Markets got off to a rocky start in 2022 as investors came to grips with the accelerating pace of tightening monetary policy, but it’s vital to take a considered view and see market corrections in context.

It’s been a bumpy ride for markets so far this year, with stocks tumbling due to concerns about central banks raising rates to tackle inflation and governments scaling back their COVID support programmes. While these moves are important, they are unlikely to derail economic growth in the year ahead. This environment should continue to support company earnings and a bias towards equities.

Markets wake up to New Year hangover

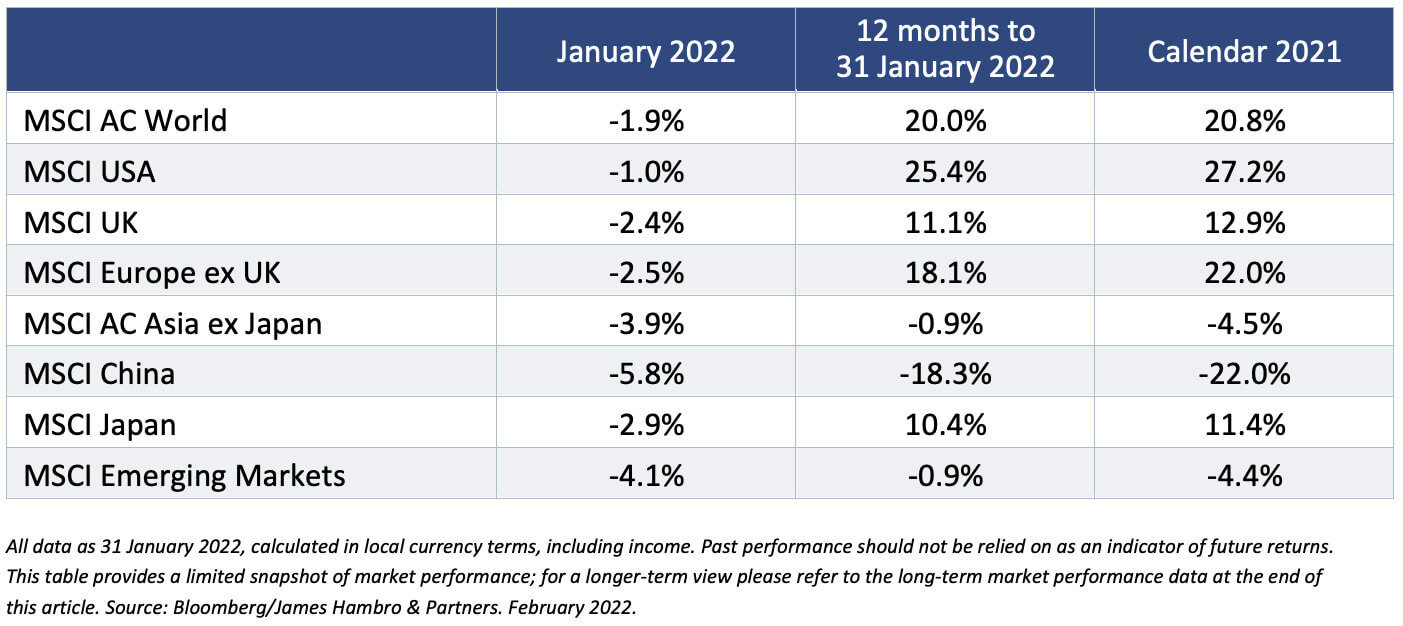

After a strong December, the new year apparently found investors full of regrets. The S&P 500 had its worst ever January, ending the month -5.3% lower (on a price return basis). This compares with the MSCI AC World index which fell 1.9%. These are the biggest market falls seen since March 2020.

Investors are worried that the increasing speed of interest rate rises could hurt corporate profits and dampen demand for equities. Notably, the US Federal Reserve (Fed) has indicated that it plans to raise interest rates as soon as March and accelerated plans to wind down its bond buying stimulus. The Bank of England raised rates again in the first week of Feb, to 0.5% from 0.25%, and while the ECB has left rates unchanged, the head of the European Central Bank Christine Lagarde signalled a shift in tone as she failed to rule out the possibility of a rise later in the year.

The Fed has a double mandate to keep inflation at around 2% and maintain low unemployment. With unemployment running near record lows and inflation at 30-year highs, it is clear that the time for ultra-loose monetary policy is coming to an end.

Tech firms no longer the smartest giants in town?

