Thomas Allsup, Portfolio Manager

Whilst the summer lasted, a recovery seemed here to stay. As governments shifted from propping up economies to lifting restrictions, the optimism that Coronavirus would prove short-lived gained momentum as consumer and business confidence was helped by hopes for a vaccine by Christmas. Global equities captured the mood, reaching fresh all-time highs by early September, some 50% above their 23rd March lows.

However, as the days shortened the optimism of the summer gave way to a ‘back to school’ feeling as rising case numbers prompted wider concerns that the disease might be here to stay, unresolved by intermittent quarantines and eat-out vouchers. As belief in the pandemic progress waned, markets wavered drawing inspiration from the varied response of the political classes.

For those capable of avoiding the relentless hyperbole of the news cycle, it might appear a lot of fuss about nothing. Overall, global equities rose by 7% in local currency terms, or 3% in sterling. Investment grade bonds finished 1% higher, somewhat behind the 5% return from riskier high-yield bonds. Gold had a busy three months amidst shifting sentiment and comments from the US Federal Reserve, reaching a record high of $2,064 before rolling over to finally close up 6% – its eighth consecutive quarter of positive returns. By comparison oil prices languished over the quarter and Crude Oil remains down 38% this year.

The recovery continued to be led by the US equity market (+9%) but, buoyed by hopes of a more sustainable global reflation, returns broadened as the Far East and Emerging Markets rose between 8 – 9% in local currency terms. Once again bringing up the rear amongst developed markets was the United Kingdom. The FTSE All Share fell a further 3% and still sits 20% lower than at the start of the year.

With COVID cases rising and restrictions returning, it is tempting to ascribe the UK’s underperformance to its Coronavirus approach. Equally, it can be comforting to blame David Frost and his team negotiating with an increasingly irascible European Union.

However, in truth the UK has become a strange, fossilised market. With its near 40% exposure to financials and oil and gas markets, the FTSE lacks the technology-focused businesses that have thrived elsewhere. Rather than reinvest in new opportunities, many company management teams have paid out their hard-earned cash to dividend-demanding shareholders for too long and left themselves with little room to manoeuvre. This year over half of UK companies have cut or cancelled their dividends, with many using Coronavirus as a cover rather than a cause.

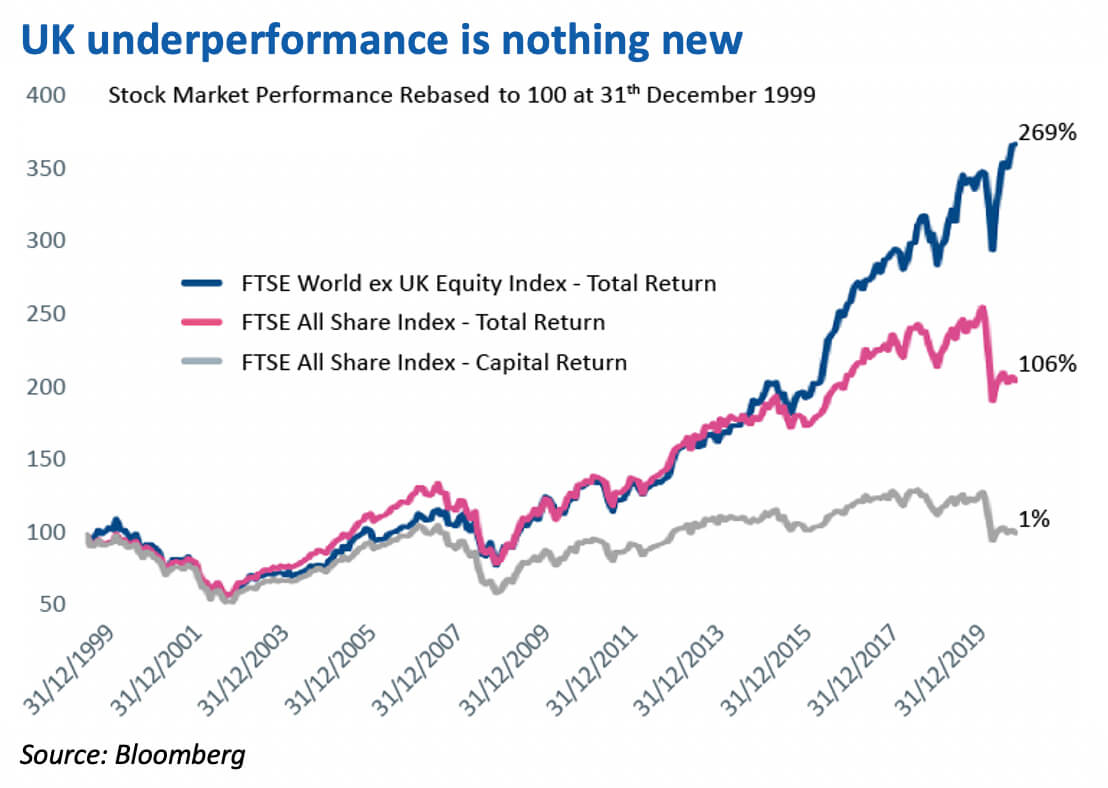

This matters because, since the turn of the millennium, the FTSE All Share has risen by 106% in total return terms. But stripping out the dividends leaves a paltry 1% capital gain. Without its 4%+ annual income yield, the UK market is increasingly uninviting – a fact not lost on international investors who have shunned the UK. The latest Bank of America Merrill Lynch survey of global fund managers shows UK exposure near historic lows.

