TARIFFS STILL ON THE MENU

WILL MARKETS STOMACH THEM OR ARE WE DUE ANOTHER BOUT OF INDIGESTION?

Even by the standards of recent years the past quarter has been a blockbuster. The headline act was the tariff saga that began with liberation day on 2nd April, which reached its zenith as Chinese reciprocity drove tit-for-tat tariffs above 100%, before Trump hit the pause button after a week of market chaos. Cue the fastest relief rally in the history of markets which saw the US recover all its falls in little more than 50 days.

Moving down the bill we had an Israel – Iran conflict, the US bombing of Iranian Nuclear facilities and the unedifying social media break-up of the Trump/Musk bromance. The end of the quarter brought a NATO summit in which members committed to increase defence spending to 5% GDP and a bumper US budgetary bill that will add more than $3 trillion to a US deficit that has already reached $37 trillion and is more than 120% of GDP.

Whilst the constant barrage of noise hit economic sentiment, it has so far failed to cause the stagflationary shock of higher inflation and falling growth that many predicted. While the outlook remains foggy, the levels of uncertainty are significantly lower than they were only a matter of weeks ago. We take nothing for granted given the US president’s mercurial approach to governing.

With the pause in tariffs expiring there is a sense of deja vu in the policy announcements on Truth Social (most in block capitals). But we are past peak tariffs and the ability to shock is much diminished. Markets have become dulled to the noise. With positive fiscal moves in the US and Germany good for growth, monetary policy easing slowly and oil prices low we find ourselves on surer footing even if we remain prepared for the rug to be pulled from under our feet.

WAS IT ALL A DREAM?

Just like Pamela Ewing, in the 80s hit show Dallas, waking to find that the entire previous series was a dream, so investors waking up on the 1st July could be forgiven for wondering if they had simply experienced a tariff nightmare.

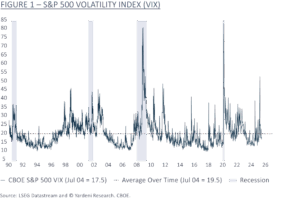

Equity and bond markets have recovered substantially all of the sharp losses suffered in the aftermath of the Liberation Day tariff announcements. With each announcement that de-escalated the extremes of policy and with each data point that showed that feared damage had not been wrought, so market measures of fear, such as the Vix volatility index, fell and risk seekers came back to the table.

After a Liberation Day surge, the VIX measure of market fear has quickly fallen back, drawing investors into markets:

However, even as share prices came off their lows, those companies with global supply chains or exposed to trade between the US and just about anyone else faced a period of havoc. Through quarterly reporting season in April many companies were left feeling in the dark as they adjusted forward projections for a range of scenarios or simply withdrew their guidance altogether. The flick flacking of policy is making it impossible to make any sensible short-term projections.

As the quarterly reporting cycle comes around again, we are about to get another real world update from the corporate sector. We shall see whether the last few months have allowed for a greater sense of clarity for management teams and whether they have taken any steps to reorientate their strategy for a changed environment. This will be a good opportunity to test whether businesses have been as willing to look through the maelstrom as markets have.

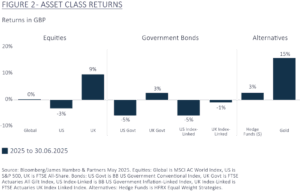

Markets have recovered their balance since April – but the echo of uncertainty can be seen in gold:

THE GREATEST SURPRISE SO FAR HAS BEEN THE TARIFF TANTRUM’S LIMITED IMPACT

Despite the initial fright caused by ”Liberation Day” and the associated collapse in business and consumer confidence, the actual economic impacts have been largely contained. In part that reflects the speed with which the US administration pivoted, moving swiftly to pause the reciprocal tariffs after only a week.

It also reflects a global economy that has stronger structural foundations than many give it credit for. It has defied repeated calls for recession in the last couple of years despite soaring inflation and interest rates and a wealth of geopolitical shocks. Much of this resilience can be traced to robust household and corporate balance sheets, repaired in the years since the financial crisis and insulated by refinancings undertaken in the shadow of COVID when interest rates were near zero.

