It was another tough month for investors after Russia’s invasion of Ukraine hit global markets. While the humanitarian impact can be profound, the impact of geopolitical shocks on markets has historically proven short-lived with long-term returns dependent on economic growth, corporate earnings and interest rates.

The past month has seen the brewing crisis in Ukraine come to the boil. Few can watch the images coming from Ukraine without rising horror, but as investors we have a duty to consider matters dispassionately and make balanced judgements about how to protect our clients’ assets during unsettled times.

Russia’s invasion has thrown a wrench into the gears of the global economic recovery from COVID-19, at least in the short term. It threatens to disrupt global energy supplies, resulting in a rise in oil and gas prices, which will hit Europe hard and potentially ripple out across the global economy. This comes on top of the decline in market sentiment already evident in January and February, prompted by soaring inflation rates and the prospect of monetary tightening from central banks.

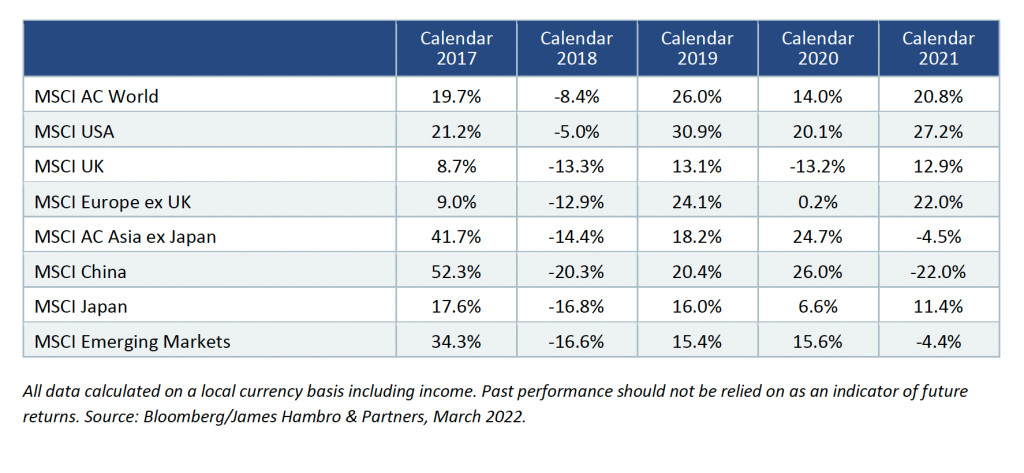

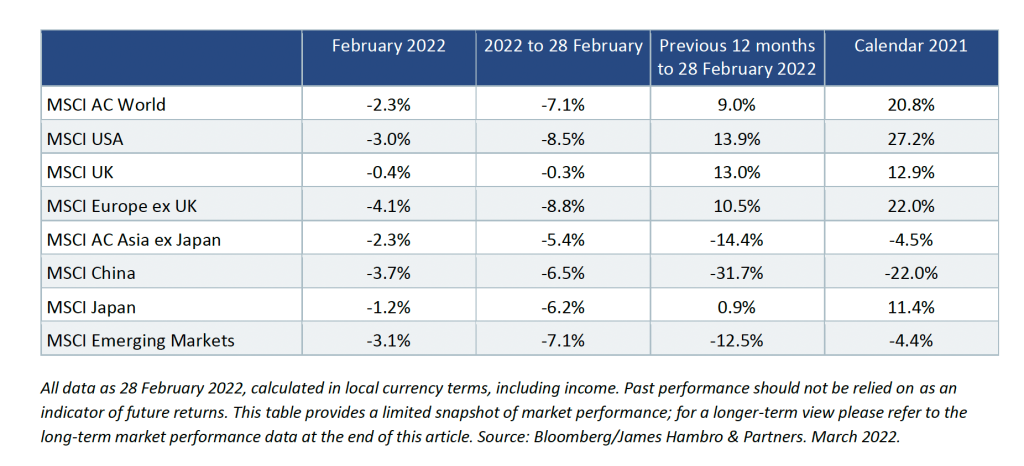

Global markets tumble

The eruption of hostilities sent stocks tumbling across the board. The MSCI AC World Total Return index fell –2.3% in February and is down -7.1% over the year-to-date, in local currency terms. It was a particularly painful month for Europe, which is heavily dependent on Russia for energy supplies, although the EU has hurriedly put plans in place to reduce this reliance.

