James Beck, Partner and Head of Investments

Last quarter’s commentary began with a quote from Citigroup’s Chief Strategist, Tobias Levkovitch, who stated that almost all expansions were ultimately killed by the actions of the US Federal Reserve. He was wrong, the Fed is in the clear, as responsibility for the death of the longest economic expansion on record can be laid firmly at the door of the coronavirus pandemic.

The equity bull market officially ended on 12th March, precisely 11 years and three days after it began in March 2009. Having taken 4,005 days to reach its record high the S&P 500 took only 16 days to collapse by 20% and thereby officially enter ‘bear market’ territory. This marked the second-fastest bear market in history bar the autumn crash of 1987 and shortly after became the fastest 30% decline on record.

The numbers associated with the first quarter of 2020 are dizzying and bear comparison with some of the toughest periods for investment and the real economy in history – the 1930s Great Depression, the bursting of the technology bubble in 2000 and of course the global financial crisis of 2008. The difference this time is the near-universal collapse in economic activity and the speed with which it has happened; the impact being felt in a five-week period during which the world moved from steady progress to full-blown crisis.

The first quarter closed with the MSCI World Equity Index down 21%, the S&P 500 declining 20% and the UK’s FTSE 100 falling 24%. The US technology and healthcare-heavy Nasdaq index fared better but still lost almost 15% of its value. The losses were not confined to the equity market with corporate bonds (-6%), high yield debt (-14%) and commodities (-42%) falling in unison. Brent crude oil declined by 65%, its worst quarter on record, as a spat between Saudi Arabia and Russia saw supply flood the market just as demand collapsed.

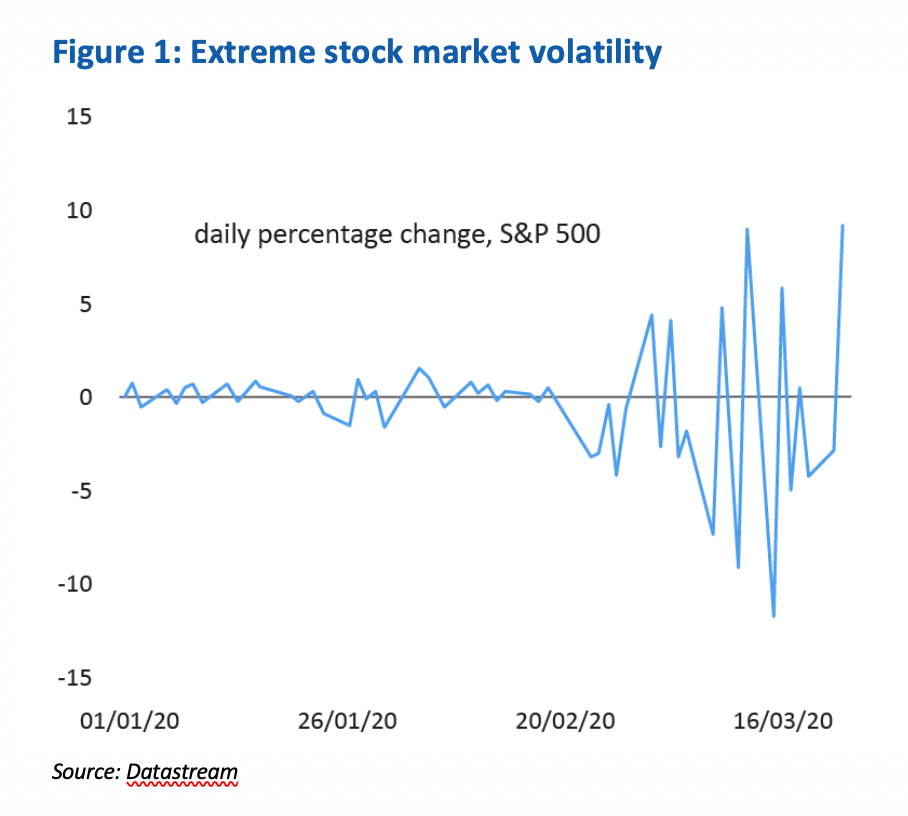

This March madness saw daily market swings of such ferocity that by the end of the month a 3% move would be greeted with little more than a shrug (Figure 1). The VIX measure of volatility and stress in equity markets averaged three times typical levels seen over the prior decade. Not even during the peak periods of 1929 or 2008 did markets display such violent day-to-day moves in value.

