Charlotte Brayton, Financial Planner

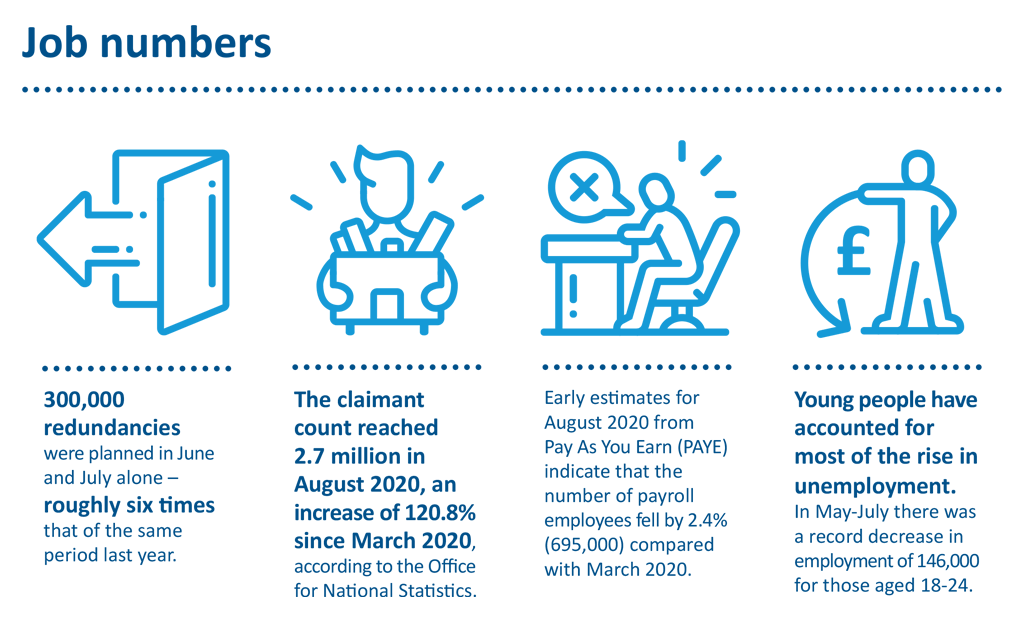

Around half a million people in the UK are expected to lose their jobs this autumn, according to the Institute for Employment Studies.

Redundancy is often a cue for writing a frenzy of job applications. Certainly, it is important for most people to find a new job as soon as possible. It is a time to contact recruitment professionals and speak to contacts you have built up over the years. It may even be a time to take that professional exam that could help your move into a slightly different role.

But it is also a time to review your financial position. If you have a financial adviser, make sure you inform them of your change in circumstances. They can help you work through a revised saving and spending strategy to keep your finances on a sound footing during this stressful period. These are some of the issues to consider.

-

Negotiate a fair exit

If you have worked for your employer for at least two years you will be entitled to statutory redundancy pay, though your employer may choose to pay above the minimum. Statutory pay is calculated based on your age, length of time with your employer and current salary. Gov.uk has a calculator you can use to estimate the amount.

Make sure your pay is fair. You may have been put on furlough prior to being made redundant, in which case you might have been earning only 80% of your regular salary. Your statutory pay must be based on 100% of your normal wage. Furlough should not affect pay during your notice period either.

Make sure your pay is fair. You may have been put on furlough prior to being made redundant, in which case you might have been earning only 80% of your regular salary. Your statutory pay must be based on 100% of your normal wage. Furlough should not affect pay during your notice period either.

Check your contract or letter of employment, which should include redundancy terms. You could be entitled to a more generous payout than you are being offered. You might even consider negotiating a better settlement than originally agreed – in which case it is worth seeking professional advice, which can be indispensable during these complex negotiations.

The first £30,000 of any redundancy payout is free of tax. If you have a particularly generous payout you may want to consider sacrificing anything over £30,000 into a defined contribution pension. You save National Insurance (NI) through salary sacrifice (12% on NI band earnings and 2% on any excess), and so do employers. They may be willing to add their own NI saving to your pension contribution, which, as it is 13.8%, can be a significant benefit. Discuss this option with your adviser and your employer. However, do remember you cannot access your pension till you are 55.

Bear in mind that pay above £30,000 is taxed at only 20% to begin with – but you might owe more. Higher-rate taxpayers are expected to settle the remaining 20% or 25% the January following the end of the tax year by submitting a self-assessment tax return. Calculate your outstanding tax and factor that into your budget before you start to spend.

-

Budget

Review your outgoings and weigh them up against your new household income. The wealthy live to the limits of their income, just as much as anyone. There are few people who would not benefit from a thorough review. If you can afford it, consider using some of your redundancy pay and savings to settle any outstanding loans and credit card debt, which can have high interest rates that compound quickly if left unpaid. (If you have redundancy looming over you, focus on paying these down now while you still have regular income.)

Go over your bank accounts and try to produce a budget. Look closely at discretionary spending and cut out waste as soon as possible.

Check your standing orders and direct debits. Small subscription payments can easily go unnoticed, but they add up. Are you paying for media services (like Sky or Netflix) that you do not really use? Do you have a monthly gym membership for a facility next to your old workplace that you will no longer visit? When did you last switch your gas or electricity provider or check if you could be on a cheaper tariff? How recently have you reviewed your car and house insurance? Are you still paying for a phone handset beyond the contract period when you could now have a much cheaper SIM-only package? These checks have been known to save some clients thousands of pounds a year.

Do you have any prepaid travel passes or season tickets for a commute you no longer need to make? In light of the current nationwide lack of travel, rail companies are accepting refund requests on passes and allowing customers to backdate these to the last use. Applications come with certain terms – for example, Transport for London requires an application within eight weeks of your last journey and you must have at least six weeks remaining on an annual ticket. Even so, railways seem to have been more compassionate than airlines.

-

Mortgage holiday

You may be worried about being able to pay your mortgage. See if you can negotiate a payment holiday or drop to interest-only payments for a while.

-

Pension pause

Generally, involvement with your employer comes to an end when you are made redundant, so employer pension contributions cease, too. There may still be retained benefits under pension arrangements, and if the pension was a Group Personal Pension Plan there may be an option for this to be converted to an arrangement in your name so you can continue to make personal contributions, subject to HMRC rules. If not then you can always open your own arrangement and contribute to that.

However, you may want to focus on putting money into cash ISAs and cash savings accounts until you have a new job. The good thing about pensions is that you can carry forward unused allowances for three years, so taking a pensions holiday and then catching up when your finances are on a sounder footing is not necessarily a problem – as long as you have the required discipline.

-

Insurance cover

Few insurance companies are still offering redundancy cover in the current circumstances, but you may have taken a policy out before the Covid crisis. Now is the time to make a claim.

Review other cover, too. Your previous job may have come with insurance benefits, and you could find yourself unprotected once you leave. Check if there is an option to convert some of these arrangements in your own name and whether it is worth doing so.

Consider your life and critical illness cover. It is tough for a family if a breadwinner is made redundant temporarily. It is even harder if they die or become so ill they cannot work.

Good luck

Redundancy is stressful, but it can often also be an impetus for positive change in your career. It can have the same effect on your personal finances if it gives you the time and motivation to have a thorough review.

By Charlotte Brayton

Posted on 14 October 2020

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document. And no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.