It was the worst of times, it was the best of times

James Beck, Partner and Portfolio Manager

Rather than a tale of two cities, for investors 2020 has very much been a tale of two quarters.

With barely a moment to draw breath following the swiftest 30% fall in market history, which reached its trough on the 23rd March, major indices began a stimulus-fuelled ascent out of the abyss. Significantly, this recovery began before suspicions of the economic damage caused by governments’ response to the public health crisis could find any basis in fact. The first real economic shockwave hit on the 26th March, after the market recovery had begun, with the US announcing a weekly increase in unemployment of 3.28 million.

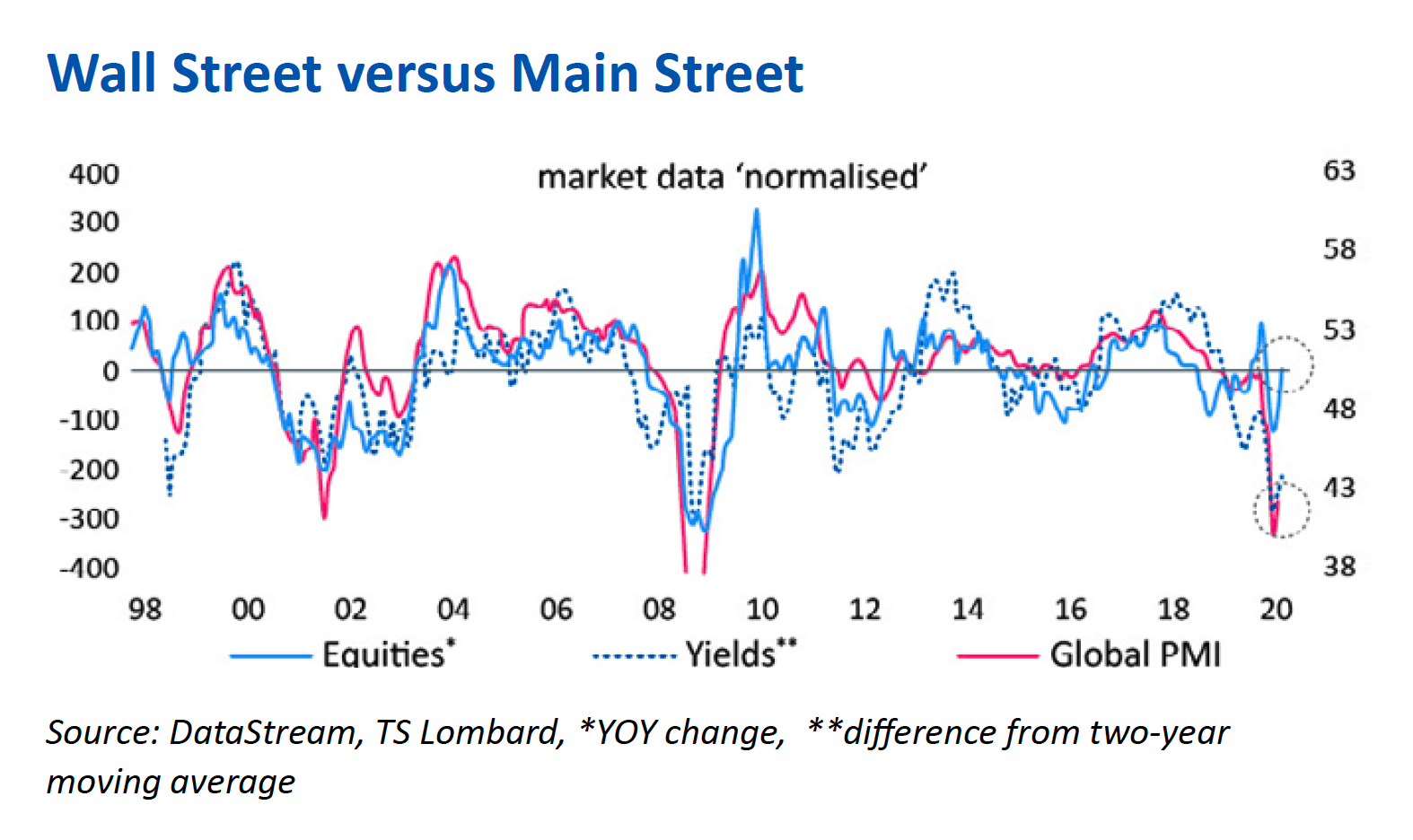

That Wall Street looked through the unfolding reality on Main Street to the potential implications of the monetary and fiscal support provided is important in our understanding and thinking around the present market environment and that still to come.

