26.01.2017

Market commentary: Q4 2016

Mark Leach, Partner, Portfolio Manager

“I don’t know where I am going from here, but I promise it won’t be boring” – David Bowie

By Mark Leach

At the start of 2016, few would have predicted that either the UK would vote to leave the EU or indeed a New York based billionaire businessman and television celebrity would become the 45th President of the USA.

Looking ahead, the political calendar of 2017 is shaping up to be equally as challenging as populist parties across Europe, emboldened by the events of 2016, look to challenge the status quo.

Driven by years of stagnant growth and policies that appeared to widen the gap between the rich and the poor, the upheavals of 2016 ushered in a new wave of populism and with it a new investment landscape.

As the year began, deflation was the predominant risk facing the global economy. However, just twelve months later, investor attention has shifted focus to higher inflation and rising interest rates. This brought to an abrupt end the bull market in bonds and yields rose in many major markets and precipitated a change in leadership in equity markets, as cyclical, or economically sensitive, companies outperformed their higher quality bond-like counterparts.

Political rhetoric of fiscal austerity and budget surpluses have been replaced with promises of infrastructure investment, tax cuts and in the case of Donald Trump, protectionism. The election of Trump and the Republicans’ control of Congress had an immediate impact on markets. The downward trend in bond yields reversed sharply post the election as investors moved to discount higher inflation and rising interest rates.

Figure 1 shows the US 10-Year yield rising from 1.3% to 2.4% by the year end. In reality, however, the election result merely accelerated a trend that was already evident in the US economy. Falling unemployment, rising wage growth and nascent inflation formed the foundation on which the Federal Reserve increased rates in December 2015, the first time since 2006.

Subsequently, the tightening cycle was put on hold as falling commodity prices at the start of 2016 threatened to stall the recovery, but robust GDP growth, a rebound in commodity prices, and the potential for greater fiscal stimulus from a Trump government, precipitated a second rate rise in December 2016.

Figure 1

Source: Bloomberg, 09/01/2017

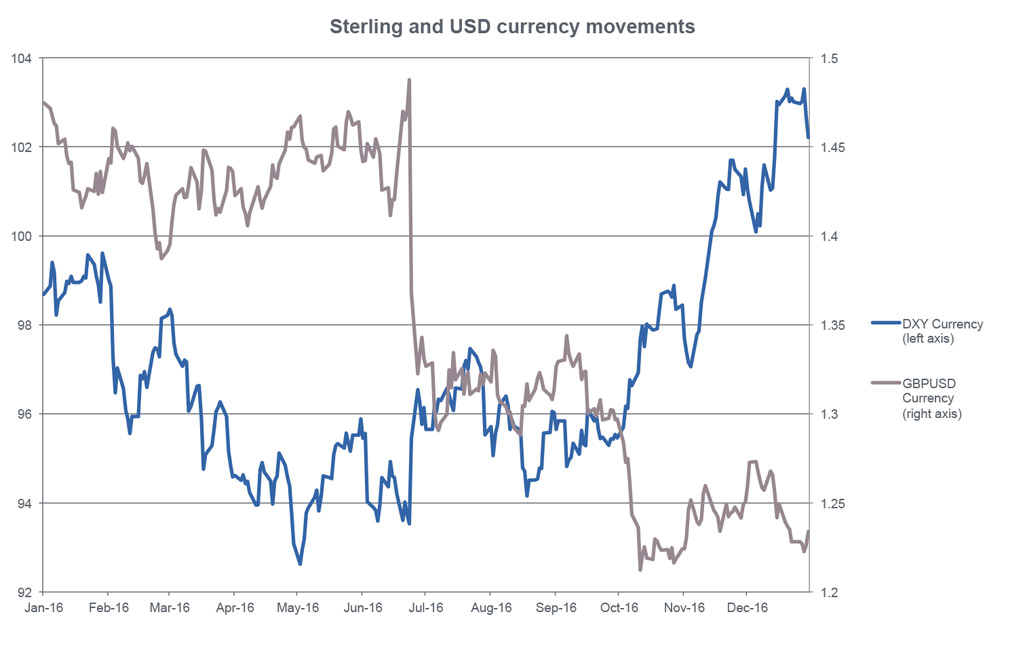

While equity returns were resilient during the year with the FTSE World Index and the UK FTSE All Share up 9.9% and 16.8% respectively, in local currencies, foreign exchange markets were considerably more volatile. Sterling fell 16% against the dollar (Figure 2, brown line) while the dollar (blue line) strengthened against the basket of currencies, rising 10% from the low in May.

Figure 2

Source: Bloomberg, 09/01/2017

Sterling’s weakness reflects considerable uncertainty as the UK looks to redefine its relationship with the EU, the destination of 45% of UK exports. Conversely, the dollar’s strength appears to be well underpinned into 2017 and beyond, as interest rate disparities between the US and other regions continue to widen.

With valuations high in both equities and bonds, we started the year cautiously on both asset classes, and looked to balance risk using assets such as absolute return funds as well as holding a higher than normal level of cash. In fixed income we favoured the inflation protection offered by index-linked gilts in the UK, and in the US, conventional government bonds, which offered some yield as well as exposure to the dollar. Within equities, portfolios were skewed to international companies with little exposure to the UK economy or sterling.

Our investment philosophy is predicated on the view that over the long term, equities offer the best means of protecting capital from the destructive forces of inflation. As events unfolded during the year we were quick to recognise the changing environment, adding to equities, with a preference for companies that have greater sensitivity to economic growth.

Given the rise in bond yields, our enthusiasm for conventional US government bonds has waned and the majority of our fixed income allocation now resides in inflation protected assets. We remain, however, mindful that equity valuations are, on aggregate, above historical averages and that the investment cycle is starting to look long in the tooth. Therefore, we continue to maintain a higher than normal allocation to cash, but with the underlying composition of our risk assets reflecting the new paradigm of burgeoning inflation and rising interest rates.

Published 26 January 2017

You should not act on this content without taking professional advice. Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made of given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions.

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. Fluctuations in interest rates may affect the value of your investment. The levels of taxations and tax reliefs depend on individual circumstances and may change. You should be aware that past performance is no guarantee of future performance.

Image: Adrian Lourie/Alamy Stock Photo