While the UK is home to some wonderful global businesses – we own a good handful – our attentions have long been focused overseas, reflecting the greater potential of finding opportunities abroad given the UK represents only 4% of global stock markets. This has been a rewarding strategy. Even including dividends, the UK stock market has underperformed the rest of the world by 133% over the last twenty years.

Assessing the economic recovery

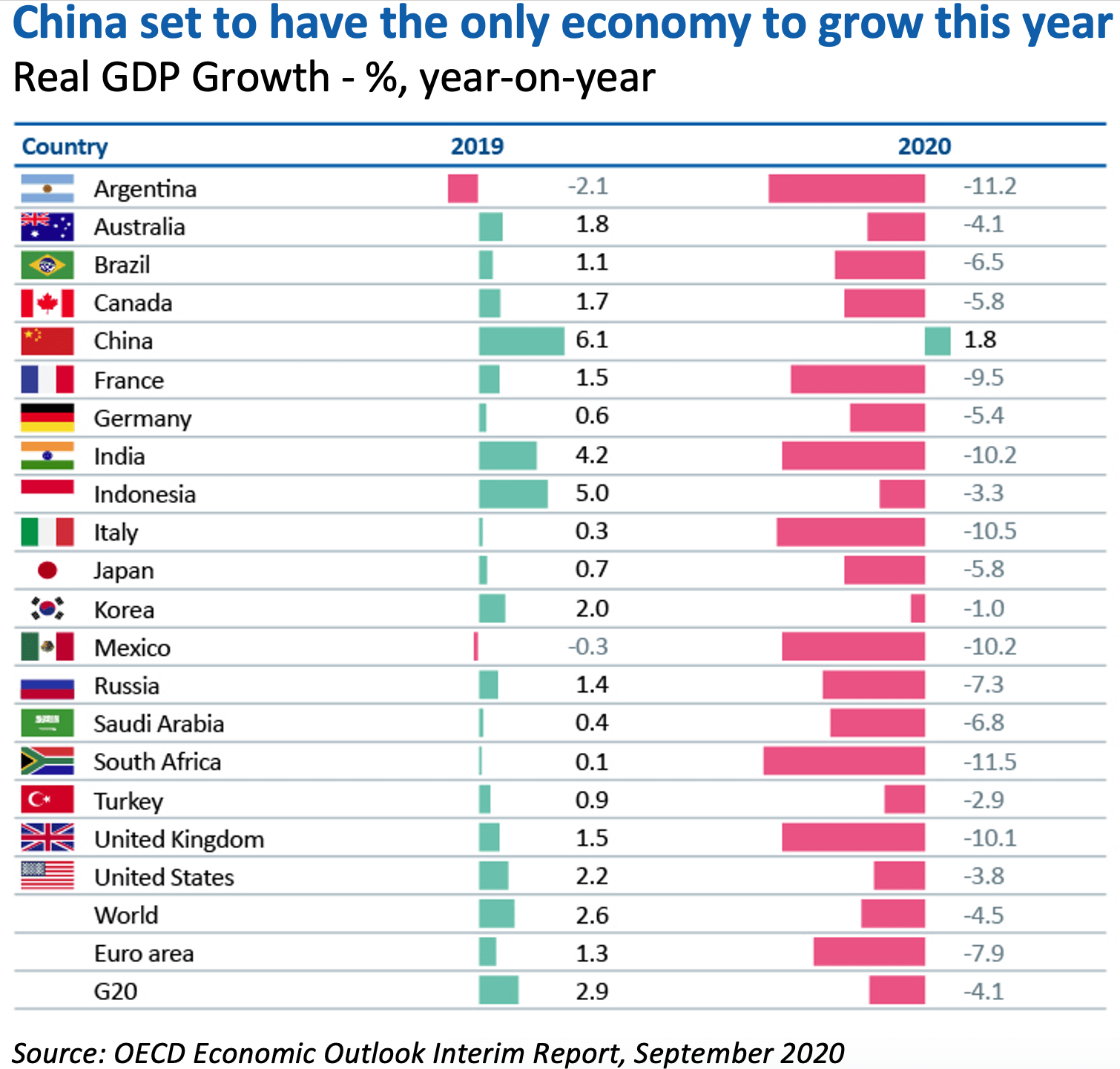

Three months on and the picture of economic progress is chequered. China has shown what can be achieved, as its ‘first-in, first-out’ position has combined with a seemingly iron grip on confining the pandemic. While such tight control is hard to replicate in Western societies, it has helped China forge the way and its economy is likely to be the only major one to grow this year.