The only ports in this storm proved to be the traditional havens of UK and US government bonds, gold and cash. But even these safe harbours were unable to avoid the turbulence completely, with gold at one point falling by over 12% in just 10 days before recovering its poise into the end of March.

Things looked even worse as recently as 23rd March, when most major indices had fallen by more than 30%. The partial recovery experienced in the final days of the quarter was built on hopes that the colossal policy response would be sufficient to offset the financial and economic implications of Covid-19 and that Italy and Spain might be seeing a peak in their infection rates, providing a path to the loosening of government lockdowns.

From isolation to suspended animation

The immediate impact of Covid-19 needs little explanation, we are all living with it. The cacophony of expert opinion and an absence of anything else to provide a distraction from the 24-hour news media has meant each of us is now a budding amateur epidemiologist. We understand the importance of social distancing, of flattening the curve to slow the spread of the virus and thereby the potential for it to overwhelm the health services.

Whether these policies are warranted and effective will only be known in hindsight and are questions better left for the inevitable political post-mortem. From an economic and investment perspective, the decision has been made to sacrifice the health of the economy to protect the health of the population and this is what now matters for markets.

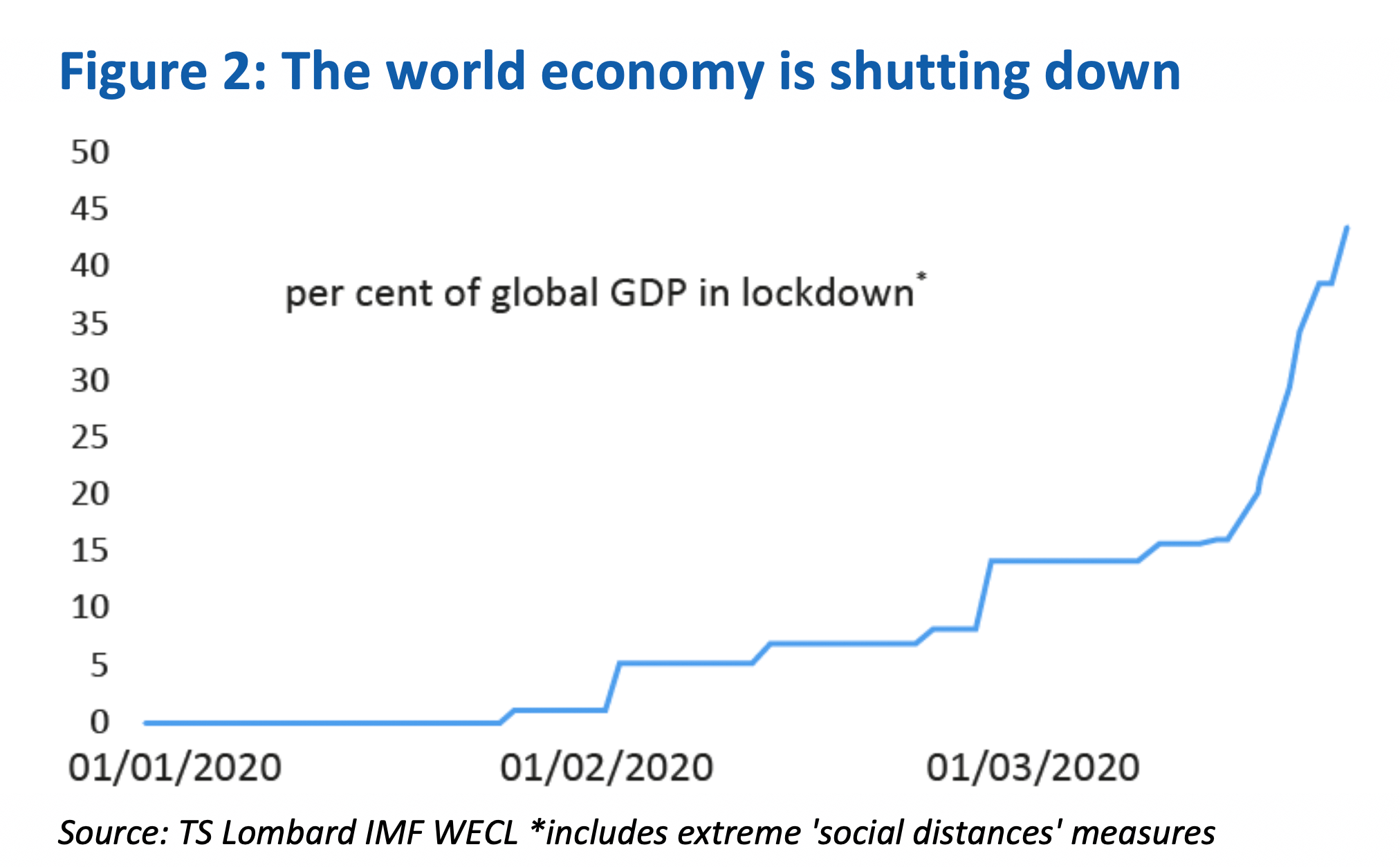

At the end of March more than 50 countries, responsible for 50% of global Gross Domestic Product (GDP), were in varying degrees of lockdown (Figure 2). The job now is assessing how dangerous these containment measures will prove to be for the global economy and the permanence of any damage. Will the treatment end up being worse than the virus?

