09.08.2017

Market commentary: Q2 2017

John Langrish, Partner, Head of Investments

“It was the best of times, it was the worst of times” – Charles Dickens, author.

By John Langrish

The opening lines of Dickens’ work of historical fiction, A Tale of Two Cities, sets the scene for his commentary on social and political unrest in both London and Paris around the time of the eighteenth- century French Revolution. Move forward to 2017 and there are faint echoes of these economic and social tensions, which provided the backdrop to the elections held in both France and the United Kingdom in May and June. Emmanuel Macron’s decisive victory in becoming the youngest French head of state since Napoleon was won on a centrist, pro-European and anti-austerity agenda that appealed to a broad audience, including younger voters in a country where more than one in four under twenty-five year olds remain unemployed. In the UK, Theresa May’s decision to call a snap general election backfired, as the Conservatives increased their share of the vote, but lost their overall majority, against a resurgent Labour party that managed to attract both older, austerity-hit voters, as well as a more engaged and Europe- favouring youth.

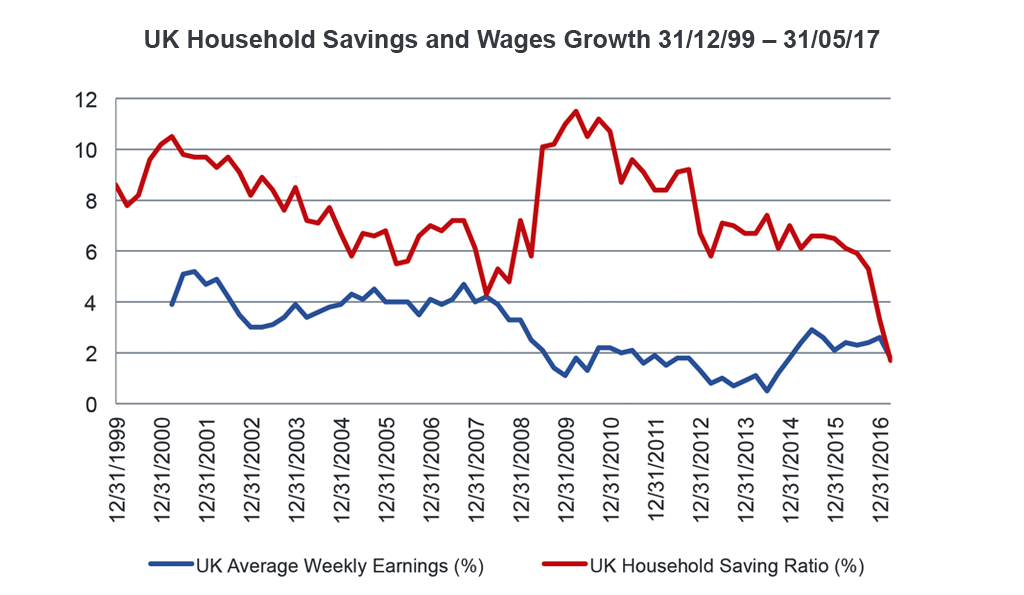

Despite the uncertain political environment, equity markets modestly strengthened during the second quarter of 2017, albeit some of the gains were given back towards the end of June, when central bankers across the globe hinted at a reduction of their previously supportive policy programmes. As the benefits of these measures have slowly worked through into the underlying economies, the US Federal Reserve has been talking more openly about tightening interest rates, the Bank of China is discouraging credit expansion and even the European Central Bank is leaning towards a less accommodative monetary stimulus package. While it is unlikely that the support will be abruptly halted, the authorities are looking to equip themselves with the requisite tools to deal with future economic scenarios. The tide has also turned against governments’ austerity measures, which have largely prevailed since the Financial Crisis of 2008. Violent demonstrations in recession-hit capitals, for example, Athens and Madrid have been replaced by votes for agendas promoting higher investment and job creation, such as that espoused by Presidents Trump and Macron and the UK Labour party. More voters now reject belt-tightening ideologies, which followed the debt-fuelled excesses of the last decade. However, problems could be storing up for the future. Figure 1, below, shows that the UK’s household savings rate (red line) is almost at a fifty year low, having risen sharply during 2008-2010, while average earnings growth (blue line) has remained lacklustre.

