HARNESSING RATIONAL OPTIMISM

It is hard to argue that the near-term future looks anything other than extremely challenging. With winter approaching, many could be forgiven for drawing the curtains. However, with good news in short supply it can be easy to forget what substantial advances have been achieved over longer periods of time. Reviewing the reasons why such progress has occurred suggests it is logical to believe in a better tomorrow. In this piece, we review how we try to build portfolios to harness such rational optimism while ensuring resilience to weather the inevitable setbacks.

“I have arrived at optimism not through temperament or instinct, but by looking at the evidence.” Matt Ridley

PART 1: THE CASE FOR RATIONAL OPTIMISM

THE SHORT-TERM FUTURE LOOKS BLEAK

Back to school feelings are hard to shake. But this autumn, it has been more difficult to avoid pessimism creeping in with the lengthening nights.

The ongoing war in Ukraine has put intense pressure on power supplies across the world. In Europe, polluting, coal-driven power generation has been replaced by a patchwork quilt of renewable energy generation. Insufficiently developed, this has combined with a lack of support for nuclear and failure to invest in adequate gas transportation and storage to leave the energy cover threadbare. Meanwhile the rising price of an ordinary shopping basket has become a common feature of the supermarket trip.

New-look governments are responding in the increasingly familiar way with fiscal handouts. This largesse understandably prioritises voters (households) over industry but likely only kicks the can down the road. Bond and currency markets seem to think so with many currencies, including the euro and sterling, sinking to levels against the dollar last seen in the 1980s.

Faced by an exceptionally wide range of plausible scenarios, central banks are focused on wrestling the inflation genie back into the bottle. However, their main tool to curb surging prices of goods and services is to raise interest rates to the point where economies are forced into recession. Demand is being destroyed to balance scarce supply.

The resulting stresses are particularly acute in the UK. Simplified figures suggest that even average households faced spending the better part of two-thirds of gross income on tax, energy bills and mortgages. With the prospect of working until August before having money to spend on anything else and after years of covid-exacerbated pressures, public service workers are on strike.

So far Asian economies have proven more resilient, perhaps having learnt the lesson of the 1990s crisis. However, China is still struggling with zero tolerance policies to coronavirus and politicians appear to have painted themselves into a corner.

The least dirty shirt remains North America. A better energy situation together with an immediate market stretching from mineral-rich Canada to labour-rich Mexico offers insulation against the world’s troubles. Unfortunately, US domestic political division seems to be growing while international tensions are running high.

Finally, we have had the death of Queen Elizabeth II. Reigning for nearly a third of the existence of the US Republic, the Queen was an anchor in many of our lives and her loss has added sadness to today’s predicament.

DON’T BET AGAINST HUMAN INVENTION

Yet this difficult near-term picture obscures the significant evidence that the world has tended to get better over longer periods of time.

In 1651, Thomas Hobbes described human life as “nasty, brutish and short”. And he wasn’t far wrong. As far as demographic research can tell, for most of human history, life expectancy hovered around 30 years.

However, using this key measure of progress, we have seen remarkable gains. Since 1900, global average life expectancy has more than doubled to over 70 years. And these gains are not isolated to high-income, industrialised countries. Today no country in the world has a lower life expectancy than the countries with the highest life expectancy in 1800.

A primary contributor to longer lives has been falling child mortality. The death of a child is a tragedy and reducing its frequency is a landmark in the landscape of human progress. It is one of the best measures of a society’s ability to protect the most vulnerable.

