08.10.2021

October investment update

James Beck, Partner, Head of Investments

The sugar rush is over – central banks have signalled that the period of maximum support has ended, and monetary policy will be reeled back. As the economy sobers up, where should investors focus their attention?

While it might feel like a rather dry topic, monetary policy is of vital interest for markets. Throughout the COVID-19 crisis, central banks slashed interest rates and poured liquidity into the economy to keep markets functioning and ensure that companies had access to funding to sustain them through the lockdowns. As economic activity gets back to normal, central banks are starting to withdraw this emergency support.

But the economic picture is complex. As well as the potential for new virus variants to bring fresh rounds of restrictions, the release of pent up demand has seen inflation – one of the key targets of monetary policy in normal times – on the rise.

Investors are watching carefully to assure themselves that the central banks are managing the transition to more conventional monetary policy deftly. With near zero rates and the wave of liquidity having acted as a support to asset prices, the gradual return to normal is likely to see a choppier path for markets than we’ve seen so far this year. While the outlook remains positive, don’t be surprised by short-term falls and recoveries in the coming months as investors adjust to the changing circumstances.

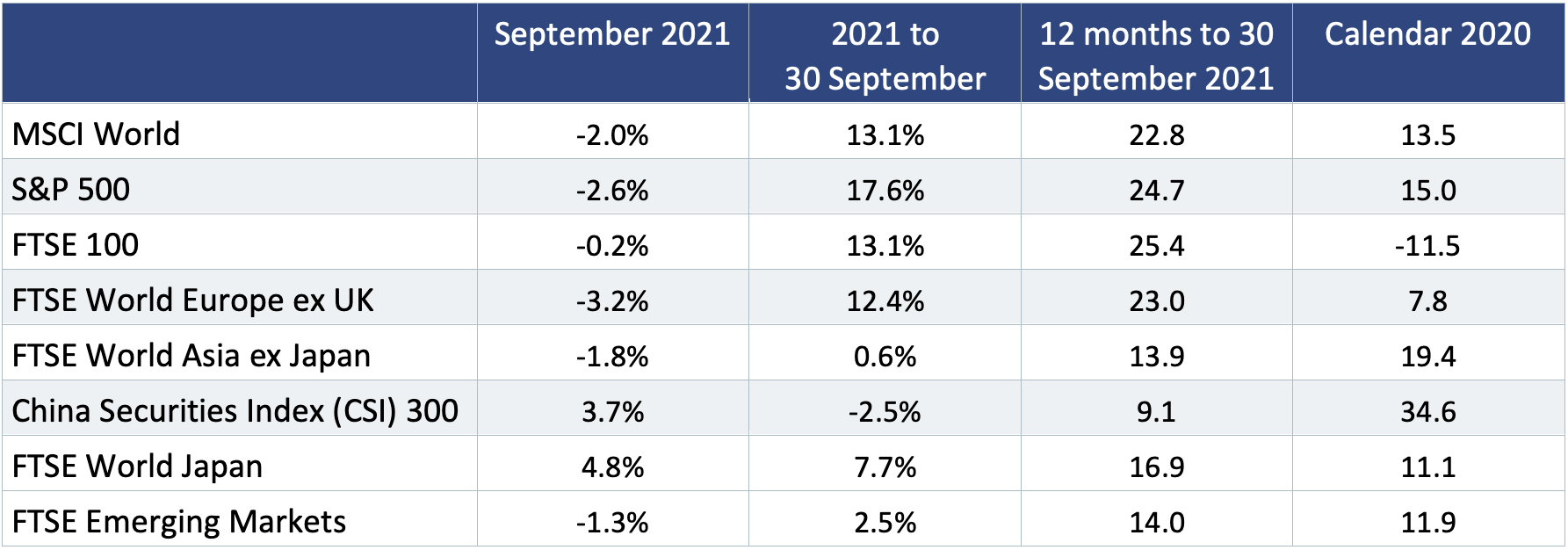

Investors return to fundamentals

The end of September marks the end of the third quarter. While these cardinal dates are somewhat artificial – markets move on a less regimented cycle – they do provide useful points for reflection.

