In our recent webinar, investment specialists shared their views on why the outlook for the healthcare sector is so exciting.

In a world gripped by pandemic, leading healthcare businesses have developed vaccines at breakneck pace to offer a way out of the Covid-19 crisis. Despite this awesome demonstration of innovation’s power to change lives, investors have marked down the value of many healthcare and biotechnology companies.

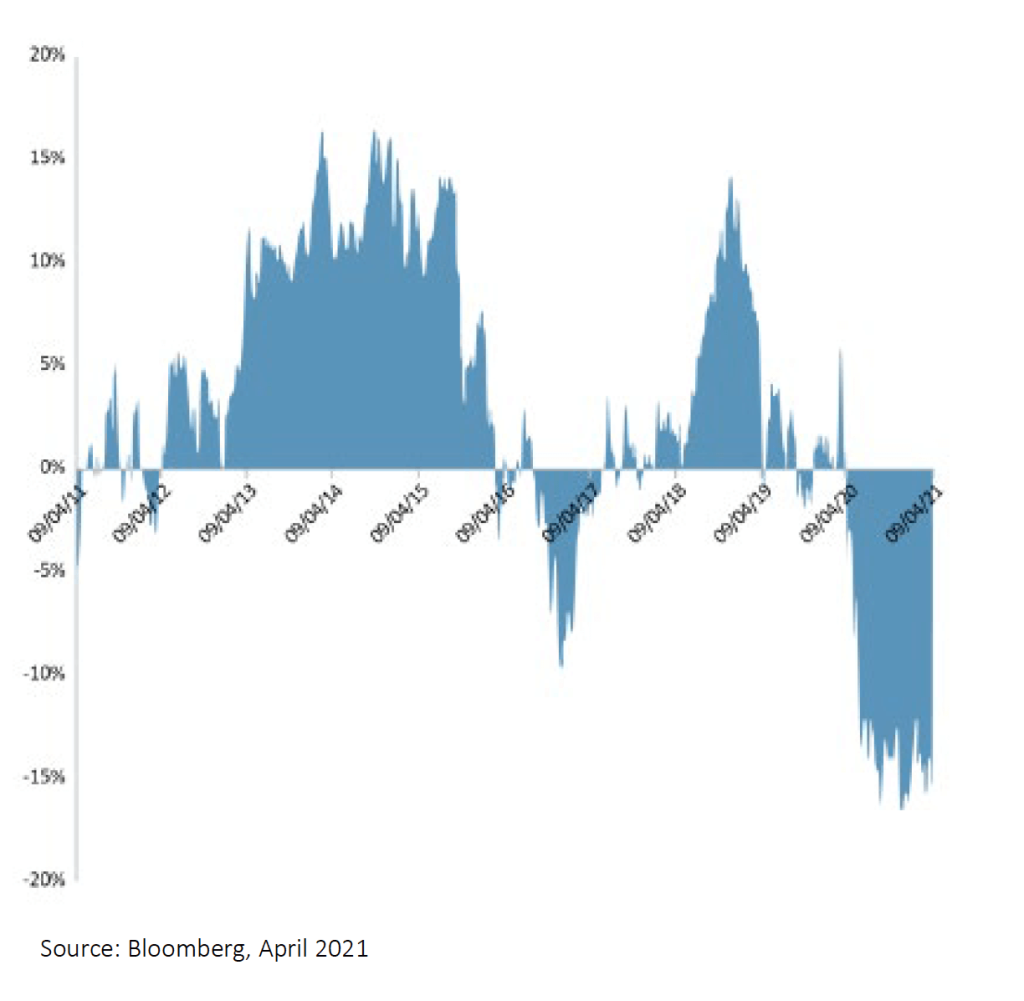

Indeed, healthcare valuations stand at historic lows. The MSCI World Healthcare Index currently trades at a discount of 15% to the MSCI World Index. In the US the S&P Healthcare Index trades at a discount of around 27% to the broader market – below even the lowly valuations seen in the early 1990s and late 2000s, when Clinton and Obama threatened the sector with reforms such as price caps on drugs.

Healthcare investing: opportunity knocks

“The history lesson here is that every time the sector trades at the sort of big discount we see today, there are incredible opportunities to increase our allocations to healthcare,” Sven Borho, Managing Partner of OrbiMed Healthcare Fund Management, told the webinar. “The healthcare sector always rebounds.”

