27.08.2021

Don’t run scared of lifetime allowance limits

Charles Calkin, Partner, Financial Planner

Charles Calkin, partner and financial planning consultant

In the piece, which first appeared in the Financial Times, Charles Calkin looks at what investors at risk of breaching the pensions lifetime allowance (LTA) should take into consideration.

In the past few weeks I have had two clients pay tax charges running into hundreds of thousands for breaching the pensions lifetime allowance.

Numbers released recently show that 7,130 people paid £283 million between them in 2018/19 for similar breaches. This looks set to be a big earner for HM Revenue & Customs in the coming years, particularly if the Chancellor fulfils whispered threats to reduce the allowance further, to either £900,000 or £800,000.

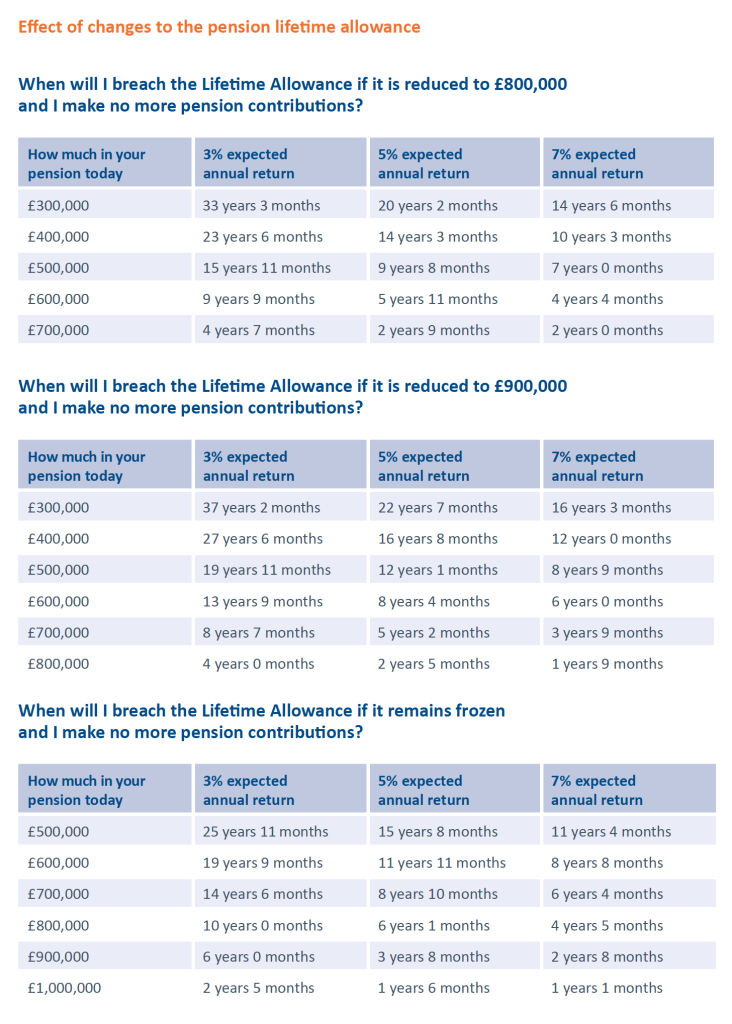

Lifetime allowance limit

Many people approaching the current limit of £1,073,100 are questioning what to do about it. That includes anyone with an uncommuted final salary pension of close to £53,655. This is because HMRC calculates the value of these pensions by multiplying the “defined benefit” by 20.

Download PDF

The lifetime allowance is the amount you can accumulate in pension savings over your lifetime without incurring a tax charge. The charge is 25% on any money exceeding the allowance that you elect to withdraw as income (on top of any income tax you might pay) and 55% on any money you draw as a lump sum (with no income tax to pay). Drawing on your pension is known as “crystallising” it. If you leave your pension savings untouched (“uncrystallised”) you will be tested for the charge when you reach 75 or if you die before then.

The immediate response of many savers is to focus on avoiding the charges by keeping their pension savings below the ceiling. But is this wise?

