Markets were steady in November until a new coronavirus variant emerged, sending a shudder down the collective backbone of investors worldwide.

Inflation may have been grabbing all the headlines, but it looks like the pandemic is once again vexing investors. The emergence of the Omicron variant at the end of November, which is potentially more contagious and resistant to vaccines, raised fresh concerns about stricter containment measures and the impact of potential lockdowns.

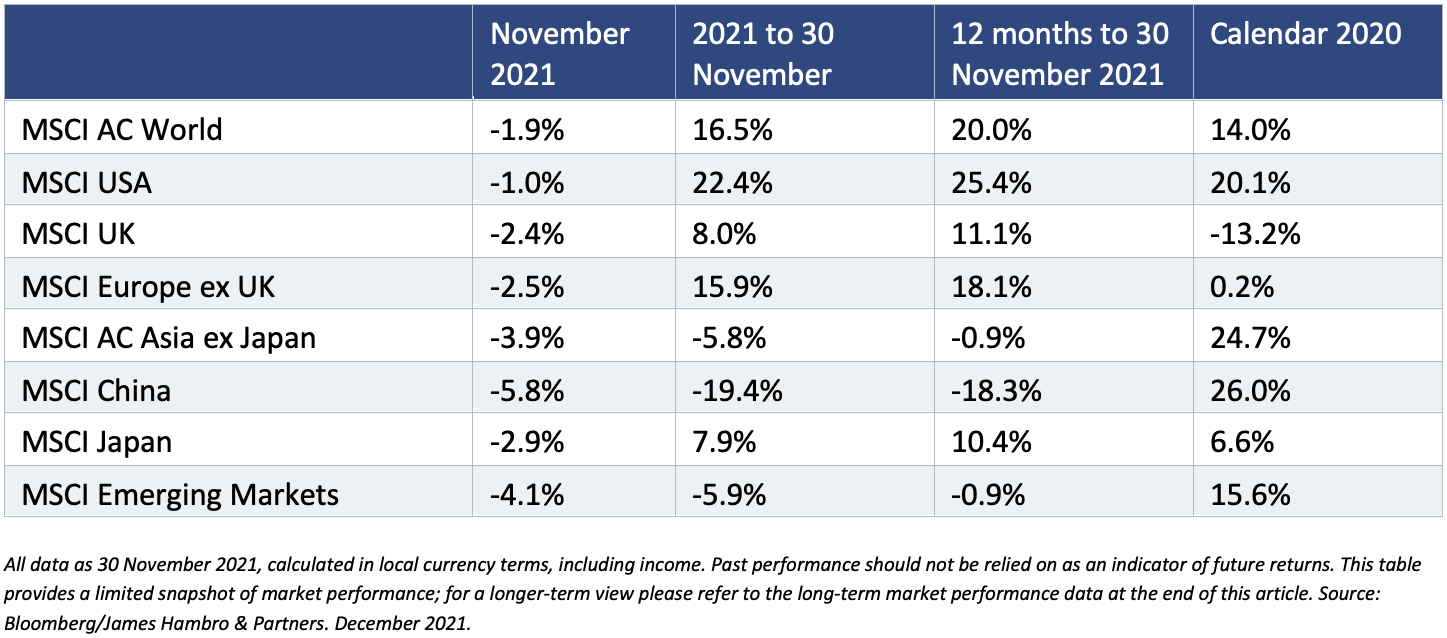

Equities had been steady for most of November, but suffered in the last week, with the MSCI All Country World Index ending -1.9% for the month (local currency, including income). Developing regions were hurt the most by this risk-off sentiment, with the MSCI Emerging Markets Index down -4.1%.

There was a sharp selloff in Europe, which is already enduring a fourth Delta-led wave, wiping out six weeks of gains on the Stoxx 600. US stocks were less affected and bounced back after US President Joe Biden said economic lockdowns are off the table.

