A BRIGHTER OUTLOOK WARRANTS A MORE BALANCED APPROACH

Our view in short

- 2024 has started well. Company updates have revealed broader-based growth alongside expectations that business momentum will accelerate through the year.

- The strong finish to 2023 reflected peaking interest rates and falling inflation. Recent moves have been driven by increasing confidence in the sustainability of economic growth.

- Inflation continues to moderate, albeit slowly. Central banks remain on course to begin reducing interest rates in the months ahead.

- The US economy has weathered significant downturns in the manufacturing economy and housing market. Both are likely to improve through 2024 supported by lower rates. This would provide a significant boost.

- Infrastructure spending linked to recently enacted government policy is ramping. The medium-term outlook for the industrial economy is promising.

- Semiconductor and technology companies are benefiting from the build out of infrastructure necessary to power artificial intelligence (AI) models.

- Whilst AI is a dominant market theme, earnings growth is strengthening across a range of sectors. We expect the broadening out of equity market returns to continue.

- Structural changes since the COVID pandemic suggest a different economic environment in the years ahead.

- The promise of AI-linked productivity improvements combined with government-assisted capital investment should lead to higher economic growth.

- Stronger growth may be balanced by more frequent supply shocks leading to shorter economic cycles and greater variability in inflation and interest rates.

- More diversified portfolios will be needed to navigate these dynamic economic and investing conditions.

Party like it isn’t 1999

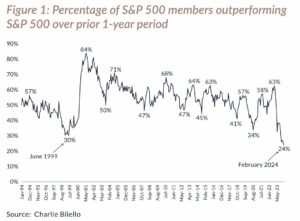

Our last quarterly ended with a prediction that stock market returns would broaden out beyond the technology driven leadership of 2023. By many measures, it doesn’t feel like it yet.

Fewer than a quarter of constituents within the US market outperformed over the 12 months to February 2024 (Fig.1). This is the lowest proportion in at least 30 years, trumping even the peak of the dot-com mania in 1999.

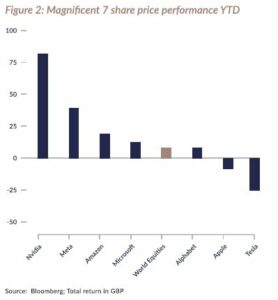

Artificial intelligence (AI) poster child Nvidia, a business largely unknown outside of the technology and investment industries, has nearly doubled in three months to become the world’s third largest company, behind only Microsoft and Apple. Its rapid ascent was responsible for almost a quarter of the near 10% rise in world equity markets. The $1.2 trillion gain in the company’s value this year is equal to around 40% of the entire UK stock market.

Last year a cadre of the world’s biggest technology companies produced stellar returns. However, outside of Nvidia and Meta, performance from the rest of the ‘Magnificent 7’ has been more mixed of late. Indeed, digging below the surface shows a different and more balanced picture.

For much of 2023 broader market progress was modest, despite strong returns from the tech behemoths which were recovering from an awful 2022. Rolling pandemic aftershocks continued to hamper specific industries, especially those that had benefited from customers stockpiling products during the supply-chain disruption of 2021-22.

Although consumers remained resilient, rising interest rates crimped spending with budgets reallocated to leisure and travel ahead of clothes, electronics and patio furniture. Consumer brands like Pepsi and Nike had flexed their pricing muscles in response to rising input costs over prior years leaving their products meaningfully more expensive. Limited growth in sales volumes last year suggested that consumers had noticed.

High property prices and rocketing mortgage rates also ground US housing transactions to a halt. With housing turnover down almost 40% on prior years, a host of subindustries that serve the residential property market found the going tough through much of last year.

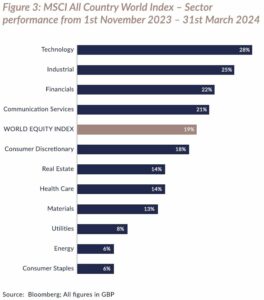

Given this backdrop it was perhaps unsurprising that the equal-weighted world index, a proxy for the average company’s share price performance, entered November 2023 below where it had started the year.

Fast-forward five months and world equities sit almost 20% above those levels in sterling terms, with this advance supported by a growing list of companies across a widening set of industries (Fig. 3).

What changed and how long will it last?

O recession, where art thou?

