03.02.2020

Why this bull market still has legs

James Beck, Partner, Head of Investments

“Business cycles don’t die of old age, they are murdered by the Fed or some exogenous shock” – Tobias Levkovich, Chief Investment Strategist at Citigroup

Twelve months ago, the market was in the grips of a near death experience. The US Federal Reserve’s attempts to normalise monetary policy, raising interest rates on four occasions in 2018, coincided with a global manufacturing slowdown, exacerbated by increasing geopolitical tensions, principally around trade. These factors combined to raise the looming spectre of recession.

With valuations looking stretched, particularly in the context of rising rates and higher bond yields, investors took fright and equity markets fell by 13% in the final quarter of 2018, one of the worst periods of market performance since the US Great Depression of the 1930s.

Facing a negative feedback loop of falling asset prices and deteriorating economic conditions the Federal Reserve, led by chairman Jerome Powell, offered the cycle a reprieve. Recognising the mounting risks of recession, the US central bank changed tack in what has become known as the ‘Powell pivot’.

Monetary policy and the rhetoric around it became progressively looser throughout the year providing much needed life support to the world economy, allowing financial conditions to ease and stock markets to recover in the US, Europe and across other developed markets.

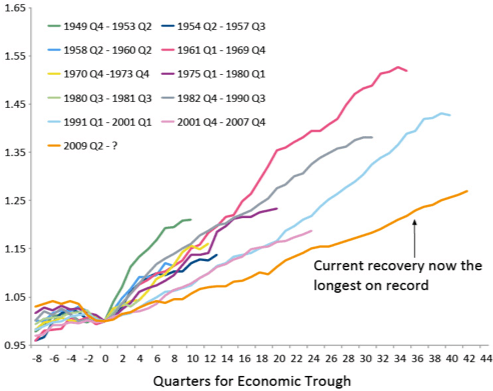

As a result, the current economic cycle is now the longest on record, but as both Levkovich, and more famously Joan Collins, suggested “age is just a number”. Despite its length the current expansion remains one of the shallowest in history (Figure 1) and there are few signs of the excesses, over-heating or dangers usually associated with the end of a business cycle.

A long but shallow bull market

Figure 1 – US GDP growth from economic trough to cyclical peak

(GDP Rebased to 1 at Economic Trough)

Source: National Bureau of Economic Research, Bureau of Economic Analysis, William Blair.

2019: from horribilis to mirabilis

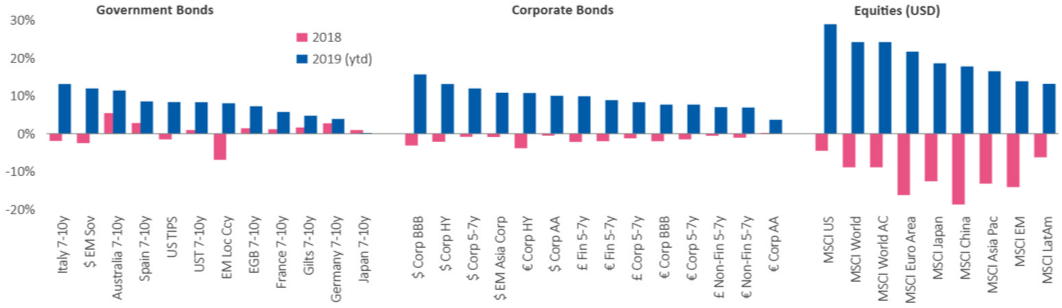

With valuations having reset lower in 2018, monetary stimulus proved to be the catalyst for strong returns from almost all asset classes in 2019 (Figure 2). Equities led the way, with the MSCI All Companies World Index returning over 23% – its best year since 2009 – driven in particular by the US and the technology sector. UK and US government bonds generated returns of over 7% in their local currency whilst oil (+27%) and gold (+18%) recovered steadily through the year.

