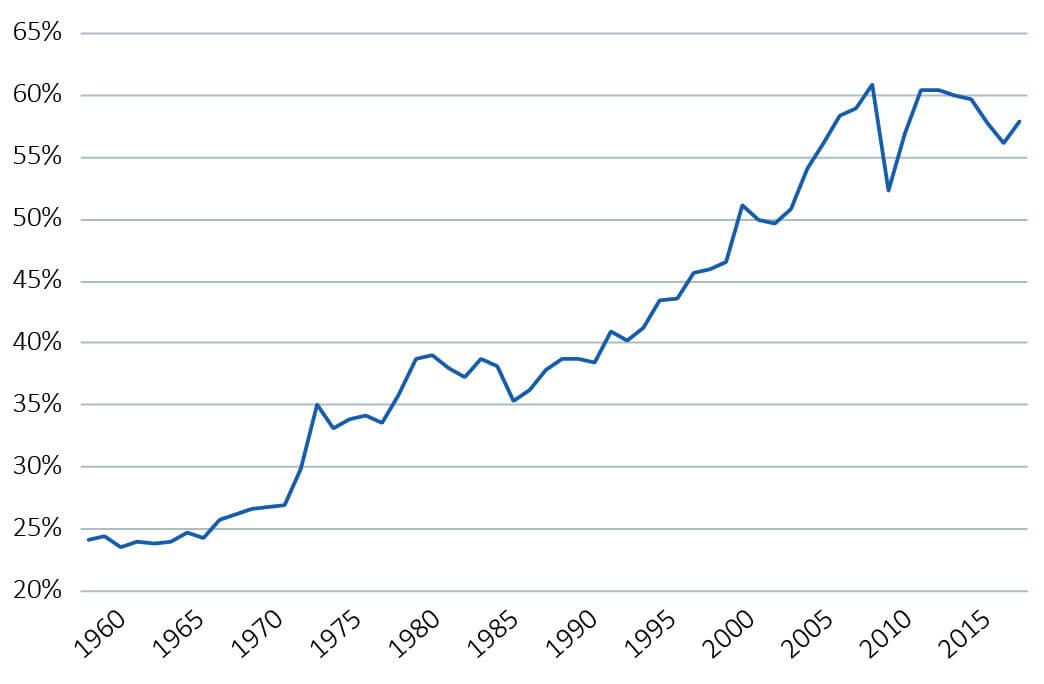

What’s more, in today’s global economy, defining a company by the country where it is based is overly simplistic. At one time, all markets were largely domestic, with business fortunes chiefly dependant on the local environment. Nowadays multinational champions such as Apple, Nike or Nestle sell products, source materials and maintain operations across five continents, while reduced barriers have facilitated a steady increase in international trade, which now accounts for almost 60% of global economic activity.

Figure two – World trade as % of GDP

Source: World Bank

Technology has made the world smaller, bringing dominant local and regional players into contact with each other on the global stage. Key investment themes are no longer confined by borders, such as demographic trends, sustainability and the digitalisation of the economy.

As companies become more globalised and financial markets more integrated, it makes sense that some stocks now display a stronger relationship with their sector, such as technology or energy, than their home country. The country isn’t irrelevant, particularly for more domestically-focused companies exposed to government policy such as in the banking or utility sectors, but for most companies perhaps it’s not the first thing we should evaluate.

Despite these dynamics, the traditional model of asset allocation remains dominant: most investors first decide how to split their portfolio across various countries, and only then how to spread investments within each country. Given the growing connection between a company’s performance and that of its global or regional sector, it seems right to question whether this remains the optimal approach.

“It is not the strongest of the species that survive, nor the most intelligent, but the one most responsive to change.” Charles Darwin

The age of disruption

In a 2018 survey of 3,600 companies, Accenture found that almost 70% of management teams expected their industry to be significantly disrupted by technology-empowered innovations in the next three years.

Of course, as any early 20thcentury horse trader would attest, disruption in business is hardly a new phenomenon. However, the gradient of any disruptive trajectory is typically tied to the pace at which the enabling technology improves – it wasn’t the invention of the automobile in the 1880s, but rather the mass-produced Model T in 1908 that signalled the end for horse-drawn vehicles. The car was the innovation, but Henry Ford’s moving assembly lines were the enabler.

