ANTICIPATING RECESSION: WILE E COYOTE OR WAITING FOR GODOT?

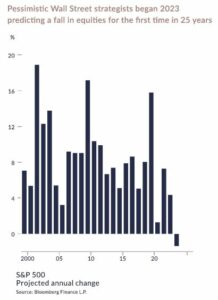

Following a year to forget, investors and economists entered 2023 in near unanimous agreement that a recession was imminent. Even famously optimistic Wall Street strategists sounded a rare warning, predicting that the S&P 500 would end the year below where it started. High profile banking failures including First Republic in the US and Credit Suisse in Europe only served to confirm expectations that the most aggressive interest rate cycle since the early 1980s would ultimately break the economy.

Following a year to forget, investors and economists entered 2023 in near unanimous agreement that a recession was imminent. Even famously optimistic Wall Street strategists sounded a rare warning, predicting that the S&P 500 would end the year below where it started. High profile banking failures including First Republic in the US and Credit Suisse in Europe only served to confirm expectations that the most aggressive interest rate cycle since the early 1980s would ultimately break the economy.

Yet six months into 2023 the most anticipated recession in history has so far failed to materialise. The economy’s performance in the face of high inflation and rising interest rates has surprised many. Will economic gravity ultimately assert itself as it inevitably did on Wile E Coyote or, like Samuel Beckett’s Vladimir and Estragon, are investors busy waiting for a recessionary Godot that may never arrive?

The case for a benign disinflation; Goldilocks may not be a fairytale this time

Economic performance this year has belied the negative sentiment and souring leading indicators that have pointed to recessions. A quarter that began with a banking crisis ended with an upward revision to US growth for the first three months of the year.

In large part this has been down to the resilience of consumers and with them the service sectors that dominate most of the larger western economies. The US, where services represent more than 70% of the economy, GDP growth was 2% in the first quarter of the year and estimates point to that momentum continuing into the summer.

That the consumer has remained so healthy, particularly in the US, reflects a still robust employment market, the buffer provided by COVID savings and the relative strength of the housing market in the face of surging interest rates.

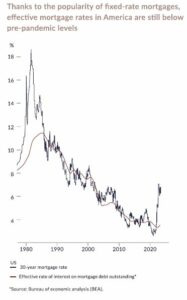

Whilst the US housing market has undoubtedly slowed, the leap in mortgage rates has failed to cause the type of financial distress associated with the last financial crisis. With most US homeowners on 30-year fixed rate mortgages, the move in interest rates has impacted new buyers rather than damaging the finances of existing owners. Most have not been hit by spiralling mortgage payments forcing them to compromise on spending or worse hand back the keys. It has been an orderly slowdown to date.

Plenty of cash in the Attic

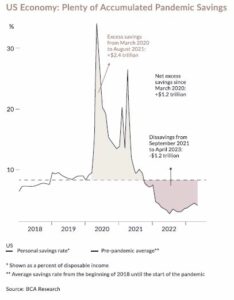

The US population is estimated to have accumulated additional savings of some $2.4 trillion during the pandemic through a combination of lower spending and government handouts. This has provided a cushion against the impact of higher prices which had been expected to weaken demand. Of that excess cash, over $1 trillion is still thought to be sitting in bank accounts.

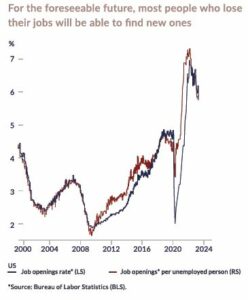

The employment picture shows few signs of fragility, even if we have seen some high-profile layoffs in the technology and financial sectors. Offsetting this has been the strength in the much larger hospitality and services industries where there remains a large gap between demand for labour and supply, with 1.6 job vacancies on offer for every unemployed person. Whilst below the post-pandemic peak, this is still well above the high of 1.2 reached in 2019 and readings of well below 1 associated with recessions. There is neither smoke nor fire coming from the labour market.

With core US inflation subsiding and employment near record levels, prospects for wage growth to overtake inflation look promising. After several years of falling real wages in the face of high inflation this would have clear positive ramifications for growth and reduces the chances of a major reversal in consumer spending over the months ahead.

The pictures in Europe and the UK have many of the same characteristics but look more insipid. Rather than COVID cheques, the dividend received came from moderating energy prices through a mild European winter. Unemployment rates are low, again reflecting the return of the hospitality and service sectors.