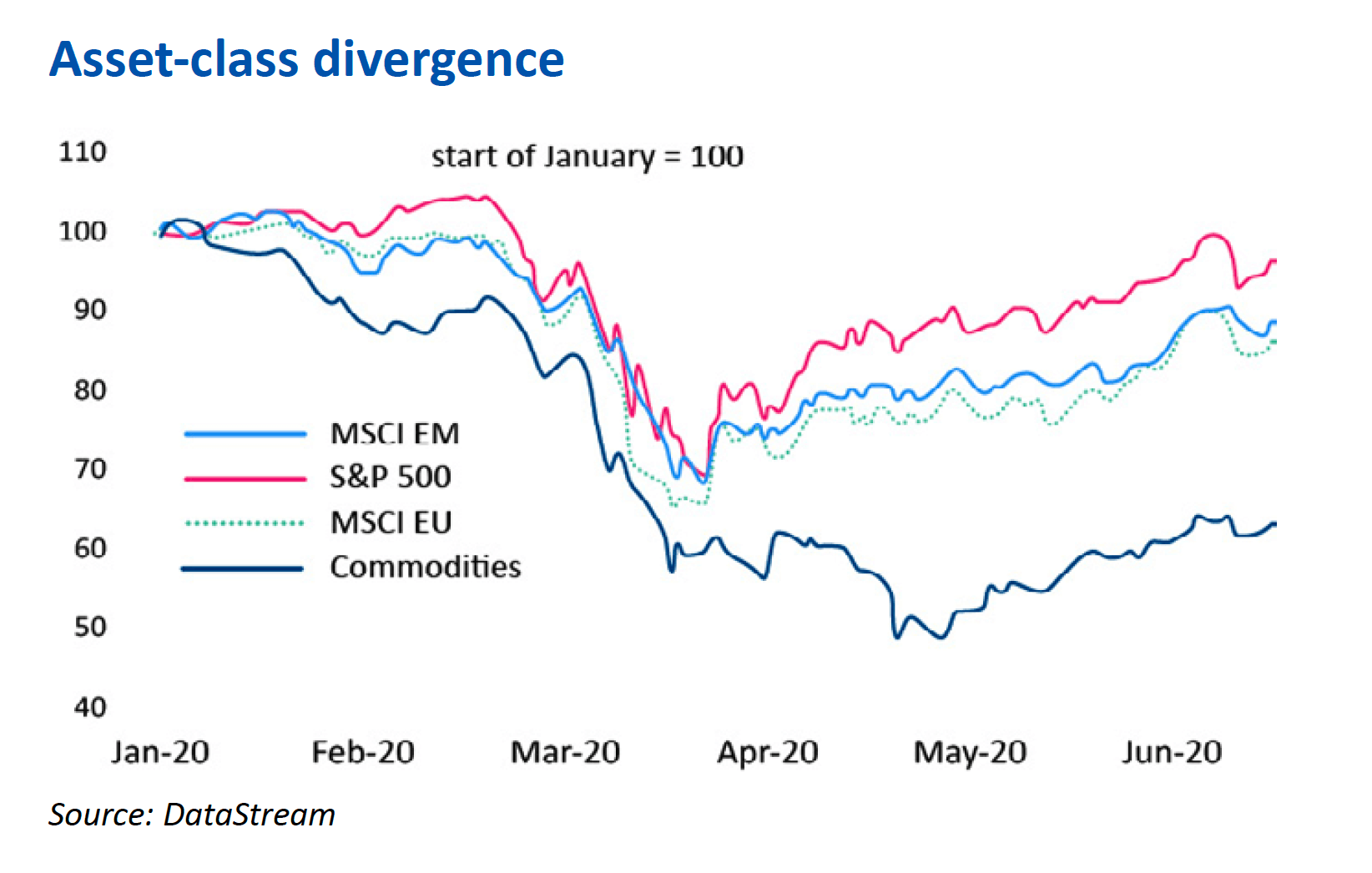

The tide of global stimulus lifted all ships through the second quarter, with every asset class posting positive returns. Global equities returned 19% in local currency terms, both investment grade and the riskier high-yield bond indices rose by over 10%, while gold returned 13% to post its seventh consecutive quarter of positive performance. Oil prices finished the quarter an astonishing 80% higher than in early April – although, in a reminder of the importance of avoiding severe drawdowns, the Brent Crude Oil prices remain down 38% for the year to date.

Within equities, the US market led the way. The S&P 500 rose 20%, its biggest quarterly gain since 1998 when the Federal Reserve again directed a rescue in the aftermath of the Russian debt crisis and subsequent collapse of Long-Term Capital Management. The US benefited not only from the most dynamic and material recovery package but also from a market dominated by more of the companies seemingly best placed to profit from, rather than simply survive, the global pandemic. The likes of Amazon, Netflix, Zoom and Microsoft all contributed to a 31% return from the technology-weighted Nasdaq. The index touched a new record high in the quarter and is now up 13% this year.

Equity markets in other regions also bounced strongly, with the FTSE All Share +10%, Europe exc. UK +16%, Japan +12% and Asia exc. Japan +16%.