Late last year a more sustainable rate of growth and declining inflation allowed the Federal Reserve to signal that we have likely seen the end of interest rates increases for this cycle.

This home-run combination of cooling inflation and peaking rates without a recession triggered a broad rally across asset classes. Within the equity market, areas sensitive to interest rates and the economy enjoyed a long-awaited return to favour, ending a lacklustre year on a positive note.

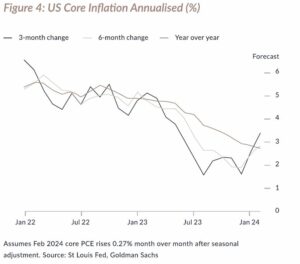

Much of this narrative still stands. However, continued strength in the US jobs market has tempered more enthusiastic views on the likely timing and speed of interest rate reductions. Inflation, while a far cry from the near double-digit levels it touched in 2022, remains too high for comfort and the pace of progress back to central bank targets appears to be stalling, if only temporarily (Fig. 4).

This has meant the ‘higher-for-longer’ camp – those who think interest rates will remain elevated for some time – are again out in full force, evoking memories of a bruising 2022 for investment returns. Beleaguered bond investors have endured another fallow period as anticipated interest rates cuts have been pushed out. However, unlike in 2022, equity markets have continued a steady march upwards.

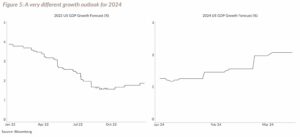

This is because higher interest rates due to a strong economy is an altogether different proposition to higher interest rates due to surging commodity prices and tangled supply chains. Simply put, today’s interest rate expectations are mainly being driven by better-than-expected growth rather than spiralling inflation. This is a much healthier environment for corporate profits (Fig 5) and by extension equities.

Thanks to the resilience of the consumer the US has weathered significant downturns in both the manufacturing economy and housing market. Economic growth adjusted for inflation is currently growing at a steady 2% rate, in line with the economy’s long-run growth potential. With manufacturing and housing likely to improve through the year, there is justifiable optimism that growth could even accelerate rather than just stay on trend.

Stronger-for-longer

As already mentioned, many manufacturing-focused industries have struggled over the past 18 months in response to a shift in consumer spending from goods to services as the world normalised post lockdowns.

Slowing end market demand for the likes of industrial semiconductors and life sciences tools has been exacerbated by a gradual work down inventories built up in response to pandemic-disrupted supply and the surge in demand for vaccine synthesis and manufacturing.

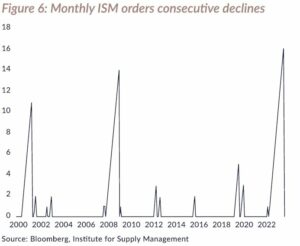

Whilst not as severe a drop as experienced in the Global Financial Crisis, activity in the manufacturing sector has contracted for 16 consecutive months. This streak of declining monthly order activity has been longer than any slump in the last 25 years (Fig. 6).

The good news is that the industrial downturn is nearly over. Demand is showing signs of modest improvement, new orders have finally started to pick up and inventory destocking headwinds are waning. A welcome manufacturing revival looks to be ahead.

The likes of life science champions Thermo Fisher and Danaher, US freight rail leader Union Pacific and industrial semiconductor giant Texas Instruments all stand to benefit from a return of longer-term growth trends as supply chain indigestion clears.

The housing market has been equally hard hit, with the rapid rise in mortgage rates having a predictable effect on transactions and renovation activity. Existing home sales in the US were at almost 30-year lows in 2023 as homeowners had little interest in giving up their attractive fixed rate mortgages (Fig. 7).

Much like the manufacturing recession, residential economic activity appears to have started to bottom out. The number of US housing units that have started construction has now grown year-over-year for three months in a row, after having fallen for 16 of the previous 18 months, and existing home sales have shown signs of green shoots.

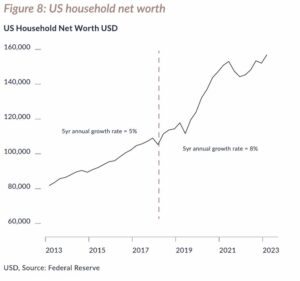

Housing market activity is influenced not only by the absolute level of mortgage rates but also the most recent change. Despite the interest rate increases of the past two years, real wage gains and the structure of borrowing has meant that consumers remain in robust financial shape relative to long-term history. US consumers have also grown much wealthier. Despite the pandemic, household net worth has increased by 8% p.a. over the past five years as wages, house prices and the US equity market have all moved higher. This is a significant step up in the rate of growth seen in the previous five-year period (see Fig 8).

