“Good times like the present, make bad times; a law sure as the swing of a pendulum.” Henry Phipps (from Henry Clay Frick, the Man, by George Harvey)

Recessions are inevitable

Mark Leach, Portfolio Manager

“Asset prices can go down as well as up”. As a regulatory requirement, this caveat, or similar, can be found on most investment literature today. It serves to remind the reader that all investments carry risk of capital loss – no doubt you will find it at the bottom of this document too. However, given the length of this business cycle, one can be forgiven for forgetting that recessions are inevitable and with them the certainty of asset price declines. As the economist Hyman Minsky recognised, recessions are the natural result of long periods of stability in an economy whereby complacency towards risk increases. As the cycle evolves, return expectations rise, appetite for debt grows and bubbles in asset prices occur.

Recessions are of significant concern for equity investors. As the economy contracts, unemployment rises, consumer spending falls and companies stop investing. The destructive nature of these events on human sentiment lead to a self-sustaining spiral of decline. For companies, falling activity results in negative sales growth and contracting profit margins, which coupled with the fixed cost of paying interest on debt has a magnified effect on company earnings. With sentiment weakened and the outlook bleak, shareholders must stomach the additional impact of overstated stock price declines as valuations (the share price relative to the company earnings) collapse. But if recessions are an inevitable downswing in the ebb and flow of the economic cycle then, “as sure as the spring will follow winter, prosperity and economic growth will follow recession.” (Bo Bennett, US entrepreneur)

The precipitous decline in share prices at the end of 2018 brought to the fore investor concerns that slowing economic momentum, threats of a trade war and rising interest rates would tip the US economy into a period of contraction. But in the first three months of 2019 we have witnessed a remarkable recovery in market prices with indices around the

world testing new highs and bringing the possibility that while economies and activity have slowed, we are not at the precipice of a recession.

“The odds change as our position in the cycle changes. If we don’t change our investment stance as these things change, we’re being passive regarding cycles; in other words, we’re ignoring the chance to tilt the odds in our favour.” Howard Marks, Mastering the Market Cycle

What does the data say?

As custodians of your capital, it is vital that we are watchful of the exogenous risks that the wider economic environment presents and that we use the tools at our disposal to limit extreme fluctuations in the value of your portfolio where possible. During 2018 we endeavoured to protect portfolios with higher cash levels because we recognised the backdrop of high market valuations and slowing growth as problematic in an environment of higher interest rates. This position served us well towards the end of the year. The current economic expansion, underpinned by low rates, and more recently by tax cuts in the US is now the second longest on record. However, the length of the cycle alone cannot be the only determinant of whether a recession is due. It is a common observation that cycles in the US rarely die of old age but are more likely killed off by the Federal Reserve as it recognises the risks of an overheating economy and uses higher interest rates to tame market forces.

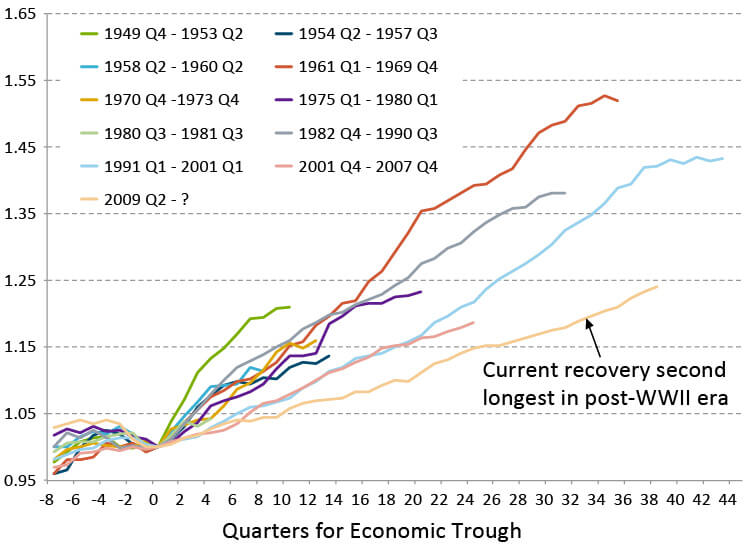

Figure 1 – US GDP Growth from Economic Trough to Cyclical Peak

(GDP Rebased to 1 at Economic Trough)

Source: National Bureau of Economic Research, Bureau of Economic Analysis, William Blair.