At the other end of the spectrum, Europe highlights how difficult it is to see a widespread and sustained recovery without a durable solution to the disease. After reasonable early signs, services growth has started to slip backwards as the second wave of Coronavirus cases has built, taking the pace of employment improvements with it. European manufacturing has so far proved more resilient, but developments are concerning especially as the UK seems to be following the path of Spain and France with a short lag.

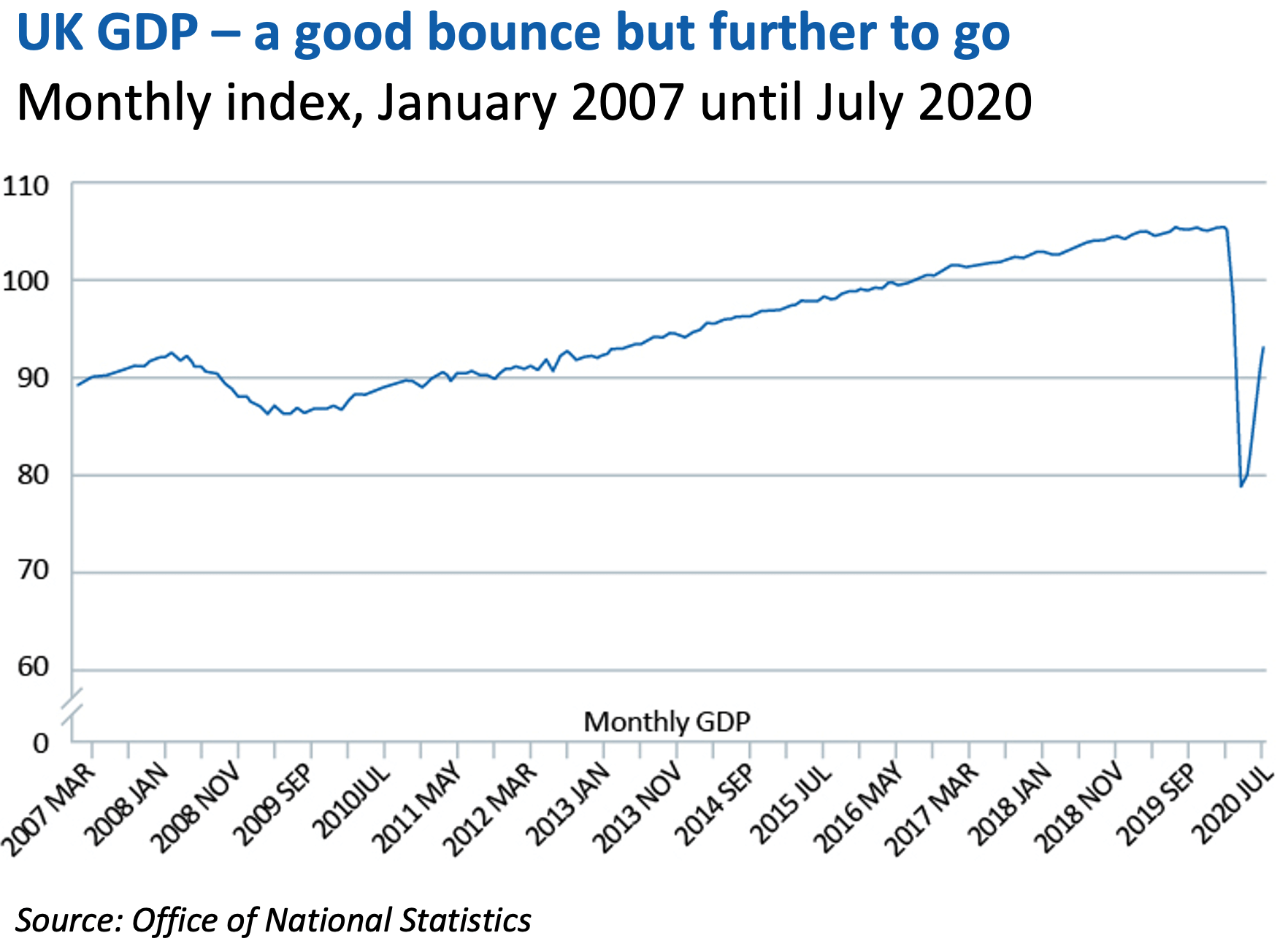

So far, the UK has made some advances. The latest Gross Domestic Product (GDP) figures contained an encouraging third consecutive month of growth. However, the challenge remains to make back lost ground. All gamblers know that if you lose 33% of your money, you need to make 50% to return to square one. To date, the UK economy has only regained half of the output lost due to Coronavirus.