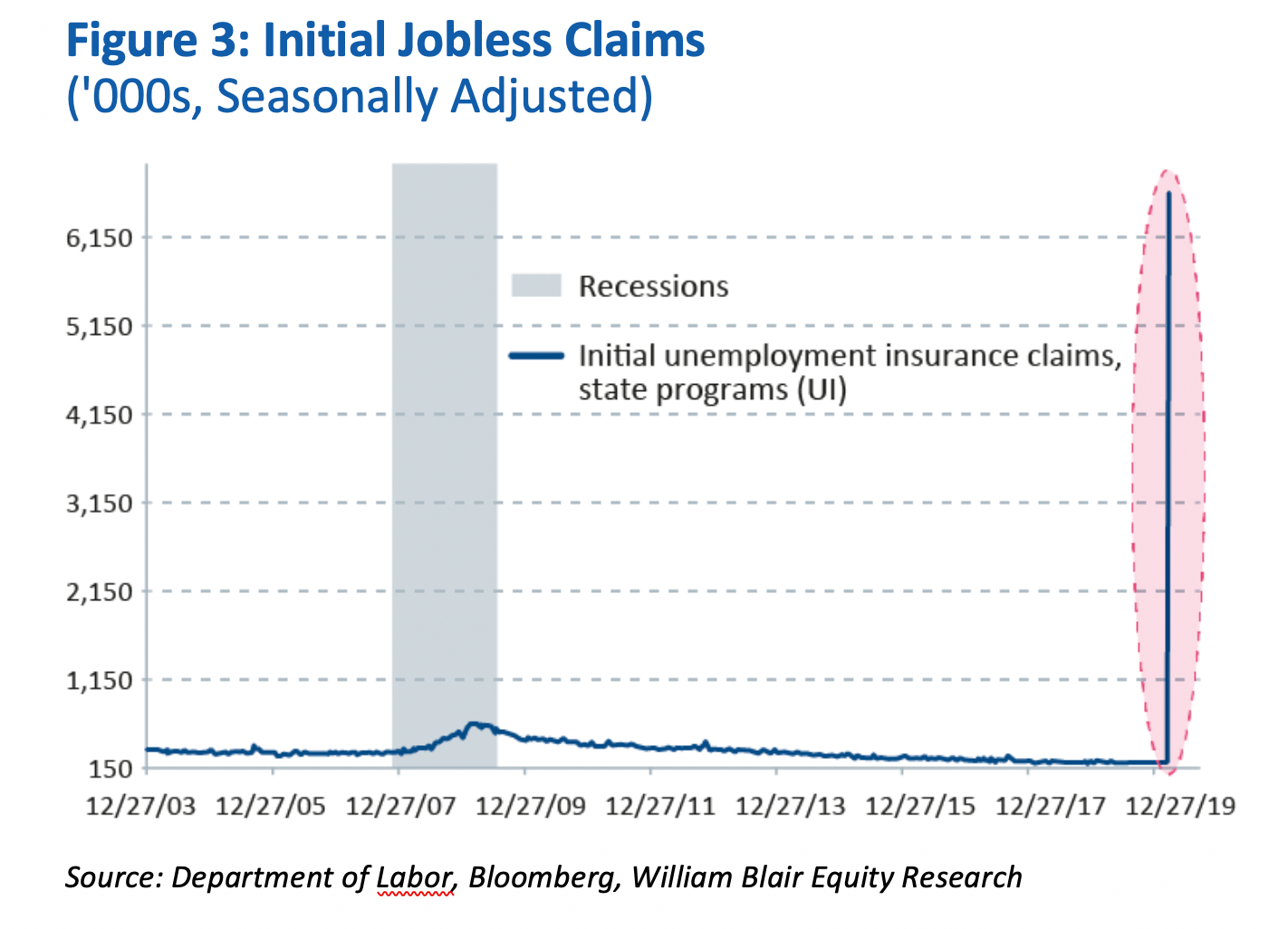

We are beginning to see the economic impact of policies that have, in effect overnight, brought to a grinding halt much of global economic activity. A rapid increase in unemployment has been an immediate and obvious consequence, with the weekly jobless reports in the US showing a total of nearly 17 million new claimants in just three weeks (Figure 3). This dwarfs the 2008 crisis both in terms of speed and scale. It seems certain that the unemployment rate in the US will increase from 3.5% in February to somewhere nearer 15% in April, higher than the 10% registered at the peak of the financial crisis.

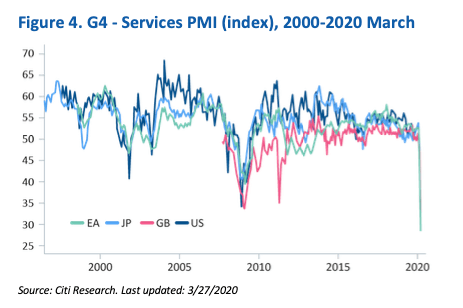

While the virus appeared isolated to China and principally Wuhan province, focus was on the shutdown of manufacturing and impact on an increasingly integrated global supply chain. As the virus has moved west the infection has spread to the typically more resilient service sector. Recent purchasing managers index (PMI) data, which gives a broad measure of economic activity, suggests output has fallen by a record amount, eclipsing all previous recessions (Figure 4).