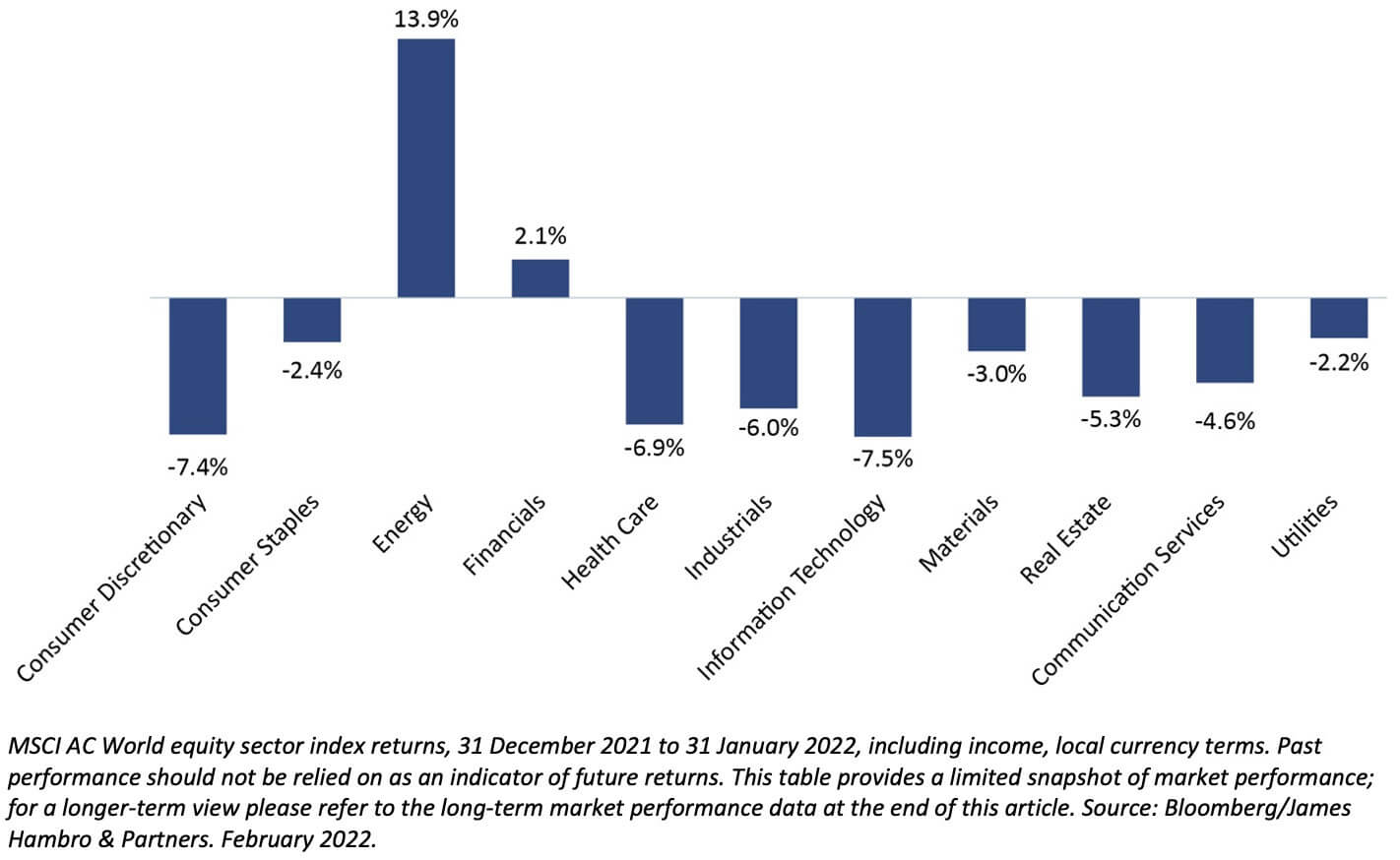

Sitting on high valuations after a strong run, tech stocks were particularly vulnerable to sell off as investors turned cautious. As a result, the technology sector fell -7.5% in January.

Energy up, tech stocks down

Sector returns, January 2022

Some of the giants that led markets in 2020 and 2021 such as Tesla, Microsoft and Meta (the new name for Facebook and related companies) suffered large falls, and the market’s increased reliance on these mega stocks – especially the S&P 500 – means these moves had an outsize impact on indices.

The energy sector bucked the negative trend due to continued high demand thanks to healthy economic growth, OPEC’s unwillingness to increase oil production and nerves over what Russian bellicosity in Ukraine could mean for natural gas supply in Europe. Financials was the other sector to see a positive return, as rising inflation tends to be beneficial to the bottom line for banks and other lenders.