In the UK, while mortgages are fixed for shorter periods than the US, house prices and consumer spending have held up better than many expected. This reflects a housing market where 70% of homeowners do not have a mortgage and fixed rate deals that have been rolling off on a staggered basis to date. However, with UK core inflation sticky and expectations building that UK base rates may get to 6%, the outlook for housing and the wider domestic economy remains challenged. The US economy appears fundamentally stronger and more resilient to shocks than those in Europe.

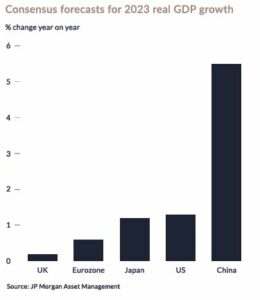

Expectations for growth have been improving, but less so in the UK and Europe

So, why the long face?

Given the strength of the service sector and upgrades to economic projections for this year, why do we retain a degree of caution about the future?

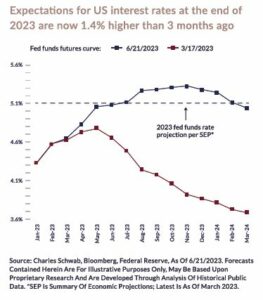

First these better economic conditions have emboldened policy setters to recalibrate ever higher their outlook for interest rates. Expectations for peak rates have moved steadily upwards in the UK, US and EU throughout the year.

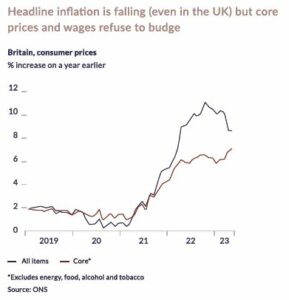

Whilst inflation has been falling, it remains well above target and core inflation is proving more stubborn than the headline numbers that include energy, food and other more variable measures. With employment still robust, central bankers face an easy choice to keep interest rates high until they see definitive signs of a moderation in pricing. Given the dynamics in the labour market this will probably require a rise in unemployment.

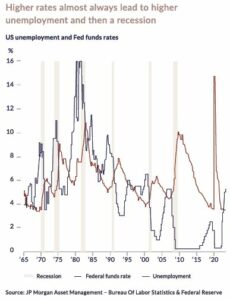

Better now = Worse Later

The longer that rates remain high, the greater the risk that they begin to hurt, particularly those with higher levels of leverage. This is both the purpose but also the problem with interest rates. They are designed to beat inflation by slowing demand and economic activity, by either making it more expensive to borrow or more attractive to hold cash rather than spend it. However, they are a blunt instrument and act with long and unpredictable lags – for instance New Zealand has just entered recession having started hiking its interest rates in October 2021, six months before the US. By the time central bankers see that interest rates are working it may be too late to stop demand overshooting on the downside bringing with it a recession.

The manufacturing sector, regularly a leading indicator for economies, is exhibiting none of the strength seen in the consumer space. Key measures, such as demand for new orders or building permits, are resolutely pointing towards more challenging times ahead. These measures have now suggested a contracting industrial sector for 8 months in a row. To date, manufacturers have been more reticent to cut their workforces than in previous cycles given the well reported difficulty in filling jobs post-pandemic but if the current trend continues then reality will eventually bite.

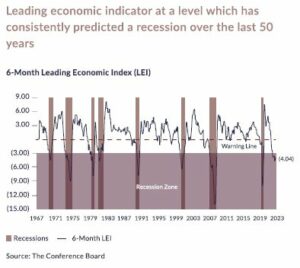

Alongside this manufacturing torpor, forward looking measures such as the inverted yield curve and the US Conference Board’s leading economic indicator continue to decisively augur a slowdown ahead. Both metrics have a near 100% record of predicting recessions over the last 60 years but with lead times of 4 to 16 months; the US yield curve inverted last October.

With the great hope of economic resurgence in China proving tepid at best, we believe it is right to give respect to precedents of the last 50 years and lean towards caution. After more than a decade of near zero borrowing costs it would be a surprise should the sharpest period of interest rate increases in four decades pass without further economic mishaps.

Our base case remains that higher interest rates and a fading of Covid-era policy stimulus will allow inflation to moderate but that the imprecise and delayed impact of policy will mean that by the time the fight against inflation is seen as being won it will be too late to avoid a recession, albeit probably a mild cyclical slowdown. We remain in the camp of recession deferred rather than recession avoided.