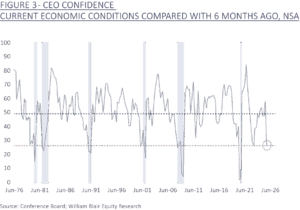

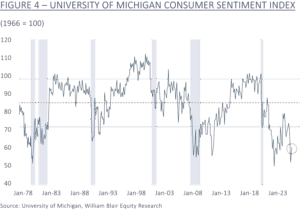

Having opened a trade war on every possible front, the US economy looked most vulnerable to a slowdown. The IMF was quick to assess the US as likely to see a bigger growth hit than any nation bar Mexico. CEO and Consumer Sentiment collapsed to levels associated with an imminent recession – something plenty of commentators expected.

US consumer and business confidence fell to recessionary levels:

However, despite the collapse in survey data we have seen few signs of weakness in the actual hard numbers.

Labour markets have been stable, with the unemployment rate falling most recently from 4.3% to 4.1%. Meanwhile retail sales and the services sector remain largely positive, pointing to resilience from the powerhouse US consumer. The manufacturing sector, after several false dawns, continues to flatline but this had been the case for two years. US growth looks to be slowing but it is not slumping. Live estimates put US GDP growth at near 3% in the second quarter.

Inflation too has remained largely in check. Whilst companies, notably Walmart, have highlighted that they will need to pass tariff costs through to customers, they haven’t done so yet. Barring a short spike following the air strikes on Iran, oil prices are low. With Brent at $68 there are few cost pressures at the pump. Inflation has remained below 3% and within sight of the Federal Reserve’s target.

Why so calm? We put this economic equanimity down to businesses adopting a ”wait and see” approach. With tariff day well flagged, many companies had pre-ordered inventory ahead of the announcement and so have been able to absorb the initial jolt as they await clarity on what the ultimate tariff landscape proved to be. It has worked so far but inventory will not last forever.

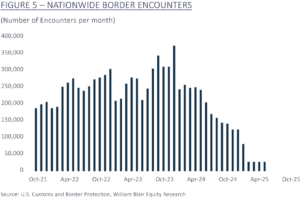

Similarly, having found it so hard to fill roles in the aftermath of COVID, companies appear to have held onto their existing workforce. With Trump’s immigration policies succeeding in their objectives, the steady stream of low-cost workers into the US that have supported its long-term growth has slowed to a trickle, keeping supply and demand closer to equilibrium. Researchers at the Brookings Institute forecast that immigration could turn negative in 2025, the first time in 50 years. This may have longer implications for the US labour market but for now it is helping keep the jobs market tight.

Trump has succeeded in crushing immigration:

IMPACT AVOIDED OR IMPACT DELAYED

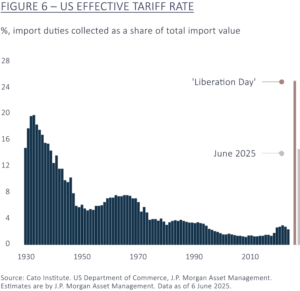

So far, not so bad but inventory stocks and stockpiled workforces are only a temporary fix. The tariff saga is not over, and it is unlikely that the impact will be totally contained.

Lower but not low!:

Recent weeks have seen win after win for the US President. The bunker busting bombing of strategic nuclear targets in Iran saw few reprisals and a rapid ceasefire. NATO’s members succumbed to his will, committing to increasing annual spending to 5% of GDP. The Supreme Court has slapped the wrists of lower courts which deigned to try and block his policies, whilst Congress swiftly and painlessly passed the One Big Beautiful Bill Act (OBBBA) in time for Independence Day. He even has the upper hand in his social media ”hot war” with frenemy Elon Musk, threatening to set DOGE on him just days before Tesla reported a 13% annual drop in sales.

