INDUSTRIAL RENAISSANCE: A NEW ECONOMIC FOUNDATION

Major events such as wars and pandemics have historically marked turning points in the economic environment. COVID-19 and the Ukraine war are likely to leave a similar legacy.

The medium-term outlook for the industrial economy is clear. High inflation is a symptom of underinvestment. The cure is greater capacity and productivity.

Powerful structural trends tied to the energy transition, remaking of supply chains and targeted investment in strategic industries will support a decade of higher capital investment with demand boosted by government subsidies.

Rising energy and labour costs encourage companies to invest in efficiency-enhancing digital technologies to modernise ageing facilities while reducing their environmental footprints.

This should prove a potent cocktail for a long-awaited industrial renaissance.

2010s: The internet era

Entrepreneurs have never been short of ideas but without customers and cash they remain just that.

Apple’s iPhones and Google’s advertising gave them an audience. ‘Pay-as-you-go’ services, from Amazon’s cloud servers to Microsoft’s software, offered a business model. Investors opened their cheque books, comfortable in the knowledge that the Federal Reserve would take care of any bumps in the road.

The combination of easy money and new technologies from Silicon Valley created a golden age for high-flying growth stocks. Valuation concerns took a back seat to stories of disruption, rapid growth and the promise of ever-expanding end markets.

At the same time, a long hangover from the financial crisis weighed on traditional, economically-sensitive industries. With consumers, corporates and governments attempting to move away from the debt-ridden excesses of 2008, there was scant appetite for large-scale industrial investment. China’s shift from resource-intensive infrastructure and manufacturing to a more services-driven economy and the painful aftermath of the North American shale oil boom added further headwinds to sectors tied to global commodities demand.

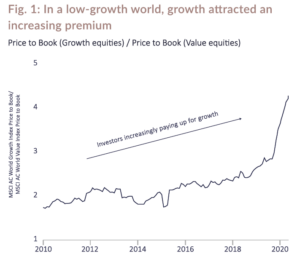

With growth scarce, the premium attached to those able to deliver expanded steadily, before rocketing higher during the pandemic (Fig 1).

Past performance is not a reliable indicator of future performance. Source: Bloomberg, MSCI. Growth equities represented by MSCI AC World Growth Index. This index captures companies exhibiting overall growth style characteristics, defined using historic and future expectations of sales and earnings growth. Value equities represented by MSCI AC World Value Index. This index captures companies exhibiting overall value style characteristics, defined using several measures of valuation, including book value to price and dividend yield.

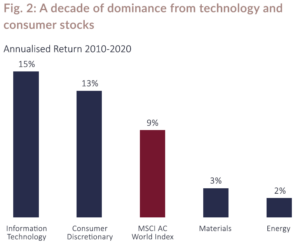

Faster growth allied to rising valuations created a compelling formula for outperformance in an ever-more concentrated market. Owning large chunks of the technology and consumer discretionary sectors, the latter the home of Amazon and Tesla, was a recipe for investment success. Paired with an avoidance of heavily cyclical, asset-intensive energy and materials companies, the path to market-beating returns in the 2010s’ paradigm is clear (Fig. 2).

Past performance is not a reliable indicator of future performance. Source: Bloomberg. MSCI ACWI Total Return in local currency

Gradually, then suddenly…from Big Tech to Big Government?

However, by the end of 2010s signs were emerging that the low inflation, low growth, low interest rates environment was beginning to change. Political populism on both sides of the Atlantic pointed to a new era focused on ‘taking back control’ and reducing international cooperation.

Events of the past two years have added fuel to this fire. The pandemic exposed vulnerabilities in complex supply chains, waning domestic production capabilities and a lack of investment in healthcare. Russia’s invasion of Ukraine revealed the risks in relying on others for vital resources. Securing access to energy while transitioning to cleaner methods of production have assumed renewed importance. Rising geopolitical tensions spurred governments to play a greater role across wider swathes of the economy, with defence spending and investment in strategic industries taking centre stage once more.

The post-COVID world looks to be characterised by a prioritisation of economic resilience over optimisation. Valuing security over efficiency will come at a price. Add in a tight labour market (another legacy of the pandemic) and the prevailing tendency of inflation seems likely to change from dropping too low to breaking too high.

Should these trends persist, the 2020s could prove a decade of higher, but also more volatile, growth, inflation and interest rates. This would translate to shorter economic cycles and more evenly distributed stock market leadership than the pre-pandemic decade.