Our portfolios have no direct exposure to Russian assets and modest direct exposure to the domestic European economy, so are insulated from the worst impacts to some extent. However, we expect the military conflict to add to the current market-wide challenges and increase market volatility.

Market sentiment is changing rapidly as sanctions come on stream and political alliances take shape. Last year’s growth winners, such as tech, health care and consumer stocks, have struggled the most in 2022, and the last weeks of February saw a flight to safety, which benefited quality stocks, and the US in particular, at least on a relative basis.

As things stand, the prospects for global growth remain positive, but the invasion of Ukraine poses increased risks to that view.

- Russia is the world’s second-biggest exporter of crude oil (11% of world exports) and also one of the largest natural gas exporters. As a result, energy prices have spiked upwards over fears that sanctions on Russia could cause global energy supply disruptions and the price of Brent crude oil reached as high as $131 a barrel. Prices have dropped back since the UAE intervened with OPEC to urge oil producers to increase production but are likely to remain elevated while the crisis endures.

- Higher energy prices will add to inflationary pressures all through the supply chain, leaving consumers with less money to spend, putting a further dampener on economic activity. This puts central banks in a difficult position as they move to normalise the money supply without choking off the recovery.

The invasion of Ukraine has put more pressure on oil prices

Quality is the place to be

Our preference for established quality companies has helped us avoid some of the worst extremes of market falls. We have already been gradually reducing our exposure to areas of the market where valuations are high, and where we see a degree of risk from higher inflation. As we hold on to the accumulating liquidity, we are looking for entry points in more promising positions or opportunities to add to our favoured positions at attractive valuations.

Our tactical allocation is evolving as asset prices move. Our allocation to equity has moved lower, while the rising gold price has increased the proportionate allocation to gold which has proven a successful haven in times of war and inflation. While we see no reason to accelerate this process for the time being, we are monitoring the ongoing situation carefully and will continue to act in line with our long-term views.