Still on course

We have been predicting that 2022 would see monetary tightening, and with it and a more volatile environment for equities, for some time. The good news is we don’t see the current market jitters leading to a wholesale selloff for several reasons:

- The economic background remains strong

While they can bring more volatility, rising rates are a good thing if the economy is healthy and growing. The current economic backdrop remains supportive to financial markets, with growth projections well above average levels and no signs of recession. Escalation of the conflict with Russia over Ukraine could cause further short-term market disruption, but the impact is likely to pass more quickly than the inevitable humanitarian crisis. - Consumers and businesses are relatively rich with cash

Growth should be supported by strong employment and consumers in the US who are sitting on high levels of cash. Companies also have money in the bank, and pandemic-caused breaks in production and supply mean they are likely to spend to replenish diminished stocks. - Monetary conditions remain among the loosest ever seen

Tighter monetary policy doesn’t necessarily mean tight monetary policy. Central bank policy in developed markets is loose compared with the past, and it’s possible we won’t see interest rates return to pre-pandemic levels until 2023. While the Fed understands the need to raise interest rates, the pace and magnitude of hikes will be moderated by the need to foster stable financial conditions and protect employment levels. Similarly, unwinding central bank debt holdings accumulated through quantitative easing is likely to be a gradual process.

Into each life some rain must fall

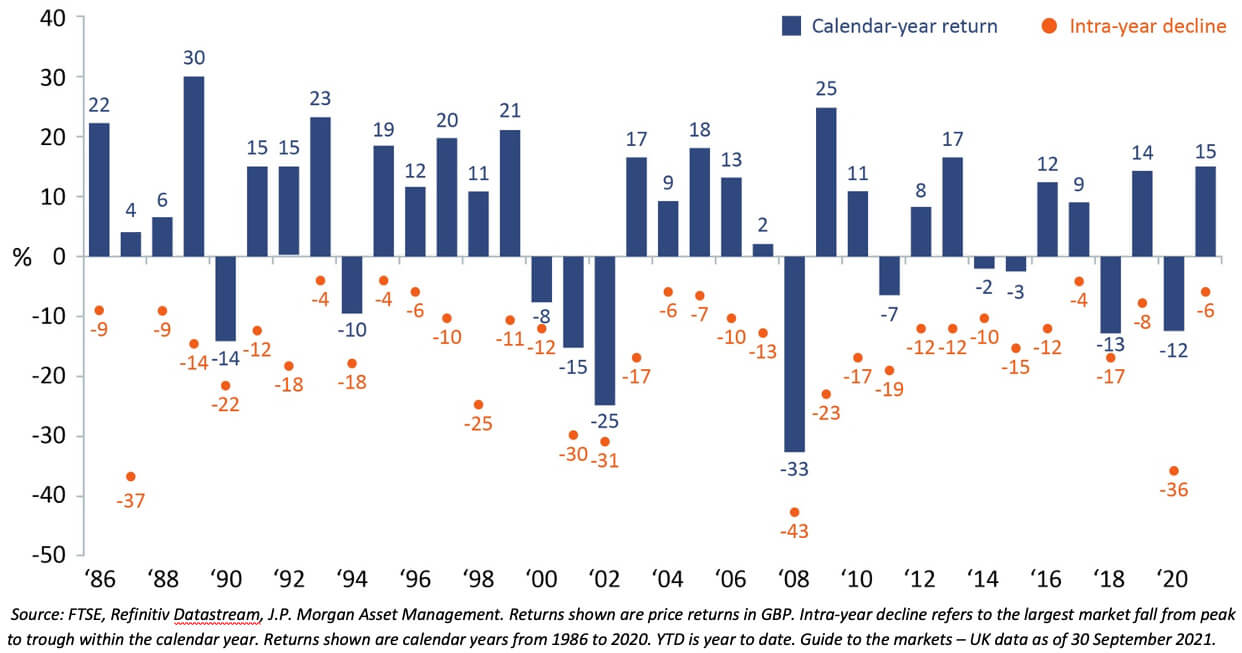

The stock market has constant ups and downs. While this volatility can be unsettling for investors, stock market declines are common, with market corrections of 10% happening relatively frequently. Markets fell this time last year after a bumper November and December, but 2021 turned out to be another very strong year for markets.

The chart below shows the performance record of the FTSE All Share over the past 35 years. As you can see, between 1986 and 2021 there were 24 years with corrections of 10% or more, while there were only 11 years with an overall negative return. This chart shows price return only – over the entire period, a total return if you had stayed invested, including income from dividends, would be around 2,200%.

Time is on our side

Many investors live by the old adage ‘time in the market beats timing the market’. This speaks to the fact that holding on through periods of market volatility is a much better strategy for long-term success than trying to sell during market highs and reinvest when they fall again. In practice, even professional investors find this approach challenging.

Long-term investment success relies on identifying companies with strong businesses and sticking with them unless the story changes. The latest turns in economic policy have not changed our underlying views for the time being. We are focused on long-term performance, and we’re very confident about how we invest.

Over the longer term, investing in quality companies with strong balance sheets and visible and robust earnings streams should provide attractive shareholder returns. If we see further share price weakness, we will consider using it as an opportunity to deploy more capital in companies with a positive growth outlook.

Long-term market performance