26.03.2020

Coronavirus update – latest thoughts

James Beck, Partner, Head of Investments

James Beck, Partner and Head of Investments

The word ‘unprecedented’ has been used so often in recent weeks that it would be reasonable to assume that even the most measured writers and commentators had succumbed to hyperbole. But it is hard not to be left open-mouthed by the scale, speed and breadth of events that we have seen across the world.

The fastest bear market of all time

Barely four weeks ago the coronavirus was deemed to be a public health emergency isolated to China, and one which was, in any event, under control thanks to the Chinese government’s ‘draconian’ response. Its impact was expected to be a temporary supply-side blip to manufacturing – only a bump in the road as the global economy continued to chug forward. Investors duly looked through the short-term implications and the S&P reached a new record closing high on the 19th February. The news that the coronavirus had been diagnosed in Northern Italy and Iran jolted markets out of their complacency.

Investment markets have since reacted with extraordinary speed. The S&P 500 has fallen by more than 30% since, entering a bear market in little more than three weeks, faster than in any previous crisis. Almost all other equity markets have fallen by similar degrees if not further. The price of oil is down 60% this year, whilst moves in corporate credit and high yield bond markets are reminiscent of the depths of the financial crisis in 2008. Though some of these moves reflect investors attempting to discount the risks of future economic weakness, others are a consequence of the fast-moving, interconnected and algorithmically-driven nature of modern markets.

The conventional response we would expect to have seen, given rising risk aversion in the last three weeks, would be for investors and banks to look to raise cash by selling riskier assets like stocks, high yield bonds and emerging market debt before buying safe or protective assets like Gilts, US Treasuries and gold. This was exactly the pattern at the beginning of March, with gold strengthening and the US 10-year Treasury yield falling to a low of 0.5%, as the price of US government bonds rose. However last week saw a particularly dysfunctional environment, with falls in all assets, including previous safe havens, coupled with wild intra- and inter-day swings in prices. Such moves were symptomatic of market panic and mass deleveraging by hedge funds and other systematic strategies. This has proven to be the case in previous episodes and there are encouraging signs this week that this indiscriminate activity is subsiding.

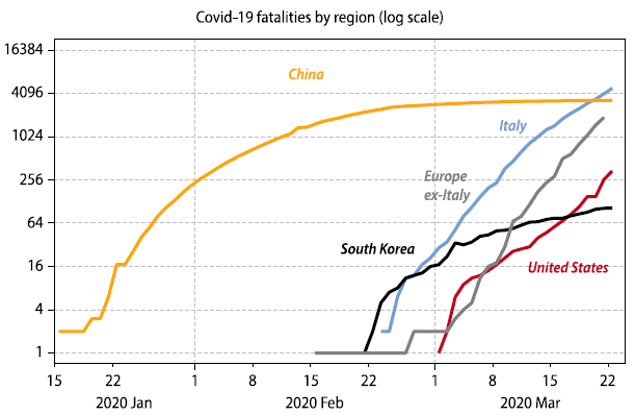

The adjustments in markets have widely tracked the progression of the coronavirus through Europe and into the US. The 100th confirmed case in Italy was only reported on 23rd February but the tally now stands at nearly 70,000 cases – and rising – with 6,900 deaths. The number of cases worldwide has also surged and has exceeded 400,000 as the outbreak has officially become a global pandemic. The World Health Organisation (WHO) believes that the spread and impact are still accelerating.

The cost of containing the outbreak

We now all know that the virus is potentially fatal, particularly to the older quartile in society and those with existing medical conditions. The original consensus that the progression of the virus in Europe might be modest and manageable has been rendered obsolete by the experience of Italy, where the trajectory of the spread of covid-19 now looks more like that seen in Wuhan province. In hindsight, Italy was badly exposed as compared to the rest of Europe. Its median age (>47), percentage of population over 65 (23% vs 19% in the UK) and under-provisioned healthcare system, when combined with a social system in which over 60% of adults under 35 live with their parents, has left it particularly vulnerable to the coronavirus. Spain shares many of these characteristics and there the trajectory looks similar, albeit ten days behind Italy.