Standing on the shoulders of giants

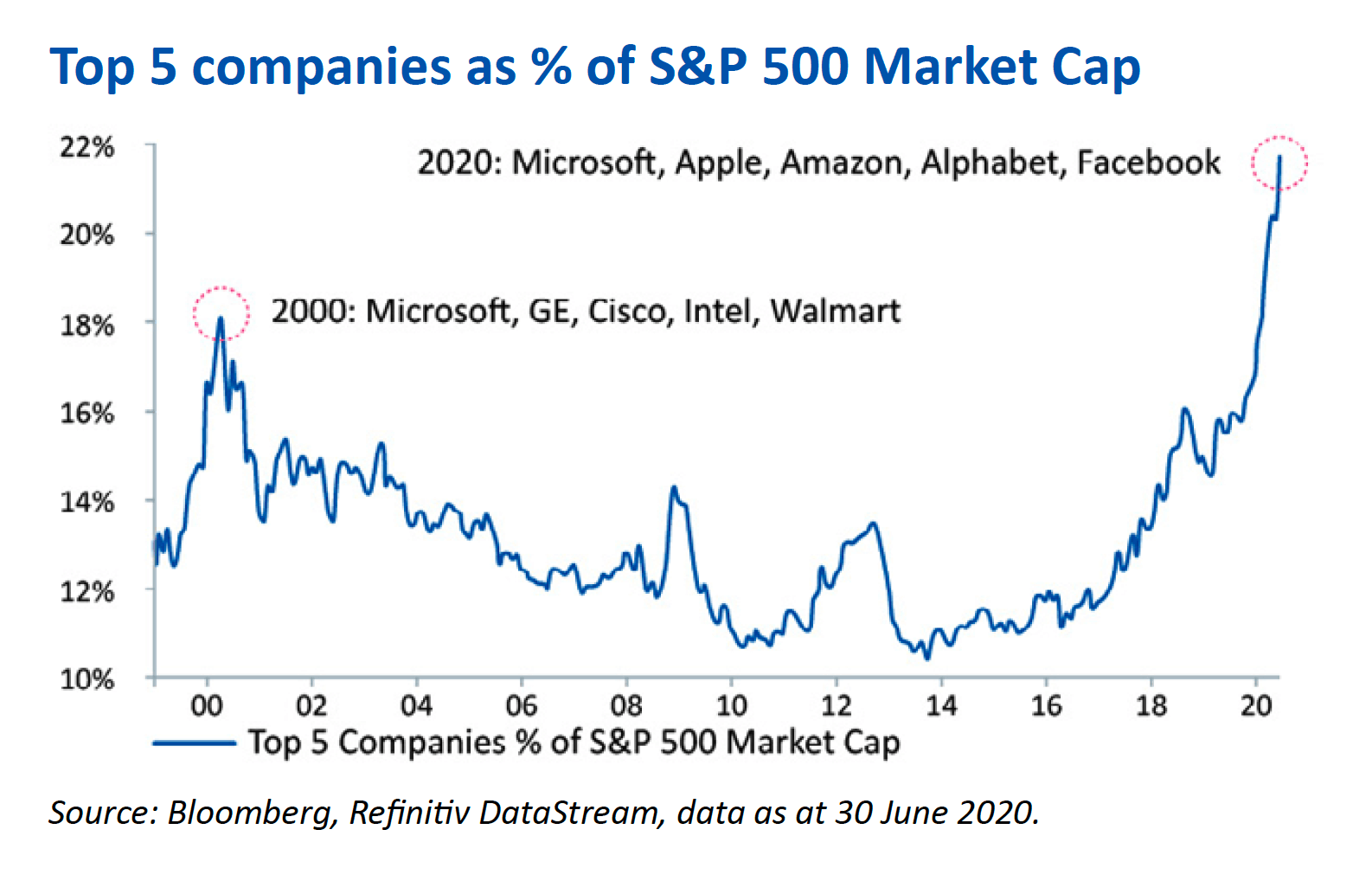

That the US has led the way is of little surprise given the composition of its market. It is home to the five technology giants of Apple, Microsoft, Amazon, Google and Facebook, which combined now represent over 20% of the S&P 500.

It can be tempting to draw lazy comparisons with the tech bubble in 2000, but these are profitable businesses with robust balance sheets that remain the core enablers of the ongoing transition to a digital economy – a trend that has only been accelerated by this year’s events. Unlike past episodes of high market concentration, the group’s weighting is very much in line with the proportion of cashflow generated. If there are building excesses, we feel it is probably amongst the next tier of more speculative growth companies, such as Tesla, Zoom, Peloton and co, where valuations are becoming increasingly stretched from underlying fundamentals.

As this dominance continues to grow, the most immediate challenge is likely to prove regulation. With Germany and France having moved a step closer to a centralised European fiscal policy through their proposed EU Recovery Fund, the technology giants represent an enticing source of funding at an EU level. Across the Atlantic Joe Biden has built a notable lead in the presidential polls, and, given their more enthusiastic approach to anti-trust legislation, a clean sweep for the Democrats in November might portend a less benign 2021 for this new ‘Famous Five’.