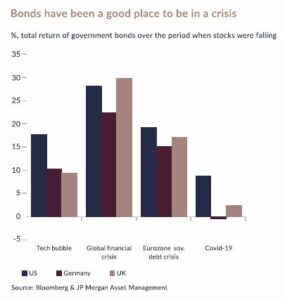

Bonds back in business

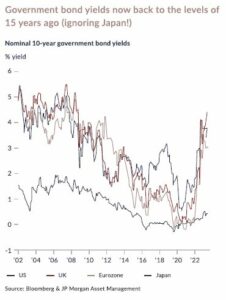

After the worst year in living memory for government bonds – one in which UK gilts lost nearly a quarter of their value and US treasuries 15% – the asset class now looks capable of delivering on its traditional dual mandate of generating a stable return whilst providing balance to equities in portfolios.

The starting point of government bond yields near 4%, whilst difficult to describe as exciting, is fair and a multiple of the levels of only two years ago. In addition, should an economic slowdown be accompanied by falling rates (as is our central view) then we would expect bond prices to move higher as investors seek security and yields fall.

In such a scenario we would expect corporate earnings and profitability to decline, providing a headwind to equity markets, leaving bonds as an effective diversifier. The yield on 10-year US government bonds need only to fall to 3% over the next year – not unlikely in a recessionary scenario – to deliver a 10% total return; the equivalent return for a 10-year Gilt would be nearly 15%.

Bonds offer balance to portfolios in anything other than a world of persistently high and unanchored inflation. We consider this a remote possibility, given the strength of central banks resolve and slowing leading indicators.

Equities – The Magnificent Seven Ride Again

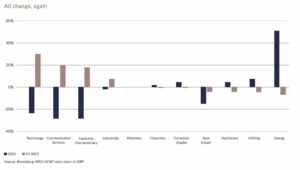

The rapid rotation of sector performance and investment styles has continued into a third year. The technology sector, 2022’s weakest performer, has led the way so far this year whilst energy and utilities have lagged.

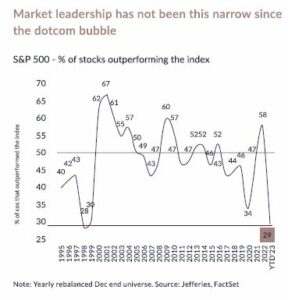

Building excitement around artificial intelligence (AI) has been the main market topic over the past few months. Those deemed to benefit – namely the largest US technology and semiconductor companies – are responsible for almost all the market’s gains this year so far. The largest seven technology companies (Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia and Tesla) were alone responsible for 80% of the return of the S&P 500 in the first half of this year.

Indeed, the breadth of the market has rarely been narrower, with fewer companies ahead of the market average than at any point since the dotcom bubble.

Corporate results and earnings expectations have been more circumspect outside this group, with disappointing updates from companies focused on the lower-income US consumer such as Dollar General and Target (neither of which are owned in client portfolios) suggesting that tighter policy may finally be having an impact.

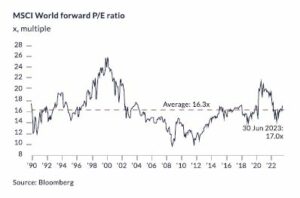

Market returns this year have been helped by a return of enthusiasm for share ownership and an improvement in the rock bottom investor sentiment rather than real growth in profits. Valuations have been getting richer rather than earnings getting better.

This has left markets priced modestly above the long-term averages but still noticeably cheaper than the recent peak.

Equities will need both a broadening out of support and an improvement in earnings to sustain the momentum from the first half. So far earnings expectations have been little changed this year with no growth expected, whilst forward expectations for 12% growth in corporate earnings for 2024 will require the better economic environment seen so far this year to be sustained into next.

AI everywhere all at once

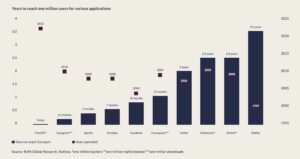

2023 will be remembered as the year that generative AI came of age. ChatGPT, an artificial intelligence chatbot, is one of the fastest growing apps ever, reaching a million users in a fraction of the time of today’s dominant applications such as Instagram, Facebook or Netflix. This has led to a surge in investor interest and the near trebling in the share price of Nvidia, a now $1tn semiconductor company, expected to be at the forefront of an explosion in demand for tools to power an AI revolution.