The spread and impact of the virus in Europe and the US show few immediate signs of slowing and, as a result, the response of authorities in each country is becoming increasingly severe. The response in the UK has been more measured and graduated than elsewhere in Europe. We understand that the government has sought initially to build up a degree of immunity but has become incrementally more restrictive as the stress in the NHS built whilst pockets of society failed to sufficiently adhere to the policy of social distancing. The UK is now subject to the same social lockdown measures being implemented in Europe and across several states and cities in the US, including New York and California (effectively the world’s fifth largest economy).

From an economic perspective, this is effectively a natural disaster (although the populist US president has alleged that the virus comes complete with the stamp “Made in China”). But unlike the localised impact, both physical and economic, of an earthquake, hurricane or typhoon, the potential devastation caused by covid-19 is truly global. The social measures that governments have taken to lessen the human cost inevitably come with economic consequences. Political leaders from Macron to Trump to our own Prime Minister have drawn parallels with wartime. Whilst the social impact cannot be anywhere near comparable, the immediate economic impact may be similar; JP Morgan estimates that in the second quarter of this year we will experience the sharpest decline in Gross Domestic Product (GDP) since World War II.

The understandable measures being introduced to slow the spread of the virus and protect the integrity of our healthcare service have the side-effect of an immediate economic impact. For some businesses economic activity has stopped dead. Many are in the services sectors which dominate the economies of the US, UK and much of mainland Europe. Data from T.S. Lombard economists estimates that in the US, ‘social distancing’ has shut down industries that account for about 30% of private sector jobs (35 million). Just food services, recreation, air travel and casinos alone account for 11.6% of private sector employment and 8.4% of consumer spending in the US. There will be a large increase in unemployment and we will see the first of a number of weak statistics when the US announces weekly jobless claims later this week. More will follow, much as they did in China. The economic and corporate news emerging in the coming weeks will be shocking and we should be prepared for that. Early estimates of Purchasing Manager Indices (indicating the state of the manufacturing sector) for March reported in the Eurozone and UK yesterday are already reflective of the Global Financial Crisis lows.

Whilst we acknowledge that the immediate impact of the coronavirus induced shutdown will be huge, with the Western world effectively shut, it need not be long lasting or permanently damaging. In that regard the current crisis could come to resemble a sharp shock rather than the long, protracted slowdowns associated with cyclical and structural recessions and bear markets. Whether it does or not will depend principally on two things:

- How long will the lockdown last?

- What lasting damage will be done?

How long will the lockdown last?

The answer to the first question will be determined by the progression of the virus together with government responses. This is a health crisis first, not a financial one, and so the seeds of the recovery will be sown in stabilisation or solution to the spread of the coronavirus. Here, much focus will be on Italy as the patient zero in Europe and the first to implement a lockdown. Italy is approximately two weeks ahead of the UK and a further week or so ahead of the US, any signs of success and control within Italy would provide encouragement of a similar prognosis elsewhere and provide the first indications of a path to normalisation. There is still a belief that as the spring moves to summer the coronavirus should be subject to similar seasonal patterns as other respiratory viruses such as influenza.

What of a medical solution? This need not be a vaccine, although in the long term that would provide the most effective protection against the risk of secondary waves, given that the policy of lockdown and social isolation means that the population will have yet to build up herd immunity. If severe cases could be treated more effectively then there would be less need to keep the working population under lock and key to protect people and the healthcare system. China has reported that Avigan, a Japanese flu drug, has exhibited some efficacy whilst hydroxychloroquine has also been cited as a potential treatment. The news on Remdesivir, a drug originally developed by US-based Gilead Sciences to combat Ebola, is encouraging: trial data from China is expected in early April and the FDA has given Remdesivir ‘orphan drug’ status for covid-19, easing the path for regulatory approval should early data suggest efficacy. Any sign of progress here would be well received by markets.

A vaccine in full production is some way off, but the first genome sequence of covid-19 was published on 10th January and hundreds of scientists worldwide will be working on a solution. Suppression strategies can only work for so long before democratic governments will need to have an exit strategy as the potential human cost does not warrant a government-enforced depression. Whilst conscious that correlation is not causation, the chart below illustrates how the fall in the S&P 500 Index maps against the surge in reported cases of covid-19.

What lasting damage will be done?

If the length of the lockdown is to be determined by a combination of medical progress and government decision-making, the scale of the lasting economic damage will be determined both by how quickly things return to a semblance of normality and the response from governments and central banks in doing whatever it takes to protect the functioning of markets, businesses and the financial wellbeing of companies and people for whom the travel ban and lockdown is an existential threat. Here there is cause for optimism.