The great unknown is the United States. Initial gains in the labour market suggested a faster recovery than expected. After the loss of over 22m jobs in three months, the US economy had added back over half of these by September, reducing the unemployment rate to c.8%. This was encouraging given the US was wrestling with rising Coronavirus cases throughout the summer as it struggled without a cohesive response to the pandemic. Similarly, the US housing market remained buoyant, helped by thirty-year mortgages rates hitting record lows below 3%.

Jobs and housing sit at the heart of the health of the US consumer whose spending makes up broadly two-thirds of US GDP. That the US consumer remained confident and willing to spend has been a bright spot, helping retail sales achieve a V-shaped recovery to pre-COVID levels. Similarly, animal spirits have returned in the corporate world in the form of mergers, acquisitions and public listings. Indeed, the last three months were the busiest third quarter on record for global deal-making with over $456bn of large transactions alone.

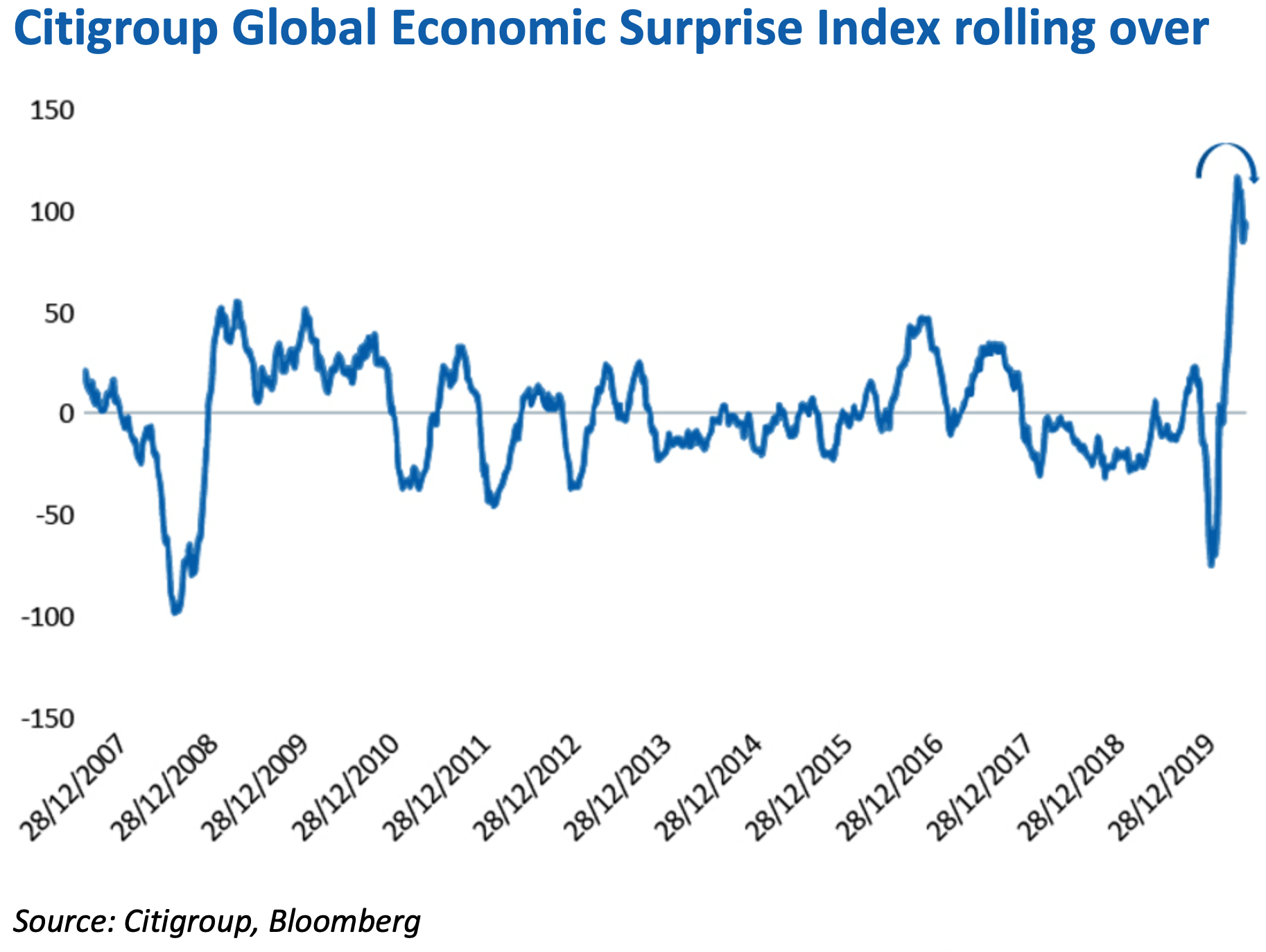

The million-dollar question is whether the gains will prove a firm foundation or slip away with the swallows as winter arrives and virus cases return. It is notable that the Citigroup Economic Surprise Index has started to roll-over from record levels.