A long-awaited capex revival

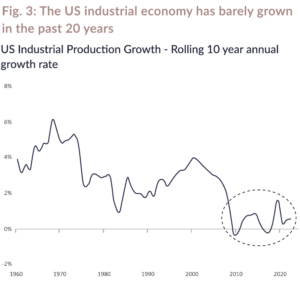

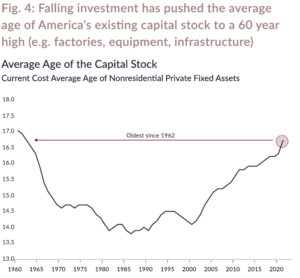

These seismic shifts are driving the re-shoring of supply chains, investments in energy security and decarbonisation and broad-based infrastructure upgrades to kick-start economic growth and create new jobs. After a long period of underinvestment, many of the post-pandemic themes are supportive of a much-needed resurgence in industrial activity, particularly in the US (Fig. 3 & 4).

Source: Bloomberg, Federal Reserve Economic Data

Source: Bureau of Economic Analysis, William Blair Equity Research

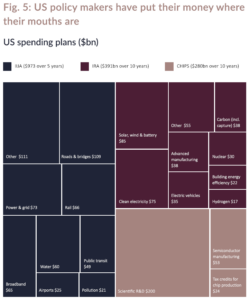

Rhetoric is starting to be backed by government action. The Biden administration has recently passed three major spending bills that will make $2tn available to improve the US’s economic competitiveness, innovation, and industrial productivity, all while dramatically reducing its carbon emissions.

The Inflation Reduction Act (IRA) contains $400bn in subsidies for energy security and climate change investments over the next 10 years. The CHIPS Act, which promotes the build out of US-based semiconductor manufacturing, provides $280bn in spending and incentives. Finally, the mammoth $1tn+ Infrastructure Investment and Jobs Act (IIJA) offers expansive funding to address transport, energy and power infrastructure, access to broadband internet, water infrastructure, and more (Fig. 5).

While Europe’s response to the US IRA still needs to be finalised, spending of €50bn per year is mooted to be on the table to drive forward green technology on the continent.

IRA is Inflation Reduction Act; IIJA is Infrastructure Investment and Jobs Act, CHIPS is Creating Helpful Incentives to Produce Semiconductors. Source: Redburn

Companies will be incentivised through subsidies to upgrade ageing factories and manufacturing lines which should sustain profit margins in the face of rising energy and raw material costs.

Whether the government is up to the task of managing such an ambitious agenda is a fair question, and, with unemployment at 50-year lows and increased restrictions on immigration, the lack of affordable workers is likely to create headaches. Ultimately this too may help promote a pickup in investment with companies looking for solutions where capital may be usefully employed to improve efficiencies (read: replace jobs!). In effect this will mean a move towards greater automation, with the adoption of machine learning, robots and AI to make processes more productive and less wasteful.

So far, so good, so what? Investing in the age of resilience.

A faster growing global economy with a more balanced split between the consumer and industrial economies should provide a far broader set of opportunities for fruitful long-term investment.

In the prior cycle, companies capable of delivering sustainable growth at high returns were mostly found in the technology, consumer and healthcare sectors. Many of the trends that supported such growth remain in place today. Cash to card, digital advertising and online shopping still have many years of growth ahead. Solutions that offer better medical outcomes at lower costs will be embraced with open arms by stretched healthcare budgets. Software is still eating the world.

But investment in supply chains, infrastructure, energy security, factory automation and decarbonisation now have the potential to transform the growth prospects of companies across industrial, energy and mining sectors too.

Fixing supply chains for a fractious world

“Basically, there is air – and TSMC.” Jensen Huang, CEO Nvidia

The most important product in the world is overwhelmingly produced on a small island 100 miles off the coast of Southeast China.

Microchips are ubiquitous in modern electronics, from everyday products like TVs and electric toothbrushes to military spearheads like cruise missiles and fighter jets. As technology continues its advance, the chips within every device must advance as well. For those that wish to be at the forefront of technological change access to advanced semiconductors is essential.

The Western world’s reliance on Taiwanese-made semiconductors is not new but rising tensions between the US and China has revealed vulnerabilities in the supply of the most sophisticated chips, where Taiwan’s TSMC retains a virtual monopoly. By one analysis, TSMC produces a staggering 92% of the world’s cutting-edge semiconductors.

The COVID-19 pandemic and Russian invasion of Ukraine heightened public and political awareness of the importance of semiconductors for all manner of applications. Fragile global supply chains were exposed, with shortages of chips hampering production of everything from cars to washing machines.

