PREPARING TO LAND?

Entering 2024, expectations were for an acceleration in corporate earnings, falling inflation and significant cuts in interest rates – 7 cuts being forecast from the US Federal Reserve alone.

As we wrote in January, running into an Olympic year, the last mile on inflation would be the hardest. For interest rates to fall as far as hoped either inflation or the economy would have to collapse – neither have. As a result, rates have barely shifted even as interest rate reductions have been pushed further into the future.

The positive US economic momentum has continued, with last year’s laggards of the UK and Europe finding a second wind after their brushes with recession. Inflation has proven harder to shake given the strength of the labour market, but this has not delayed the anticipated improvement in corporate earnings and broadening out of business confidence beyond last year’s single story of Artificial Intelligence.

Stable rates, solid economics and improving company earnings have provided the foundation for markets to track higher. This has been achieved with unusual calm given the maelstrom of recent years. Investor consensus has consolidated around a benign outlook and glidepath to a soft, almost perfect, landing.

As we enter the second half of the year the fundamentals still underpin further progress. However, the next six months represent “decision time”. Central banks will face a decision as to when and by how much to ease interest rates whilst the political pendulum looks set to shift with the UK and France having voted for change at the ballot box, while the big one, the US Presidential election looms large for markets in November.

Battle-hardened against complacency, facing the upcoming circus of the US Presidential election and with signs of fatigue in the powerhouse US consumer, we expect the smooth approach seen so far this year to be subjected to increased turbulence even if the final touchdown ultimately proves as gentle as consensus currently expects.

Our view in short

- Market expectations for 7 interest rate cuts this year were always optimistic as has proven the case. Stickier inflation has kept central banks on hold. With employment and growth resilient they have prioritised pushing inflation decisively lower towards their 2% target.

- By the end of the year, the US and UK are likely to cut rates by 0.25%-0.5%, in line with the economy and what central banks are saying. Europe’s lower inflation has allowed the ECB to begin cutting although President Christine Lagarde has made clear that they will take their

- Improving economic performance has been mirrored in rising company earnings and a broadening out of earnings growth beyond the technology sector. Data provider FactSet estimates that MSCI World earnings will grow by 11.5% in 2024.

- Diminishing expectations for interest rates proved a modest headwind for bonds which fell modestly and remain slightly underwater this year.

- Despite improving earnings, equities largely paused for breath from April following a strong first three months of the year; 8 of the 11 equity market sectors were flat or down between April and the end of June but all bar real estate are positive for the year.

- The exception was those companies seen as benefitting from the building out of data centre infrastructure to support artificial intelligence. Microsoft, Amazon, Google and Meta announced cumulative annual investment plans of $200 billion to be spent on Al and related capital expenditure.

- Gold surpassed $2,400 for the first time, buoyed by continued buying by Central Banks, led by China.

- Headline equity market valuations look stretched, but this reflects bubbly conditions in Al where momentum and prices have surged ahead of fundamentals. Valuations outside of this narrow group look more attractive and are supported by earnings that are accelerating rather than slowing.

- The US remains the force in markets. This has been justified by the corporate, economic and sector strength in the US. These advantages should persist but improvements in other regions may reveal opportunities at attractive prices.

- The role of bonds in portfolios is to provide reliable income and protection in the event of a recession. With yields over 4% they can now fulfil both criteria.

- Politics has played a peripheral role in markets so far. However, the US election should raise the stakes. With deficits elevated, trust in the US reduced and the seemingly likely return of Donald J Trump to the White House the potential for Treasury and currency market volatility is rising.

- Gold provides an alternative safe haven to US Treasury bonds. Central banks have recognised this and have been buying. If investors join in prices could head higher.

- There are certain structural certainties that will transcend the short-term anxiety and uncertainty about economic and political cycles. Demographics, technological innovation and climate change provide companies and investors with opportunities for growth irrespective of where the world takes us over the next 12 months.