Please sir, can I have some more?

Recent weeks have suggested that more support will be required to keep economies moving forward. This will likely be the case even if a vaccine is unveiled before the end of the year, given the difficulty in ramping the safe production and distribution of any medical breakthrough. The testing experience does not augur well for a seamless roll out should a vaccine arrive.

Faced with an economic shock from the first Coronavirus outbreak of a scale and nature unlike anything in recent memory, governments proved willing to do whatever it took to try and protect jobs and businesses. The indications are that most policymakers stand ready with new measures to get us through the winter, although there is a building acceptance that the emergency support in its current form of furloughs and loans cannot continue indefinitely.

Unfortunately, the position is less straightforward in the United States where pre-election partisanship has made further fiscal stimulus difficult. This has been exacerbated by the vitriol surrounding the replacement of the iconic Ruth Bader Ginsburg on the Supreme Court.

Thankfully, until now Jerome Powell, Chair of the Federal Reserve and the world’s most important central banker, has stepped up where his elected counterparts have not. In August, he outlined a historic change in US monetary policy, announcing that higher inflation would be allowed in order to safeguard jobs and growth. To achieve this, it is expected that interest rates will remain welded to the floor for at least three years.

For those who understandably do not spend their time reading such Federal Reserve runes, this statement has some major implications.

Firstly, it suggests the Federal Reserve is happy to stand behind the US government as and when it decides to take more action. Don’t forget that governments, unlike ordinary mortals, cannot run out of money – they can always just print more. But money is a promise and reliant on the trust that governments can finance their debts. That trust, like a reputation for sobriety, takes years to build but only moments to lose. Low rates make the interest on any new debts close to zero and imply that any government ‘IOUs’ can be squirreled away without fear.

Secondly, the Fed’s move represents a subtle but significant shift away from fighting inflation towards promoting employment. Powell indicated that he was prepared to let the US economy ‘run hot’ (if it could be provoked into so doing) with the hope of sucking workers back into the economy, especially the lower-skilled, minorities and the young.

Indeed, it is a timely reminder of how unequally the pain of Coronavirus has been spread, affecting most those with the fewest skills and lowest pay across all categories. True, the impact could have been worse. In 1870, 46% of US jobs were in agriculture and 35% in manufacturing or crafts. Today, 40% of jobs are ‘managers, officials and professionals’ and 41% are in other services which are often able to ‘work-from-home’. Nonetheless, there seems to be a tacit acknowledgement that the Federal Reserve, like the US army, leaves no man or woman behind.

This evolving landscape of interest rates and inflation is why we have looked to complement our shareholdings in companies which can typically raise prices in times of rising costs with other inflation-protected holdings. While not cheap, index-linked government bonds provide insurance should inflation materialise higher than expected or uncertainty increase. Similarly, we have prioritised real assets such as infrastructure where revenues, for example from toll roads or bridges, increase with inflation. Finally, we hold gold, the attractiveness of which rises when the real yield on other assets falls. It also provides a last line of defence in a panic.