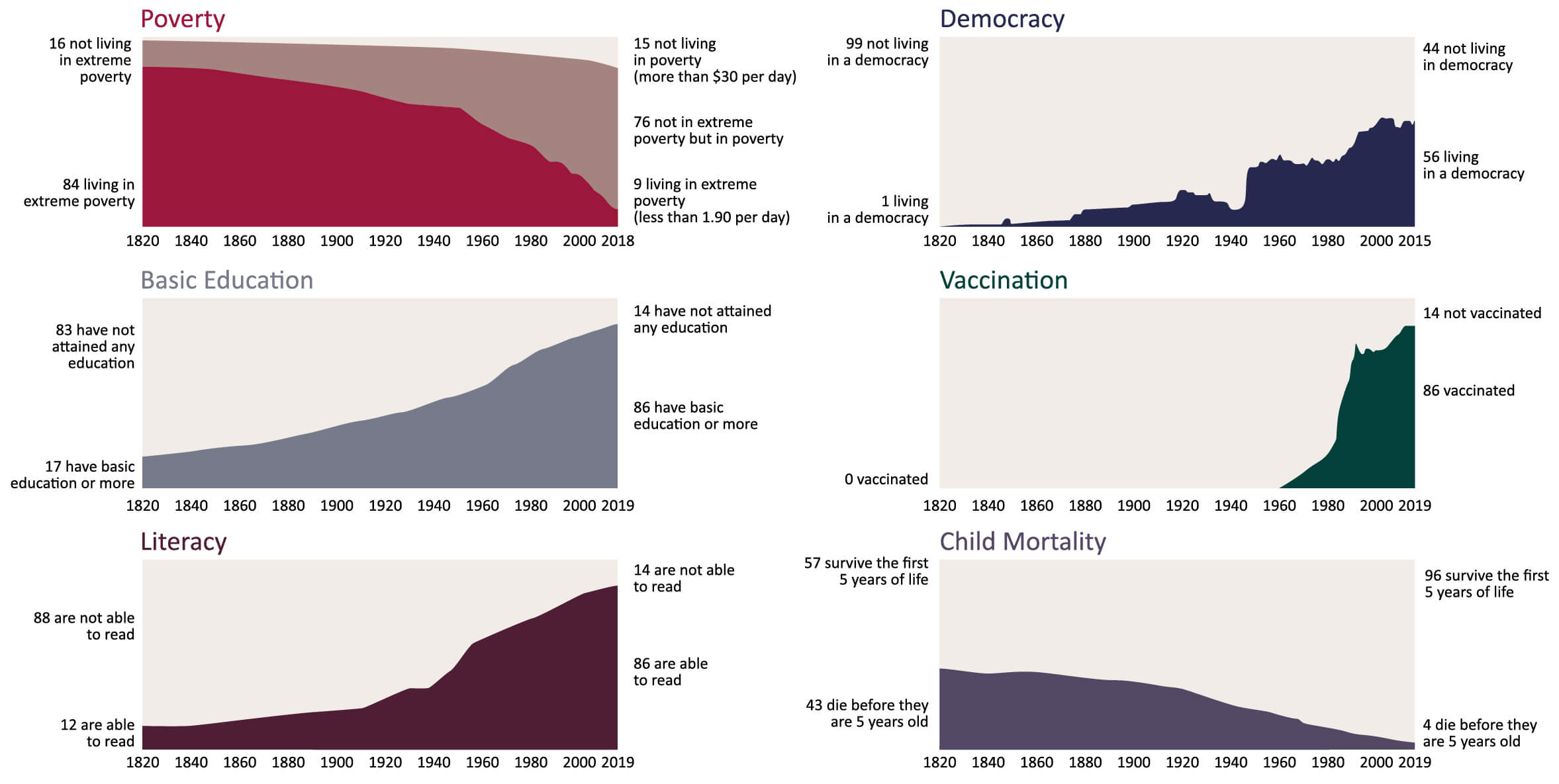

According to the UN, in 2020 globally 4% of all children died before they were 15 years old. That meant nearly 6m children died that year. Even one is too many, but compare that to the pre-modern world in which 1 in 4 children died before their first birthday and nearly half didn’t reach adulthood. As recently as 1950, some 20 million children died a year and that was with a population a third of the size. We have come a long way.