The CHIPS and Science Act, signed into law by President Biden in August 2022, grew out of a $12bn deal to bring TSMC to American soil. The Act now provides almost $300bn to boost American semiconductor research, manufacturing, and supply chain security, with the explicit aim of sidelining China from the sector.

Early evidence suggests the incentives are working. Major US-based investments have been announced by both domestic and international semiconductor giants such as Intel, Texas Instruments, Micron, TSMC and Korea’s Samsung.

TSMC alone now plans to spend $40bn to bring the world’s most advanced chip production technology to Arizona by 2026. The spill-over from these investments will be substantial and will stimulate capital spending across a spectrum of industries. Building and operating advanced semiconductor manufacturing facilities demands vast quantities of equipment and material, from machinery to instruments, chemicals to gases, and labour to cleaning supplies. Not to mention significant incremental demand for power – both conventional and renewable.

Given the powerful stimulative effects, there is every reason to believe that new and planned chip factories in the US could help unlock a broader resurgence in manufacturing with its related benefits.

Beyond the first-order recipients such as chip manufacturer Texas Instruments, where the US government is effectively paying for them to expand their capacity, the future now looks brighter for a range of companies exposed to the wider US industrial economy. Industrial gas giant Linde, equipment rental company Ashtead or America’s leading freight rail company Union Pacific are all examples of companies we have long admired but where the growth outlook has materially improved.

Net zero is going to require a lot of carbon

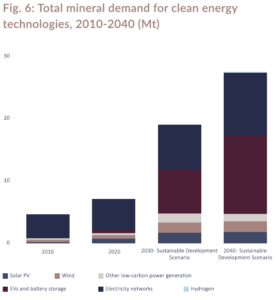

The transition towards a lower carbon world will be incredibly metals intensive.

Clean energy technologies – from wind turbines and solar panels to electric vehicles and battery storage – require a vast range of minerals and metals. An electric vehicle (EV)requires six times the mineral input compared to a conventional car, including over twice the copper as well as significant amounts of nickel, lithium, graphite and cobalt.

The International Energy Agency (IEA) estimate that clean energy related demand for minerals will have to quadruple in the twenty years to 2040 if we are to reach the key energy-related goals of the United Nations, including the climate goal of the Paris Agreement (Fig. 6).

Source: International Energy Agency

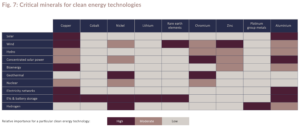

Technologies related to the energy transition have already become a major factor for overall demand for some minerals. In the past decade EVs and battery storage have overtaken consumer electronics to become the largest consumers of lithium, together accounting for 30% of total demand.

As countries step up their climate ambitions, investments to decarbonise economies are set to become an important source of demand for most minerals, particularly copper, aluminium, nickel and zinc.

Source: International Energy Agency

While shifting to a low carbon economy is clearly positive, the reality remains that extracting, refining and processing the required raw materials will carry a near-term environmental cost.

Russia’s invasion of Ukraine created an increased sense of urgency. There has then been an overdue acceptance of the role fossil fuels must play during the energy transition in the years ahead. All are positive developments for companies operating in these most demanding of sectors.

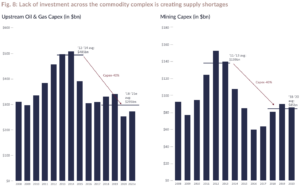

Historically we have found investing in commodity producers challenging. There is a long-held law in commodity land that the cure to high prices is high prices. In a traditional cycle, higher prices of oil, copper or iron ore create an economic incentive for producers to drill new wells or build new mines. When that supply hits the market, prices respond accordingly – usually at just the point that demand is falling.

A vital difference today as compared to previous cycles is the relative lack of supply response to the combination of higher prices and a more favourable picture of longer-term demand. Even in a world of weak Chinese growth, supply in big commodity markets such as aluminium, copper, nickel and oil is already looking tight.

Several factors have contributed to this paucity of supply. The bursting of the Chinese-inspired ‘commodity super-cycle’ in the early 2010s drove a period of forced deleveraging, asset sales and capex cuts (Fig. 8). Share price pressures and management team changes then acted in concert to force the industry to adopt a new mantra of cash returns over asset growth. More recently, the decarbonisation agenda, supported by growing awareness and implementation of ESG considerations on the part of investors, has created a backdrop where governments, key stakeholders and society at large are uncomfortable with the idea of energy and mining companies adding new fossil fuel intensive projects to their future business mix.