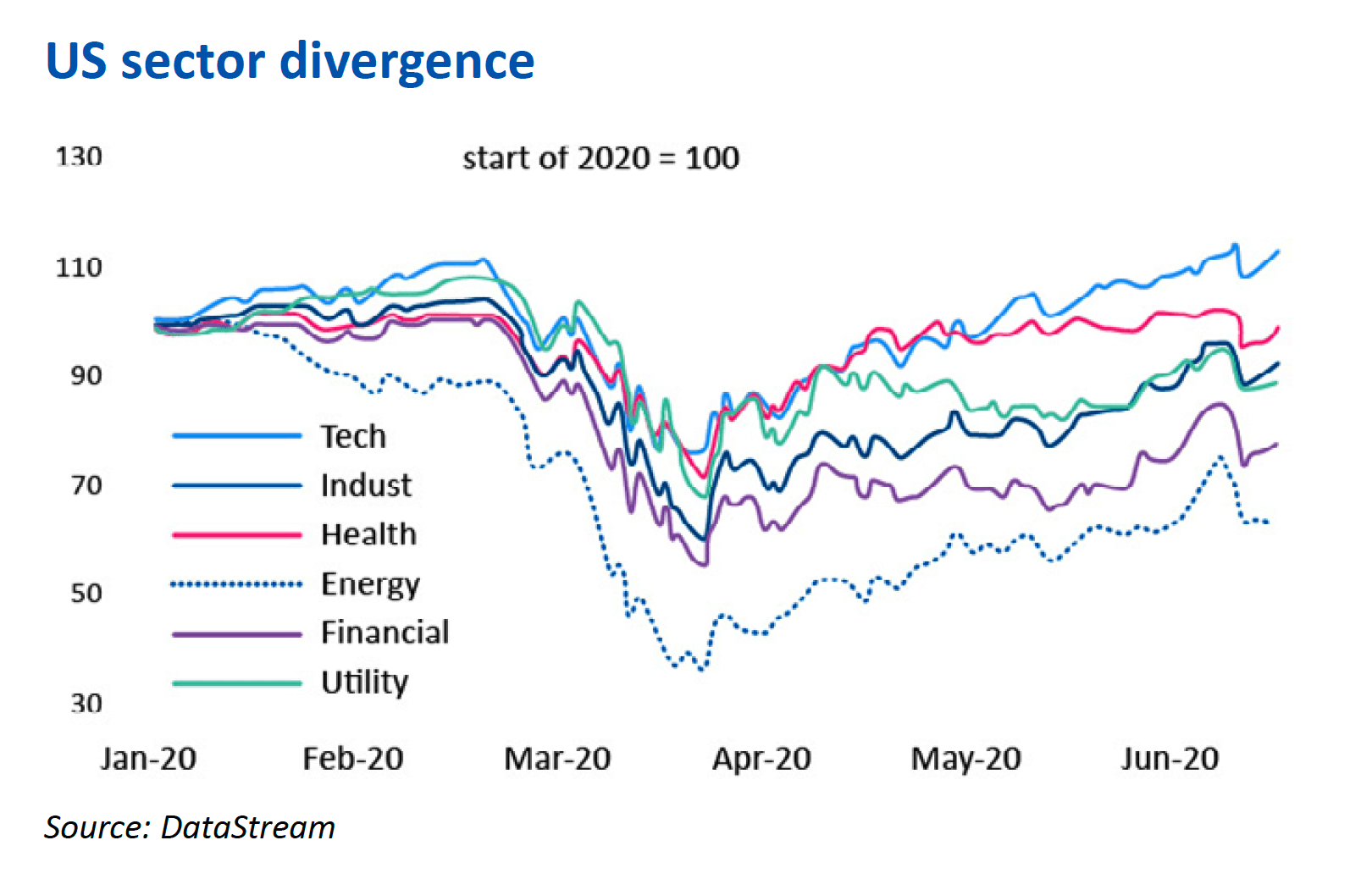

While the headline resilience of markets this year has surprised most investors, the recovery has not been all-encompassing. Technology and healthcare have performed well and are in positive territory this year, whilst many more cyclical or interest-rate-sensitive sectors such as financials, energy and real estate remain substantially below their recent peaks. Despite questions over the perceived disconnect between Main Street and Wall Street, the relative returns from sectors seem very much more rational.

Closer to home, the UK continues to be a notable laggard amongst developed markets. Whilst the S&P has recovered much of its poise, the FTSE All Share remains down 17.5% for the year. This is partially due to the composition of the UK indices, with their heavy weighting to oil, mining, banks and traditional retail and almost complete lack of digital champions that are proving the winners during the crisis.

But there are other factors at play. UK investors’ fixation with income has caused many companies to compromise on capital allocation over the decade since the financial crisis, with management teams overlooking the reinvestment needed to support future growth in order to protect high yields and payout ratios in the shorter term. This year has exposed the fragility of this policy, prompting a savage cut to dividends by many leading UK companies. The continuing uncertainty around Brexit has also not helped to attract international investors; with only six months left until the end of the transition period, it will require diplomacy of Herculean proportions for Michel Barnier and David Frost to agree a deal. The strains are evident in sterling, which, following a brief Boris bloom in the afterglow of the general election, has resumed its descent, falling by 6.5% this year against the US dollar and euro.

This points to why we typically consider industry sectors over geography and focus on the individual merits of companies. Given we can invest in businesses with operations that transcend borders and where the value of their earnings can be comparable to the GDP of a small nation, classifying companies along geographical lines seems an artificial construct. A decision to invest in AstraZeneca should be considered against the relative merits of Pfizer, Novartis or Merck rather than those of Tesco, Barclays or Shell.

Our exposure to companies quoted in the UK is near the lowest point in our history. This is not so much a reflection on Great Britain – we have exposure to fantastic companies such as Experian, Rentokil Initial and London Stock Exchange – but rather a consequence of our ability to cast our net wider to invest in the best businesses globally wherever they happen to be quoted.

Central Banks to the rescue (again and again and…)

“We’re not even thinking about thinking about raising rates.” – Jerome Powell, chairman of the Federal Reserve, June 2020

This statement accompanied a release from the US Federal Reserve in which it stated that US interest rates would likely remain near zero until the end of 2022. That is in two and a half years’ time!