In it for the long run

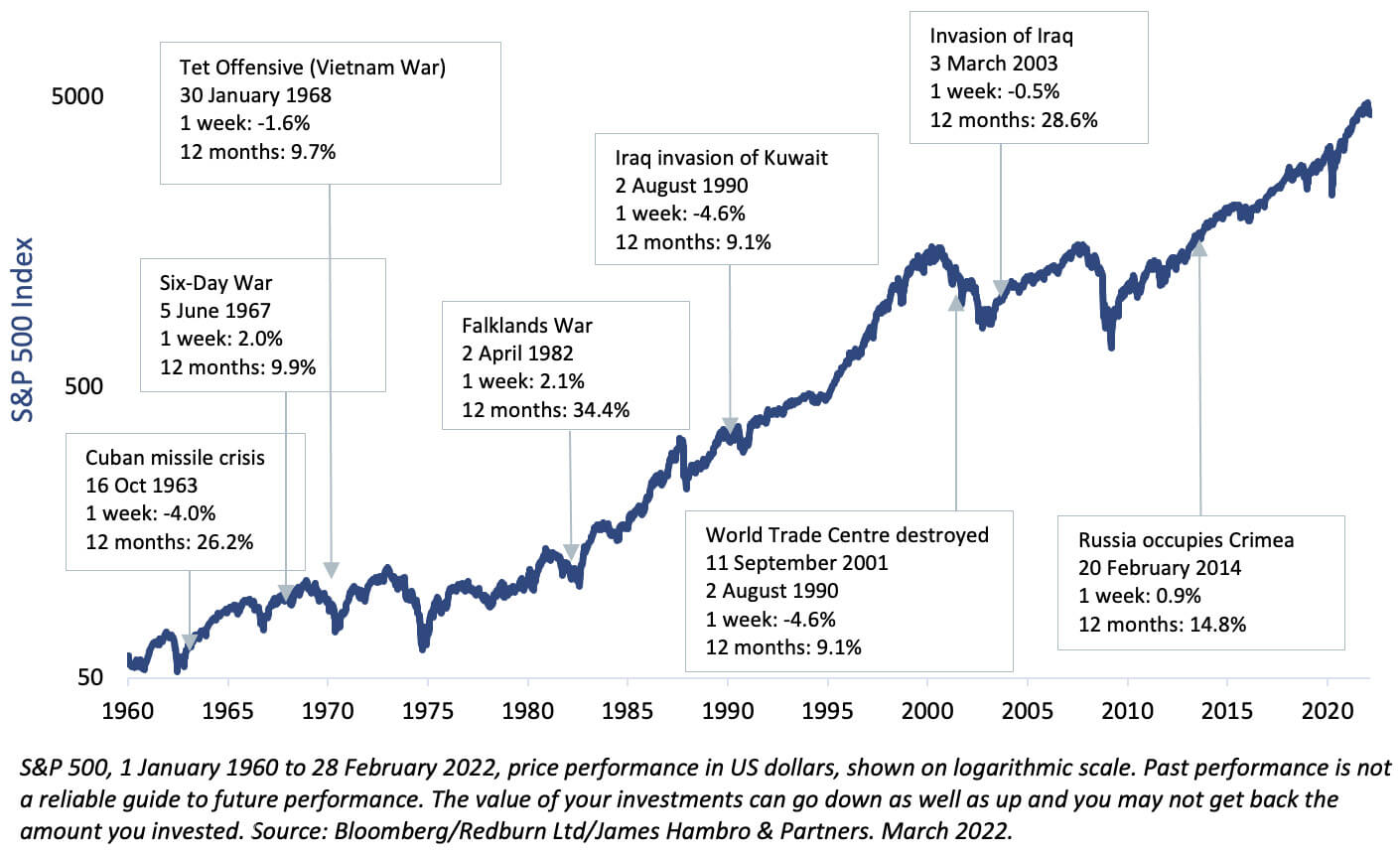

Events such as those seen in Ukraine are highly alarming and have left markets on edge. The shock of images can have a powerful affect and lead to sharply negative sentiment in the short term.

However, market sentiment can swing quickly, and the underlying economic picture and company fundamentals are what drive investment returns over the long term. History shows us that while geopolitical shocks can cause asset prices to swing significantly, they don’t tend to disrupt underlying trends in the long run.

Market reaction to military conflict is typically short-lived

Investors concerned about the value of their portfolio in the short term should be invested in lower-risk assets that are less likely to be impacted by these events. Long-term investors need to hold their nerve and only make moves when it becomes clear that market drivers have changed.

Global tensions on the rise

It seems a long time since Francis Fukuyama declared the end of history in 1992; as with Mark Twain, it would appear that rumours of its demise are grossly exaggerated.

In recent years we have seen Brexit, the US-China trade war, and rising tensions between the US and Iran. Rising nationalistic sentiment in many countries has also given geopolitical considerations greater importance. It’s possible that we are witnessing a shift away from the globalisation consensus that has driven economic growth since the 1990s in favour of more protectionist policies.

This is just one of the longer-term trends that we are keeping watch over. Our investment approach has been built by focusing on the fundamentals of companies rather than short-term price movements when selecting stocks. Our investment professionals thoroughly research each individual company to determine its financial strength, selecting a mix of assets to ensure portfolios are balanced.

We invest in high-quality and growth assets, while ensuring company valuations look reasonable given their medium-term prospects. We are confident that this approach makes sense over any reasonable time frame. While politics, policy and sentiment have regularly driven swings within asset markets over shorter periods, corporate and economic fundamentals have proven the most reliable driver of growth over time.