2024 SO FAR SO GOOD- ‘GOLDILOCKS LIGHT’

Market expectations heading into 2024 were a little too grounded in a rose-tinted view of the future. Bond and equity investors heard what they wanted to hear from central banks and underplayed what was being said. As we commented at the time, circular expectations of robust growth, accelerating corporate earnings, falling inflation and slashed interest rates were going to prove almost impossible to square. For interest rates to fall sharply either inflation needed to continue sinking like a stone or growth would have to collapse taking company earnings with it.

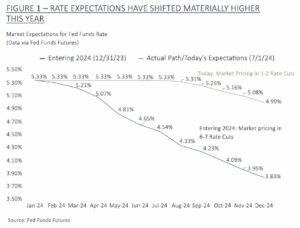

Neither proved to be the case. Forecasts of March interest rate cuts were torn up and expectations for 6-7 rate cuts adjusted to the far more reasonable 1-2 cuts anticipated today (Figure 1).

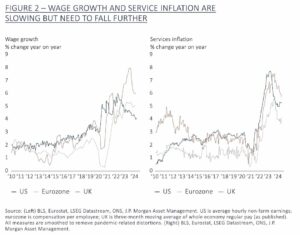

The final furlongs of the race to subdue inflation were inevitably going to prove a challenge, especially whilst wage growth and services demand continued at high levels. Our view is that inflation driven by strong demand is far more acceptable than that caused by problems with supply.

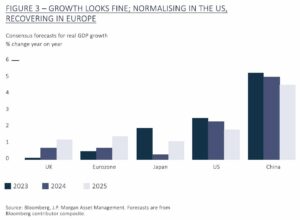

The jobs market has been well behaved although unemployment rates have ticked up a little recently. For now, this looks like normalisation after a period of extraordinarily tight labour markets and should mean costs continue to fall. Higher interest rates and inflation have failed to disrupt economic progress. US growth for this year has been steadily upgraded. UK and European growth should continue to recover over the course of the year whilst the US looks well supported even if the rate of growth slows. (Figure 3).

Europe has fired the starting gun on interest rates. The Swiss, Swedish and the European central banks all cut interest rates last quarter. The most recent UK inflation data showed a decisive move lower. The Bank of England’s trigger finger will be getting pretty itchy and a cut by the autumn looks likely.

CONTINUING THE DESCENT, THE APPROACH LOOKS GOOD BUT WE HAVEN’T TOUCHED DOWN YET.

Our central view remains that we are moving back to a period of trend growth, involving deceleration in the US and recovery in Europe. As labour markets cool, wage and service inflation should continue to fall allowing central banks to ease interest rates, normalising policy. Rates and inflation will not return to the near zero levels for structural reasons we have elaborated on previously. But a landscape of slightly higher interest rates and inflation should be supportive for growth even if they bring with them slightly more volatile cycles.

We see two risks to this smooth approach:

- stickier inflation that forces central bankers to delay rate cuts further or worse resume hiking again.

- a faster slowdown which gathers sufficient momentum to overshoot the runway and prompt a recession.

For now, the signs are good. Global inflation is falling, manufacturing activity is expanding again after nearly two years in recession whilst services remain positive but not as red hot as a year ago. This is feeding through into hopes for higher corporate earnings.

The return to growth in manufacturing should help those economies with an export focus, principally Europe, Asia and Emerging Markets. Falling energy prices should support consumer spending particularly with wages still growing at a clip.

US data has been choppier, with signs that the economy may be slowing. The labour market is cooling but from an extraordinarily strong level, which is part of the Fed’s plan to rein in inflation. The strength of fiscal support is dwindling, the number of job openings is heading back towards its long-term average and higher rates are biting on unsecured borrowers. Credit card and auto-loan defaults are picking up in the US, nearing 2010 levels. This is a challenge for the lower income parts of society and may be responsible for the disappointing updates from the likes of McDonalds, Starbucks and Walgreen Boots. Given the importance of the US consumer we are watching this closely.

The concern is that interest rates are not a precision weapon and so by the time that the authorities are confident that the jobs market is slowing it will be too late to stop the negative momentum from taking the economy into recession.