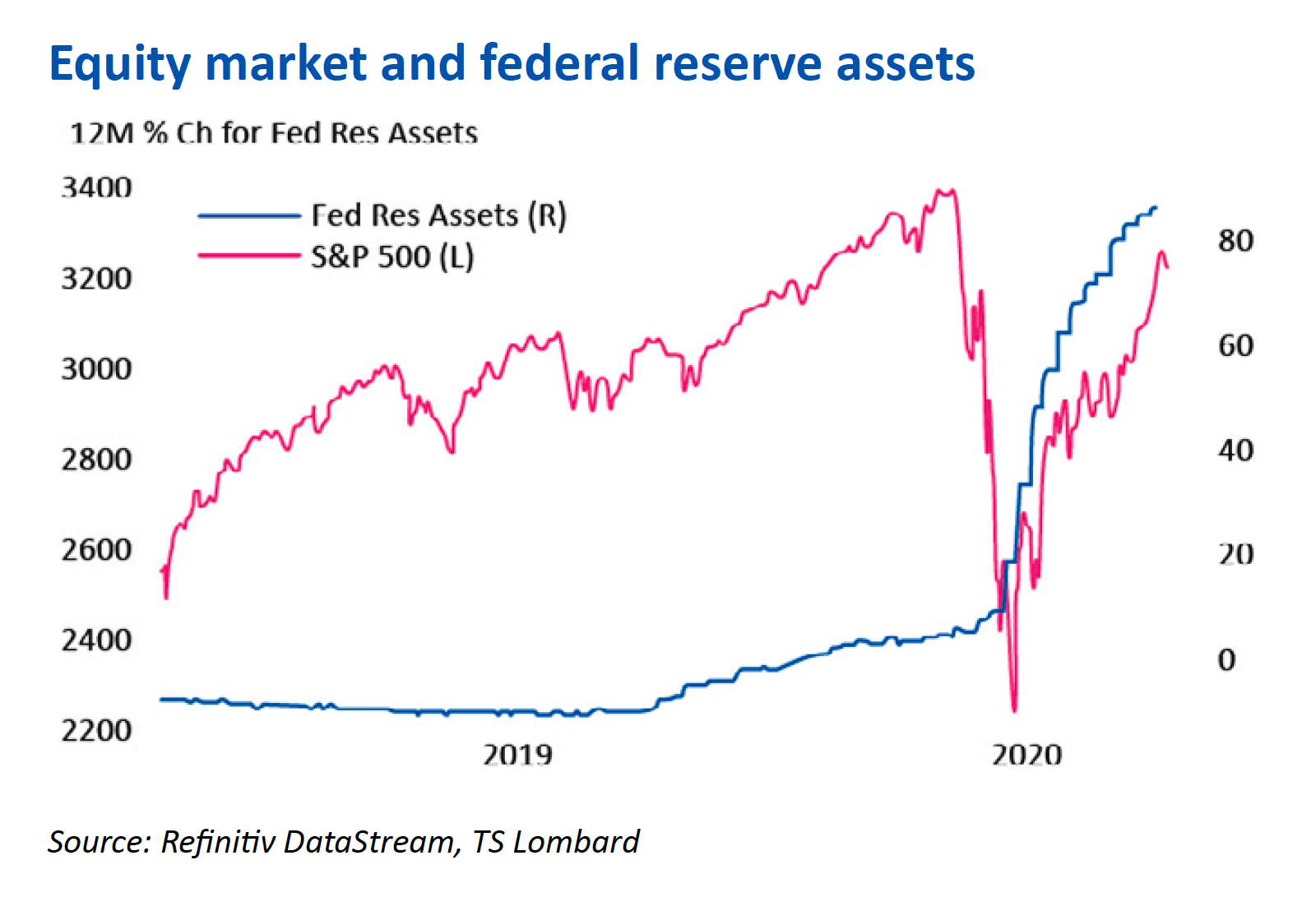

It is hard to overstate the importance of central banks, principally the US Federal Reserve (the Fed), in underpinning the economy and investment markets. Their swift and decisive actions during the most acute phase of the crisis were vital in ensuring that the pandemic did not cause more widespread destruction.

Not only did the Fed cut rates aggressively from 1.75% to 0.25%, having more scope to do so than the Bank of England or the European Central Bank, but it also proved far more radical in providing additional measures to support financial stability. It is not an exaggeration to say that the Fed effectively averted a credit crunch and financial crisis through the extension of liquidity to corporate bond markets through the purchase of both investment grade and high-yield debt.

This has led to an explosion in corporate debt issuance and refinancing in the second quarter, allowing companies to shore up balance sheets, often at rates below even those of only six months ago. Boeing alone has $30 billion of new bonds since March, despite the obvious turmoil facing its commercial aerospace operations. Crucially, the ability of companies to raise capital allowed fears over a solvency crisis to fade, and as confidence returned debt raises have given way to equity issues both for balance sheet repair and opportunistically to fund growth. Investors have been receptive, capital forthcoming and investment bankers extremely busy; it will be hard for the big US investment banks to play down the success of their capital markets divisions in the coming quarterly reporting season.

Central bank balance sheets are set to continue to grow in the second half of the year, and their purchases have moved beyond government bonds to include the purchase of high-quality corporate bonds (in both the EU and US), high-yield debt and even direct lending to small businesses in the US via the banks. Here the Fed is stepping beyond the realms of monetary policy and beginning to blur the lines between monetary and fiscal behaviour. This might prove another nail in the coffin of central bank independence.