Three things to look out for

There’s a lot we don’t know about the Omicron variant. We think that market direction will largely depend on three factors:

1. How will central banks react?

The threat of the new variant has already had an impact as market expectations of monetary policy turn more dovish, despite rising inflationary pressures. Both the Fed and the Bank of England are scheduled to report on monetary policy later in the month, and we’ll be watching keenly for indications of where they’re heading next.

2. What are the inflationary impacts?

Depending on how long restrictions last – and whether further restrictions are imposed – supply chain bottlenecks could narrow further, intensifying already high inflation. Worker shortages could also add to inflationary pressures given labour markets where there are already more jobs than candidates to fill them.

3. How will consumers react?

Travel restrictions imposed on some destinations will doubtless have an impact on travel stocks, and there is anecdotal evidence of Christmas party plans being scaled back that will damage the hospitality sector, even as the government insists that there will be no further lockdowns. In the last lockdown consumers switched spending to goods rather than services; if their response proves Pavlovian it could keep inflation higher for longer. However, there are only so many Pelotons and laptops people need – without the impetus of government support lockdowns could prove destructive for demand and economic growth.

Focus on quality provides some immunity

While we are more concerned about the potential long-term economic impact than the recent short-term moves, there’s not enough information at the moment to make forecasts with any certainty. The good news is that over the past 18 months governments have largely risen to the challenge of supporting economies through the worst of the pandemic, and the medical industry has demonstrated that it’s able to act quickly to deal with new variants.

In the meantime, resilience is a key characteristic we look for when we invest, precisely because it mitigates against these types of shock. Additionally, we are not overly exposed to those sectors most at risk from restrictions on travel, which have inevitably experienced the biggest falls.

Investing for the long term

Like a lot of countries at this point in history, the UK government is keen to invest in big infrastructure projects. Investment and rebuilding have been a key element to this government’s platform, and the economic damage of the pandemic has sharpened appetites for the kind of stimulus that big projects can create.

There’s just one problem: how to pay for it.

Government spending over the period of the pandemic has left little room for new expenditure – quite the opposite in fact. Investment markets, in the meantime, have typically run shy from direct investment in this type of project which can take decades to show a positive return.

Long-term asset funds to the rescue

In an effort to encourage investment, the UK Financial Conduct Authority (FCA) recently finalised rules for a new type of fund designed to make it easier. The Long-Term Asset Fund (LTAF) regime will encourage investment in venture capital, private equity, private debt, real estate and infrastructure opportunities.

LTAFs won’t be for everyone. They’re intended for sophisticated institutional investors – in particular defined contribution pension schemes, which have long-term investment horizons – and certain high-net worth individuals. The FCA will be consulting next year on the potential for widening the distribution to other retail investors, but they’re unlikely to be made available to ordinary investors any time soon.

The risks of locking your money away

We are interested in innovation that offers the potential for returns, and we recognise the opportunity that investing in long-term assets presents. The new LTAF framework could be an interesting opportunity for private investors, and we’ll be watching how the market develops with interest. We take a long-term view by default and would certainly consider including these new vehicles for portfolios.

But there are reasons to be cautious. These funds would be investing in highly illiquid assets – this will inevitably have an impact on how easy it is to get one’s money out when you need it. LTAFs will come with rules to make sure redemptions are managed sensibly, and these will need to be considered against the long and short term needs of investors.

Although investing the assets types targeted by LTAFs offers the potential for higher returns, recent history reminds us that it can be difficult to cash in when markets turn against them. Between 2016 and 2020, many real estate funds were forced to close to redemptions for periods as the demand for redemptions outstripped the funds ability to liquidate assets. Investors were left trapped in funds, leaving them powerless in the face of future falls in value.

At this point in time, no LTAFs have been launched, so the questions are largely academic. When (or if, even) products come to market we will consider them carefully, but for the time being the illiquid nature of the underlying assets merit a degree of caution.

Long-term market performance