A reacceleration in inflation looks less likely today, although its impact would be worse both economically and for investment markets than a recession. Having had a taste of such a stagflationary environment in 2022, a second round so soon could embed the experience in people’s minds leading to a change in future expectations and behaviour.

The economic picture today supports our cautious optimism. However, the range of very different economic scenarios that could quickly unfold underpins our diversified portfolio by asset class, sector, and geography invested through high quality assets underpinned by strong fundamentals. There is no point in putting insurance in place after the event.

EQUITIES – ARTIFICIAL INTELLIGENCE IS IMPORTANT, BUT IT ISN’T THE ENTIRE ECONOMY (YET?)

We all look forward to not writing about Artificial Intelligence at some point, or at least to the day when we can get Chat GPT to do all the work for us without the need for forensic fact checking!

Performance from January through March validated our view of broadening opportunities beyond Artificial Intelligence (Al), a fact confirmed by company earnings announcements during the reporting season in April and May. Corporate earnings and management outlook forecasts pointed to positive momentum beyond the previous market leadership and the dominant United States. Analysts have raised their growth expectations for earnings across the board including the previously lagging regions of Europe, Asia and Japan.

At a sector level the story also seemed to be moving beyond technology. Industrials, financials, and utilities performed well as economic performance brightened and manufacturing activity recovered.

But the market has struggled to move on from its 2023 obsession and in an echo of the second quarter of last year, returns since March have returned to a narrow focus on the anticipated beneficiaries of Al. Eight of the eleven major market sectors were flat or down over the quarter even as earnings were upgraded across the board.

This second wind of Al excitement has been fueled by the capital expenditure plans of the mega-tech companies announced in late April. Collectively Apple, Amazon, Google and Meta may spend as much as $200 billion per annum over the next four years on capital projects much of which may support Al – a commitment the size of most government fiscal programmes.

Enthusiasm was centred in those companies most directly exposed to the capital spending tsunami needed to build out the infrastructure crucial to support artificial intelligence models. So far this has translated as chips, data centres and power. Analysis by Bernstein estimate that planned data centre construction in the US will require an additional 17 gigawatts of power: the equivalent of another three New Yorks! The momentum behind these powerful trends has proven a powerful and self-perpetuating force focused on ever fewer companies. This is not the first time we have seen this.

The concentration of the top 10% of stocks in the S&P 500 has been in this range twice before – 1929 and 1999. Once concentration gets this extreme, it tends to give way to periods where taking a more balanced approach will yield excellent returns both in an absolute sense and relative to an index. It’s worth highlighting that all of the technological innovations popularised during previous periods of excitement – automobiles, aviation, radio, and the internet – did indeed change the world and dramatically increased productivity and improved lives. Al may do the same. Yet all the related thematic stocks where valuations had ballooned still came crashing down. In the case of the dot-com crash, no catalyst was required. Asset prices simply rolled over due to exhaustion.

We have seen a number of these secular themes come and go over the decades of our experience. Markets being dominated by the new thing is not a new development and is usually grounded in fundamentals and real spending. However, the current level of intensity has begun to feel extreme with momentum stocks leading the way to an extent not seen since the dot-com bubble (Figure 4).

We do not underestimate the potential for this new technology and are invested in many companies that will benefit. Synopsys provides the design software that allows semi-conductor developers from Nvidia to Samsung to develop ever more powerful and sophisticated chips. Microsoft, Google and Amazon host the cloud servers where the Al models and data resource will live. Amphenol manufactures the connectors and sensors that sit as vital components in the physical infrastructure of data centres and in linking real world information to digital analysis. Owners of robust, reliable, specialist data sets such as Relx and Wolters Kluwers have the informational feedstock without which Al cannot create valuable use cases for business. They have real and growing profits.