In the past three months, average 30-year mortgage rates in the US have fallen from 8% to 7%. Importantly, this has happened without any rate cuts, driven instead by reduced uncertainty over the future path of monetary policy. With inflation moderating and the Federal Reserve expected to begin lowering rates, a continuation of the recent declines in mortgage rates is likely to lead to a strong rebound in demand through 2024.

Although housing’s direct contribution to GDP is a relatively modest 5%, its impact on consumer sentiment, job mobility and discretionary income means it has significant effects across the broader economy. A housing recovery would be a significant tailwind in 2024.

An increased pace of construction and remodelling bodes well for the near-term fortunes of US pool equipment distributor Pool Corp. The associated lift to consumer sentiment, affordability and loan volumes should boost JPM’s traditional banking activities and consumer credit bureaus like Experian.

Building for the future

Alongside the improving short-term outlook for more economically sensitive manufacturing and housing markets, the medium-term trends for longer-cycle industrial and infrastructure activity remain compelling.

We wrote a year ago about the return of ‘strategic industrial policy’ from governments across the world and its potential to spur an industrial renaissance.

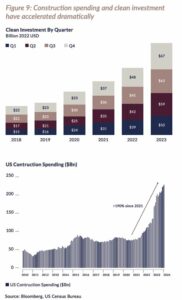

Although not alone, the US is at the forefront of this. The Biden Administration has passed three major spending bills promising $2 trillion of grants and subsidies to improve economic competitiveness, innovation and industrial productivity, all while dramatically reducing the country’s environmental footprint. The money is now starting to flow (Fig. 9).

Two years on from the passing of the Infrastructure Investment and Jobs Act (IIJA), implementation is hitting its stride. Over $300bn has been distributed into state coffers and direct investment projects while competitive grant-making is increasing steadily. Importantly, there has been little political bias in splitting awards across states which should help protect the IIJA’s future should Donald Trump return to the White House later this year.

Incentives focused on the semiconductor industry (the CHIPS Act) have encouraged the likes of Intel, Samsung, Micron, TSMC and Texas Instruments to break ground on new US-based manufacturing lines. Intel alone will receive $8.5bn in direct funding and $11bn in loans from the US government to expand its capacity to make high-end chips. With so much leading-edge manufacturing currently concentrated in Asia the strategic rationale has strong bipartisan support.

The Inflation Reduction Act (IRA) has catalysed significant investment into green energy solutions. $230bn poured into US deployment of everything from battery factories to wind farms in 2023, up 38% from 2022. Investment in the electric vehicle (EV) supply chain hit $42bn, more than double the previous year. Meanwhile, retail spending on things like EVs, heat pumps and rooftop solar panels topped $100bn. Federal investments are already exceeding the Administration’s own estimates and, barring Republican repeal, the Massachusetts Institute of Technology predicts the government is on track to spend as much as $1 trillion on the clean economy across the life of the IRA.

We recently met with the management of equipment rental leader Ashtead. The company offers its customers a one-stop shop for all their rental requirements, with one of the industry’s deepest and broadest ranges of equipment from earthmovers to aerial platforms (Fig. 10).

Encouragingly for Ashtead, many of the new and planned infrastructure projects are large, such as data centres, bridges and factories. Ashtead has identified around 500 of these mega projects ranging from $400m to $12bn in size that have either started or are soon to begin. Projects of this scale require suppliers with the expertise and breadth of product to meet the needs of the customer so lend themselves to larger industry players. Ashtead’s share of mega projects already underway is around 30%, more than twice their existing share of the total rental market. The roll out of infrastructure projects backed by government dollars should provide a runway of profitable and predictable growth for companies such as Ashtead over the decade ahead.

Specialty chemical business Sika is another that should benefit. The company has a globally leading position in products for bonding, sealing, reinforcing, and protection in the building sector and automotive industry.

Sika products tend to be relatively low cost but high value, such as cement admixtures used to decarbonise building materials or tile adhesives that double as waterproof sealant, meaning decorators can complete a job in a single visit.

