18.10.2019

ESG: Embracing sustainability

“Improving the quality of life without borrowing from the future is the single largest investment opportunity in history.” Al Gore

Portfolio Manager Mark Leach

Increasing awareness and understanding of the impact humans are having on the planet is driving a significant change in consumer behaviour, supported and facilitated by shifting political and regulatory priorities. At James Hambro & Partners (JH&P), we believe companies that allocate capital responsibly, putting environmental, social and governance (ESG) considerations at the centre of their strategic frameworks, are more likely to succeed in the longer term than those companies that do not.

A rising tide

Socially responsible investing has evolved considerably. Originally the decision was more negative than positive. Investors chose not to invest, for example, in tobacco or defence companies, taking an ethical view on their products and their impact on society. However, as the realities of climate change and humankind’s broader impact on the planet have been realised, investors have adopted a more comprehensive framework for measuring the sustainability of all companies.

Over time the ability to analyse the ESG credentials of public companies has gradually improved. As pressures have built, corporations have been forced to pay more attention to the impact they have on the world around them. Investors have asked not just for profits but for evidence that companies are working to reduce their carbon footprints, that they are respectful to all their employees and the societies they impact, and that everything they do is governed by corporate policies of the highest standard.

The accumulation of data has both improved standards of practice and increased our ability to compare one company with another. With comprehensive analytics at our disposal we can hold businesses to account and identify risks that might mitigate attractive long-term returns in the future.

“Operating to the highest standard of ESG is good business.”

Jakob Stausholm, Chief Financial Officer, Rio Tinto

Avoiding the bombs

In the first instance poor ESG standards have been found to be directly related to a higher incidence of bankruptcy. ESG-related controversies in large US companies have cost investors over $500bn in capital in the past six years. To a large degree successful investing is not just about finding the winners but about avoiding substantial losses, and ESG provides a powerful tool to help prevent this. Volkswagen is a prime example of a business where poor governance led to an environmental scandal that cost its shareholders dearly.

Conversely, high ESG standards are directly related to higher returns. According to Bank of America Merrill Lynch (BAML), companies that are highly rated on ESG have significantly outperformed the wider market over the last five years.

As the data has improved, the pace at which investors are incorporating ESG considerations into their analysis is accelerating. In 2018, The Global Sustainable Investment Alliance estimated that $31tn of professionally managed assets were subject to some form of sustainable investment overlay. This represents nearly one third of all global assets under management, and is 36% higher than in 2016.

Transparency and accountability

Strong corporate governance practices are the foundation on which sustainable social and environmental policies are built. With independent board members, greater levels of diversity in gender and ethnicity, and with protections in place for shareholders (owners), strong corporate governance should ensure that companies allocate capital for the longer term in a sustainable manner and with all stakeholders in mind. It stands to reason that employee productivity goes hand in hand with employee satisfaction. BAML analysed the share price performance of companies with high employee satisfaction ratings on Glassdoor.com (a recruitment website) and found that these companies considerably outperformed those with low ratings.

Developed markets, in particular the UK, have long been held in high regard for their corporate governance standards. It is for this reason that we have often preferred to gain access to emerging market trends through owning companies incorporated in the UK as well as other developed economies, such as Europe and the US, over local companies. Examples include Unilever, the global consumer products firm with nearly 60% of sales to developing economies, and Mondelez, the snacking powerhouse, which has a 60% market share in chocolate in India.

Analysing and comparing governance practices is increasingly

an objective exercise. We engage with management teams on a regular basis and use a proxy consultant to advise us on how best to vote at AGMs.

The tide is turning

The evidence documenting the impact modern society is having on the planet is undeniable. The UN’s latest science-based report on climate change makes for some uncomfortable reading. The last three decades have been hotter than any previous decade; the rate at which mean sea levels are rising has increased from 3mm per year between 1997 to 2006 to 4mm per year between 2007 and 2016; and global plastic production is expected to triple by 2050, by which point there will be more plastic than fish in our oceans. The problems we face are not only accelerating but are reaching crisis levels.