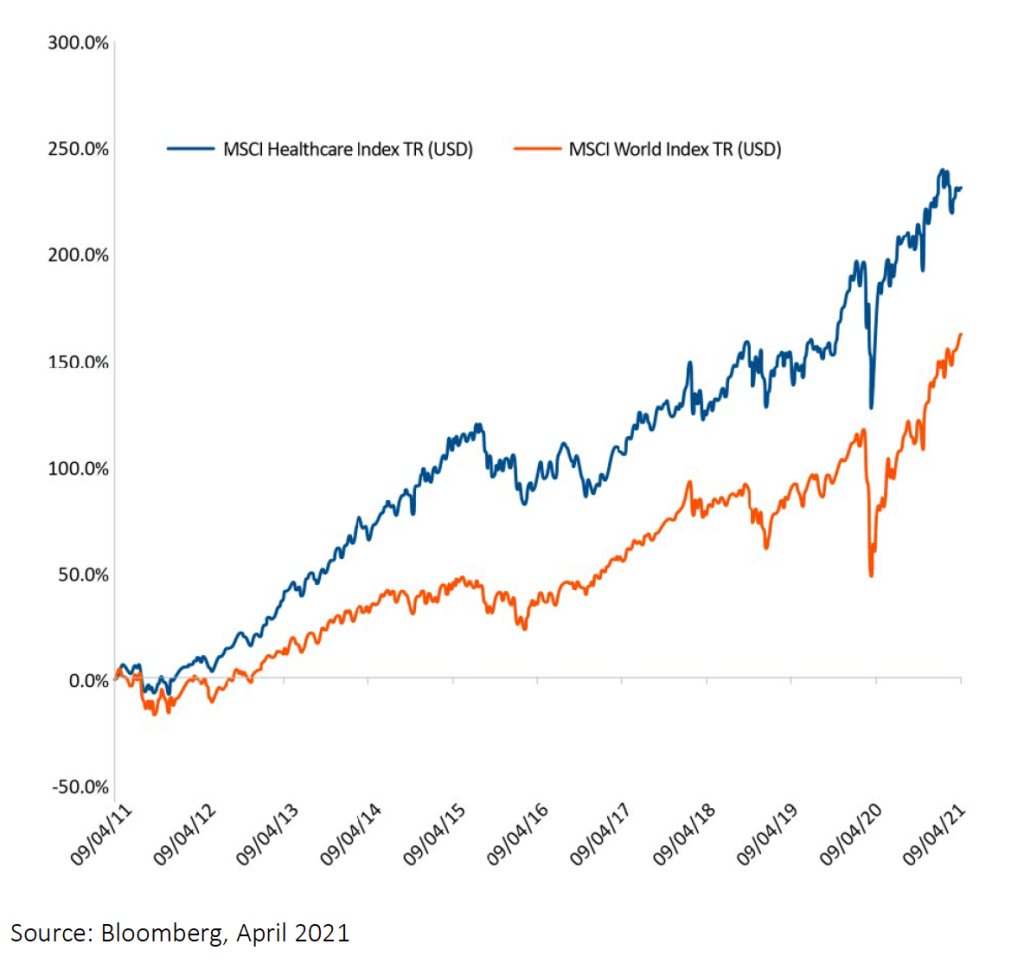

Dan Zegleman, a portfolio manager at James Hambro & Partners, says. “Past performance is no guarantee of future performance, but this looks like a great opportunity to get exposure to a growth sector at a value stock valuation.” He told the webinar: “The healthcare sector has a history of meaningfully outperforming global stocks, and I would argue that the fundamentals today are more compelling than they have been for a very long time.”

According to Borho, the key will be to focus on the most innovative areas of the sector, as well as to explore opportunities in fast-growing developing nations. He pointed to four areas where he is particularly enthusiastic.

Cancer immunotherapy

“Cancer immunotherapy has been the biggest breakthrough in the healthcare space during the past few years,” Borho said. These are drug treatments that stimulate the body’s own immune system to fight off cancer. Pharmaceuticals companies such as Bristol Myers Squibb and Merck are launching drugs that are proving highly effective against some forms of melanoma and non-small cell cancer.