With deposit rates and inflation below 2%, 2019 proved an exceptional year for inflation-adjusted returns: balanced portfolios produced some of their best returns in nearly thirty years.

Figure 2: 2019 – the bull market in everything

2018 and 2019 returns couldn’t have been more different. What will 2020 look like?

Source: Bloomberg, TS Lombard

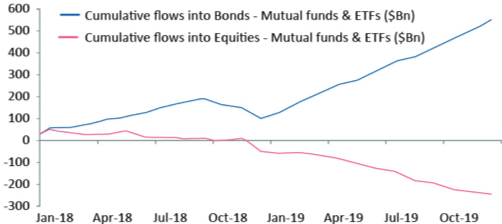

Given this strength in asset returns and the improving political noises that fuelled festive spirits, it is easy to forget the challenges faced over the year; not least in the spring and autumn when equity markets fell as trade and growth disappointments rattled investor confidence. It was as recently as September that recessionary concerns reached their peak, driving more than $17 trillion of bonds into negative yielding territory. Investors were in effect so worried that they were willing to pay governments to hold their cash.

If the early part of the recovery in 2019 was built on monetary stimulus, it was one in which few investors had any conviction given the fragile nature of the real economy. Despite rising markets, over the course of 2019 record levels of investment flowed into cash and bond funds at the expense of billions withdrawn from equities. This was in spite of the prospect of low, no or even negative returns.

Figure 3: Cumulative investment flows, 2018-19

Source: ICI

It is only more recent market moves, charged by improving economic and political expectations, that have tempted material flows back into equities. With investors having spent much of the last two years selling equities and buying bonds, sentiment and positioning is in no way complacent which should provide further support for markets.

“Trade wars are good and easy to win!”

Donald Trump

Whilst the falls in asset markets and spike in volatility may have hastened its communication, the volte-face from the Federal Reserve was largely a response to concerns over the direction of global growth given the impact of an increasingly abrasive trade conflict between the US and China.

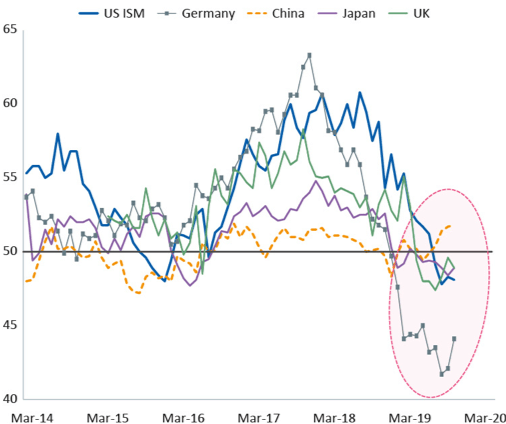

In March 2018 President Trump first turned his economic guns on China, having found his range with an aggressive renegotiation of NAFTA. Manufacturing activity had already begun to roll over as China’s desire to deleverage its economy and the collapse in the automotive sector in the aftermath of the VW emissions scandal began to pinch. However, the uncertainty caused by the trade war in the second part of 2018 undoubtedly exacerbated the downturn (Figure 4) ultimately forcing central banks to adapt.

Figure 4: Global manufacturing activity

Purchasing Managers’ Activity Indices for Manufacturing Sectors Diffusion Indices (Below 50 = Contraction, Above 50 = Expansion)

Source: Bloomberg, Markit, Institute of Supply Managers, William Blair

Having been 3% prior to the trade war, the average US tariff on Chinese goods increased from 12% to 24% in 2019. The conflict continued to escalate through much of the year with the US loudly labelling China a currency manipulator in August. The detrimental impact on trade, business confidence and capital investment was clear. Trade now represents the clearest and most immediate threat to the business cycle and investor confidence.

The pause in hostilities towards the end of the year understandably cheered investors as the US first agreed to postpone the imposition of additional tariffs in December, before the announcement by the US President of a phase one trade agreement.