On a hot streak, there is a danger that he overplays his hand on tariffs and pushes for rates closer to those outlined on his table of reciprocity. We know he needs the revenue, to offset the rising deficit. With the UK facing a 10% tariff at the low end and Vietnam mooted to face a 20% rate for goods and 40% for transshipments (stuff from China!), we may have established a base range. But don’t count on it, the EU and Japan look certain to be in the Tariff Man’s crosshairs.

Whatever the final level of tariffs they represent a substantial increase on what went before. Expectations are that tariffs will raise $250 billion in annual revenue, so far this year tariff revenues are $97.3 billion, a 110% increase on 2024. Businesses and consumers will in time adapt to higher taxes, but uncertainty undermines decisions on employment and investment. The stagflationary threat that has been avoided so far remains a clear and present danger.

FROM THE TARIFF MAN TO MR TOO LATE

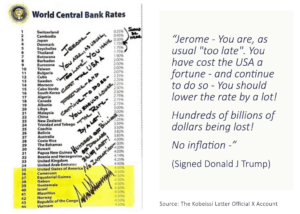

The resilience of the US economy has allowed the Federal Reserve to take a wait and see approach on lowering interest rates. Albeit under intense pressure from the White House, firmly and publicly aimed towards the Fed Chair Jerome Powell:

The central bank has been explicit that it wants to bide its time to see whether the tariff policies result in a rise in inflation. The resilience in the economy has allowed them to do so. Jay Powell has even poked the bear, stating that if it hadn’t been for the tariffs they would be reducing rates today.

If the personal animosity ratchets there is a risk that the independence of the Fed is undermined, either through an attempt to remove Powell or undermine him by the early appointment of a successor/shadow. This would certainly upset markets.

With the Fed resolute in doing its job, we do not expect any US rate cuts before September, with no more than one or two cuts this year. That is unless the economy truly begins to wobble. Central banks have shifted from pro-active to reactive mode.

Why does the White House care so much? As a property developer by birth, the president is conditioned to love cheap debt as the lifeblood of the dealmaker. Second, he sees cheap money providing as a further impetus to growth. Although, the housing market aside, current levels of interest rates have not been an impediment to US growth.

Most important is the impact on government debt. Spiralling interest costs are now the third largest outlay of the Federal Government, behind only social security and Medicare and are likely to exceed $1.2 trillion this year. With the ”One Big Beautiful Bill Act” increasing debt by over $3 trillion, future interest payments could be even higher. If interest payments consume more and more government receipts, then fiscal flexibility gets constrained, creating issues for Treasuries and government funding.

BOND VILLAINS

Higher rates, higher bond yields and bigger deficits means that the bond market no longer represents the dull, reliable, low return asset of the 2010s. With austerity out of the window, bond markets are now exerting influence not seen for decades.

It was the US bond market that decisively challenged Trump’s resolve in the early April. Bond prices slumped in response to tariffs. With government borrowing costs surging Trump blinked and was forced to step back from the brink. Bond markets stabilised. The yield on the US 10-year Treasury falling to 4.24% at the end of June and US government bonds positive over both the quarter and year to date.

Back in the UK, in early July we saw the Gilt market snarl. With the UK government forced to back track on plans to cut spending, an emotional appearance by Chancellor Reeves in the Commons led to speculation over the government’s commitment to fiscal responsibility alongside the Chancellor’s job security.

Bonds fell, as did sterling. A public show of support from the Prime Minister calmed the markets, averting a Liz Truss moment.

After a decade in which Central Banks judiciously managed the longer-term cost of borrowing, we are transitioning to one where swollen deficits and unpredictable government policies will have an increasing influence. This will bring greater volatility and uncertainty to what was previously a safe haven. The jolt felt by the market in 2022 as inflation surged and bonds collapsed was the point at which the bond bubble burst. Whilst not our base case, we could be in early innings of a multi-year bond bear market.

With deficits continuing to rise, and governments unable or unwilling to take hard decisions on spending we see few attractions in owning longer-dated bonds. Investors are offered little additional return for the latent risks from deficits and inflation.

As we noted in April, the capacity for long bonds to effectively provide balance and protection in portfolios is limited. During the worst of the April crisis, both long-dated bonds and the US dollar notably failed to fulfil their traditional safe haven roles. Something is changing.

