03.03.2021

Are ESG investors expecting too much?

Sarah Goose, Portfolio Manager, Responsible Investment Lead

Momentum behind corporate climate ambition is building and our expectations are rising in tandem. Where we used to applaud companies that set targets and announced bold intentions, now we require it.

Momentum behind corporate climate ambition is building and our expectations are rising in tandem. Where we used to applaud companies that set targets and announced bold intentions, now we require it.

In an impatient world it is easy to hope for immediate reform, but this is a marathon with a staggered starting line that makes it more complex to judge relative performance. It is helpful for investors to understand how the challenges differ from business to business.

Pressure from all sides

Risks to climate, biodiversity and changing social attitudes have prompted mounting consumer pressure; employees have gained confidence to speak out, and governments are responding by setting ambitious targets and timelines. This exciting movement is evolving quickly, but the responsibility for much of the action lies with individual companies.

2020 provided an inflection point for corporate sustainability. Many of our jobs moved online, and the pace of work increased, whilst other aspects of life were put on hold. The fragility of our relationship with the natural world and our dependence upon it was highlighted by the global pandemic, and by the increasing availability of information on climate change and biodiversity loss

Companies must now grapple with a shifting dynamic from the traditional focus purely on shareholder profit to one on stakeholder engagement. In the past few months we have seen the UK government pushed to introduce a mandatory shareholder vote on corporate climate policy at AGMs, and in some cases companies have been urged to consider their legal structure to ensure sustainability targets are sincere.

It is tempting to be reactive and focus on the short term, but we need to look for long-term structural changes in how companies interact with their stakeholders.

Challenge varies from company to company

Outlining the challenges companies face allows us to ensure we understand the risks and opportunities from an investment perspective. The starting point is different for each company. Sector, size, supply chains and distribution networks are just some of the considerations when creating a roadmap of achievable targets. Materiality is a key concept; identifying which factors, risks and opportunities are most material and relevant to a company helps us analyse if steps are being taken to address necessary risks. However, those businesses with the biggest material risks are often the gate keepers to genuine societal progress (companies like Rio Tinto, which provide vital supplies of copper, for example).

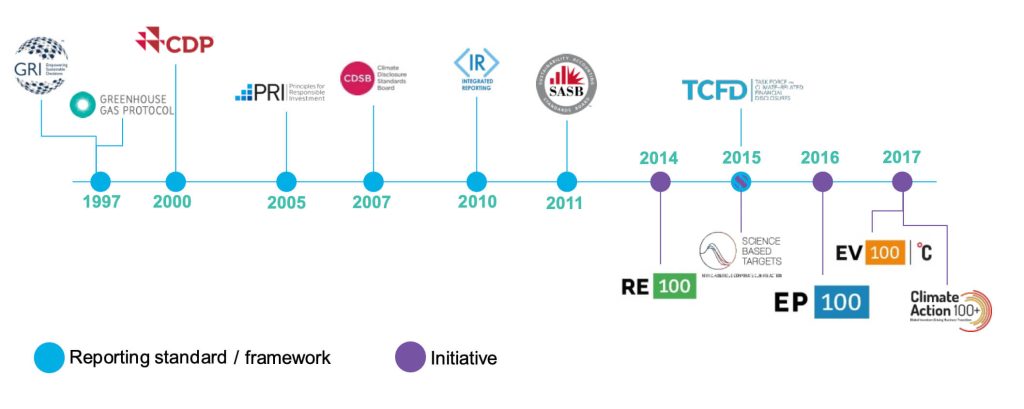

The absence of a single, or widely-adopted framework for disclosure and reporting makes analysis difficult and highlights its critical importance. The current alphabet soup of standards and initiatives is a source of confusion and complexity.

Source: CDP

However, we must be wary of unintended consequences. A net-zero announcement may be applauded, but the viability of such a commitment requires thorough research. The impact may create ripples for management teams, but tidal waves down the supply-chain, with communities unable to adjust and livelihoods destroyed. Bill Gates has been vocal on climate change, highlighting recently that “those of us who have done the most to cause this problem should help the rest of the world survive it.”

This introduces us to the possible release valve. Investment is required to fund research and development, drive innovation and help scale up new technologies worldwide. For public and private investment to take off, we need to ascribe a cost to decarbonisation and a value to natural capital. We have to price in and account for the risks of climate change to unleash financial capital in the most effective way. This latter point is where standards are required.

Benefits

Companies have come together to create frameworks and initiatives, such as RE100, ZDHC, the Plastics Pact, and many more. Great progress has already been made, with frameworks for nature and climate-related financial disclosures being willingly adopted by companies, and now also by countries. The upcoming COP 26 carries high hopes for progress here, and corporate cohesion should perhaps be an example to countries with increasingly competitive agendas.

Annual new TCFD supporters

Source: BloombergNEF, TCFD

Timeline of major sustainability commitment announcements

Source: BloombergNEF

Meanwhile, companies taking a holistic approach to sustainability are, in some cases, seeing significant share price appreciation. Intergenerational transfers of wealth, combined with incoming regulation in Europe and the UK has seen ‘green premia’ ascribed to some of the more obvious beneficiaries of these tailwinds, and President Biden’s prioritisation of environmental matters is driving similar moves across the Atlantic.

Need for pragmatism

Whilst uncertainty remains, the direction of travel is becoming clearer. We believe companies exhibiting sustainable growth are best positioned to protect and grow our clients’ capital, but we must be cognisant of the pressures applied to companies, ensure we understand ambitions, risks and opportunities in this changing landscape, and be pragmatic in our analysis.

By Sarah Goose, Portfolio Manager

Posted on 4 March 2021

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.