The economics of reopening

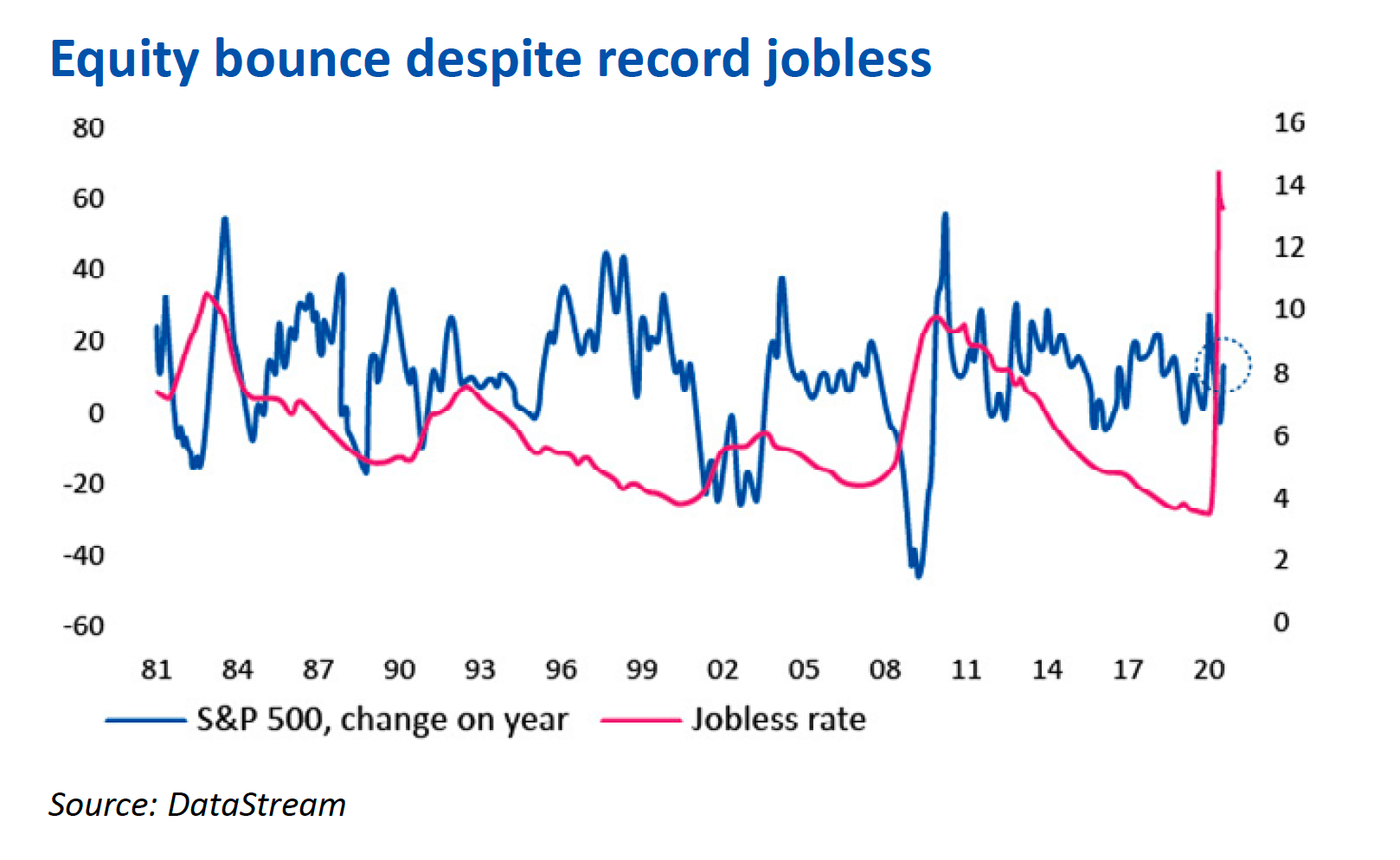

The recent economic data has been breathtakingly bad and reminiscent of numbers more commonly seen during times of conflict. The UK economy contracted by 20% in April, the largest monthly fall on record, whilst in the same month the US reported an additional 20.5 million job losses, taking the unemployed rate from 3.1% in March to nearly 15% little more than a month later. Even during the 2008 global financial crisis unemployment failed to rise above a peak of 10%.