This change is interwoven with the increase in vaccination rates. Vaccinations are one of the most efficacious public health interventions and are a useful indicator of basic healthcare provision. In 2021 81% of infants globally received 3 doses of diphtheria-tetanus-pertussis (DTP3) vaccine judged by the World Health Organisation. Such vaccinations save lives. In 1990 measles killed more than half a million children a year. Since then, measles deaths have fallen 87%, largely due to vaccinations. Before 1798, vaccinations had not even been invented.

Vaccinations require many things, from expensive research to the last mile infrastructure to reach the arm of a child. Their prevalence goes hand-in-hand with poverty rates and there too we have seen great strides.

While estimating poverty is a science of uncertainty, experts largely agree that the proportion of the world living in extreme poverty (on under $1.90 per day) has fallen from 85% in 1820 to 9% today. In the last 20 years alone, the proportion of the world population living in extreme poverty has more than halved.Longer lifespans, fewer child deaths, less poverty, surely Malthus was right and humanity will be unable to feed itself?

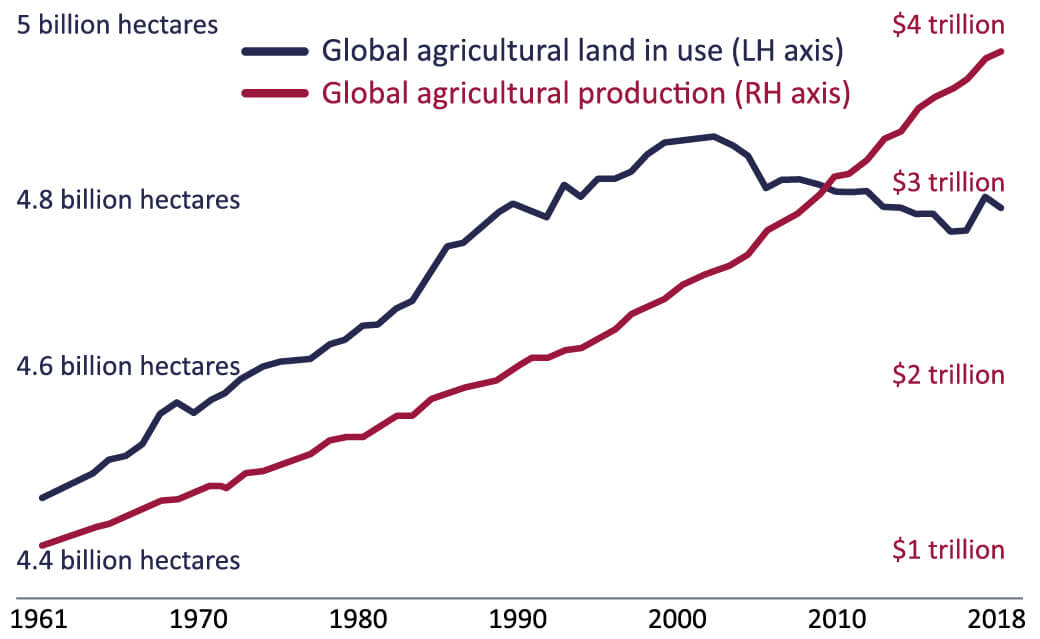

Global decoupling of agricultural land and food production

Agricultural land is the sum of cropland and pasture for grazing livestock. Production is measured in constant 2015 international-dollars, which adjusts for inflation. Includes all crops and livestock. Source: Our World In Data

The reverse. While the world’s population grew from 2.5 billion in 1950 to near 8 billion, the share of undernourished people fell from 2 in 3 to 1 in 11 according to the United Nations’ Food and Agricultural Organization.

Incredibly, this is despite global agricultural land (pasture and cropland) peaking 20 years ago. We have stopped needing more land to produce more food, largely due to more intensive farming methods. Indeed, without fossil-fuel-based fertilisers, we probably couldn’t feed half of those alive today and those left would be tied to the land – in 1800 83% of the US population were farmers compared to 2% today.

