19.03.2021

What is the future for traditional income investors?

Edward Binks, Portfolio Manager

Edward Binks, Portfolio Manager

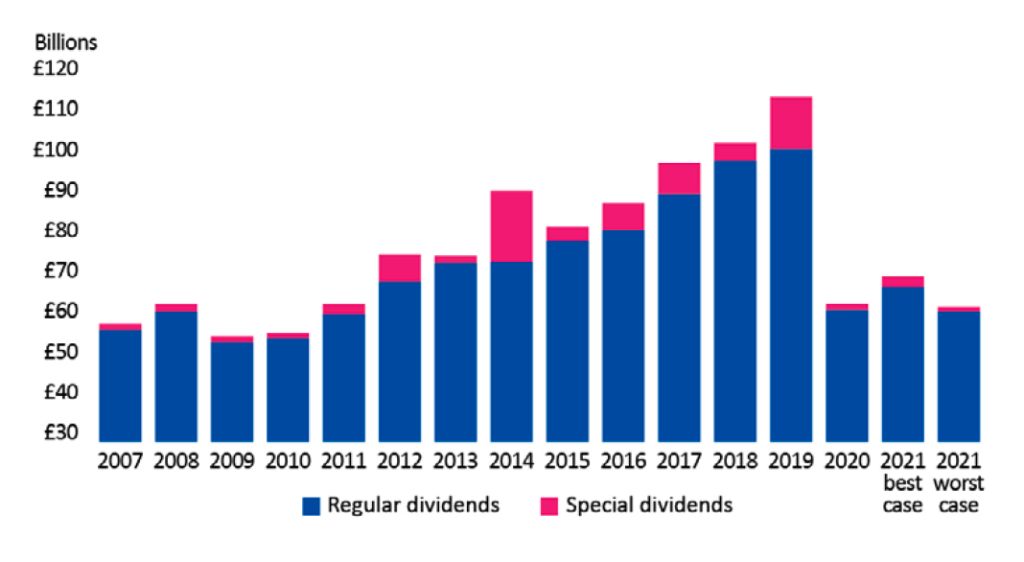

As the seismic waves of the Coronavirus pandemic crashed over the UK economy last year, many companies slashed their dividends. By the end of 2020 the FTSE 100 had seen a total dividend cut of 44%. That compares to just 13% in 2009, during the Global Financial Crisis. Nearly a decade of dividend increases was wiped out in weeks.

Projections for future dividend growth suggest it will take till 2025 for pay-outs to reach 2019 levels. And this may be optimistic. Many companies gained a loyal investor base over the years for their generous – but arguably unsustainable – pay-outs. They look set to use the 2020 crisis as an opportunity to reset dividend policies to a more affordable level.

A recent study analysing the discretionary fund management industry calculated that even the income yield from the average balanced portfolio – one not dependent purely on equities – has fallen from 1.8% nine months ago to 1.3% now. That is a fall of nearly a third.

For income investors – those who rely on investment income to pay the bills – this is a sobering thought. Is it time to rethink your approach?