Microsoft too has been at the vanguard given its $10 billion investment in OpenAI, which took its stake in the company behind ChatGPT to 49%. Stock markets have history in rapidly extrapolating technological changes with the associated cries of new paradigms and revolutions in societal behaviour. Certainly, the initial movements in share prices may overestimate the near-term benefits and as with any potentially revolutionary technological innovation the expected winners of today may not prove to be the ultimate champions. Just ask investors in the tech “gorillas” of the dotcom era such as Cisco, Nokia and Ericsson.

AI has in fact been permeating our lives incrementally for years. Whether through the technology powering our phones and chatbots such as Alexa and Siri, autonomous driving features on our cars or the tools that enable retailers and advertisers to surprise, delight and annoy us through sophisticated targeting. It was as long ago as 2016 that AlphaGo, an AI programme developed by DeepMind (owned by Google parent Alphabet) beat a human professional at the Chinese game Go – a game considered several times more complex than chess, whilst IBM’s Deep Blue defeated Chess Grand Master Garry Kasparov in 1997!

ChatGPT has captured imaginations in a way that has garnered headlines and hyperbole in equal measure. It is the ease and range of tasks that these generative AI applications can perform that has ignited excitement from the analysis of data, writing of text, composition of music and creation of digital art. There is a renewed imperative for companies to grapple with the implications of generative AI on their businesses as well as wider economic and societal impacts. As ever there will be a balance of risks and opportunities, but at its simplest level AI does seem to offer the potential for meaningful increases in productivity. A report by McKinsey & Co. has projected that the productivity improvements associated with embedding generative AI in businesses could add between $2.6 trillion – $4.4 trillion of value each year to the world economy (equivalent to somewhere between one and one and a half times the annual output of the UK). Previous rounds of automation have largely been centred on augmenting efficiency in manufacturing but generative AI now provides the opportunity of applications across far broader markets.

Much as the internet and the smartphone created opportunities beyond the immediate technology so we see the potential for change across the entire economy with AI playing an important role in a vast array of industries. In healthcare, AI could support personalised medicine, drug development or smart devices and implants as well as squeezed efficiencies out of creaking health sectors faced with an aging population. In insurance, companies such as Aon can use AI to enhance risk analysis and claims processing. Owners and curators of data, such as Relx with its focus on legal, science and risk, will be able to apply AI to those data sets to provide new tools and products for their customers.

AI will also create problems. We will leave the existential threats to humanity firmly and safely in the hands of James Cameron, Elon Musk and Co. but there will be challenges around privacy, data security and intellectual property rights that will prove costs and threats to many businesses. Progress is rarely achieved without unintended consequences.

The potential applications of AI are undoubtedly exciting and stretch beyond panicked students struggling to reach essay (or investment letter) deadlines. As with any new advancement the perceived winners of today may not prove the ultimate beneficiaries. This may well prove to be those businesses who successfully harness the technology rather than the hardware providers or original thinkers at the vanguard of the shift.

Less certainty but more Options

The much-anticipated economic slowdown has not materialised even in the face of interest rates that have risen higher than expected and inflation that has not moderated as quickly as hoped. That is due to a services sector that has benefited from consumers that have carried on regardless in the face of rising prices.

Something will give. We believe the most likely outcome is that it will be the consumer and jobs before the central banks are sufficiently emboldened by weakening core inflation to take their foot off the brakes.

The risks to this scenario are balanced. Inflation may come down quickly enough to allow interest rates to pause before the economy decisively slows. Alternatively, rates may stay too high for too long leading to a deeper contraction. In any of these scenarios we think that bonds now offer a reasonable each way bet for the first time in many years.

Outside of the technology behemoths, equity markets look more fairly valued. Whilst a recession would not be good for earnings, it need not be disastrous given the absence of the structural imbalances seen in previous slowdowns such as 2008. We see plenty of interesting businesses where valuations have been getting more appealing. There are strong structural opportunities that will endure beyond current short-term cyclical concerns; many of these will be found in companies serving the industrial sector given our expectations of a revival in capital spending and the re-shoring of manufacturing. We have already seen a doubling of construction spending on manufacturing this year and a surge in commitments to build battery infrastructure; the Inflation Reduction Act is already having an impact.

Whilst the leadership of market returns this year has been concentrated in a narrow group of familiar favourites, we see a far wider panorama of investment opportunities. In the longer term we will be able to build a more diversified portfolio, exposed to a wider range of drivers behind the evolving economic and market dynamics, without compromising on the principles of resilience and quality that remain the hallmarks of our approach.

Article written by James Beck

For illustrative purposes only and should not be construed or relied upon as advice.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.