The world as 100 people

Source: Our World In Data

THE FLYWHEEL HAS FURTHER TO RUN

Naysayers will say that these examples are all in the past. Could this be the moment at which progress stops? Why should we hope that these trends continue?

That is to examine the true reason it is rational to be optimistic. It is why these changes have been occurring that supports positivity about the future.

Humans were primed for success, blessed by large brains and bodies capable of carrying them.

“Man is the lowest cost…non-linear, all-purpose computer which can be mass-produced by unskilled labour.” NASA, 1965

But what sets humans apart from other species is our ability to pass ideas from generation to generation. Unlike other animals, our learning is cumulative not cyclical.

This is what makes human innovation powerful. As Matt Ridley argues, over time an increasing number of people have been freed from labouring for the necessities of life by specialising their efforts – becoming better at what they do. By exchanging their goods and services with others, they have been able to do one thing and benefit from many. This created the room to innovate by thinking up better solutions to existing problems. The miracle is then passing those improvements on to the next generation.

In investing, we look for opportunities for compounding. For processes that result in good outcomes which in turn improve the processes to give better outcomes. These flywheels can become powerfully self-sustaining. And this neatly describes human progress, sitting at the intersection of ingenuity and luck.

The increase in knowledge has both driven and been driven by the build-up of a web of culture, technology, wealth, science, behaviour, markets, government. With more people and more innovation, there are sound reasons to think that our best days lie ahead.

WHY IS PROGRESS HARD TO SEE?

In life, many of the best things happen too slowly to notice: children growing up, wine-making, Ottolenghi pasta sauces…

Progress with big consequences is frequently gradual, from increasing vaccination rates to crop yields. And slow is often synonymous with invisible. Similarly, much progress lacks neat storylines or heroes that can be compressed into 180 characters. Instead it involves the sometimes complex and sometimes humdrum interaction of a host of successes and setbacks.

By contrast, bad news is typically sudden and alarming. One plane crash makes the news, the one hundred thousand planes taking off and landing safely each day do not. The dopamine hit of empty-calorie news keeps us hooked to the feed. And with the wonders of instant communication, everyone can be their own journalist.

But there is also something deeper, more human at work. Pessimism sounds seductive and clever. It appears to have exactitude on its side while optimism seems woolly and naïve. Optimism means believing in the ability to crack problems tomorrow that are intractable today, to drive change into areas that have been impossible to reach. Accordingly, while optimists are treated with caution, a pessimist at the right time is revered.

“It is not the man who hopes when others despair who is regarded by a large class of persons as a sage but the man who despairs when others hope.” John Stuart Mill

No surprise that so many think that the world is going downhill!