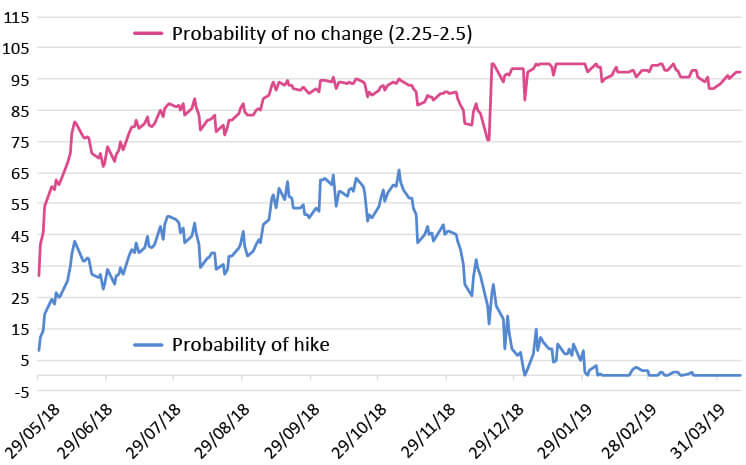

As figure 1 illustrates, this cycle does indeed stand out for its longevity, but it has also been the weakest on record as growth and inflation have remained surprisingly low. So, while it may be obvious to observe that we are more likely closer to the end of the cycle than the beginning, it remains extremely difficult to accurately predict when the next recession will finally occur. The primary driver of the sharp turnaround in markets at the start of this year was the dramatic shift in interest rate policy at the Federal Reserve. Towards the end of 2018 the message was that rates would continue to rise throughout 2019; however, the message today is that there will be no change to the Fed’s policy rate this year and some committee members are even advocating that rates be cut.

Figure 2 – The change in expectations for interest rates in the US

Source: Bloomberg.

While the more accommodative policy has been welcomed by the markets, the speed at which the language changed led many to speculate that the Fed had access to information that showed activity was deteriorating more aggressively than official data posited. We are not subscribers to this theory and it has left many investors sitting on the sidelines watching as markets have rallied. It is our view that the events of 2018 gave policymakers a window into the fragility of the recovery and provided enough evidence that raising rates at a time when other markets, most notably China, were slowing was not the right course of action.

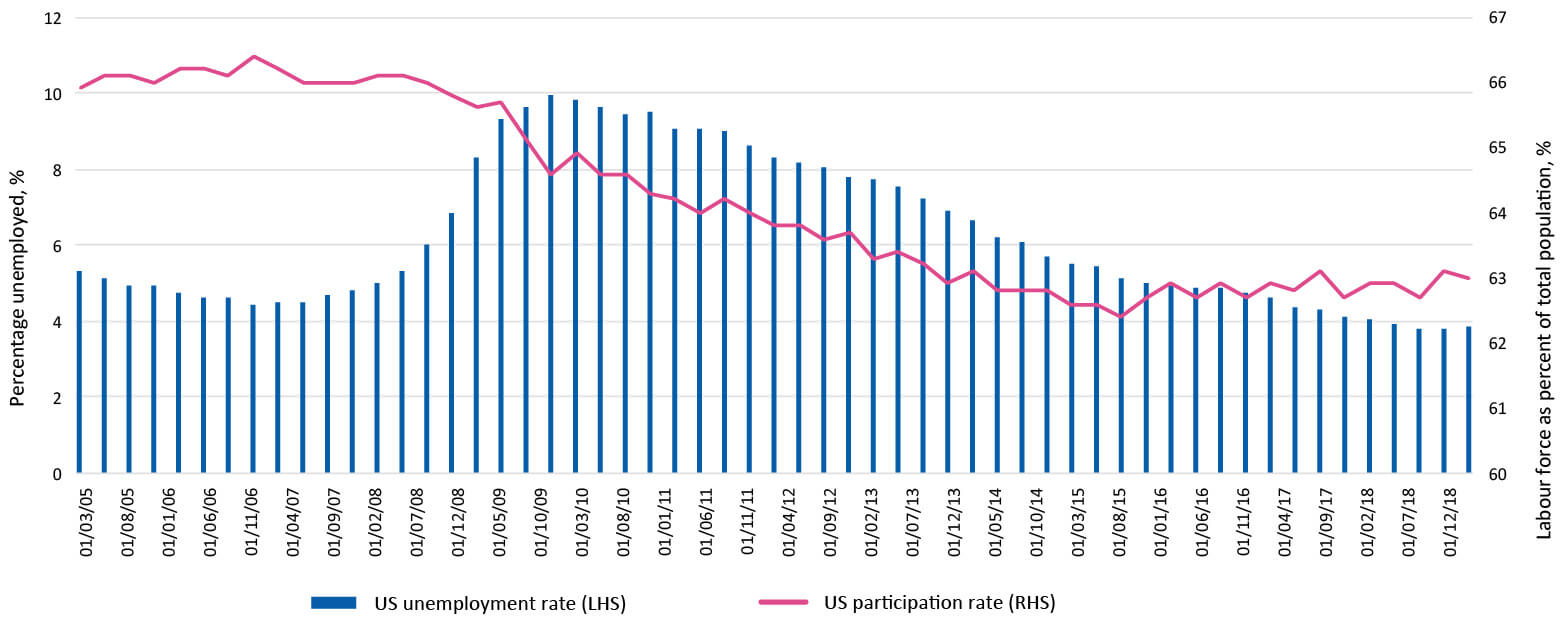

The Fed has additional comfort that persistently low inflation in the US economy gives them breathing room to steady the trajectory of interest rates. The US continues to print strong employment numbers – an important factor given the US consumer accounts for 70% of US GDP. But crucially, despite record low unemployment, inflation has been weak throughout this cycle and while it has started to pick up in some areas, such as wages, it has remained stubbornly below the Fed’s target rate. During the crisis many workers left the employment space altogether. As wages have risen so too has the participation rate, providing a steady flow of workers back into employment and keeping a lid on wage costs.