This should not be a surprise, as for some businesses activity has ceased entirely. Economists at T.S. Lombard estimate that in the US ‘social distancing’ has shut down industries that account for 30% of private sector jobs (35 million). Food services, recreation, air travel and casinos alone account for 12% of US private sector employment and 8% of consumer spending.

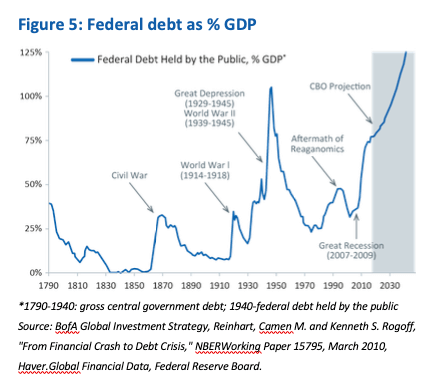

A sharp drop into recession now seems inevitable, with many commentators drawing parallels with wartime. Although the social impact cannot be anywhere near comparable, the immediate economic effects may be similar; JP Morgan estimates that in the second quarter of this year we will experience the sharpest decline in GDP since World War II and this will be matched by an explosion in budget deficits previously associated with periods of global conflict (Figure 5).

The OECD in their snappily-titled report, “Evaluating the initial impact of Covid-19 containment measures on economic activity”, estimated that the median economy faces an initial decline in output of around 25%.