The scars of the Global Financial Crisis remain fresh enough that Central Banks have responded almost immediately and in an increasingly coordinated manner to the escalation of events and the threat to the functioning of the financial system. The US Federal Reserve led the way, cutting interest rates by 1.5% and resurrecting a number of familiar policies as well as unveiling some new tricks. Quantitative Easing (QE) is back and unlimited, with the Fed currently purchasing $125 billion of treasuries and mortgage-backed securities a day. This week the Fed also announced that it would provide liquidity to support US companies, including the purchase of investment grade bonds. The Bank of England has cut rates to 0.1% and increased QE by 40%, whilst the ECB has announced another €870 billion for QE that will be extended to corporate bonds and peripheral states’ (Greece) bonds. The Bank of Japan is buying Yen100 billion ($900m) of bond and equity ETFs per day.

Central banks have responded, doing all they can to ensure that banks are open, functioning and funding markets, and that the financial system has sufficient liquidity. They have moved to avert the risk of a funding, financial or credit crisis. What they cannot do is influence demand in a forcibly shut economy. Here the responsibility passes to government fiscal policy and here too we have seen a rapid and material response.

Prior to the crisis, there were signs that a wave of expenditure on infrastructure might be coming, fueled by ultra-low borrowing costs in government bond markets. This is now being redirected to support or replace demand and earnings across the global economy. In the UK the £30 billion of targeted measures announced by Rishi Sunak in the March Budget were usurped within a week by a wide-ranging spending package to support businesses and employees, worth up to £330 billion – or 15% of GDP. French President Emmanuel Macron has appeared before the nation to say that the government would not let any French business fail. Even in Germany, notorious for its fiscal conservatism, a €156 billion supplementary budget is being approved. Last night the US Senate approved a $2 trillion fiscal aid package, the largest congressional bailout in history. It appears that governments understand the enormity of the situation and that, having imposed the lockdown, they have a responsibility to keep businesses and consumers afloat and limit the permanent damage until business can resume. They will and the sooner they do, the steeper the gradient of recovery.

How we have been positioning portfolios

At James Hambro & Partners, whilst optimistic that a combination of central bank policy, government support and human resilience will lead the recovery from this natural disaster, we are realistic that the social and economic impact may last longer and prove more severe than current estimates. We are conscious of our responsibility to our clients to ensure that we deliver long-term growth in the good times but also look to protect their wealth in the bad.

We entered the acute phase of the slowdown with an equity exposure below our long-term average. We also had no exposure to the lower quality end of the bond market where high yield bonds, Emerging Market debt and even some corporate bonds are exposed to both solvency and liquidity risks. Our focus has been on UK and US government bonds which, whilst offering modest returns, provide real protection against the challenges in equity markets and other assets. We have since reduced our overall equity exposure and steadily raised cash to levels above those we had during the market upheaval of 2018.

The focus has been on reviewing all our investments and assessing which previously-strong companies might become threatened if the economic slowdown becomes deeper and more prolonged. Principally these are businesses that have exposure to the travel and leisure industries, where demand has ceased as a result of the lockdown and where their secondary or tertiary suppliers might enter financial difficulty. We are fortunate in that our investment philosophy leads us to avoid companies with excessive leverage or those in deeply cyclical industries. Our experience of 2008 means that we are prepared to think the unthinkable and so have sold a small number of the most exposed holdings. Our fixation on liquidity in all we do has meant that we have not had any problems selling where we wanted to. We are now comfortable with our positioning given the present circumstances and we have sufficient liquidity to take advantage of opportunities that will undoubtedly present themselves when we begin to see light at the end of the tunnel.

It is too early to turn attentions to the longer-term impacts of the current crisis. However, it is clear that it will create permanent changes to government policy and businesses as well as accelerate some trends that were already in place. From an economic perspective, the fiscal cat is out of the bag and with populist leaders in power in many countries the prospect of modern monetary theory (MMT) – crudely the printing of money by central banks to directly finance government spending – becoming reality looks more likely than ever. With governments to pay money directly to support citizens, a universal basic income does not look farfetched.

There will be time in the coming months for us to consider these implications, now our focus is on looking after all our clients and proving safe custodians of their investments.

I hope that you and yours are safe and well.

By James Beck

Posted on 26th March 2020

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.