However, in such periods of high enthusiasm a cool assessment of valuation becomes essential to making sure that you are not overpaying for potential and storing up trouble. What price are you willing to pay for these companies today? Nvidia trades on 40 times sales (as Cisco did in 2000), leaving little or no room for disappointing lofty expectations. Even great companies can prove average investments if you pay too much for them – again, see Cisco!

The leadership of the magnificent 7 technology companies last year was entirely justified by the strength of their growth, they were growing their net income by 50% or more last year at a time when the rest of the market was moribund. They continue to grow quickly, but not as fast as they have done. Their rate of growth is slowing just as the other 493 companies in the S&P 500 are accelerating. In the second half of the year they are forecast to be growing nearly as fast, FactSet forecasts earnings growth of 11.5% for the market in 2024. With the 493 trading at a much cheaper valuation for similar growth we see plenty of potential for catch up.

US EXCEPTIONALISM – A STORY OF MORE EXCEPTIONAL GROWTH BUT NOW PRICED ACCORDINGLY.

If Al returned as the leading sector narrative, so inevitably did the US as the dominant region. The US now accounts for 64% of global equity markets, whereas the US accounts for 26% of global GDP. However, we would follow the earnings.

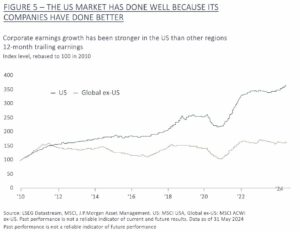

US leadership is not a new phenomenon. Economic and market factors have been working in the US’s favour since the financial crisis. Since 2008 Japan has battled deflation, Europe has grappled with political crises, sovereign debt crises and an obsession with austerity whilst China has created a number of growth shocks and is in the midst of a slow-motion property crash. In contrast the US has enjoyed a long and stable expansion, punctuated by bursts of fiscal support such as the Trump tax cuts of 2017 or Biden’s infrastructure spending. US companies have outstripped their global competitors thanks to greater investment, faster expansion in their margins and stronger revenue growth. Add to this a sector composition that favours the growth sectors that have led the way since 2010 and this “US exceptionalism” is well justified. Just look at the earnings growth of the US vs the rest of the world (Figure 5).

Whilst the strength in the US and some of the US’ leading sectors has been thoroughly justified, recently that success has been based on stocks getting more expensive rather than earnings growing more quickly. The valuation of the US market now stands at more than 21x the next 12 months’ earnings, as compared to an average of 16x over the last 20 years. This falls to a more manageable 18x if you remove the 10 largest companies, which trade on a toppy 28x.

Whilst valuations may ultimately be justified by a higher level of growth and the US retains many outstanding companies and many of the advantages that have driven its market hegemony, the margin of safety for investors has shrunk just as the relative attractions of a broader collection of regions and sectors has risen, particularly given their improving fundamentals. With the rest of the world looking, many more attractively valued opportunities may arise beyond the continental US, but only where we can find the quality.

BONDS-TIME TO GO BACK TO BASICS

After their annus horribilis in 2022 when they were knocked to the floor by inflation, bonds have struggled to climb off the canvas.

The transition from the low rates, low inflation regime that held following the deflationary bust of the financial crisis has been painful. But starting from today the prospects for bonds look fine. In a multi asset portfolio where equities are expected to deliver the growth, bonds serve two roles: they provide a reliable income stream and they provide diversification in the event of a growth shock. Bonds should be capable of delivering on both parts of that bargain.

The yields on US and UK 10-year government bonds are back to the levels of 2004, the year the band The Killers released the anthemic Mr Brightside. Unlike bonds, The Killers are more popular today than they were 20 years ago, but destiny may be calling again for fixed income. Current yields of 4%-4.5% look quite reasonable especially should interest rates begin to fall modestly. They will look outright attractive in the event that the world slows faster or worse lapses into recession.