Whilst we will see some contraction in GDP in the first quarter, the second quarter is expected to bear the brunt of the drop in economic activity. We will not know the full extent until we near the middle of the year.

Everything including the kitchen sink

Governments and central banks have recognised that economic activity faces its biggest and sharpest contraction in modern times. They have responded rapidly and with remarkable scale. The lessons of 2008 loom large and highlight the need to ‘go big and go early’ to limit damage from what is effectively a global natural disaster.

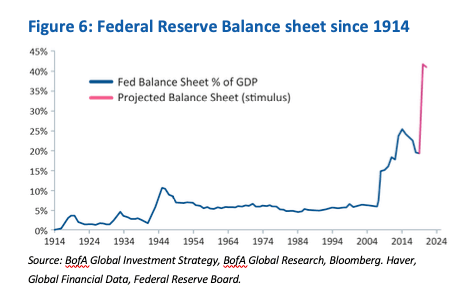

Central banks acted as first responders, cutting interest rates and flooding the system with liquidity. The increase in the size and breadth of intervention is beyond anything we have seen before – quite remarkable given they have purchased $13 trillion of financial assets since Lehman Brothers failed in the autumn of 2008.

Having cut interest rates by 1.5% since the beginning of March, the Federal Reserve has moved beyond simply buying US government bonds, committing to buy first investment grade corporate bonds and most recently announcing a further $2.3 trillion package which will allow it to buy high yield (or junk) bonds. They have acted decisively to prevent an economic shock from evolving into a credit crisis (Figure 6). The Bank of England, Bank of Japan and European Central Bank have shown a similar willingness to do whatever it takes to ensure the ongoing functioning of financial markets.

Whilst central banks have assumed responsibility for the financial system, lower interest rates do not replace lost wages and cash flows from idled businesses. It appears that governments understand the enormity of the situation and, having imposed the lockdown, they have a responsibility to keep companies and consumers afloat and limit the permanent damage until business-as-usual can return.

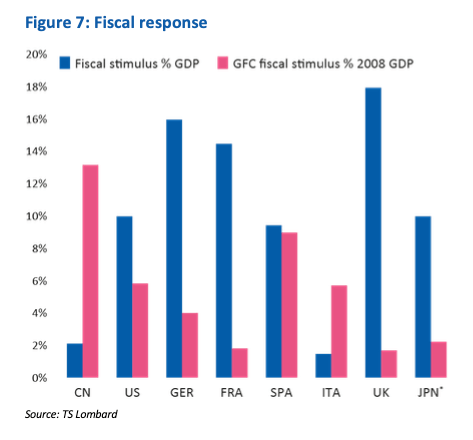

To date, the fiscal impulse announced by the largest economic powers looks set to surpass 5% of annual global GDP, well in excess of that provided during the global financial crisis (Figure 7).

The policy response has been impressive but represents disaster relief rather than stimulus – governments cannot spur demand when the world is in quarantine. Undoubtedly the odds of success will diminish the longer it takes for the world to return to a sense of normality. However, this is not a depression and the speed and size of the response gives us encouragement that it will not become one.

“Nothing is so permanent as a temporary government program” – Milton Friedman

Whilst policymakers may prove successful in averting the worst of the potential permanent structural damage, further fiscal stimulus will be needed to reaccelerate growth in the aftermath of the lockdown. With the Bank of England now providing direct lines of credit to the government and the Federal Reserve extending its reach alongside the US government the lines between monetary and fiscal policy are becoming increasingly blurred.

The independence of central banks could easily become a longer-term casualty of Covid-19 with the next stage of policy defined by Modern Monetary Theory as central banks are called upon to directly fund government infrastructure spending.

Dividends join the casualty list

One of the lasting legacies of the previous crisis has been the destruction of secure sources of income from cash deposits and bonds. With interest rates unable to climb sustainably off their lows, huge swathes of the government bond market offer low or even negative real yields, with the distorting impact of quantitative easing writ large.