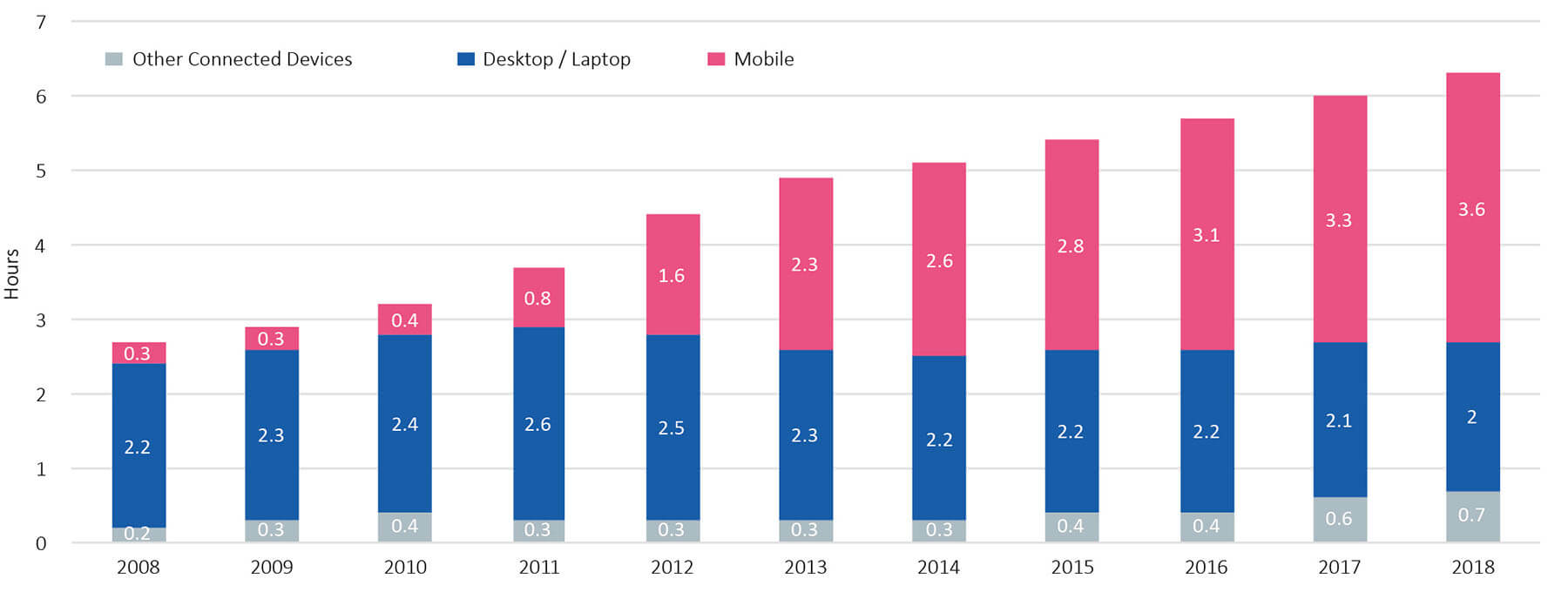

In the modern age, innovations such as the internet and the smartphone have created overwhelming amounts of data and information. Consumers and businesses can now find what they want, whenever they want it, at the best possible price. Moreover, mobile internet access has been mainly additive, rather than eating into time spent online on other devices (see Figure three).

Figure three – Daily hours spent with digital media per adult user, USA

Source: Bond Internet Trends 2019; eMarketer

This explosion of devices and applications has helped drive global internet traffic up 56-fold since 2005, a 36% compound annual growth rate, according to Cisco, a worldwide leader in IT and networking.

Still, as the dot-com crash almost 20 years ago illustrated, the data created is not in itself necessarily sufficient for lasting disruption. But recent enabling technologies of scalable computing power and rapidly advancing analytical and processing capabilities have made this information accessible as never before: the internet may have been the innovation, but the ability to harness the power of ‘Big Data’ has been the enabler. Combined, this has created a powerful cocktail for disruption.

For example, affordable targeted advertising through the likes of Facebook and YouTube has opened the door to smaller businesses looking to establish themselves in industries like food, fashion or beauty. In the industrial world, simulation and design software can be teamed with sophisticated analytics to help companies develop products faster, and at lower cost.

In the past, such productivity-enhancing tools may only have been available to those who could afford the significant up-front cost of buying computer hardware to run on-site data centres, not to mention non-stop electricity for power and a burgeoning IT team to manage the infrastructure.