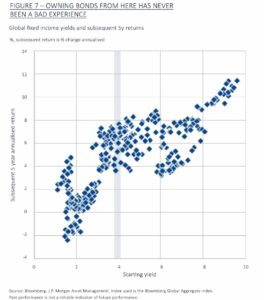

Even if we remain in a higher for longer environment for rates and inflation, bond yields are in excess of current and expected future inflation and so provide a real return. History is also on bonds’ side. Buyers of bonds at current levels have historically always received a positive outcome over the subsequent five years with an average annualised return above 6% coupons (Figure 7).

Bonds will provide a solid return in our central scenario of a soft landing and will do well if the slowdown spills over into a recession. However, as we have seen recently, unanchored inflation is kryptonite for longer-dated bonds and those risks whilst doused, are not extinguished. Politics has the potential to cause mischief.

RETURN OF THE TARIFF MAN – CARS, CHIPS, COGNAC AND A THREAT TO EXORBITANT PRIVILEGE?

Which brings us to the elephant in the room that is the US election. Given the chastening first Presidential debate and (current) speculation as to whether President Biden will even run, Donald Trump currently looks odds on to return to the White House.

This could have major implications for the US Treasury market and the dollar. Donald Trump is no fiscal conservative and has an unhealthy disrespect for the “establishment”. His policy objectives point to a further increase in the US debt burden. The world’s risk-free asset, US Treasuries could be vulnerable.

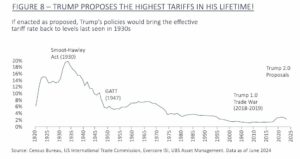

More pernicious for US Treasury yields are the former President’s tariff plans which include a blanket 10% on all imports and 60% on imports from China. With the Biden administration having already taken aim at Chinese solar and electric car imports there is cause to think these may gain wider support. This would take protectionism back to levels not seen since before the Second World War (Figure 8).

Trade tensions are also heightened between Europe and China, currently being played out in a proxy war of cars and cognac. This creates a wider potential for tit-for-tat tariffs to add to price and inflationary pressures limiting central banks ability to reduce interest rates and raising yields on longer maturity bonds as investors and consumer expectations on inflation adjust higher. Not helpful for economies, companies, or markets.

Former French Prime Minister Valerie Giscard d’Estaing described the US as having an “exorbitant privilege” conferred on it by the dollar being the world’s reserve currency. That privilege provides the US with an advantage that allows it to run higher deficits at lower cost than other nations and is an important tool of soft power. A Trump administration could see that privilege abused to breaking point. Add to that rumours that Trump would seek to undermine the independence of the Federal Reserve and the potential for upheaval in the US Treasury and dollar is not a zero risk. This would cause ructions across global markets.

Whilst these risks may prove overblown, the very existence of such previously unimaginable risks reduces the attraction of longer dated US sovereign bonds as the default safe haven and counterpoint to more volatile equities – indeed in the last 18 months bonds have proven a more volatile asset class.

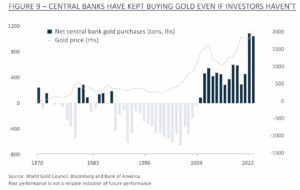

Gold increasingly looks like an alternative. Governments certainly think so, particularly those who fear being on the wrong side of the US, a risk that must also increase should ‘The Donald’ return. Data from the world gold council shows that central bank buying of gold has risen materially since the financial crisis and accelerated further following Russia’s invasion of Ukraine (Figure 9). The realisation that the US could weaponise the dollar by freezing or confiscating assets has led countries to look for other stores of assets. China has sold $102 billion of US treasuries reinvesting more than half into gold in the last year. 70% of global central banks expect to increase their gold holdings from today.

With investors having been net sellers of gold since the summer of 2022 any escalation in global tensions could see a rapid change in investor sentiment, further burnishing gold’s credentials as a safe harbour in a geopolitical storm. We see gold as a valuable part of portfolios and one that looks well supported even if fears prove unfounded.

LOOKING THROUGH UNCERTAINTY, THERE ARE A FEW THINGS THAT WE ARE CONFIDENT OF.