Buildings and infrastructure are responsible for 40% of global carbon emissions, of which half is generated during the construction phase. The buildings industry has been increasingly looking to Sika’s innovative solutions in response, with this dynamic now amplified by tax incentives for investment in buildings with higher energy efficiency.

Sika recently increased their long-term growth targets, reflecting their leading position within a construction chemicals industry that is set to grow at a faster pace in the years ahead.

Artificial intelligence – from enablers to beneficiaries

A broadening market still leaves room for technology and artificial intelligence remains the dominant market narrative today.

We are firmly in the arms-race stage of AI rollout. While Nvidia and its high-performance chips has been the most high-profile to date, enablers throughout the semiconductor supply chain and large technology infrastructure providers will continue to benefit from the early build out.

The real-world value of AI is yet to come. Initially this will be cost savings and productivity enhancements for nontechnology companies. This suggests material near-term opportunity for companies with large customer support teams and, a year on from the initial ChatGPT hype, early use cases are emerging.

Klarna, a Swedish financial technology company, recently released statistics showing its AI chatbot does the work of 700 customer service agents. The AI assistant is on par with human agents in terms of customer satisfaction, makes fewer errors and resolves customer enquiries in less than 2 minutes as compared to 11 minutes with a typical agent. The cost savings are material: Klarna estimates a $40m uplift to full year profits as a result.

But the real promise of AI is what may be achievable once the likes of JP Morgan, UnitedHealth or Visa put their own data on top of the foundational AI models being built. The healthcare industry will use AI to develop new drugs quicker, better predict cancer or improve the use of preventative therapies. Retailers will be able to anticipate changes in demand more easily, banks improve loan underwriting and insurers more accurately forecast

weather catastrophes.

The uniting feature, both for enablers and beneficiaries, increasingly appears to be scale. An AI start-up aiming to build its own large language model cannot compete with the capital investment of the likes of Microsoft, Alphabet and Amazon, let alone get access to the necessary volume of Nvidia’s chips. Likewise, any model is only as good as its inputs: the largest proprietary data sets win.

The long-term case for a more balanced approach

A resilient global economy with a more balanced split between the consumer, industrial and manufacturing economies should provide a broader set of opportunities and with it greater diversification. Our portfolios are well positioned with investments across a mix of industries that should enjoy the improving near- and medium-term dynamics.

The longer-term strategic considerations that support a broader set of portfolio exposures are arguably even stronger, both within the companies and other asset classes we own. Even if central banks achieve their aims – namely taming inflation and reducing restrictive levels of interest rates before something breaks – there has been a fundamental change to the economy relative to the prepandemic decade.

Governments across the world have shifted to prioritise economic resilience over optimisation. Strategic industrial policy has returned with trade increasingly flowing along political rather than economic lines. Massive public and private investment to support decarbonisation, shorten supply chains and secure technology leadership will drive a decade of materially higher capital investment.

This has the potential to power the growth prospects of battle-hardened companies across the industrial, energy and mining sectors that have endured a long period of muted demand.

Productivity should improve too with companies forced to work existing resources harder and invest in efficiency enhancing tools such as automation and AI rather than relying on cheap borrowing and low wages. Technology companies, spanning software, semiconductors and data analytics should benefit.

Increased government spending, productivity-enhancing corporate investment and higher wages should lead to faster economic growth than we have become used to over the past decade.

Whilst growth may be higher, it may be more fragile too. Supply shocks are likely to become more frequent, driven by geopolitical flare ups, supply chain reorganisations and both the physical effects of climate change and the impact of the transition to cleaner energy sources. This will create additional volatility in inflation, and by extension, a return to more dynamic interest cycles and greater swings in the pace of GDP growth.

If the ‘new normal’ is marked by higher, but also more volatile, growth, inflation and interest rates, then we should expect shorter economic cycles and more rapid shifts in stock market leadership than the pre-pandemic decade. This is not necessarily a ‘bad’ environment for investing but will necessitate a portfolio with breadth beyond the narrow technology leadership and AI theme of the last twelve months.

With a greater range of opportunities for growth, a more diversified approach should also shield portfolios against shifts in momentum, market leadership and economic direction. We have already had a flavour of this in the years since the pandemic.

Article written by Daniel Zegleman, Portfolio Manager

For illustrative purposes only and should not be construed or relied upon as advice.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.