24.09.2020

NS&I cuts: Where next for your cash?

Charles Calkin, Partner, Financial Planner

Charles Calkin

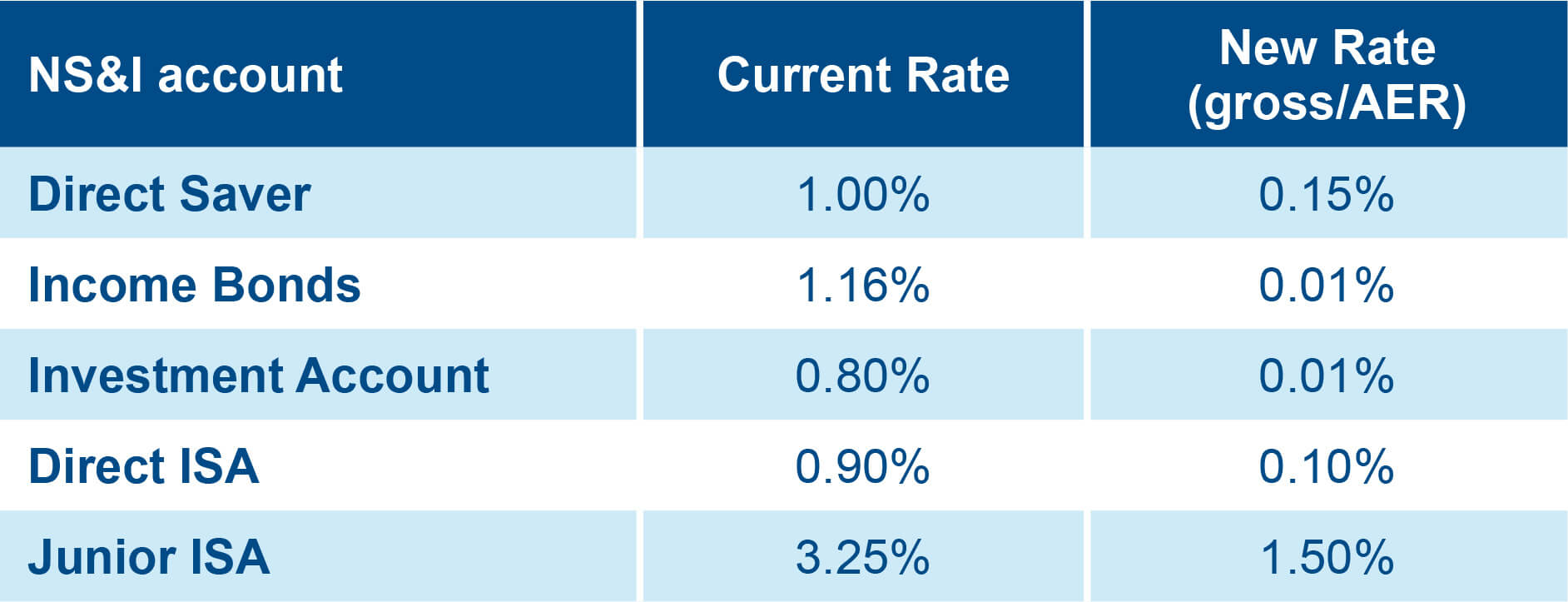

The Treasury-backed National Savings & Investments (NS&I) has announced drastic cuts to the rates of interest it offers. For its 25 million customers this raises a serious question: should you move your money?

NS&I has long been a natural home for cash savings – some accounts pay gross and you do not have to worry about the institution going bust because it is government-backed. It has good administration and has long offered close to market leading rates consistently. But these are significant reductions and the move will be tough on those hoping to generate something close to a real return on their cash savings. So what are your options?

Shop around

With the Bank of England considering negative interest rates, the likelihood is that all banks and building societies will be looking to reduce their rates – if they have not already. This may be a good time to lock in what rates you can. The best buy tables show that lesser-known institutions will give you close to 1.35% for two years. It is important before considering a deal that you check that the institution is covered by the Financial Services Compensation Scheme. This means if the bank or building society goes into liquidation you will receive up to £85,000 (double for a joint account) back. Do not invest more than that limit – spread your money around if you have large cash amounts to save.

Consider premium bonds

The prize pool on NS&I premium bonds has been reduced, but only to 1%. That means the odds of a £1 premium bond number winning a prize will shrink from 24,500 to one to 34,500 to one. There will still be two £1 million prizes but the estimated number of £100,000 prizes will fall from seven to four and the number of £50,000 prizes from 14 to nine. Investors may take the view that if returns are going to be so low generally they may as well be in with a chance of earning a tax-free million, even with these poorer odds.

Increase your risk

Those for whom returns on cash are important may have to start looking to go up the risk spectrum. We have been encouraging some clients with large cash savings to let us invest a proportion in short duration investment grade bonds and what are known as ‘liquidity funds’. These aim to preserve capital while generating a modest return – often less than 1% after costs – but better than nothing, which is what the NS&I income bonds rate of 0.01% pretty much will be from November.

Many cautious investors sit on too much cash because they think that the alternative is equities, which they consider high risk. A good wealth manager can build you a portfolio that truly reflects your attitude to risk and need for return, using a broader range of investments. This could mean you have a better balance of investments and your money generates better returns without you going beyond your comfort zone.

Avoid temptation

One other concern I have is that these rates will make many people more vulnerable than ever to fraud from scammers offering what looks like an attractive return. They may also be tempted into regulated products that appear safer than they are – last year alone investors are estimated to have lost £1 billion in collapsed mini-bonds.

If it looks too good to be true, it probably is.

James Hambro & Partners specialises in looking after those with £1 million or more in investable assets. We are always happy to talk to investors worrying about how to make their savings and investments work more effectively.

Changes taking effect to NS&I returns from 24 November 2020

Charles Calkin

Posted on 24 September 2020

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.