While the outlook for the world may be reasonable today, the risks of a shock that blows off course are ever present. The scope for monetary policy errors and election-related uncertainty cautions against going all in, whilst the frenzy around Al looks stretched in certain areas. Conflicts continue around the world, and we have seen how vulnerable supply chains are to the increasing number of disruptions from the natural world. The future is by its nature unpredictable.

However, in a fundamentally uncertain world, there are some big features of the global economy that are not really up for debate and can help us look through the noise and identify areas of structural opportunity that can weather the inevitable shocks and storms and emerge on the other side.

Demographics, technological advancement, and global economic growth represent trends that are structural in nature and present opportunities for those businesses and investors willing to look through the very short term.

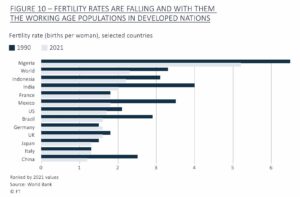

All the people who will be adults in twenty years have been born, everyone who will be over fifty in thirty years is an adult today. Fertility rates are dropping globally (Figure 10) whilst the developed world faces an ageing population. Japan and China’s populations are shrinking, whilst according to data from the European Commission the working age population in the EU shrank from 66.3% in 2013 to 63.6% in 2023. There are fewer workers to support an older population with ramifications for growth, social care and housing.

An ageing society will provide ongoing opportunities for the healthcare sector, not only in terms of demand for drugs and therapies but also for those capable of improving the cost efficiency of healthcare provision. Healthcare is one of our biggest exposures, whether through those aiding drug discovery and diagnosis (ThermoFisher), improving surgical efficiency and outcomes (Intuitive Surgical) or companies at the leading edge of treating chronic conditions such as diabetes and obesity (Novo Nordisk). Age demographics will drive different demand trends in different regions, the young and dynamic populations of India and Southeast Asia will have very different needs to the ageing citizens of the Mediterranean.

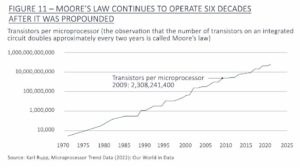

Technological advance is a feature of human ingenuity and development. Part of our belief in rational optimism (JH&P Quarterly, Q3 2022) is founded on humanity’s ability to harness technology to solve its biggest problems. The harnessing of the internet, smartphones and now artificial intelligence have all shown the capacity to advance productivity and create new paths for progress, innovation and new industries. That Gordon Moore’s eponymous law that the number of transistors in an integrated circuit doubles about every two years holds, nearly sixty years on, is testament to the power of technology and progress (Figure 11).

Technological advancements will continue to create new opportunities, as Moore’s Law looks ahead to a 7th decade chip designers (Synopsys) and manufacturers (Texas Instruments, ASML) will continue to push the boundaries of processing power. Al may become your office assistant and revolutionise white collar productivity, using Microsoft co-pilot whilst driverless cars no longer seem farfetched with Alphabet’s Waymo and Tesla potentially freeing time on our daily commutes and school runs to focus on work and leisure whilst releasing drivers to work elsewhere within the labour force, ameliorating demographic pressures. Technology may also provide solutions for potentially existential challenges such as climate change.

Then there is economic growth itself. According to work by the IMF, the world economy has grown every year since 1950 with the exception of 2009 and 2020, 97% of the time! The global economy has managed to absorb the seemingly economically existential crises of the GFC and COVID to reach new highs. Whilst growth may be slower today with very real challenges ahead, to bet against growth would be to go against the evidence of the last 70 years. We continue to see the potential for growth in many areas of the economy and within our clients’ portfolios.

One final thing we are confident of and which underpins our investment in companies is that wherever share prices move in the short-term driven by whatever exogenous event, shock or shift in sentiment, ultimately, they will track earnings. The highest quality companies with the best management teams will always find opportunities to drive growth in their earnings for the ultimate benefit of us, their shareholders. Our job is to identify enough of them to create sufficiently balanced portfolios to prove resilient enough that, when the going gets tough, we can just keep going.

Article written by James Beck, Head of Investments

For illustrative purposes only and should not be construed or relied upon as advice.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.