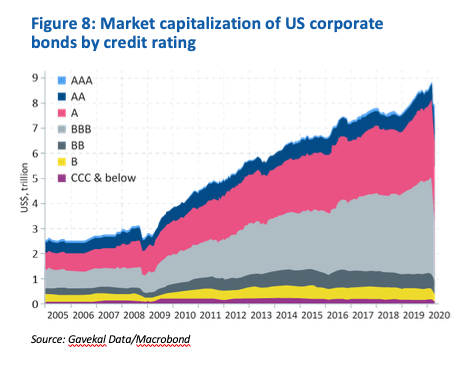

Investors have been increasingly driven into more exotic and higher risk areas of the fixed income markets with investment grade corporate bonds quickly making way for high yield, emerging market debt and collateralized loans investments with uncertain liquidity, complex covenants and increased threats of default.

This ‘reach for yield’ supported a near trebling of the outstanding corporate debt in just the US market to nearly $9 trillion between 2009 and 2020 (Figure 8).

We have deliberately avoided such a strategy, given the returns looked too low to compensate for the much greater risks associated. The dangers have been laid bare in recent weeks, with sharp falls in higher risk debt markets even before we begin to witness the defaults associated with a recessionary environment.

The dividends generated by established, high quality companies provide a more attractive long-term source of income. These can offer both higher starting yields than bonds and the potential for that income to grow over time in line with growth in companies’ earnings and cashflow. For long-term investors, this continues to make sense. However, the present crisis is threatening the current level of dividends in two ways:

- Given the uncertain nature of the duration and impact of the shutdown, many companies are choosing to cut dividend pay-outs first and ask questions later.

- Governments and regulators are explicitly restricting the ability of companies in certain sectors to pay dividends.

At the time of writing, 20% of the top 600 companies in Europe and 25% of the FTSE 100 had cut, suspended or deferred their dividends. This is already nearly twice as many as in the financial crisis and the number will grow.

In previous recessions management teams did all they could to preserve the dividend, but this time it has been different with the speed of the slowdown forcing the retention of cash within the business over shareholder distributions. With investors increasingly accepting of this policy we expect many more businesses to adopt this approach out of precaution even if they could comfortably maintain payout ratios.

There will also be a reaction to the increasing involvement of governments and the court of public opinion. Politicians in France, Germany and the US have announced limitations to dividends for companies that receive state aid during the crisis. The European financial sector has come in for attention with the UK Prudential Regulatory Authority making it clear that UK banks should withhold dividends and the European Central Bank ordering their European counterparts to refrain from making distributions this year.

Dividend income will be lower this year, with cuts already confirmed in higher yielding sectors such as property and financials. Current dividend futures in Europe and the UK predict a greater than 50% fall in dividends in 2020, in line with potential reductions in corporate earnings. This may prove too pessimistic and would be worse than in 2008.

For less cyclical sectors the impact on dividends will undoubtedly prove transitory and as the gloom lifts so pay-outs will return. Yet with governments having already extended their reach there will be a temptation for their influence to linger beyond the crisis. With the rise of populism already well established, one of the enduring impacts of the crisis might prove to be a renewed focus on the balance of returns between shareholders and other stakeholders such as employees and society. This focus will inevitably fall on the higher profile, highly regulated and strategically important companies.

A focus on the detail

Should the lockdown and economic impact prove short-lived then the liquidity and support provided by the authorities will provide a base for a recovery in sentiment, activity and investment markets. We hope that this proves the case, however, in a world where the uncertainty over the length and depth of the economic impact still reigns, a more cautious view seems warranted for now.

Chinese data suggest that when the lockdown ends it takes longer for consumer behaviour to return to normal than for manufacturing to recover. This is intuitive, it is easier to get people back to work than it is to persuade individuals to behave in the way they did prior to the lockdowns given the increased risk to health, jobs and earnings. This has a greater bearing on the service-led economies of the US, UK and mainland Europe. Hopes of a swift return to the previous trend look overly ambitious. We have retained a more defensive positioning through the sell-off and have not been tempted to speculate as to the stability of the rally seen in equity markets in the last two weeks.

Now is not the time for sweeping macro-economic predictions, and so our attention has been on the individual holdings within portfolios. With so many companies withdrawing their guidance any attempt to forecast corporate earnings is founded on a ‘best guess’ basis and so adds little benefit; we have focused on two things, the balance sheet and the business model.