THE DEATH OF THE DOLLAR BULL

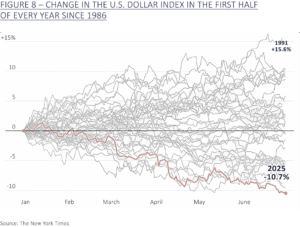

The US dollar has just had its worst six months in nearly 40 years, falling by more than 10% on a trade weighted basis. With US growth and interest rates still higher than many of its partners, more than half the fall has come since the US administration turned its focus to trade. It is clear that the dollar has become the financial canary for investor concerns about US policies.

After such a sharp fall it is likely that we are due for a period of consolidation. But further weakness is a risk. The dollar has been in a bull market since 2009 and on many measures still looks expensive as against other currencies. This is not a difficult thing to rationalise given the US’s many economic advantages.

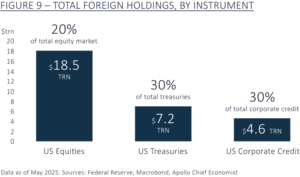

Yet foreign investors have been getting increasingly agitated. Rhetoric and proposed legislation has threatened foreign investors in US assets with new taxes on returns and remittances. We have yet to see much evidence of assets leaving the US but there has been plenty of talk. Foreigners own a meaningful proportion of US assets and if confidence in the sanctity of US assets deteriorates to the point that capital begins to flee the country then further dollar weakness will follow.

Non-US investors still own plenty of US and $ assets:

With the US representing 65% of global equity markets it is impractical and inadvisable to avoid the dollar altogether. The US retains manifest economic and investment attractions, and the dollar is unlikely to cede its role as the world’s reserve currency not least because of a lack of credible alternatives!

We have always looked to diversify portfolio exposures across a range of assets and currencies. The risks to the dollar represent another reason for us to do so.

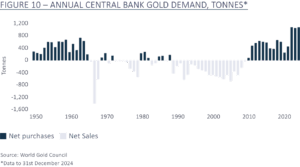

STILL A GOLDEN OPPORTUNITY

If government bonds and the dollar are no longer the protectors of the past, then Gold should remain on investors’ radars.

After having its strongest quarter in nearly 40 years, gold had a more sedate, if still positive second quarter. Fundamental support continues from Central Banks who remain committed to increasing holdings.

With US treasuries subject to sanctions should you fall on the wrong side of the US administration, and inflationary pressures elevated by a de-globalising world, gold makes sense.

There is a neat correlation between the rise in the price of gold and the US deficit over the last decade. Coincidence? We think it reflects a growing awareness that one of the most likely ways for governments to reduce deficits is through financial repression, just as the US did after the second world war. By keeping interest rates low, below the rate of inflation, then the real value of debt can be kept under control as GDP grows at a faster nominal rate (another reason Trump might like a dove in the Fed).

Financial repression deliberately undermines the value of bonds and cash in real terms, leaving gold as a better store of value.

For now, gold provides a buffer in a world where instability is on the rise and longer term it might prove the best defence should governments see inflation as the most acceptable way out of their funding hole.

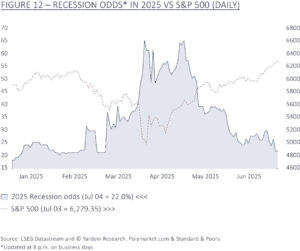

EQUITY MARKETS HAVE DECIDED IT’S ALL GOING TO BE OK

Just as bond markets regained their poise, so equity indices have recovered not only all of the tariff losses, but the US has shrugged off the uncertainty elicited by the threat that China’s DeepSeek could undermine America’s technology hegemony.

The capacity to shock has diminished with every post on Truth Social. The return of stability to Treasury markets has increased confidence that economies had weathered the squall and relief that events in the Middle East failed to spill over into further unrest or a destabilising surge in oil prices all served to becalm investors. Markets have climbed the proverbial ”wall of worry” back to the peaks of the year.