Ready, steady, vote

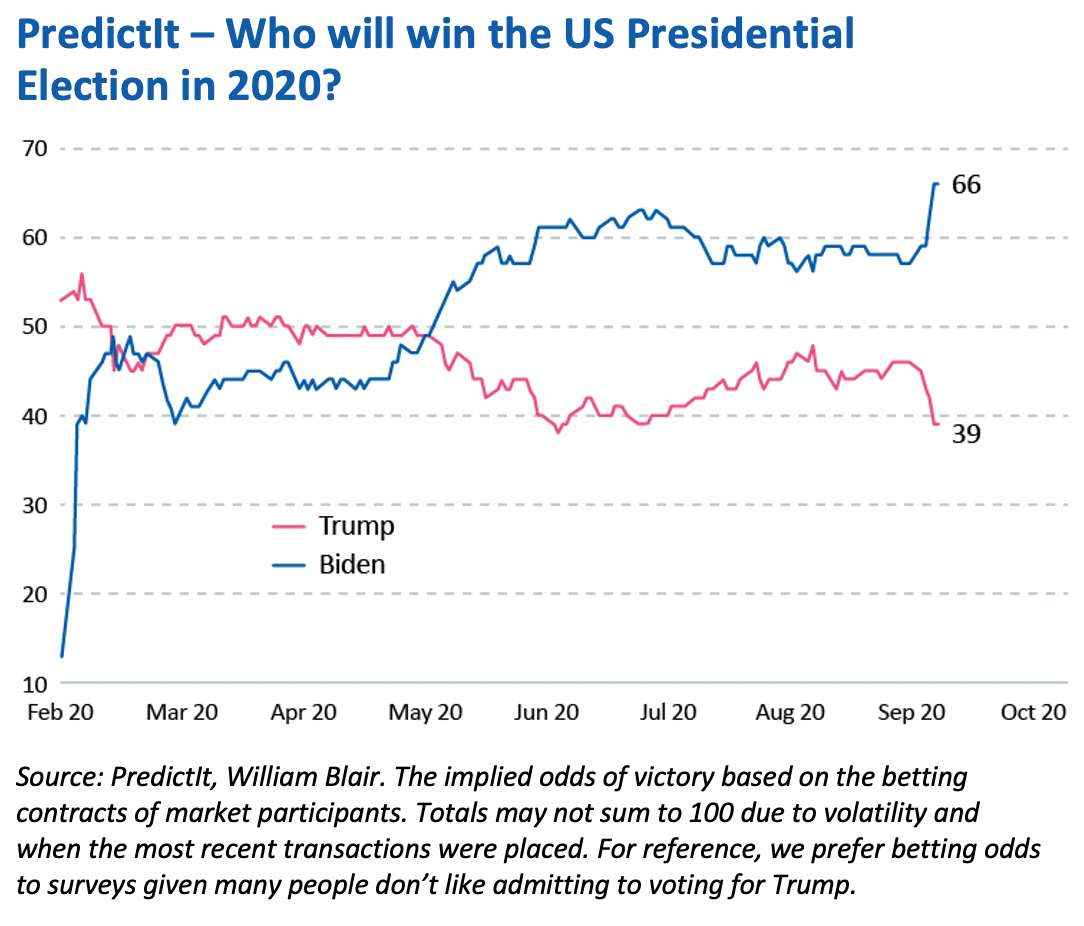

The Coronavirus context means the final sprint of the US election could not be coming at a more critical juncture, with the President’s recent infection adding another dynamic. History suggests that incumbent presidents have an advantage when fighting for re-election but this reduces if the economy is in recession. Accordingly, it is interesting that Trump’s approval ratings have started to rise again, since the election will be as much a weighing of his first four years in power as a comment on the future.

This year’s election is buffeted by particularly strong cross-winds. The Black Lives Matters protests and wider social unrest have highlighted the end of the age of deference to institutions and authority. And isolated by Coronavirus and divergent state policies, the role of social media in echoing back one’s own views feels more potent than ever. Throw in mail-in ballots in key swing states such as Michigan and we stand prepared to be surprised, not least given our experience of recent votes elsewhere.

Nonetheless, while the odds have narrowed, betting markets continue to favour Joe Biden. There also remains a possibility that the Senate might turn Blue too. This would increase the likelihood that the corporate tax cuts enacted by Trump would be reversed and that the far-left of the Democrat party would be empowered, with many commentators seeing this as having a potentially detrimental effect on the stock market, at least in the short-term. Conversely a Trump re-election would likely see a continuation of the current chaotic status quo.