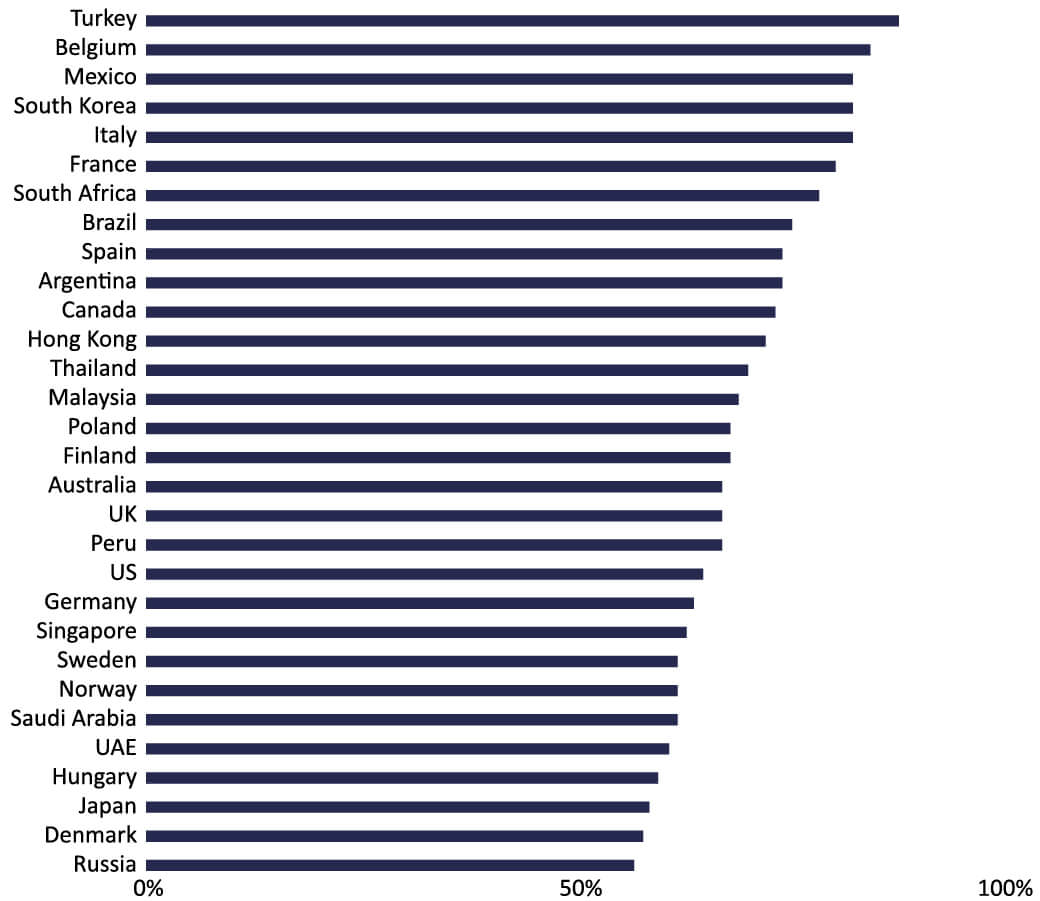

What is happening to the world?

Percentage who answered “getting worse”.

Overall, do you think the world is getting better, staying the same, or getting worse?

Source: Hans Rosling, Factfulness

HEALTHY SCEPTICISM COEXISTS WITH RATIONAL OPTIMISM

“I’ve got to admit it’s getting better / A little better all the time (It can’t get no worse).” The Beatles

Indeed, scepticism is warranted at times. Progress is possible and probable but not – much as McCartney and Lennon would suggest – inevitable. Like most trends, it suffers slowdowns and even reverses in places over shorter or longer periods of time.

A prime example of this is life expectancy through coronavirus. The National Center for Health Statistics highlighted that covid killed such a number in the US that life expectancy fell from 79 years in 2019 to 77 in 2021, the largest two-year decline in nearly a century.