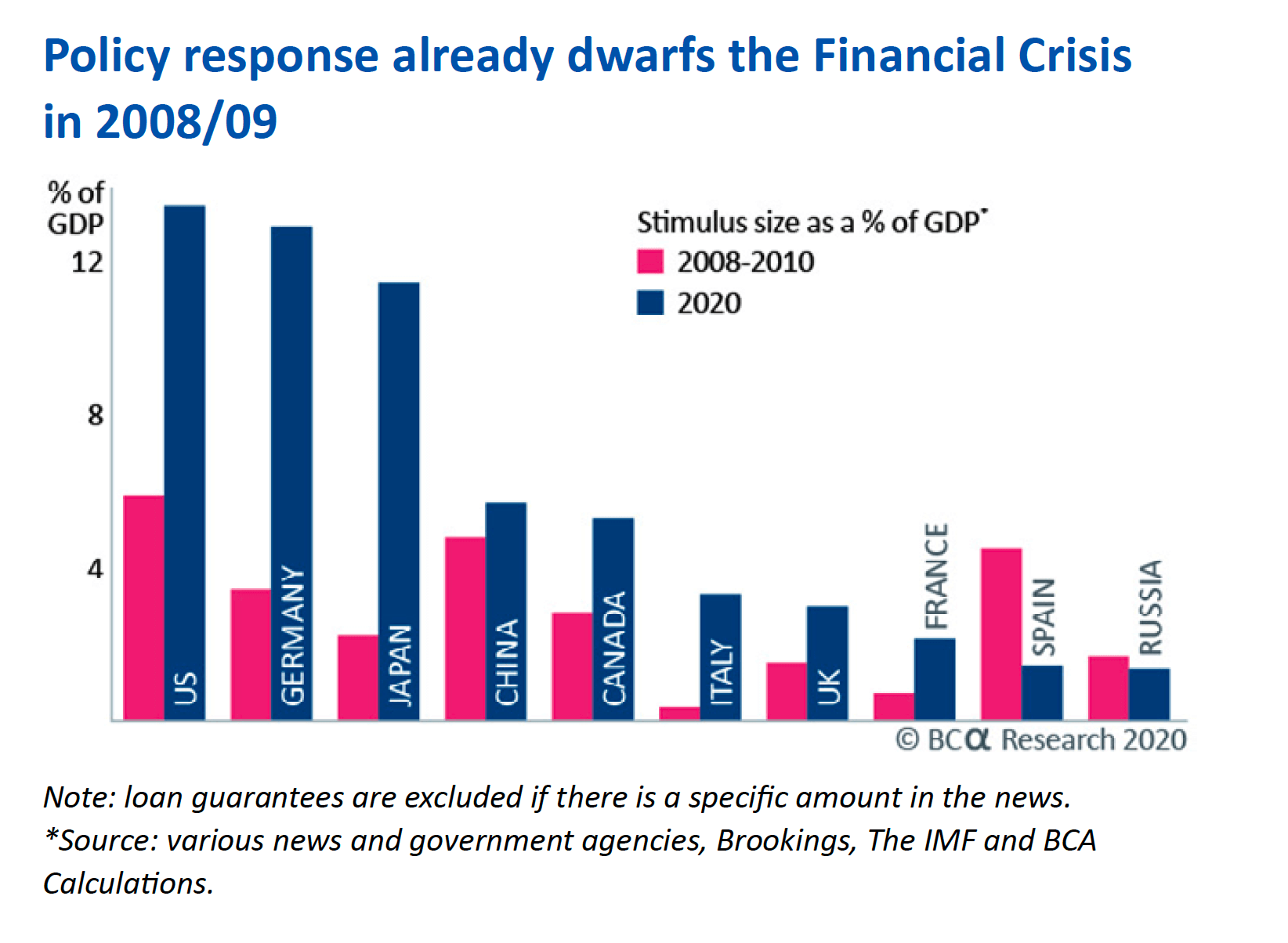

However, as we now know, April proved to be the nadir for economic data in the UK, the US and Continental Europe. With the spread of Covid-19 slowing, governments started easing restrictions and began the gradual process of normalising economic activity. Supported by fiscal stimulus that dwarfs that seen in the last recession, policymakers appear to have been effective in stopping both activity and sentiment from suffering irreparable damage.

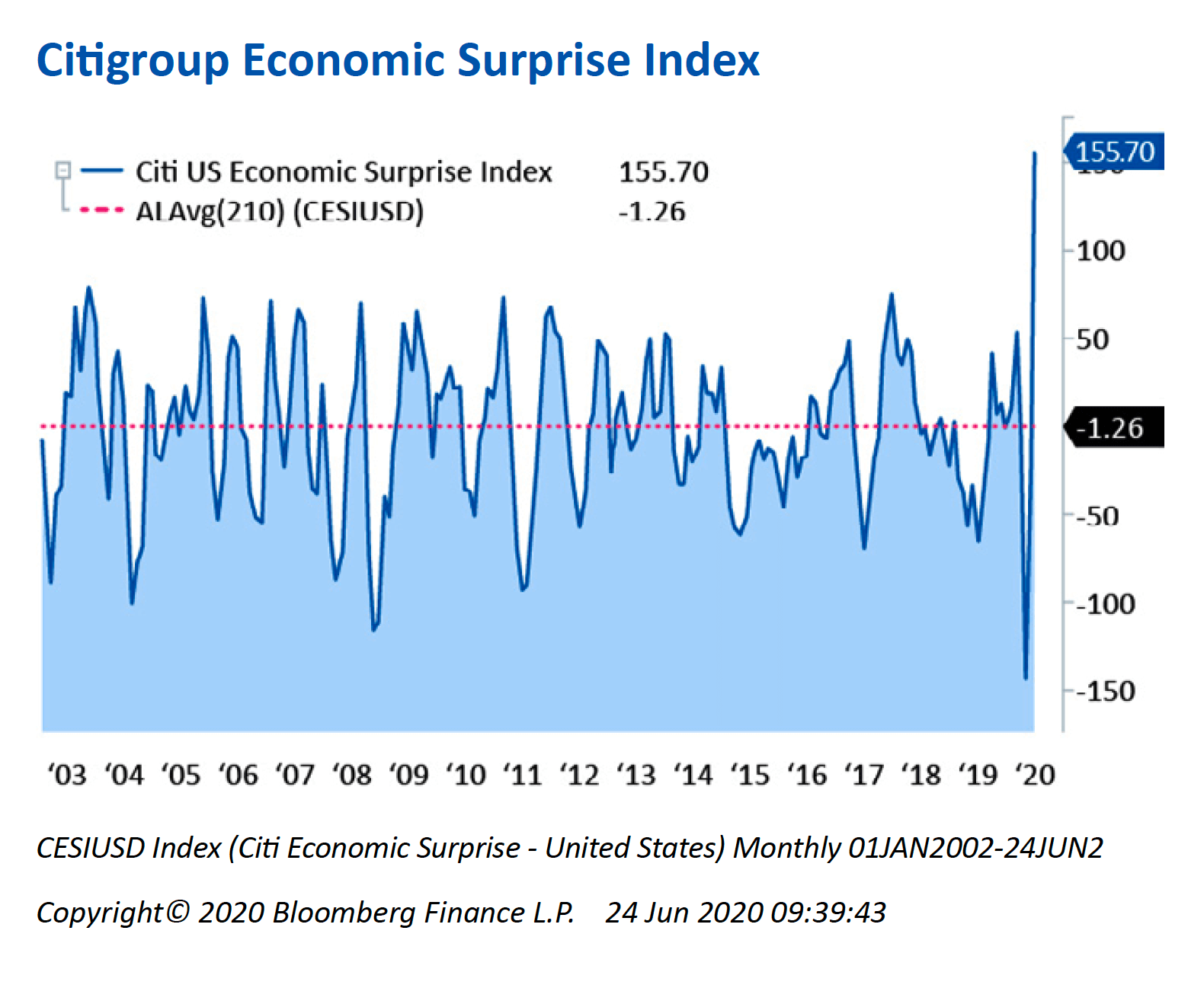

As economies have reopened, the data has snapped back. Rapid recoveries in activity and spending have confounded many economists. It seems likely that the shocking collapses in data will be followed by a correspondingly remarkable recovery. We often note that financial markets move sharply when extreme investor sentiment meets changing expectations. The record positive levels hit by the Citigroup Economic Surprise Index suggest that forecasters have been overly pessimistic on the real economy impact to an unparalleled degree.