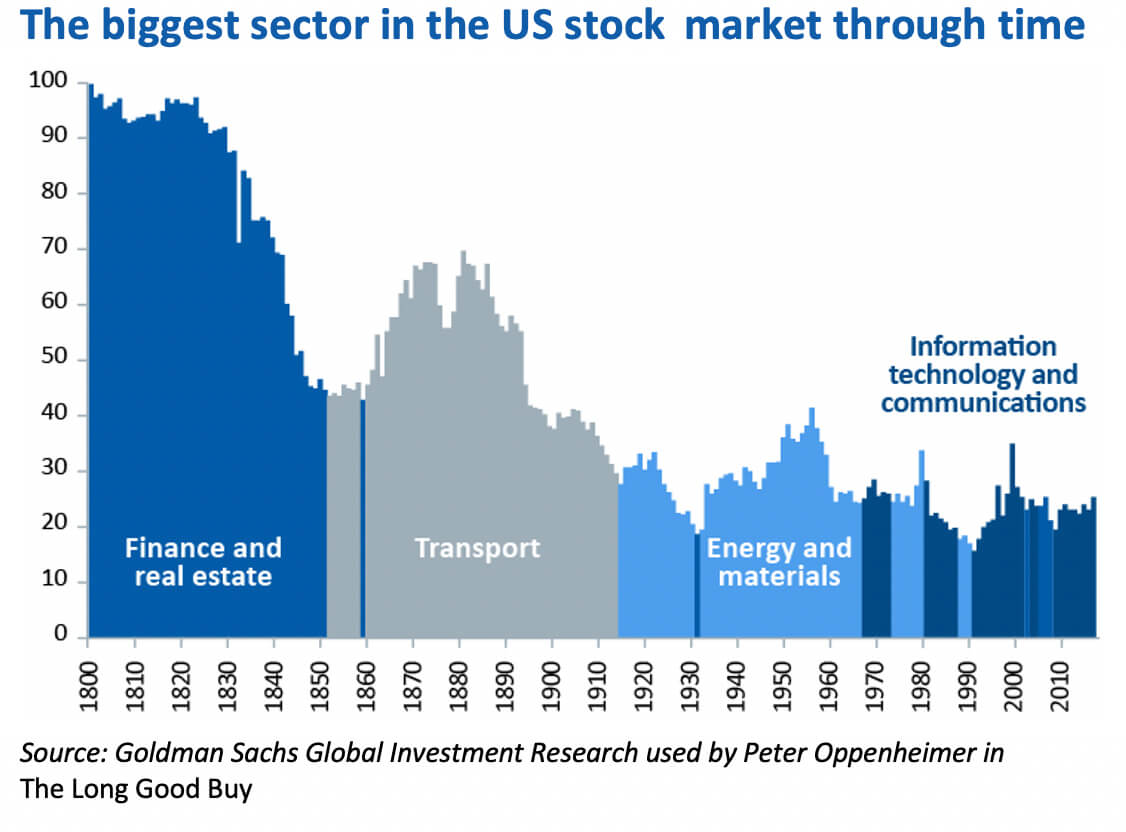

What do we do with tech?

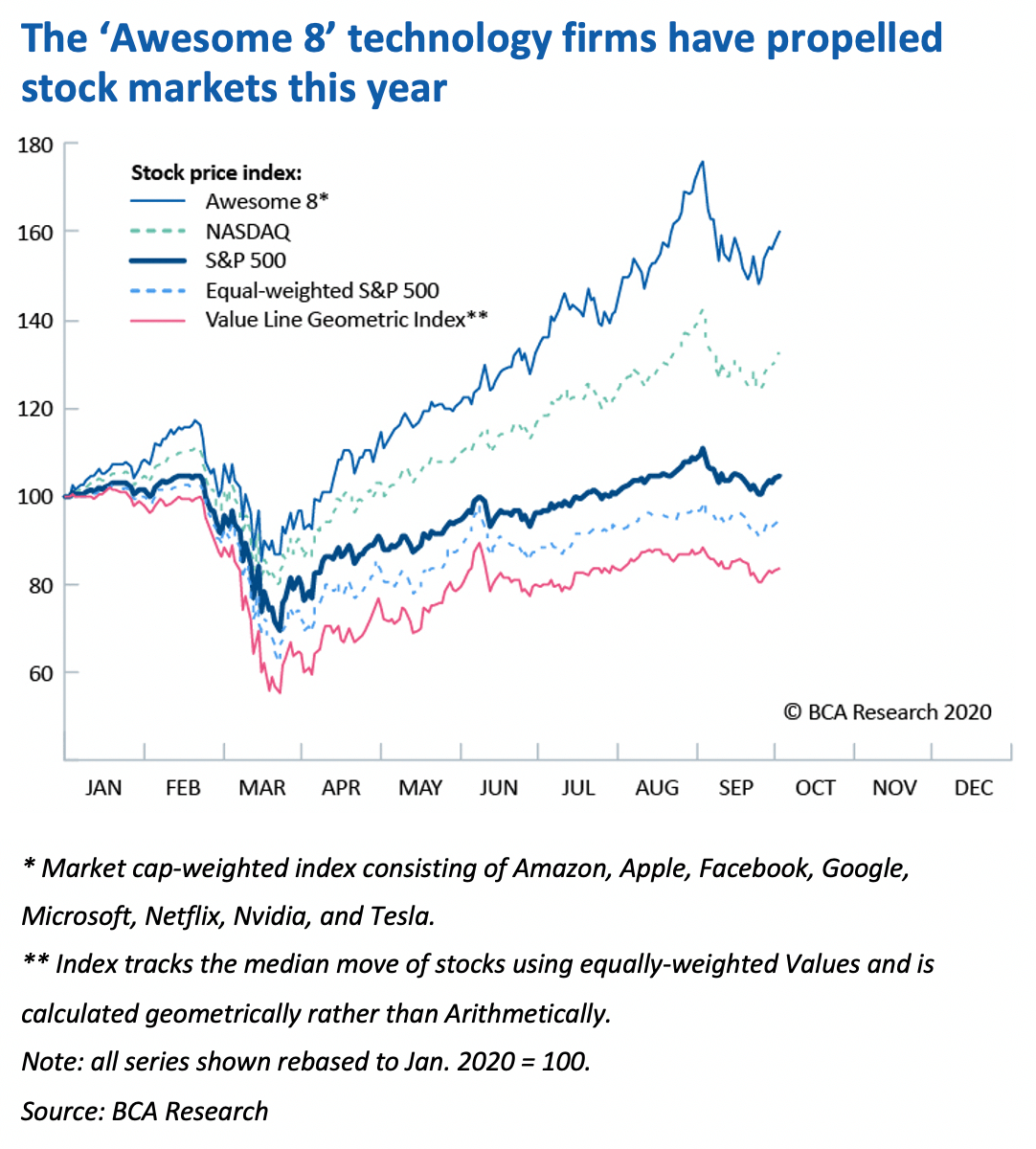

The election is particularly relevant for the large technology companies which continued to drive equity markets in the third quarter. Indeed, while the NASDAQ fell 5% in September, it still rose 11% over the three months and is up 25% this year.