Looking back at equity markets in the third quarter, it’s striking how the highly cyclical period that followed the announcement of the vaccines at the end of 2020 has given way to a focus on company fundamentals and ability to grow in the longer term. As a result, companies that benefit from structural, sustainable growth trends – established companies with strong positions in their industry and pricing power – have seen improved returns.

These types of company are at the centre of our equity investment philosophy. While they were out of favour earlier in the year, we understood that when the sugar rush of reopening wore off the enduring quality of these companies would still stand out. Sticking with our convictions through the earlier part of the year has been rewarded.

Central banks: No more easy money

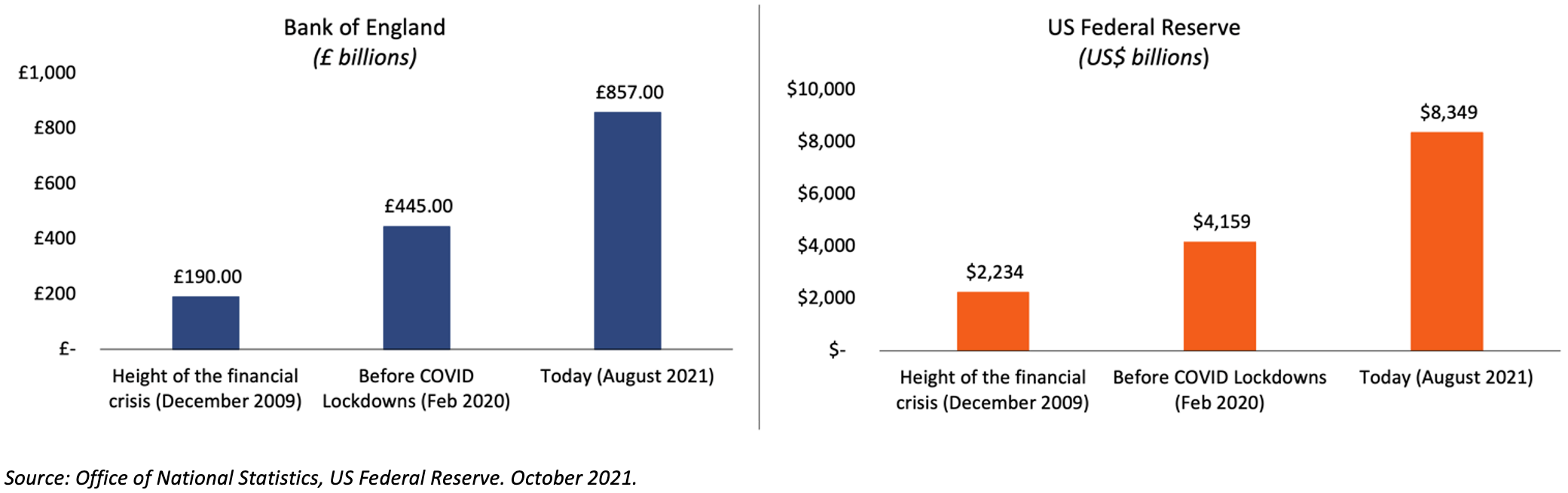

The Norwegian central bank – Norges Bank – was the first among the G10 economies to fire the starting gun on tightening last month, raising rates from zero to 0.25%, but they are unlikely to be the last. Both the US Federal Reserve (the Fed) and the Bank of England (BoE) made announcements consistent with gradual policy tightening. The trend for monetary tightening is clear: we are past the point of maximum support.

The Fed said that assuming the current trend in COVID-19 remains on track, fund purchases are to gradually reduce through the year, a process widely referred to as ‘tapering’. Purchases are likely to come to an end in the middle of 2022, although the Fed stopped short of committing themselves to a definite timetable. The BoE Monetary Policy Committee voted to keep current policies in place but edged closer to the possibility of a rate rise, perhaps in the early months of 2022 and possibly even earlier.