From documentaries like An Inconvenient Truth, Cowspiracy and Sir David Attenborough’s Blue Planet, through to the protests inspired by Swedish teenager Greta Thunberg, action on climate change is beginning to move from the fringes of politics to the core – it is becoming a vote winner. People and politicians are coming together to demand a more sustainable future. Whether this comes from greater regulation, government incentives or a more discerning consumer, all companies must adapt to this new reality.

Sustainability is key

At the core of our investment philosophy is a bias for companies that we judge to have a long runway of sustainable growth. Given our ability and preference to invest over an extended time horizon, we consistently question whether that growth is also sustainable from an environmental point of view. Therefore, ESG is not a box-ticking exercise but a consideration at the heart of all our investment decisions.

We are not impact investors; the shift to a more sustainable society will be gradual, and we must maintain a diversified portfolio to achieve an attractive risk-adjusted return over a prolonged period. Impact investing is focused only on companies involved in finding solutions to the world’s sustainability conundrum. To follow this route, we would limit our investment universe and risk building technology-based portfolios potentially exposed to binary outcomes – the technology or product either succeeds or it does not. It would also mean being overly concentrated in a narrow set of subsectors.

Therefore we think in a more pragmatic fashion, looking for evidence that our companies in the first instance are not at risk from an exogenous consumer or regulatory shock and that they are actively engaged with the issue of sustainability. By doing so successfully, companies that already enjoy high market share and strong brand power are likely to expand their barriers to entry and prove tougher competition for their peers.