The deal is good news for markets, whatever the content, building on tentative signs of an improvement in the previously weak manufacturing sector. However, it likely represents a politically expeditious ceasefire rather than the first step towards a lasting peace. We are in an election year and so Trump’s focus has turned to winning a second term; this gives us comfort that the détente should be with us until November.

Long-term, US policy towards China has fundamentally changed under this Administration. Trade is only part of a strategic struggle between two global super-powers with very different economic and social models. The US strategic objective appears to be to stem the global advance and influence of China. Importantly, this is an area of rare bi-partisan agreement between Republicans and Democrats and so we expect a resumption of tensions in 2021 irrespective of the outcome of the presidential election.

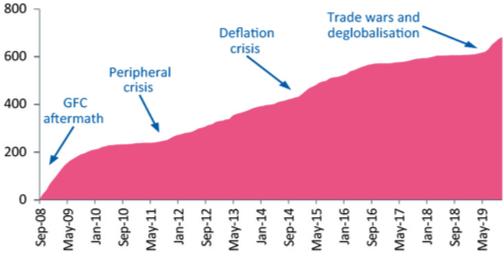

To QE infinity and beyond

More than a decade on from the Global Financial Crisis it is easy to forget the rancour and scepticism that greeted the introduction of quantitative easing (QE) by then Fed governor Ben Bernanke. An extreme response intended to rescue the financial sector in late 2008 evolved into a widespread monetary tool to stimulate the economy through lower borrowing rates and increased liquidity (Figure 5). Many commentators and economists regarded this as folly, monetary sacrilege and a one-way ticket to the hyperinflation of Weimar Germany.

Figure 5: Cumulative number of rate cuts since the Global Financial Crisis (global cuts)

Source: BofA Merrill Lynch Global Research, Bloomberg Large sample of 100+ central banks.

QE has become the defining economic policy of the decade. Adopted by central banks across the world it has already spawned three sequels in the US; the recent commitment by the Fed to buy $60 billion of short term treasuries a month is QE4 in all but name. Yet despite all the doomsday predictions global inflationary pressures remain firmly under wraps.

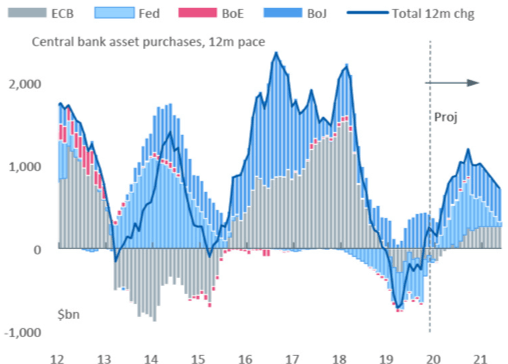

Given the stubborn absence of inflation and the cautionary example of Japan, it is likely that monetary policy will remain loose throughout this year, providing liquidity and supporting asset prices (Figure 6).

Figure 6: Central bank asset purchases are rising

Source: Central banks, TS Lombard

2020: reasons to be optimistic

In 2019 it would have taken a brave individual to predict a 20% return from equities in the face of the economic, political and social challenges faced by investors. The returns throughout the year followed the gradual improvement in many of these headwinds allowing investors to climb the proverbial wall of worry.

We begin 2020 with a more settled environment; supportive central banks, improving liquidity, abating trade tensions and nascent political progress.