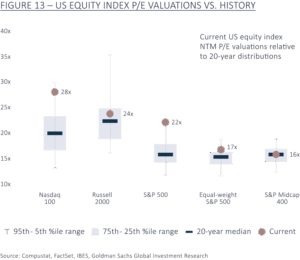

This has been achieved in the face of a modest downgrade in expectations for profits growth. Consensus US earnings growth has been cut from 8.5% to 3.7% as the more tangible impacts of the tariff tantrum were priced in.

With markets up and earnings down, equity valuations have risen across the world. The US returned to peak levels that had valuation signals flashing red earlier this year.

Expensive valuations alone are not a reliable signal of share price returns in the coming months and so are a catalyst for vigilance rather than concern. It places a greater reliance on growth in the economy and profits to support what looks an extended market. It also leaves the US market vulnerable to disappointments in economic growth or lapse in investor sentiment. There is not much margin of safety to protect against surprises.

Valuations for the rest of the world look far more reasonable with the UK and Europe several turns cheaper than the US, despite their stronger performance this year. Emerging Markets are cheaper still and remain unloved by the investment community.

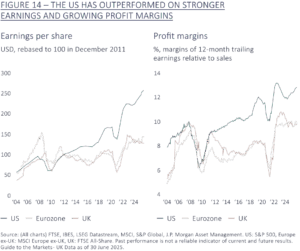

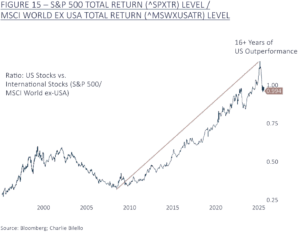

The US has deserved its premium valuation as it has delivered stronger growth, higher levels of innovation, greater investment and has benefitted from having a growing, mobile, dynamic labour force alongside low energy costs. The technology sector in particular has proven a major driver, generating exceptional earnings growth and higher profit margins. Indeed, to take a decisively negative view on the US is in some ways to bet against technology.

However, markets trade on fine margins and marginal change matters. After fifteen years in which the US has increasingly dominated capital markets, its share of equity market capitalisation, investor flows and level of out-performance against other regions means it will only require modest changes in flows to see other regions do better.

In the context of 16 years of outperformance, the last 6 months are but a blip:

Europe looks to be a current favourite as the US’s hostile approach to old alliances and isolationist agenda jolted the continent into action. Germany in particular has found fiscal spending religion promising industrial renewal and defence spending on a scale that would have made Mutti Merkel blush.

Emerging Markets too are tiptoeing from the shadows cast by China’s slow-motion property crash. With the retreat from globalisation placing more importance on regional trade the scale and potential for growth from Asia’s huge population is exciting. With growth stabilising, the dollar weakening and interest rates falling, interest in the region is growing.

Unloved, under owned and undervalued. The investment attractions of the region are growing.

IN THE ABSENCE OF NUMBERS JUST BUY THE NARRATIVE

Given ongoing uncertainty about tariffs, the economy, and with many companies unable or unwilling to provide short-term profit guidance, markets have chosen to focus on narratives, stories and thematics over fundamentals. This has meant huge dispersion in returns between sectors and stocks, with the shades of grey obscured by black and white. With companies still unsure of what the rules will be, market participants have coalesced around those things that they think they know for sure.

In the US this has meant a return to all things Artificial Intelligence and data centre related. Chip manufacturers, cloud providers and large language model developers have staged a Lazarus-like recovery from the trough. They have been followed by the historically pedestrian utilities that will generate the power needed to slake the insatiable thirst of AI and data centres.

In Europe the story has been a simple one of defence (part of the industrial complex) and banks. The argument for defence needs no introduction, with the US having raised the stakes NATO has responded with ever-increasing commitments to ramp spending. Given the rising trend in industrial nationalism much of this is expected to be spent with domestic manufacturers rather than the US heavyweights.

After a decade of repair following the GFC, European banks are now on a surer footing and seeing earnings accelerate with interest rates off the floor. They are largely out of the glare of tariffs and add to the mix excitement around consolidation and the potential for regulatory form and the cocktail is bubbling nicely.