Figure 3 – US unemployment Rate & Participation Rate

Source: Bloomberg, Participation Rate is the total labour force as a percent of working age population.

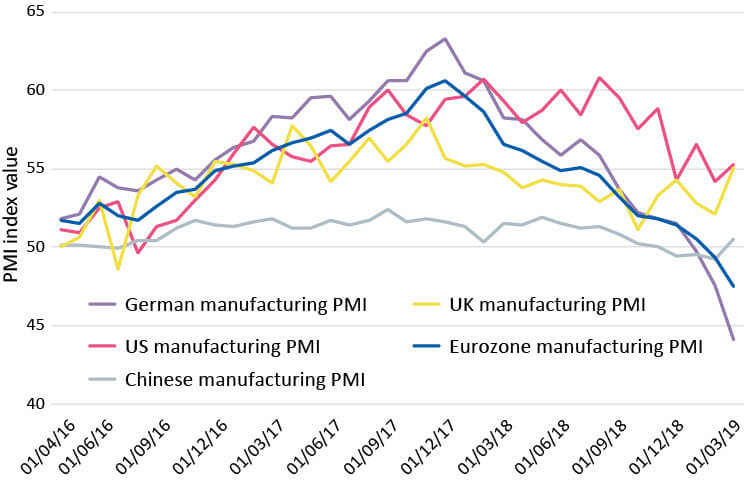

More widely the data today suggests that the global economy continues to display signs of vulnerability. However, there is evidence that the deterioration is slowing, and some areas are improving. As illustrated in figure 4, it is reassuring to see that a policy of stimulus in China is having a positive effect on activity – China is a crucial driver of growth for many exporting European countries, not least Germany.

Figure 4 – Global Purchasing Managers Index

Source: Bloomberg, 2019. The Purchasing Managers Index tracks the sentiment among purchasing managers at manufacturing firms.

It is also comforting to observe that since the end of 2018, analysts’ earnings forecasts have been revised down considerably. This reduces the risk that companies miss profit expectations going forwards and provides a firmer footing on which market valuations and sentiment can build.

Our main cause for concern is the level of indebtedness that exists in the corporate sector. Low interest costs and limited growth have given many companies a chance to borrow more, using the proceeds to either buy back shares or buy growth through acquisitions. Looking at key metrics such as profits relative to interest costs we are comfortable that, while interest rates remain low, the situation is containable for now. For some time we have had no exposure to corporate credit within our portfolios.

With investor sentiment and valuations far from euphoric, macroeconomic indicators stabilising and monetary conditions accommodative, we have become more positive on equities relative to our position in 2018. Our central thesis is that the next recession whilst on the horizon, but is not imminent.

“Even if one knows what the stock market was going to do, it would be more profitable to forget it and concentrate on trying to find the right stock to buy” Thomas Phelps, 100 to 1

Companies for all seasons

While Thomas Phelps’s comments, above, are deliberately provocative, knowing when the next recession will occur with any degree of accuracy is certainly very difficult. As the renowned investor and writer Howard Marks says, we need to recognise when there are extremes in the market that allow us to tilt portfolios to maximise return or reduce risk. However, the majority of our focus is spent seeking to identify the right companies to own for the longer term. It is vital to recognise that cycles occur but also that capital loss is only confirmed when crystallised. That is why time horizon is such a crucial consideration – knowing one will not have to sell at the trough of the cycle.

At JH&P, we construct portfolios with a central pillar of high-quality companies and funds around which we use other assets classes to provide diversification and risk mitigation. As long term investors in companies (rather than mere renters of shares) we need to be comfortable with owning these businesses in bad times as well as good. Therefore, we seek to identify characteristics that limit the cyclicality of company earnings in periods of economic weakness. We look to own businesses that produce mission critical products or provide services that have a recurring nature. The companies we seek have strong secular growth drivers that can moderate short-term cyclical swings. In addition, they have high levels of market share which gives them greater pricing power and higher profitability than the average company. These companies will also typically carry lower levels of debt relative to their ability to generate cash flow.

If recessions are an inevitable part of the economic cycle, then it is the above characteristics that allow companies not only to protect earnings but also to give them the ability to invest when others are not and to ultimately exit the recession – in the equally inevitable recovery – stronger than they entered in. Our refusal to own highly leveraged companies provides a level of protection so that should we be wrong in our thesis, as we inevitably are from time to time, the downside is limited.

Past performance is not a reliable indicator of future performance. James Hambro & Partners LLP is a Limited Liability Partnership incorporated in England and Wales under the Limited Liability Partnerships Act 2000 under Partnership No: OC350134. James Hambro & Partners LLP is authorised & regulated by the Financial Conduct Authority and is a SEC Registered Investment Adviser. Registered office: 45 Pall Mall, London, SW1Y 5JG. A full list of partners is available at the Partnership’s Registered Office. Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently). The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.