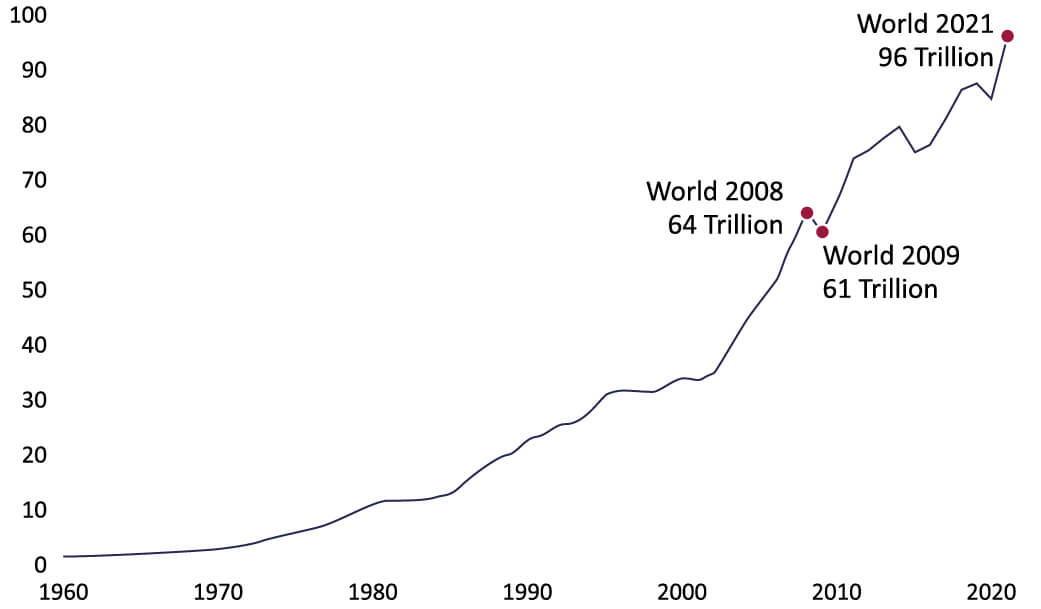

Such short-term reversals are an expectable part of progress, much like a traffic jam or diversion on a long car journey. During the worst financial crisis in decades, global domestic product (GDP – a measure of the size and health of an economy) shrank by 5% but rose 10% the next year. 13 years on, global GDP is 60% higher than it was in 2009.

Global GDP since 1960

Source: World Bank, GDP in current USD

POSITIVE CHANGE HAS UNINTENDED CONSEQUENCES

Of course, progress must be scaled against the costs involved, and sometimes it creates its own issues.

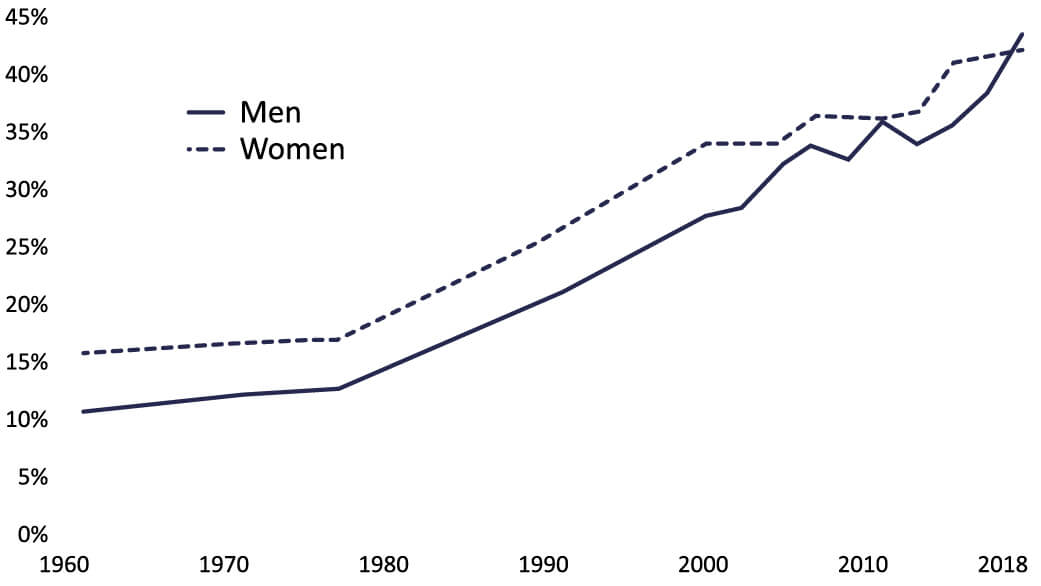

An example are problems of abundance, such as food. Through increased production and the globalisation of trade, we have reduced famine deaths nearly 99% compared to the 1800s. But humans are not good at saying no. ‘Too much’ has often replaced ‘not enough’, visible in soaring rates of obesity in many parts of the world.