However, the arrival of cloud computing – the delivery of computing services including servers, storage, software, databases and analytics over the internet – now allows companies to pay only for the resources they use, with none of the maintenance and upkeep costs. This provides the flexibility to scale usage up or down as business needs change without significant investment, and challenges traditional barriers to entry such as scale and distribution reach.

Competitors emerge from unexpected places

In addition to smaller players snapping at their heels, incumbents are increasingly being forced to contend with new competition from outside their industries. Web-based service providers can expand on a global basis at a faster rate than ever before, without having to invest in the traditional tools of the trade. Uber, founded in 2009, has become the biggest taxi company in the world without owning any vehicles, while Airbnb has grown to be the world’s largest accommodation provider in little over a decade, despite owning no property.

Amazon is the poster child of this blurring of lines between traditional industry categories. Jeff Bezos’s company is the venue for almost 40% of US online shopping, captures 10% of all US digital advertising spend and is quickly expanding into new business lines including groceries, video and healthcare. Meanwhile its subsidiary Amazon Web Services is the leading provider of cloud computing services, offering computer power, data storage and other applications that allow business of all types to scale and grow. With competitors ranging from Google to Walmart and Microsoft to Disney, Amazon can justifiably be branded a tech giant, retailer and media powerhouse all at once.

The spread of internet and digital technologies is redrawing battle lines in many markets and breaking down long-established boundaries between sectors. Accordingly, we need to ensure we enhance our approach to be responsive to these changes. By narrowly focusing on any single geographic market, or even the industry sector in which a company is categorised, investors risk ignoring the emergence of changing competitive dynamics until it is too late.

Picking companies, not countries

Over the 10 years since James Hambro & Partners was founded, our investment approach has steadily evolved to become more international in outlook, and portfolios more ‘stock-specific’ in allocation. The trends already discussed have undoubtedly been a factor, alongside the recognition that our research process was unearthing more international opportunities than UK champions among the large-cap companies in which we typically invest.

While broadening the opportunity set is a good start, navigating the seemingly accelerating pace of disruption across every sector of the market is becoming the greater challenge. At JH&P, we approach the task from two directions. First, we try to identify the ‘enablers’ – companies whose products and services are becoming more valuable, more embedded and more essential to a growing market of customers.

Examples include software and data analytics services that help clients interpret information to improve understanding of their own customers and markets, making them more productive and able to launch more compelling new products.

Likewise, in an increasingly competitive world, companies that add value for their customers by making them more efficient should continue to be well placed. This could either be through providing technologies that allow clients to do ‘more for less’ –such as solutions that save costs, enhance yields or reduce energy use – or by offering outsourced services for non-core parts of clients’ business, like catering or product testing.

Secondly, we look for companies that are well-positioned today and, in the words of acclaimed investor Phillip Fisher, “have inherent qualities making it difficult for newcomers to share in (their) growth”.

These qualities could be easily identified features such as the hundred-year heritage of a luxury fashion brand or the high proportion of recurring sales from a software subscription business model. Equally it could be a more nuanced attribute such as a low cost but essential engineering product that is difficult to replace, or even intangible qualities such as company culture or accumulated internal know-how. We think these business traits can create a set of time-tested advantages that limit the risk of disruption, even in the current feverish climate.

“Put together a portfolio of companies whose aggregate earnings march upward over the years, and so also will the portfolio’s market value.” Warren Buffett

Good companies outlast bad politicians

Populism, tariffs, trade wars: these headlines will undoubtedly affect shorter-term moves in equity markets, so we cannot simply ignore the fact we are operating in a more politically polarised world. But equally, as patient investors in companies, we must be careful not be consumed by it.

Given it is the fundamental economics of the business that will drive the bulk of stock performance as time goes by, not fluctuations in price and valuation, our time will likely be better spent evaluating the staying power of our existing and potential investments.

On that note, we were recently reminded that UK-based Prudential sold its first life-insurance policy in Asia over 95 years ago, consumer goods company Unilever was selling Sunlight soap in India as far back as 1888, and luxury goods conglomerate LVMH celebrated the 350th birthday of its Dom Perignon champagne house last year.

At a time when political views are dividing but businesses are becoming more connected, we believe taking a global view is more important than ever. By doing so, we can refocus the primary investment question away from geographic and political concerns towards a more integrated approach – aiming to identify and compare great companies that span the markets of many countries, straddle the boundaries of industry categories and outlive the sell-by date of today’s politicians.

Posted on 16th July

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.