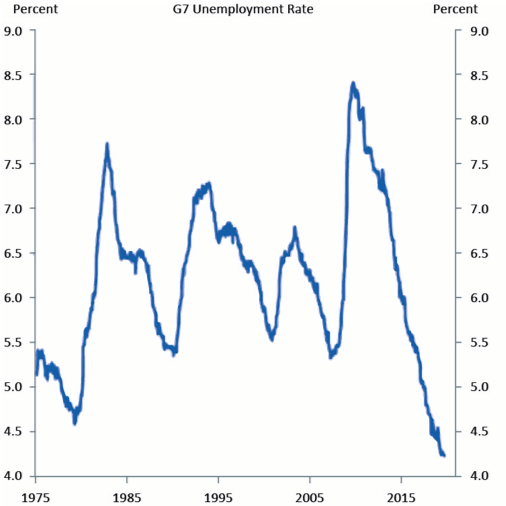

Global growth is positive, if pedestrian, and consumers are in good health, if not in a good mood. Unemployment in the G7 group of developed countries has fallen from a 2009 peak of 8.4% to current levels of a little over 4%, lower even than in 2007 (figure 7).

Figure 7: G7 Unemployment Rate

Importantly for growth, US consumers appear in particularly rude health, with unemployment at 3.6% (the lowest since 1969), wages growing ahead of inflation, and a savings rate of 7.8% that has barely been seen since the 1980s.

The strength of the US consumer and their ability to spend and support the service sector is key to sustaining the current expansion and has enabled the economy to continue to grow in the face of a manufacturing recession. Encouragingly, leading indicators are showing early signs of a stabilisation, if not a recovery in manufacturing. Should the trade truce prove lasting, we would expect to see further green shoots which would be positive for equity and commodity markets. Were this to be followed by a subsequent increase in business confidence and capital investment we would see a further impetus for the global economy and asset returns.

Some optimism is already reflected in equity valuations. However, these remain below the levels associated with previous peaks and are attractive compared to bonds. With the broader stock market having seen little growth in earnings through 2019, any pick-up in corporate earnings through the first half of this year should be sufficient to support equities.

Tensions, elections and inflation

Our expectations this year are for a period of stabilisation and modest acceleration. However, growth is low and remains fragile and susceptible to external shocks. Trade and the Middle East represent the most immediate challenges.

Whilst trade looks set to take a back seat this year, we are guarded against complacency given the volatile nature of White House policy and the President’s tendency to govern by Twitter. We remain alert to developments particularly should the US begin to focus more on Europe.

At the time of writing the Middle East is again a cause for concern. Tensions in the Middle East are not a new development for investors. Despite the headlines emanating from Iran the situation seems likely to be contained without the escalation necessary to cause an oil price shock or impact material enough to rock the economy.

The bottom line is politics now matters for investment in a way that it didn’t in the decade prior to the Global Financial Crisis, given the rise of populism, nationalism and protectionism. The US election dominates the calendar, although it is likely to exert more influence on the second half of the year. Much will depend on who wins the Democratic candidacy. Elizabeth Warren and Bernie Sanders both sit to the left and would represent a significant shift in policy towards greater regulation with serious implications for many sectors including technology, banks, oil and healthcare.

Over the last 100 years, the incumbent tends to win re-election 75% of the time. It is even rarer for a sitting president to lose in the absence of a recession during their term. On that basis, history favours Trump but as the election looms into sight we would expect markets to become more uncertain.

Further out we consider inflation to represent the clearest structural risk to the current investment cycle. Inflation has been notable by its absence for more than a decade and remains stubbornly below central bank targets. There are many reasons for this, debt, demographics, technology and globalisation to name a few.

There is a growing complacency around inflation and the prospects of its return. There are few current signs but, with the cycle built on the largesse of central banks and cheap financing, its re-emergence would represent a significant challenge.

Citius, Altius, Fortius!

As we enter an Olympic year, we are reminded of the motto of the modern Olympics – ‘faster, higher, stronger’. We think that the foundations are in place for the global economy to accelerate this year. This would undoubtedly be supportive of investment markets and strengthen investor confidence.

However, with central banks on hold, the consumer strong and geopolitical stress moderating, a continuation of the current ‘lower, slower, longer’ cycle should be sufficient to drive further progress for portfolios.

By James Beck, Partner, Head of Investments

Posted on 3 February 2020

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.