Figure 1

Source: Bloomberg, (June 2017) Office of National Statistics

Of course, artificially low interest rates are hardly conducive to higher savings, but buoyant retail sales, leisure expenditure and personal car registrations arguably demonstrates that many consumers are not easily weaned from poor borrowing and spending habits, even with increased uncertainty looming over Europe. Although the UK’s jobless rate is now just 4.6%, the economic recovery from 2009 onwards has been fairly uneven; typically benefiting the employed, homeowners and investors and not favouring the less well-off. Indeed, in 2017 it has been the best of times for some and the worst of times for others.

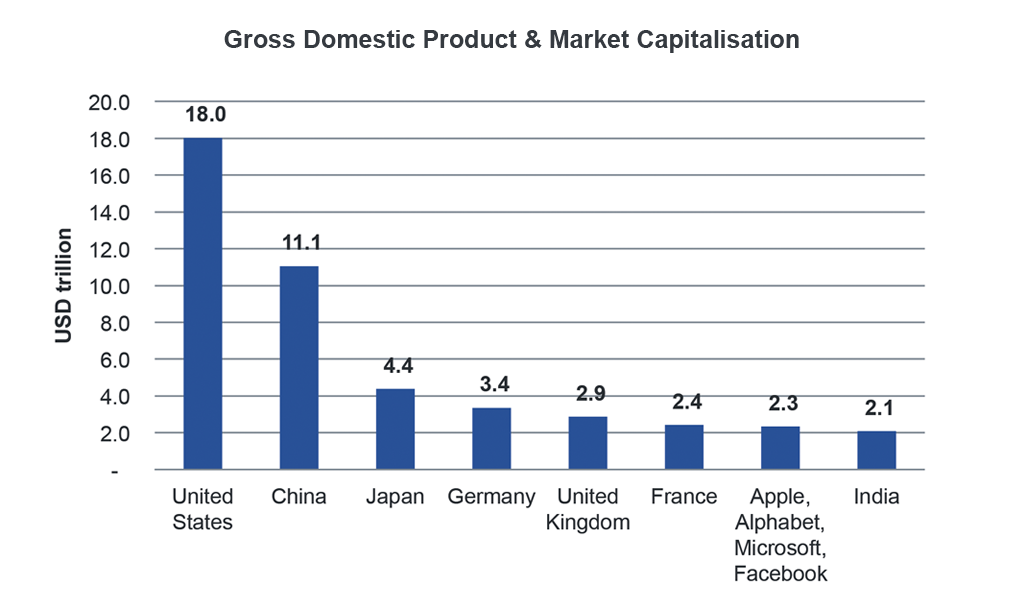

One of the strongest sources of market returns recently has been the US technology sector. Figure 2, below, shows that the combined market capitalisation of Apple, Alphabet (Google), Amazon, Microsoft and Facebook would now place them as the fifth largest nation in the world, as measured by economic activity. This is remarkable. We recognise that technological change is increasing, that the internet touches many advancing industries, helps drive efficiencies and improves countless aspects of our lives, but there are arguments stirring that the highly profitable owners of data should not only pay higher taxes, but face increased regulation and government intervention. While technology valuations are nowhere near as extreme as during the late 1990’s, share prices do not advance in straight lines and some profit-taking looks prudent in this sector.

Despite equity markets having enjoyed solid returns over the past few years, we remain optimistic that further gains could still be made. However, a move towards higher interest rates by central banks may push bond prices lower and affect near term sentiment in risk assets. For the moment, we retain our gold positions and absolute return funds, as well as elevated cash positions to benefit from any setback.

Figure 2

Source: Source: Federal Reserve Economic Data

* Apple, Alphabet, Amazon, Microsoft, Facebook Source: World Bank (May 2017), Bloomberg

John Langrish

Posted 9 August 2017

You should not act on this content without taking professional advice. Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made of given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions.

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. Fluctuations in interest rates may affect the value of your investment. The levels of taxations and tax reliefs depend on individual circumstances and may change. You should be aware that past performance is no guarantee of future performance.

Image: iStock