As a reminder, the Fed has been buying between $40 billion and $80 billion a month since the middle of last year. The way the BoE buys bonds means that tapering is less of an issue, but the question of when these bonds will return to market – and thus mop up excess liquidity – is still unanswered.

Central banks in the US and UK now hold record-busting amounts of assets

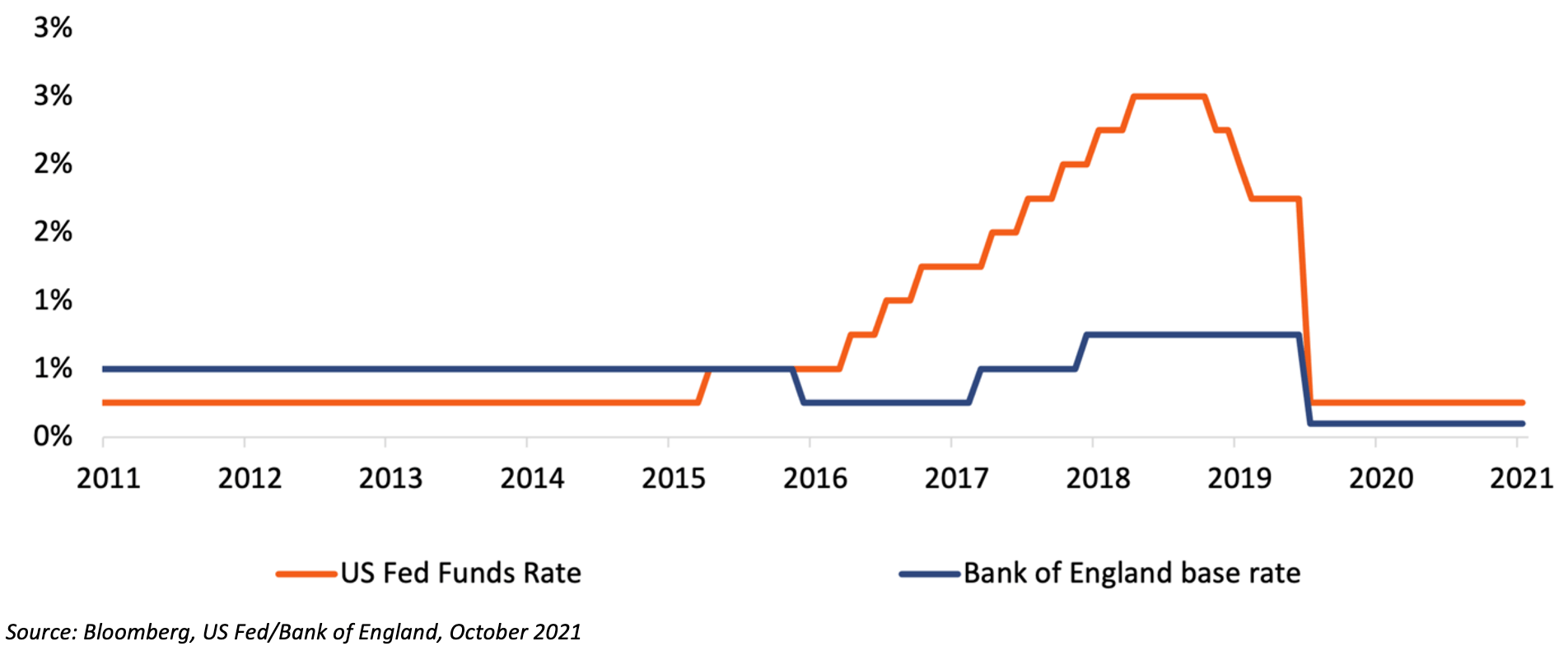

Similarly, interest rates are at historic lows, even compared to what we saw during the financial crisis. The pace and scale of rate rises – which increases the cost of raising money for development for companies and can erode the value of bonds issued at lower rates – is also a critical matter for investors.

Interest rates are at historic lows but could start to rise as early as 2022 –

maybe sooner

Markets were volatile in the days ahead of the BoE and Fed meetings in September, but seemed at ease with the tone of these announcements in the aftermath. However, as policy tightens we’re likely to see further shifts in sentiment as investors adjust. The path of inflation has also proved to be unpredictable, and this could lead to further instability in equity markets as the situation evolves.