First, we are making sure that our companies are strong enough to survive a prolonged period of economic disruption and emerge in a stronger financial position than their competitors. These are the survivors and we have applied a pessimistic view of the future to avoid permanently losing capital.

Having identified the survivors we are looking to ensure that we are invested in companies that have the right business models, operate in the right industries and have the right management team to succeed when the recovery comes, as it inevitably will.

Whilst this period will prove a catalyst for change and innovation – there cannot be many who haven’t taken part in a family or work quiz over Zoom in the last four weeks – the more immediate impact will be an acceleration of trends that were already in train. In a world where people have been confined to barracks the growth in online retail and the associated migration from cash to card and digital payments will only increase; this will support not only the likes of Amazon but also the providers of the payments infrastructure such as Visa and Mastercard.

Business travel, already challenged by the desire of companies to burnish their environmental credentials, will be further impacted by both the need to reduce costs and a realisation that some face-to-face meetings can be replaced with video. With 65% of profits for the airline and hotel industry derived from business travel, there will be knock-on effects across many industries.

A focus on conservatively financed businesses, looking to generate sustainable returns and operating in markets or industries with durable structural growth should provide a strong foundation however unclear the immediate trajectory of the world and markets.

Beyond the crisis

Making bold predictions about the economic future is fraught with danger. But we know from history that many of the seeds of the next cycle are being sown through the actions of policymakers today. At the very least we expect that Covid-19 will act to hasten tectonic shifts that were already in motion.

The long period of globalisation since the fall of the Berlin Wall was already in retreat, pushed back by increasing income inequality, rising populism and a burgeoning nationalism in politics. This reversal into a creeping protectionism found its clearest expression in a strategically motivated economic cold war between China and the US.

A global disaster such as the coronavirus might have provided an opportunity to halt this trend. But rather than lead to a new wave of collaboration, the first truly global health crisis has prompted an acceleration in the collapse in international co-operation.

In Europe borders have closed, member states have hoarded medical supplies and the Maastricht Treaty rules on fiscal discipline have been jettisoned in a rush to protect domestic economies. Relations between China and the US, which seemed to be thawing as recently as January, are deteriorating rapidly as the blame game begins. Further recriminations will surely follow once the acute phase of viral control is over.

The retreat from globalisation will not be confined to the political sphere. The supply chain interruptions caused by the manufacturing shutdown in China will cause a reassessment by companies of their supplier base. There will be pressure to onshore production, particularly of medical supplies and products deemed of national security. This will have implications for costs, impacting margins and potentially place greater bargaining power in the hands of workers as manufacturing returns home.

All this comes at a time when government involvement in the economy is on the rise. With many western governments elected on a nationalist agenda the recent emergency intervention could easily become permanent with associated implications for regulation and greater state intervention to protect national interests and reduce inequality. Only last week Margarethe Vestager, the powerful EU competition commissioner, urged European States to take equity stakes in companies to ward off Chinese buyers. Government involvement in business has rarely improved efficiency or reduced cost.

Increased intervention will need funding. With tax rises unpalatable in a recession and austerity no longer acceptable, even to the fiscally conservative Germans, budget deficits will soar.

Yet with bond yields at lows and central banks determined to keep them there for the foreseeable future, the cost of this debt appears manageable. Governments will therefore inevitably turn to central banks, seeking either tacit or explicit funding for policies to stimulate growth. The long-cherished independence of these institutions will struggle to survive as they are increasingly seen as tools of government.

The combination of increasing protectionism, ballooning government deficits and a more intrusive state has caused some investors to raise the spectre of inflation. The massive policy response to COVID-19, especially the popular wartime analogy, is clearly a big part of this.

The revival of inflation has been heralded many times since Paul Volker waged war on it in the early 1980s. We suspect these worries are premature, however, one of the legacies of the crisis may prove to be a long-anticipated shift from the disinflationary regime of the last 40 years. That is a topic for another time, for now our focus remains on the safe negotiation of this crisis.

By James Beck, Head of Investments

Posted on 17 April 2020

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.