Many suggest you stop paying contributions if you are nearing the limit – or prospective limits. I would be wary of doing that too soon. Illness or redundancy may force you to retire early. In this which case you would have needlessly stopped saving tax-efficiently, and rates of relief may not always be so generous as today. Money in your pension grows free of tax and is free of Inheritance Tax (IHT) when you die. These can be substantial benefits.

Scenarios to consider

There are several other scenarios where ceasing contributions might be counterproductive.

If your employer is paying into your pension and will not give you the benefit any other way then you might as well continue to take it, even though you may be taxed punitively. It’s better than nothing! But do ask if your employer will pay it as taxable income instead.

If you are a higher-rate taxpayer and salary sacrificing, you save 40% income tax and the 2% National Insurance (NI) charge. So you enjoy a 42% benefit. Your employer saves 13.8% in NI as well, and some will add this to your pension contribution – bringing the tax saving to over 55%.

If your salary is between £100,000 and £125,140 then you are effectively being taxed at 60%, because for every two pounds you earn above £100,000 you lose one pound of your personal allowance. So if your taxable income, after allowing for charitable donations, is over £100,000 you might consider paying this element into your pension fund.

If you own your own company then pension contributions on your behalf come off the company profits. They reduce your corporation tax bill, making it an effective way to take profits tax-efficiently. Again there are NI savings.

If you have earmarked your pension savings for your children then you can be growing them tax-efficiently. At 75, if you have any benefits you have not accessed, you will pay the 25% charge on anything over the LTA. The remaining fund then passes to your children on your death free of IHT (usually payable at 40%). They pay income tax at their marginal rate of tax on any withdrawals. That is not a bad deal. Withdrawals are free of income tax if you die before 75.

Lifetime allowance protection

It is worth pointing out that there are various forms of LTA protection, which means you may be entitled to a higher LTA than the standard rate. If you (or anybody on your behalf) have not made any contributions to a pension since 5th April 2016 then you may be able to claim a personal LTA of £1,250,000 in the form of Fixed Protection 2016 assuming you were a member of a suitable scheme.

Those close to the limit and over 55 may consider taking the 25% tax-free lump sum – a benefit that may not last forever either. The growth on this money will not then be subject to these charges, but if the money is invested in assets outside an ISA, you may face Capital Gains Tax on future disposals. And the money does not have the IHT benefit of a pension.

You can take taxable income from your pension each year to prevent it from breaching the LTA – or at least mitigate any final LTA bill. But be warned, if you might still want to contribute to your pension, once you start taking income your contributions are limited to £4,000 a year.

Even if you restrict contributions and withdraw capital you may breach the limit, simply through growth – and especially if the allowance is reduced. If it falls to £800,000 then someone with £500,000 in pension savings, generating 7% a year net returns on their portfolio, will hit the ceiling in seven years. (At the current allowance level it is 11 years and four months.) Dial down your risk and bring returns to 3% and it will be 15 years and 11 months before you breach the limits (25 years and 11 months at today’s limit).

When might you breach the lifetime allowance?

You might want to look at your savings as a whole and have the lower-risk elements in your pension, leaving your ISAs to do the grunt work for returns. But I would caution against being too cautious in your pension just to avoid a tax. That smacks of cutting your nose off to spite your face. Some investors who have breached the limits may even be tempted to increase their risk, because the impact of losses is mitigated by the tax savings that come with them.

Those clients I mentioned earlier were lucky. They had secured fixed protection to ensure they enjoyed the old limit of £1.8 million. The tax is paid out of the pension fund so they did not have to find it from elsewhere. And they knew what was coming. It has not stopped us managing their money for growth. They saw the charge as a tax on success. But, of course, it hurt.

Need for advice

This is fiendishly complex and there are numerous factors to take into consideration when deciding your own response. You might ask why any Chancellor ever thought such a charge sensible. It is surely simpler to limit how much people put into their pension and the rate of tax relief, rather than penalising their success at investing money wisely.

But we live with what we are given. For people with pension savings approaching the limits there are significant costs to mismanaging your pensions – or big savings from managing their strategy correctly.

It’s worth taking the time to make the right choices.

Charles Calkin is a financial planner at wealth manager James Hambro & Partners

Published August 2021

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.