Sector performance this year has been a game of best story wins:

All of these themes have a decent foundation in fact. Data Centre spending remains unbridled, increased defence spending is coming, and European financials are on a much sounder footing. But we also know that there are two sides to every story and that the most dangerous period in markets is when the story becomes fact and valuations become unhinged. As Mark Twain said:

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

The return of US valuations to extreme levels reflects a degree of complacency around the speed, scale and persistence of spending on AI. The numbers could be correct but when we are talking about such big numbers and such rapidly evolving technology things can change quickly. Remember DeepSeek?

European nations need to and want to increase defence spending, but it will take time for the money to flow, and it doesn’t take much cynicism to question how close they will get to 5%. With budgets stretched, governments face plenty of demands for funding from areas likely to have a far more meaningful impact on elections than defence.

It has been the nature of markets in recent years to leap on themes and stretch them far beyond where fundamentals and valuations make sense. Reflecting the changing composition of market participants, including the rise in the quantitative trading machines! This is a reality of markets and so something to be factored into decision making and to be adapted to. It creates different sorts of opportunities for active managers such as us, where we have a strong sense of the fundamental qualities and outlook for a company and so can take advantage of the overshoots.

We have exposure to and see plenty of opportunities that will arise in or because of increased spending and opportunities across technology, defence and financials.

Demand for semi-conductors, connectors, sensors and data will thrive on the back of the increases, as they should as we see growth in a range of other industries and markets exposed to the structural growth in digitisation and automation. However, we are also conscious that values in certain parts of the market have run substantially ahead of reality which sees share prices moving into Icarus territory. If the fundamentals are good, then we stand ready to buy them but only at the right price.

ANOTHER BRAT SUMMER?

As we have written in previous quarterly reviews and outlooks, the regime that persisted following the GFC has ended. We are transitioning to something different. A regime that will provide plenty of opportunities for growth but will require a more dynamic approach and a greater level of diversification if we are to maintain the resilience and consistency of returns to which we aspire on behalf of our clients.

This new world is inherently more unstable. The post Cold War peace dividend, globalisation, stable alliances, conventional politics and predictable policies have been disrupted meaning a search for a new equilibrium, one that is likely to prove fragile even if it exists.

Despite the noise, the most likely direction for the rest of the year is that we will see more balanced and geographically diverse growth, moderating interest rates and increasing corporate profits. However, most likely does not mean likely!

The nature of policy and the velocity with which things are changing means that making short-term decisions or chasing markets can be about as effective as chasing shadows. What we think we know for sure today could look completely wrong tomorrow.

Having a stable strategy to cope with a world in flux is critical to avoid being overwhelmed by the political noise and the flip flopping of policy. Such an environment calls for a broader and different type of diversification and being brave in areas where one has confidence.

Alan Little of the BBC recently wrote an article about how the centralised decision making of President Trump has made his own unpredictability a key strategic and political asset. Political scientists call this Madman Theory. It certainly seems to be proving effective.

For us as portfolio managers it makes a new environment even more challenging. For a world order that is rapidly being reset, we may look back on this period as one tinged by political genius just as we look back to 1971 at one of Elton John’s seminal works of genius which seem to resonate as much today as ever…

Article written by James Beck, Head of Investments.

This document is a Financial Promotion for UK regulatory purposes and is directed only at investors resident in the United Kingdom.

This document does not constitute investment advice or a recommendation.

Past performance is not a reliable indicator of future performance. The value of investments, and the income from them, may go down as well as up, so you could get back less than you invested.

This material has been issued and approved in the UK by James Hambro & Partners LLP, which is authorised and regulated by the Financial Conduct Authority and is a registered investment adviser of the Securities and Exchange Commission. It is listed in the Financial Services Register with reference number 513246. James Hambro & Partners LLP is a limited liability partnership registered in England & Wales with number OC350134 and registered office at 45 Pall Mall, London SW1Y 5JG. A list of members is available on request. The registered mark James Hambro® is the property of Mr J D Hambro and is used under licence.