Sales of two key drugs alone in these areas are expected to hit £33bn in 2021. And the healthcare sector is now looking at the potential to combine treatments to achieve even more effective outcomes for patients.

Targeted therapies

“Targeted therapies in oncology is probably the area where I’m most excited in the near term,” Borho told the webinar. These precision medicines, typically administered in tablet form rather than via injections or infusions, disrupt cancer’s progress by very effectively targeting the specific proteins that control the growth of the disease.

Several companies are innovating in this area. But Borho is particularly enthusiastic about the development of drugs that target the KRAS sub-group of cancers, including a common form of lung cancer. These could dramatically change the health outcomes for patients in a market worth as much as $5bn-$7bn a year in just this single therapeutic area.

Diagnostics

“In the diagnostic tools space, liquid biopsy reflects the holy grail of cancer diagnostics,” Borho said. The ability to diagnose cancer by drawing a small sample of blood is potentially revolutionary, with patients no longer having to put up with invasive procedures such as biopsies.

Liquid biopsies will substantially improve the initial diagnostic experience. They will also enable healthcare professionals to screen more people for cancer more regularly, to very specifically identify the type of illness they have and to check recovering patients for any recurrence of disease.

Relative to the forward P/E multiple of the main index, the MSCI World Healthcare Index is at a historic discount

Healthcare investing: The sector has outperformed over the long term

Past performance is not a reliable indicator of future performance. For illustrative purposes only and should not be construed or relied upon as advice. The value of an investment and the income from it can go down as well as up. And investors may not get back the amount invested.

Emerging markets biotech

The fourth area Borho highlighted represents a different way to think about innovation. “We strongly believe that investing today in the emerging Chinese biotechnology companies is the equivalent of investing in the Chinese technology space a decade ago – in the Baidus and Alibabas of the healthcare sector,” he told the webinar.

Traditionally, the biotechnology sector in developing markets such as China has been regarded as good at copying the science of the West, but it has not been associated with genuine innovation. That has now changed, Borho believes. The best Chinese biotechs have now caught up with their Western counterparts – and in some cases jumped ahead.

With such huge potential on offer, why are healthcare company valuations currently so discounted? One reason is that US President Joe Biden had been widely expected to target the sector with reforms that could squeeze drug pricing and so hit profits. Research suggests Americans often pay at least twice as much for their branded drugs as people in other countries.

“Drug pricing was supposed to be a big part of the Biden administration’s early push, but we have just heard that it is going to be excluded from the next infrastructure package,” Borho told the webinar. “That’s a big surprise to us all. But it seems like the Biden administration has made a calculated choice. It wants to achieve so many other things that it is not worth expending political capital on drug pricing right now. That has been the story for the past 15 years – the drug pricing issue has always been kicked down the road. This has been hanging over us and is probably part of the reason why the sector is trading at a large discount to the market averages. Maybe now we’ll see that gap narrow.”

Seize the moment

In which case, investors need to get on with thinking about which aspects of healthcare innovation most interest them. Zegleman makes a distinction between enablers and innovators. He describes enablers as the equivalent of those who supplied “picks and shovels in the gold rush”. They provide equipment to support trials and testing or to accelerate drug discovery. It is innovators that develop new intellectual property.

The latter may be more difficult to evaluate without specialist healthcare expertise. Most investors, after all, lack the biotech knowledge to decide whether one drug in development has better prospects than another. Zegleman told the webinar: “That is why we use specialist healthcare funds, managed by experienced investors in the sector, to find a route into the most attractive businesses.”

Bottom line

The bottom line, according to Borho, is the power of healthcare companies to drive commercial success and improved patient outcomes through innovation. “The right way to be a successful investor in the healthcare space is not simply to buy the cheapest company,” he told the webinar. “We want to be in the most innovative healthcare companies – the highest-growth companies that are introducing transformative products.”

Daniel Zegleman, Portfolio Manager at James Hambro & Partners, has a particular interest in the healthcare sector.

Sven Borho is a founder and Managing Partner of Orbimed, a healthcare-focused investment firm with over $17bn under management across public and private investment globally. Sven has 30 years’ experience of investing in the healthcare market.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up. Investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.