Inflation still has plenty of puff

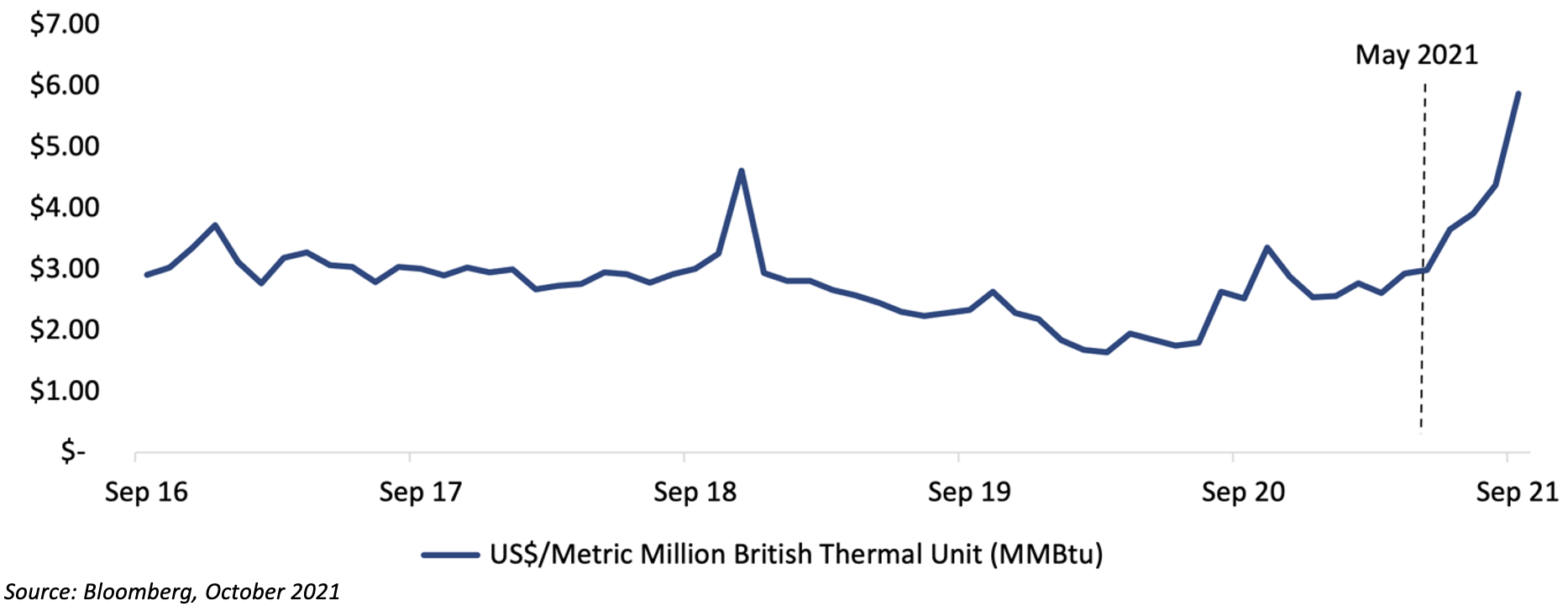

Over the month it’s become clear that inflation is proving more enduring than markets previously thought. Supply chains continue to look stretched and commodity prices have risen as the surge in economic activity has had an impact on demand. Labour shortages are having the double impact of exacerbating supply chain problems while also driving up wages. In the UK you will have read the headlines about the 100,000 deficit of HGV drivers, while the service industries are also experiencing difficulties and the situation is especially acute in the hospitality industry.

Rising energy prices are also having a big impact. The price of wholesale natural gas has trebled since the summer and this is feeding through to electricity prices for consumers. This is before winter hits and falling temperatures will see demand from energy companies rise, which has the potential to send prices even higher. Structural problems in energy supply and the limited capacity to store gas, particularly in the UK, which would enable energy companies to ride-out price spikes could contribute to continuing price rises.