These companies have logically been viewed as safe ports in a storm. Free from expensive and disrupted physical shackles, their digital products have become indispensable for our ‘everything-at-home’ lives. Furthermore, replicating software for new customers is largely a copy and paste job. This means that each additional dollar of revenue is nearly all profit. The resulting stream of cash can then either be reinvested for growth or hoarded for the future. For example, Alphabet has over $100bn of cash on its balance sheet – enough to buy almost any company in the FTSE. And because these companies are viewed as having growth stretching far into the future, their share prices have benefited as interest rates have fallen to record lows.

The outperformance of a limited portion of the market is not new. Dominant companies in the past were bigger as a proportion of the wider market than is the case today. However, with Apple now as valuable as the entire FTSE 100, we note that the old rule has not been repealed: trees do not grow to the sky. Size and growth are hard to reconcile, and these businesses will need to find new avenues if their success and dominance is to continue at the same pace.

This is looking increasingly difficult as regulators wake up. Last quarter the chief executive officers of Apple, Amazon, Alphabet (née Google) and Facebook were grilled before Congress and had to bend over backwards to emphasise their social merits and the vigorous competition they face (the latter itself a hallmark of monopoly positions). With the US-China spat ongoing and antitrust cases increasing, it looks likely that the largest technology firms will come under further scrutiny whichever way the US election goes.

“Throughout the centuries, what we’ve seen when the masses think the elites have too much, is that one of two things happens: legislation to redistribute the wealth…or revolution to redistribute the poverty.”

Alan Schwartz, Guggenheim Partners

For these reasons we have been careful about our exposure within portfolios. We have limited our holdings to those we think are least exposed to or will be less impacted by legislation, particularly avoiding those with social media dilemmas. We have then looked further afield, preferring companies in other industries harnessing technology and digitalisation. Technology is a ubiquity rather than a sector and those businesses that use it most effectively will prosper whether in the financial, healthcare or consumer realms.

A portfolio for all seasons

Many parts of the market have moved a long way in a short period of time. Investors have been quick to discount a vaccine breakthrough and going back to normal. However, faltering growth in many economies and renewed social restrictions as winter draws in suggest that the easy innings of the recovery may be nearly finished. While further support will likely stave off the worst-case outcomes, the coming months are likely to contain more upsets and higher volatility, even if the trajectory remains one of progress. Against this backdrop, we continue to hold a deliberate balance of assets that should perform reasonably well across a range of different economic environments.

“It is better to be roughly right than precisely wrong.”

John Maynard Keynes

At the heart of our portfolios remains a core of high quality, globally diversified companies. We continue to invest in a diversified group of businesses across a variety of sectors, but which display similar characteristics that we believe will underpin long-term sustainable growth. These firms are united by having strong underlying businesses and we have used the crisis to redouble our meetings with company executives, aware that as minority shareholders we ride on the coattails of management.

In our efforts, we are conscious that Coronavirus and low interest rates have made some parts of the market appear expensive. This includes some of the ‘Coronavirus winners’ that are likely to come under increasing scrutiny as we move through the US election and trade tensions persist. In these instances, we remind ourselves that high valuations can prove a case of borrowing returns from the future. After strong runs, we expect more pedestrian growth from some recent winners and have worked to uncover interesting opportunities elsewhere. Into these we are carefully deploying parcels of cash where we can.

“Historic returns are the rear-view mirror and the reverse gear has been left out of the investment gearbox. The windshield is an uncertain future.”

Jeremy Siegel, Professor of Finance, Wharton

Finally, we retain an array of protective assets. Whether in areas of the bond market, alternative assets, such as gold and absolute return funds, or cash, we seek assets that can help us weather the short-term setbacks that are the price of investing for the long-term. However, this has not come at the cost of simplicity. By avoiding the complicated, we benefit from the flexibility to trim our sails and run before the wind, rather than into it.

Whilst the extraordinary measures of six months ago are now treated with little more than a shrug we remain conscious that the post-COVID environment has yet to reveal itself. The economic damage may prove deeper and more permanent and the final quarter of the year will bring challenges both known and unknown.

With a substantial recovery in asset values already in place and a wide range of future outcomes – second waves vs vaccines, inflation vs deflation, recovery vs relapse – a cautious stance remains appropriate. We are focused on deepening our understanding and confidence in the securities we hold and ensuring long-term resilience in portfolios should the future take a turn for the better or the worse.

By Thomas Allsup, Portfolio Manager

Posted on 15 October 2020

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.

James Hambro & Partners LLP is a Limited Liability Partnership incorporated in England and Wales under the Limited Liability Partnerships Act 2000 under Partnership No: OC350134. James Hambro & Partners LLP is authorised & regulated by the Financial Conduct Authority and is a SEC Registered Investment Adviser. Registered office: 45 Pall Mall, London, SW1Y 5JG. A full list of partners is available at the Partnership’s Registered Office.