Building blocks of progress

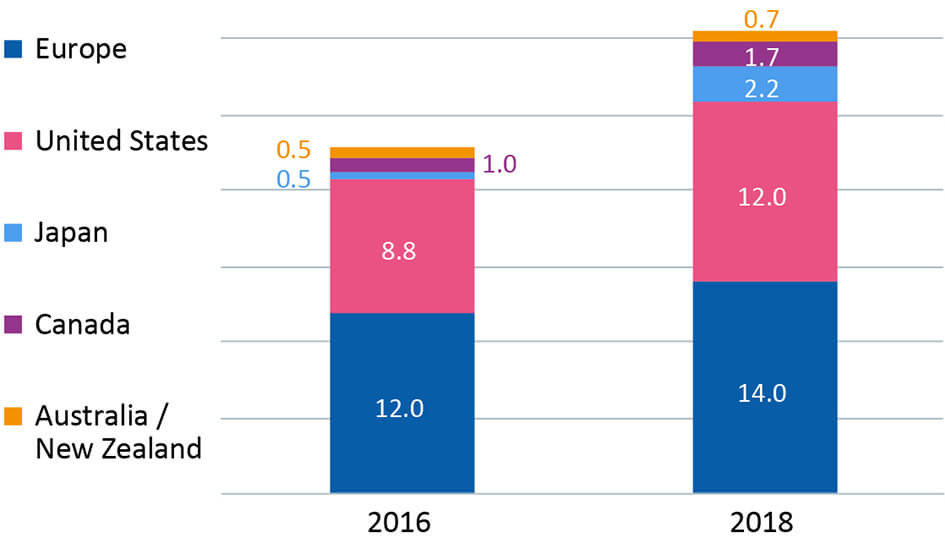

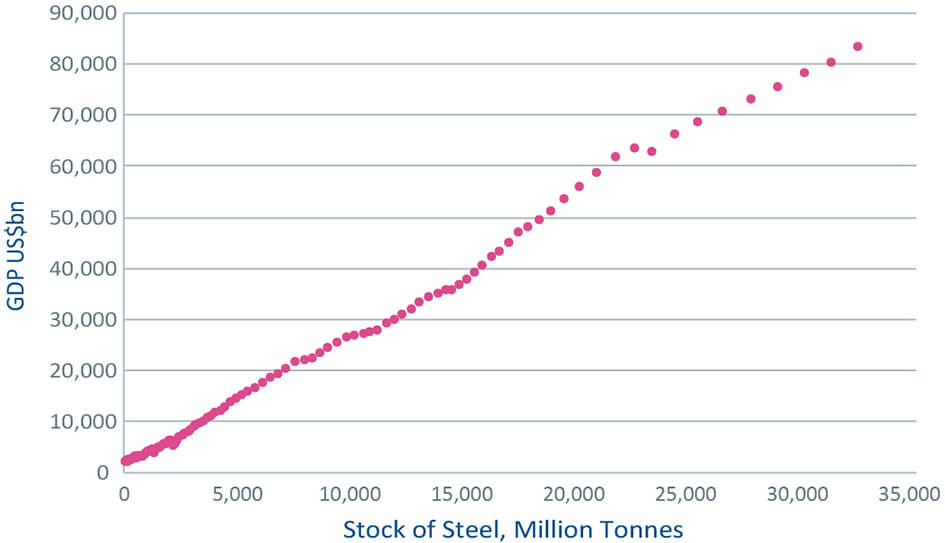

The mining industry is often labelled a ‘sin’ sector because of its environmental impact. We do not disagree, but the extraction of minerals is also at the centre of human advancement. Iron ore, for example, is a fundamental building block of a modern society – as GDP per capita rises and nations get richer there is a direct correlation to the installed base of steel, of which iron ore is the fundamental ingredient. According to Bernstein, a research provider, the stock of steel in the global economy is 32bn tonnes today, representing four tonnes per person, but this is unevenly distributed with 15 tonnes per person in the West and only one tonne per person in Africa and 6.5 in China. To bring the world up to 15 tonnes per person would require a 240% increase in the global stock of steel. Growth in demand for steel remains directly linked to human economic progress and to deny emerging nations the opportunity to modernise would have grave consequences for global stability.

“Copper is the world’s new hydrocarbon.”

Robert Friedland, Founder and Executive Co-Chairman of Ivanhoe Mines

The extraction of copper is similarly problematic. One of the great industrial revolutions of our time will be the electrification of vehicles and the demise of the internal combustion engine (ICE). Today, transport accounts for 24% of energy-related carbon dioxide emissions globally and so replacing the ICE is a significant step forward in addressing climate change. Copper is one of the key components that will facilitate this change within electric vehicles (EVs) and also within the renewable power generation assets and electricity transmission networks that will replace carbon-emitting fossil fuels. Only then can EVs truly claim to be green.

These forces offer the opportunity to invest in a trend that will drive sustainable growth for the foreseeable future, for example through Rio Tinto, which derives the majority of its profits from the extraction and sale of iron ore and copper. Rio’s pedigree is impressive: it is a rare member of the FTSE100 survivors list, having been part of the index since its inception in 1984. In that time Rio is the fourth best performer, delivering an annualised total return of 12%.1

Rio’s iron ore operations are of the highest quality, meaning they require less energy for extraction and smelting. It has high standards of corporate governance that have led to sensible strategic decisions. It sold its coal assets and resisted temptation to chase growth in regions where corruption and labour practices have seen others stumble.

Keeping it clean

Consumer goods companies are under more and more pressure to ensure that the source of the raw materials they use is sustainable, that the packaging is recyclable, and that the product is not polluting, all while trying to reduce their own carbon footprints. Their customers want to continue washing their clothes and cleaning their teeth but in the knowledge that it is not costing the Earth.

Unilever was an early mover in addressing the sustainability conundrum and has an ambitious target of becoming carbon neutral by 2030. Last month, the company announced that it had reached 100% renewable energy use across five continents. Mondelez, the global leader in the snacking category and owner of Cadbury’s, through its Cocoa Lifeprogramme is working to improve the sourcing of its cocoa beans, tackle child labour practices and through education and technology is improving cocoa yields, thus reducing land use. Mondelez also targets 100% recyclable packaging by 2025.