Wholesale price for natural gas has spiked sharply since May

Central banks seem relaxed about inflation for now. Both the Fed and the BoE suggested they see these pressures as temporary and expect inflation to return to within their 2% target range over the next 12 months. But the situation is not entirely certain. If the signs change, central banks could have to accelerate their tightening measures, which will have a similar impact on financial conditions.

We are well positioned for rising inflation, having added to our equity exposure earlier in the year. We focus on companies that have pricing power in their sector and strong positions against competitors. These companies are better placed to pass on high input costs to consumers.

We also have a small but significant position in gold, an effective hedge against inflation becoming unbound, particularly in an environment of zero returns on cash and negative real yields for government bonds.

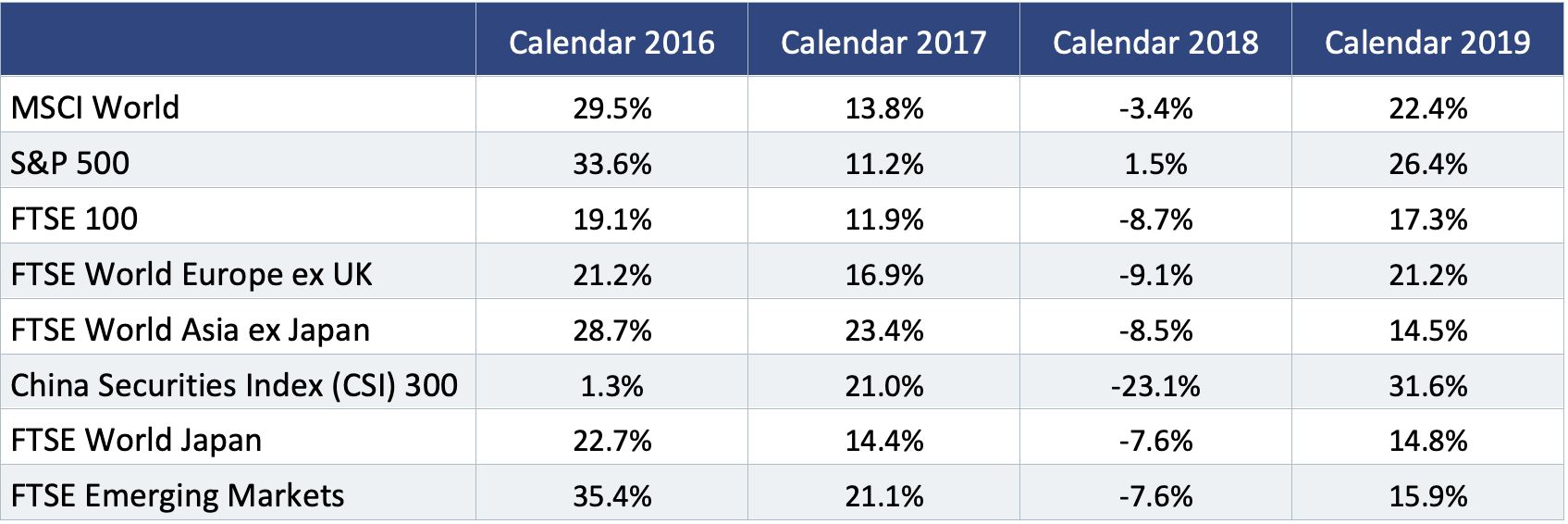

Long-term market performance

All data calculated on a sterling basis including income. Past performance should not be relied on as an indicator of future returns. Source: Bloomberg/James Hambro & Partners. October 2021

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.

James Hambro & Partners LLP is a Limited Liability Partnership incorporated in England and Wales under the Limited Liability Partnerships Act 2000 under Partnership No: OC350134. James Hambro & Partners LLP is authorised & regulated by the Financial Conduct Authority and is a SEC Registered Investment Adviser. Registered office: 45 Pall Mall, London, SW1Y 5JG. A full list of partners is available at the Partnership’s Registered Office.