While the picture has certainly brightened, given the scale of the lockdowns, the impact of second waves on consumer behaviour and the wave of redundancy announcements coming from the likes of Airbus, BP and SSP, it seems unlikely that economies can quickly reassume the levels of January, as some are predicting. The challenges of successfully reopening economies is highlighted by the news that US sunbelt states, including Florida, Texas and California, are experiencing a resurgence in new cases, with daily infection rates currently ahead of those experienced in March. How legislators and consumers react remains to be seen, but in an election year there will be a political desire to keep the economy open; the Swedish model is gaining traction almost by default.

More support will be needed to keep economies moving once the generous government furlough and unemployment grants are removed. There will undoubtedly be further policy to fill the gap, and others may follow Germany’s attempt to foster spending with the state giving families €300 to spend per child as an immediate impulse alongside longer-term infrastructure projects. Further incentives and investment are certain, but estimating what the new normal will look like is currently an exercise in luck rather than judgment.

“Economists are often asked to predict what the economy is going to do. But economic predictions require predicting what politicians are going to do – and nothing is more unpredictable.” – Thomas Sowell, Hoover Institute

Forecasting is always mired in uncertainty, but the range of potential outcomes today seems wider than ever.

- Will there be a second wave?

- How bad will the second wave be?

- Will governments lock down the economy again?

- Will a vaccine be discovered?

- What will the structural damage to the economy be?

- Will there be further government stimulus?

- Who will win the presidential election?

- What will be the outcome of Brexit?

Even if we knew exactly what was going to happen, there is no guarantee that the markets would react in the way that we would expect in the short term.

Analysts, too, are groping in the dark, starved of the usual guidance given by company management, with only 48 companies in the S&P 500 attempting to provide guidance for the second quarter and nearly 200 having thrown in the towel for the entire year. Forecasts for this year and probably next will vary widely and be subject to such regular revision as to be practically useless.

Rather than spend our time in the alphabet soup of potential shapes of any economic recovery or try to assess the relative merits and efficacies of potential vaccines, we have been focusing on business models and trends that will endure beyond the current public health and economic malaise. In a world of low growth and zero rates, companies capable of delivering sustainable growth will remain in demand and should continue to command a premium.

Valuation, inflation and is it different this time?

The seeming disconnects between market levels and the news headlines have prompted some commentators to question the stability of the recovery, pointing out that current valuation levels look high compared with history. We do not disagree, but valuations are not as unjustified as some would suggest. With interest rates having been dramatically cut and seemingly anchored at low levels, the discount rates used to value equities alone mathematically justify a higher rating, whilst the relative attractions of reliable cashflow from good companies have also increased in a world of zero (and potentially negative) returns on cash.

However, if stocks have simply rerated to reflect the trend decline in interest rates, this is a move that is unlikely to keep going – and so we will need fundamental growth in earnings and cashflow to pick up the baton. Looking at the aggregate valuation of the FTSE and S&P is always an easy shorthand, but this number obscures the underlying mosaic of sector and individual company data that is far more varied, with areas that are clearly expensive and those that look cheap. We need to be aware of the headline valuation, as it can be an indicator of short-term turbulence, but we remain more focused on the price we pay for individual securities and whether that is fair given the expected returns over the next five years.

Whilst valuations are high, so is the risk premium demanded by investors to hold equities over bonds. This seems fair, given the state of the world. The despair of March and April has given way to hope; we now await evidence of the reality. The coming quarterly earnings season is unlikely to provide definitive answers, given the speed with which events are unfolding and the overarching cloud of uncertainty. We are comfortable holding those securities we have thoroughly researched and believe we understand but do not see a compelling case to add further.

With the monetary bazooka firing again and government deficits exploding, concerns are again building that this may precipitate a resurgence in inflation not seen since the days when Paul Volcker chaired the Federal Reserve 40 years ago.

Even before the crisis struck, the US had experienced a decade of negative short-term real interest rates for only the second time in nearly 200 years and had run a large fiscal deficit in a period of near full employment. Every economic textbook written would tell you that those are the ideal conditions for inflation. That it did not appear has been credited to a veritable cornucopia of deflationary forces – demographics, technology, globalisation. Whatever the reason, its absence has allowed central banks to keep policy loose, an important support to asset prices.

However, in contrast to the recent past, it is clear that austerity will not be part of the recovery. The crisis has hastened an end to the mantra of fiscal conservatism that accompanied the post-financial-crisis world in the UK and parts of the EU. The future appears likely to be one of increasing fiscal largesse beyond the economic triage seen to date.

Rising deficits financed by central banks are too tempting a means for administrations to address the challenges posed by creaking infrastructure, climate change, societal inequality and the unrest caused by rising political polarisation. Against this backdrop, some inflation would be welcome to help erode the real value of the debt on government balance sheets. Add in growing tensions between China and the US potentially causing a reversal in globalisation and there are strong forces at work that could prompt a transition in the inflationary regime.

These future challenges are ones that we think about regularly and are building into our long-term planning. Today, though, our focus remains on continuing to manage the risks, challenges and opportunities presented by this extraordinary period and ensuring portfolios are resilient should the pandemic lead to a resurgence in restrictions.

By James Beck, Head of Investments

Posted on 22 July 2020

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.