Source: Bank of America, Bernstein, Colossus

These structural supply shortages have created the tightest supply/demand balance for decades, which is likely to keep prices higher for longer.

Much like the industrial world, the outlook for many commodities is considerably brighter after a long period in the wilderness. These improved dynamics are making the likes of Shell, Rio Tinto and BHP more attractive as a potential home for long-term investment within our portfolios.

Data, digitalisation, automation: producing more from less

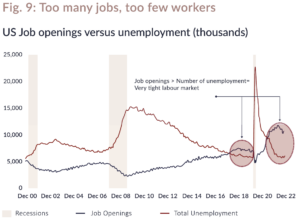

One of the most notable factors in in the US economy over the past few years has been the shortage of workers. While clearly exacerbated by the pandemic, this is not purely a COVID-19 phenomenon; there was a growing excess of demand for workers even prior to 2020 (Fig. 9).

Source: Bureau of Labour Statistics, William Blair Equity Research

Falling labour participation rates – a function of increased early retirement, growing university enrolment, health and drug abuse impacts – have combined with ageing demographics, slower population growth and falling immigration to reduce labour force growth over the past decade. In the UK, Brexit has provided its own shock to the labour force. With fewer workers to serve consumers there is a growing burden on the existing workforce to become more productive if our economies are to avoid embedded wage inflation.

For companies, the question is obvious: how to deliver more output from less input? As is so often the case, technology has the answers.

As industry becomes truly computerised, we expect a revolution in how things are made. Opportunities abound for providers of the necessary tools, software, sensors and semiconductors that can help automate, integrate and interpret in an increasingly digital and connected world (Fig. 10).

Source: Elite Electronic Systems Ltd

We recently met with the management of Amphenol, a leading manufacturer of electrical, electronic and fibre optic connectors and cables. A company well-placed to benefit from these trends.

The business is benefitting from durable long-run growth tailwinds tied to rising electronic penetration across multiple end markets, including industry, automotive and aerospace and defence. Wherever there is electrical content, there will be connectors and cables.

These are ‘mission-critical’ products and services (no-one wants their iPhone to catch fire or car to break down) yet only represent only a small portion of customers’ overall spend, giving the likes of Amphenol the ability to pass on higher prices over time, especially valuable in a more inflationary world.

Many of Amphenol’s products are required to function in harsh environments with near zero redundancy – think fighter jets and car drivetrains. This means close engagement and long relationships with customers to produce highly engineered solutions, often beginning at the product development stage. Switching costs and barriers to entry for potential competitors are high.

Similar characteristics can be found at Texas Instruments (TI), the world’s leading analogue semiconductor company. Analogue semis convert “real world” signals such as temperature, pressure and sound and into digital signals that can be processed by other chips. Every electronic device has analogue content, from cars to medical equipment to home appliances, and rising chip content is key to products becoming more digitally sophisticated over time.

Much like a connector, an analogue chip typically plays a very important role in a product, for example, the airbag crash sensor, but represents a small proportion of the cost of materials. As a result, competition tends to be less on price and more on product quality, availability and service, creating a subscription-like business with consistent revenue from long-lasting and low-churn products.

What’s more, unlike their more advanced, computer-focused digital semiconductor cousins, analogue chips are built on older technology less at risk of being innovated away, reducing capital intensity and technological risk.

Semi content is certain to grow strongly amid electrification of vehicles and the rising use of automation across industrial applications. TI should be able to translate their superior manufacturing and cost structures into higher margins and share gains too.

Hidden champions for a new world

The economic environment is changing. This is likely to usher in fresh leadership as different companies come to the fore. However, we think the future’s winners are likely to have similar characteristics to the businesses we have always looked for: durable competitive advantages we can understand, exposure to growing markets, robust balance sheets and aligned management teams with equal parts talent and integrity. If bought at reasonable valuations and held for a number of years this approach can be rewarding in any environment.

We often find these companies operate out of the limelight. Amphenol’s connectors and TI’s chips, Rio Tinto’s minerals and Union Pacific’s railcars, Linde’s gases and Ashtead’s equipment. These are the enablers of progress, acting as a royalty on the investment and growth of others. And the pace is quickening.

We have spent much of the past year adapting portfolios to account for the shifting economic winds, embracing the evolving world in front of us beyond the short-term concerns around the next interest rate announcement or jobs report. Portfolio asset allocations are more balanced and equity exposures broader reflecting the increased opportunities and the scope for the world of tomorrow to look quite different to that of today.

Article written by Dan Zegleman, Portfolio Manager.

For illustrative purposes only and should not be construed or relied upon as advice.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.