Playing the theme

The evolution to a more sustainable future provides a rich backdrop of opportunities that we are actively looking to exploit. To achieve this successfully we analyse the entire value chain to identify where we can benefit from the growth without risking being wrong with how the end market develops.

For example, electrification and autonomy are visible trends in the auto market, but rather than speculate on whether Tesla or Volkswagen will be the ultimate winner, we prefer to focus on the suppliers that stand to benefit from the wider adoption of EVs. Within the semiconductor sector, Germany’s Infineon has high market share in manufacturing microchips used to manage the distribution of engine power. The electrification of vehicle drive trains and the shift to greater levels of autonomy provide a larger market for Infineon’s products. The company states that the value of content sold per vehicle rises by a factor of two for a fully electric drivetrain and by a factor of six for full autonomy.

DS Smith, the packaging business, has invested heavily in building a pan-European network that can provide solutions to the consumer goods companies (70% of sales) as well as benefitting from the growing demand in ecommerce. Cardboard can be recycled in a way that many plastics cannot, and it is biodegradable if thrown away. DS Smith is investing to find ways that cardboard can take share from plastics. In addition, as ecommerce grows, the company is investing in box technology that can reduce both the weight of deliveries and empty space inside boxes – both measures will make significant reductions in delivery emissions. Such investments are why Mondelez has chosen DS Smith as its European partner for all its packaging needs.

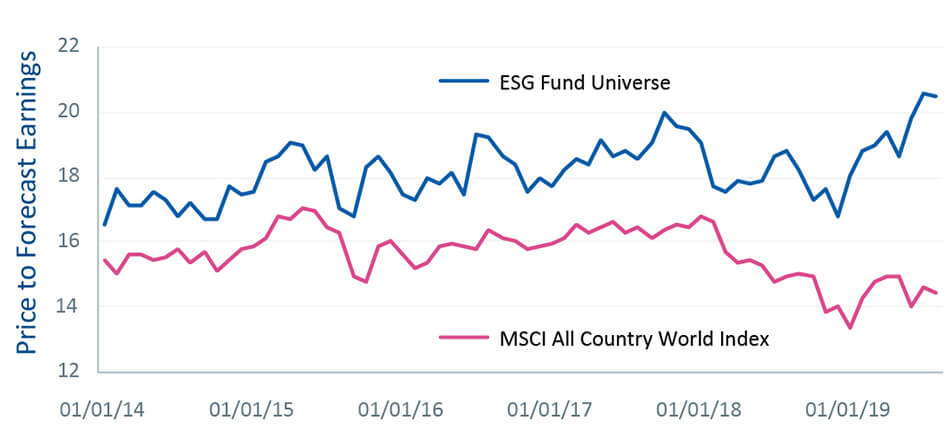

We must of course pay heed to the increasing premium emerging in the price of stocks identified as ESG champions. The bank Goldman Sachs has found that the companies most often held in ESG-focused funds have on average a 40% valuation premium relative to other companies. While we are strong believers in the persistency of the trends discussed in this report, we must be diligent that the price we pay is justified by the likely return.

Practice what you preach

There would be no sense in putting ESG considerations at the heart of our investment process if, as a corporation, we did not look to abide by best practice ourselves. At JH&P we have a Corporate Social Responsibility (CSR) committee that focuses on four core pillars to ensure we operate to the highest standards. These include our environmental impact, the wellbeing of our employees, giving back to the local community, and investing in a sustainable and responsible manner. Through care and consideration for all stakeholders in our firm we believe we can attract the best people and offer industry-leading service and performance for our clients.

By Mark Leach, Portfolio Manager

Posted on 18 October 2019

1. Bernstein, March 2018.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.