With the global economy set for its fastest recovery in 80 years, we’re maintaining our positive position in equity to benefit from the improving backdrop.

Four-minute read

Investment outlook

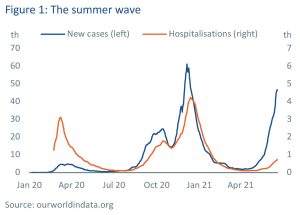

While the economic outlook is improving, the shape of the recovery will depend on the Delta variant and how this affects the emergence from lockdowns. If cases continue to surge, the brightening economic outlook risks being undermined by rising infection levels and the reintroduction of social restrictions.

Commodity prices have risen significantly this year, driven by accelerating economic activity as lockdowns ease, so it is little surprise inflation rose in the second quarter, particularly given the comparison to the economic freeze of 2020. We are also seeing a number of supply bottlenecks caused primarily by Covid-related disruption, but not helped by events such as the Suez Canal blockage. This is causing a shortage of goods, which is adding to inflationary pressures.

Commodity prices have risen significantly this year, driven by accelerating economic activity as lockdowns ease, so it is little surprise inflation rose in the second quarter, particularly given the comparison to the economic freeze of 2020. We are also seeing a number of supply bottlenecks caused primarily by Covid-related disruption, but not helped by events such as the Suez Canal blockage. This is causing a shortage of goods, which is adding to inflationary pressures.

The Federal Reserve (Fed) has raised its forecast for inflation to 3.4% by the end of this year, up from 2.4% in its previous projection in March. While Fed officials had predicted that current rates would be maintained until 2024, the consensus has now shifted, with two rate increases expected in 2023. The move acted as a catalyst for a reversal in those asset prices that have been rising on the expectations of higher inflationary levels, such as some commodities and more cyclically exposed sectors of the equity market. The consensus among economists and central banks remains that these inflationary pressures will probably prove to be transitory.

Technology was the strongest sector globally in June, followed by energy and healthcare. The worst performers in June were financials and materials. While the tech sector lagged during the first half of the year, tech stocks have surged higher with the change in the growth and interest rate outlook.

As a result, the Nasdaq recorded growth of 5.5% in local currency terms in June, boosted by a rally in the giga-cap companies including Apple, Alphabet and Microsoft. This compares to the FTSE All Share Index, which recorded a rise of 0.2%. The copper price fell by 7.9% as economic growth expectations declined. Meanwhile, the oil price rose by 8.4% in the month as OPEC failed to reach an agreement that would increase supply.

The speed of US monetary policy tightening relies to an extent on how fast the economy returns to full employment. While hiring is picking up in the US as the lockdown eases, the lingering effects of the pandemic are keeping many potential workers out of the labour market. Although another 850,000 jobs were created in the US, the largest monthly increase since last August, employment is still well below the pre-pandemic level.

China’s economic growth is beginning to lose steam after reducing its pandemic stimulus measures since returning to full employment. Alongside this has been a tightening of its monetary and regulatory policy, which has seen the Chinese market lag. Leading tech names have also fallen in value following a regulatory backlash, most recently against Didi Chuxing, the leading ride-hailing company and app.

While the tech sector lagged during the first half of the year, tech stocks have surged higher with the change in the growth and interest rate outlook.

Our positioning

Our investment strategy and outlook remain unchanged from June. Strong performance in July meant our equity weighting rose slightly, but we are content to maintain our positions for the time being, reflecting the ongoing strength in corporate and consumer confidence and the view that the economic recovery looks well embedded over the next 12 months. This should support both a recovery in earnings and ongoing momentum in equity prices, although we think increases over the next six months will be more modest than in the first half of 2021.

Periods of sharply rising inflation tend to be bad for all asset classes in the short term. However, equities can continue to make progress if inflation settles at a higher level than it was pre-pandemic as many companies have the ability to pass on increased costs to consumers in higher prices.

For any long-term investor, bonds look to offer few attractions from a return-seeking basis, particularly after adjusting for inflation. Government bonds in the US and UK still offer some protective characteristics and a positive nominal return, providing some insulation against external shocks and unforeseen risks.

We see few benefits of investing in investment grade credit, which offers little yield pick-up to justify the additional risk over government bonds. The yield on US high yield bonds has now fallen below 5% and is negative after adjusting for inflation. Although this situation may persist given the benign environment, it looks an unattractive prospect given the current and past risks involved with this asset class.

We see few benefits of investing in investment grade credit, which offers little yield pick-up to justify the additional risk over government bonds. The yield on US high yield bonds has now fallen below 5% and is negative after adjusting for inflation. Although this situation may persist given the benign environment, it looks an unattractive prospect given the current and past risks involved with this asset class.

The economic recovery will likely peak this summer and then begin to slow in the second half of the year but should remain in positive territory. This transitionary period is likely to be characterised by some mixed signals and volatile data, which could prove challenging for assets. However, the biggest risk remains the further spread of the Delta and other variants of Covid, which could force further economic and social restrictions.

Important information

This is not advice and you should not act on the content of this comment without taking professional advice. Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made of given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions.

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. Fluctuations in interest rates may affect the value of your investment. The levels of taxations and tax reliefs depend on individual circumstances and may change. You should be aware that past performance is no guarantee of future performance.

James Hambro & Partners LLP is a Limited Liability Partnership incorporated in England and Wales under the Limited Liability Partnerships Act 2000 under Partnership No: OC350134. James Hambro & Partners LLP is authorised & regulated by the Financial Conduct Authority and is a SEC Registered Investment Adviser. Registered office: 45 Pall Mall, London, SW1Y 5JG. A full list of partners is available at the Partnership’s Registered Office. The registered mark James Hambro® is the property of Mr J D Hambro and is used under licence by James Hambro & Partners.