US ADULT OBESITY RATE

Source: Centers for Disease Control and Prevention

Greater are the existential risks that we have created, from climate change and genetic engineering to nuclear weapons. We may have reduced the number of nuclear warheads from 60,000 in the 1980s to 10,000 today but it only takes a handful of decision-makers or even accidents to end the game for everyone. In 2007, six nuclear-armed cruise missiles were mistakenly loaded onto a B-52 bomber in North Dakota and their absence was not noticed for a day-and-a-half…

“As a society, we have been engaged not in the reduction of risk but in the reconfiguration of risk.” Malcolm Gladwell

These risks matter because many of our gains have come with increased interdependence, as individuals and as nations. In 1959, Leonard Read published his masterful I Pencil. An ‘autobiography’ of a humble pencil’s journey from Oregon loggers to Sri Lankan graphite miners, it highlights the complexity of its creation:

“Millions of human beings have had a hand in my creation, no one of whom even knows more than a very few of the others…There isn’t a single person in all these millions… who contributes more than a tiny, infinitesimal bit of know-how.”

Dispersed knowledge is powerful. But it is also vulnerable, exposed to any sharp shock that can tear society’s fabric.

GETTING BETTER + NOT GOOD ENOUGH = THE OPPORTUNITY

Rational optimism for the future is not to gloss over the real problems of the present. Rather, rational optimism requires a juggling act, holding two seemingly conflicting ideas in your head at once: that the world has been getting better but is not good enough.

“The future is already here – it’s just not evenly distributed.” William Gibson

There is much further to go and the progress to date shows change is possible.

PART 2: RATIONAL OPTIMISM IN PRACTICE

HOW WE HARNESS RATIONAL OPTIMISM

Over short periods of time the world looks alternately rosy and bleak. Yet over long stretches, it tends to get better. And in getting better, economic value is created that was not there before. So, if the long run is a string of short runs, how do we build an investment portfolio that can harness rational optimism while overcoming the inevitable near-term hurdles?

The core of our approach lies in identifying businesses that enable the innovation. Investing in those businesses allows us to capture a small sliver of human progress.

For example, history highlights how human lives have been lengthening and improving through better healthcare. And, healthcare innovation is seemingly accelerating as breakthroughs in technology such as cell and gene therapy combine with faster approvals for new treatments for unmet needs.

However, the odds of spotting the next big thing are low. Instead, we focus on finding the companies underwriting those advances, such as the US company Thermo Fisher.

Thermo Fisher is the world’s largest life science tools company selling products from centrifuges to analytical devices to pharmaceutical firms, academia and industry. They may not conduct the research but their equipment does – often critical to everyday tasks. Any improvement that Thermo Fisher can make to its products is a ‘win-win’, good for its customers, healthcare outcomes and the company alike.

Investing in such a business might not be as glamorous – or lucrative – as locating the next wonder drug. But it is probable that Thermo Fisher will still be powering healthcare innovation in a decade’s time. This matters because harnessing rational optimism requires finding companies with the durability to stick around and support the world’s real needs years in the future.

The same is true of the North American railroads, such as Union Pacific. One of only 7 major railroads, Union Pacific operates in an industry with high barriers to entry given regulation, capital requirements and network effects (it is hard to build a new railway!).

Their rails provide an essential transportation option which is often the cheapest or only viable option for long distance freight delivery giving significant pricing power. Attention over recent years on improved service together with pressure on companies to reduce carbon emissions should allow continued share gain from trucks which are the majority of North American transportation spend.

We don’t know exactly what the future world will look like. But we think it likely that people will still be trying to move physical things over long distances. Union Pacific was established in 1862 and we think it will be a royalty on American invention in 2062. Betting on continuity within a world of change can be rewarding.

Of course, in some parts of the world change happens quickly, nowhere more so than technology. Therefore it is important in these areas to find companies with high degrees of adaptability, such as Amphenol.