The benefits of total return

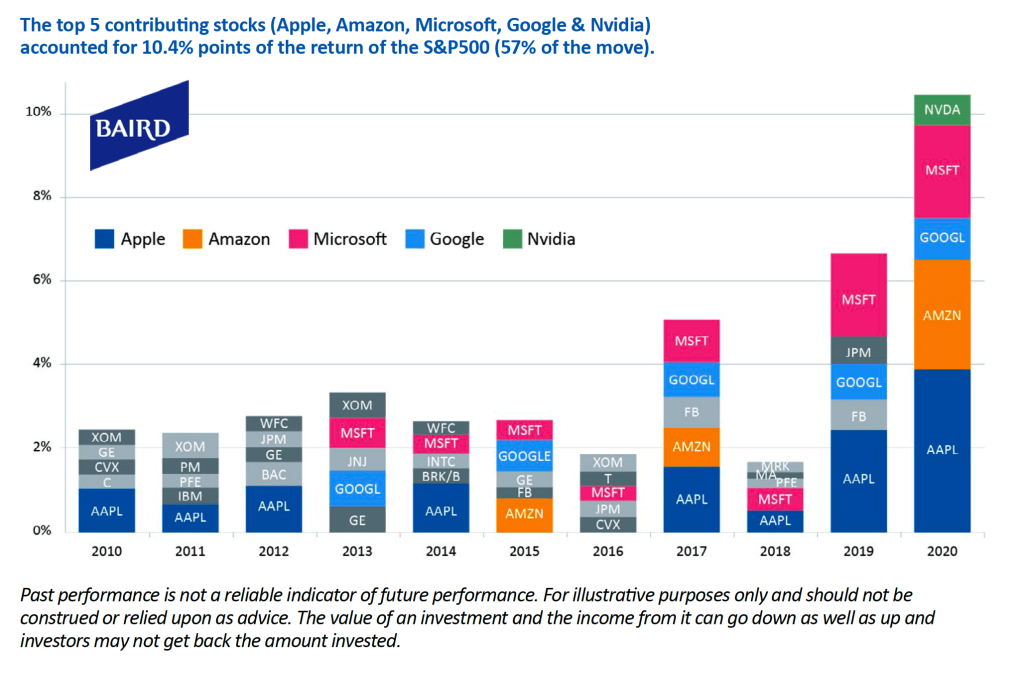

Allowing yield to dominate your investment strategy is arguably counterproductive and even dangerous. There is a strong case for investors to focus on high-quality companies with sustainable growth characteristics. By their nature, these companies tend to re-invest most, if not all, their cash flows into future growth opportunities. They pay little or no dividends, but they are good at growing capital. And the market has rewarded them for their success.

The past five years have seen a growing divergence in global equity returns between these higher-growth companies and those typically characterised as ‘value companies’, which tend to pay higher dividends. Between 2016 and the end of 2020 the MSCI growth index returned 123.4%. That compares with the equivalent value index of 47.1% – and this assumes all dividends are re-invested.

In other words, over five years the total return from growth stocks was on average two-and-a-half times more than from traditional dividend-paying stocks.

Risks

Investors with an overarching focus on income may have inadvertently narrowed their investment universe, excluding many of these superior growth companies. They may have also heightened risk in their portfolios.

To illustrate this, just 10 companies are forecast to pay 54% of the total dividend for the FTSE 100 in 2020. The companies in question are generally operating in sectors such as Oil & Gas, Utilities or Telecommunications, which one might describe as ex-growth or which in some cases are under pressure in the new world of ESG and sustainable investing. Barely a week passes without us hearing of another large investment institution that is jettisoning carbon stocks.

The challenge facing income-orientated investors has been turbocharged by the way society has responded to the global pandemic. Before the crisis, we were already seeing the positive impact of wider digitalisation in our lives. Many growth companies owed their success to this shift. They were benefiting from what investment managers call “secular trends”. In the crisis many of these trends accelerated rapidly. As a consequence, companies exposed to them did extraordinarily well.

So, those who had positioned portfolios towards some of these areas of higher growth, attracted by the technological and economic tailwinds that supported them, prospered.

No turning back

There is a view that these growth stocks are now overpriced and that mean reversion and a global recovery will favour value stocks in the months ahead. This might enable unloved sectors, arguably on a discount, to narrow the valuation gap and slowly rebuild their dividend policies.

There may be some truth in this over the short term. But for this view to hold for the long term you have to believe that society will reverse or at least halt the many changes in habit that have taken place over the past 12 months.

This is hard to conceive. The way the world has adapted and continued to function only re-enforces the structural headwinds many large, established companies faced before the crisis.

Looking ahead

We believe that we are now at a critical inflection point for income investors who adopt the traditional model of living off the income generated from invested capital. Outside of fixed interest, which looks increasingly challenged by inflationary threats, there are still some attractive income opportunities, like infrastructure. Some structured products are evolving to meet this need, too. But they can only help mitigate the problem. They cannot solve it.

The direction of travel was clear, if not widely acknowledged, before the pandemic gripped us. Society is not going to give back all the positive changes that have happened in the past year. This has long-term implications for investment returns and the types of companies you should be owning.

On the positive side, there remain great opportunities for investors who embrace a total return approach and think globally. By doing so you maximise the potential for real growth in invested capital over the long term. And you enhance your ability to meet your financial objectives.

By Ed Binks, Portfolio Manager

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up. Investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.