Amphenol manufactures electronic connectors and sensors which go into everything from sea cables to planes. The first-order investment case for Amphenol is simple: will the world’s economy grow; will electronics grow faster than economic growth generally; and can Amphenol’s products capture some of that growth?

While we are positive on all these questions, the second-order investment case is more powerful. This rests on Amphenol’s culture of adaptability that can allow it to change course as technology and demand changes.

The business operates on a decentralised basis with 130 general managers empowered with the authority to run their individual areas. This allows the flexibility and incentives to change course quickly. When coronavirus increased demand for the company’s pressure sensors in ventilators 20-fold in a month, Amphenol was one of the few able to react. As CEO Adam Norwitt put it to us:

“Competitors couldn’t deal with that…it’s about the speed and ability for a general manager to make the hires, invest the capital required. They called me at home on a Sunday and we made the decision. It’s about ingenuity and entrepreneurship at the lowest level of the company.”

Enablers to innovation coupled with durability and adaptability gives us the ability to harness long-term progress, with companies able to remain relevant even as the long-term trends to which they are exposed change.

RECONCILING THE NEAR-TERM CHALLENGES

The challenge is that while progress occurs over the long run, the world, markets and individual businesses inevitably have setbacks, some of them severe. For those moments, we have lines of defence to protect portfolios and turn difficult times into opportunities.

For many of our portfolios, this means supplementing our shares in companies with diversifying assets, such as bonds, alternatives, gold and cash. The exact composition of these defensive assets will vary through time depending on where we think safety is to be found. For example, for many years we found owning bonds difficult given low interest rates and uncertain inflation. Accordingly, we looked for other foxholes such as gold. Similarly, we can hold more or less of these protective assets depending on whether we think the skies are darkening or lightening.

The resilience this provides is buttressed by our balancing conviction with diversification. We want to hold positions in sufficient size as to make a difference if they perform strongly. However, we do not want our portfolios’ fortunes to be dependent on any one decision.

Like amateur tennis, investing is often a loser’s game. It’s about avoiding unforced errors rather than hitting aces and down-the-line passing shots. We want to avoid wipeout risk because the probability of being right is never close enough to certainty to justify excessive conviction. There is always room for an unforeseen event, as we experienced with the war in Ukraine.

Furthermore, our rational optimism does not mean that we know exactly how the future will look. So we invest in a range of companies to boost our odds of being on the right side of change. We want to have many shots on goal.

All of this is why we prize liquidity – the ability to buy and sell investments on good days and bad. We want the flexibility to take action should our clients’ circumstances evolve or we change our minds with the facts. The future is by definition a long time and will change substantially. Our team often talk about trying to make a series of sensible, well-informed choices rather than a single, perfect, ‘eureka’ decision when everything is solved forever and a day. This applies equally to our investment process.

Lastly but critically, our investment success is built upon the patience and commitment of our clients. It is why we go to great lengths to ensure that we have the right strategies for them and understand their needs, tolerances and time horizons. And it is why we try and be transparent on what we are thinking and doing. When the partnership between investment manager and client works, it creates a self-sustaining force that can power compounding for years.

LOOKING TO THE HORIZON

The world today feels a difficult place. Each day seems to bring a fresh headwind. It is easy to lose sight of the scope for improvement. Yet looking at the changes to date and the reasons why those changes happened make clear that it is rational to believe that the world of tomorrow can be substantially better than the world of today.

Reconciling rational optimism for the future with the litany of short-term challenges requires resilience and it is why we construct our portfolios as we do: letting our equity investments dip deep into the stream of progress while ensuring lines of defence to allow our portfolios to emerge stronger from the inevitable downturns.

Setbacks are a product of human behaviour and that is unlikely to change. Last year, rational optimism gave way in places to irrational optimism which lead us into today’s valley of pessimism. Markets will have to climb the wall of worry to get back out. In such moments, it is worth remembering that, even in the darkest of times, the sun also rises.

For illustrative purposes only and should not be construed or relied upon as advice.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.