INVESTING THROUGH THE NOISE

Humans have a natural tendency to reduce complex situations to simple stories. This makes us susceptible to being seduced by short-term narratives that portray an inevitable future in an uncertain world. In investments, this shows itself in thematic bubbles that inflate to the point that they burst. The COVID era has supercharged this phenomenon with a rolling set of bubbles in a number of areas.

In our enthusiasm for the new and different, the value of stability and consistency is often ignored. For those looking to preserve and grow their wealth, plotting a stable course around the highs and hangovers, has usually delivered returns ahead of the average.

In a year when the market has been gripped by hype about Artificial Intelligence (Al) and its potential to upend the world, we outline why we focus on proven performers and have confidence that they remain well placed to thrive whether Al lives up to the billing or not.

Blowing bubbles

A teacher asks her class, “if there are ten sheep in a pen and one jumps out, how many are left?” Everybody in the class says nine, except one pupil who says, “none of them.” The teacher comments, “I don’t think you understand simple arithmetic’; to which the pupil replies, “I don’t think you understand sheep”.

Successful investment strategies involve a balance of financial analysis and behavioural psychology. Despite the rise of so called ‘passive’ and quantitative trading strategies, the market remains a human system. This means it lurches from one emotional state to another; from optimism to panic; from the belief that change is afoot to despair that nothing ever changes.

Humans are a herd species. Scientific studies have revealed our inclination to follow the prevailing view even when we believe it to be wrong. We are also competitive. It’s difficult watching others do better than ourselves. Unsurprisingly, we often succumb to the ‘fear of missing out’.

Combine this with the tendency to rationalise life and complexity through simple but powerful stories and you have the ingredients for an investment bubble.

Eventually, as fresh buyers dry up, momentum breaks. What went up must come down as the bubble bursts. Of course, there is the potential to make money through this cycle but only by timing your entry early and your exit before the music stops. This is difficult to do once, let alone consistently.

Wind Market – Inflating Expectations

The US population is estimated to have accumulated additional savings of some $2.4 trillion during the pandemic through a combination of lower spending and government handouts. This has provided a cushion against the impact of higher prices which had been expected to weaken demand. Of that excess cash, over $1 trillion is still thought to be sitting in bank accounts.

Source: Bloomberg.

We have seen plenty of bubbles in the last few years. In 2019, the momentum behind sustainable investing and those companies exposed to it accelerated. A simple story emerged: good versus evil; renewables versus fossil fuels; asset light technology versus resource hungry miners. These black and white characterisations have obvious flaws. Regardless, parts of the market began to soar as excitement built.

The wind industry is a good example. Investors were focused purely on the growth opportunity – the green energy transition will mean more wind farms. Share prices of companies operating in the wind industry, such as Danish-listed Orsted, rose exorbitantly as potential rates of growth were extrapolated into the future.

Fast forward to today and reality has caught up with the narrative. Offshore wind is a complex industry wrestling with plenty of unknowns: the price of buying auctioned seabed in an intensely competitive marketplace; the untested degradation of capital equipment out at sea, and at its most simple, how much the wind will blow. The story sounded obvious, but the real world was more complicated.

Lockdown Winners – Extrapolating a Future Life Lived in the Spare Room

Source: Bloomberg.

Similarly, the extraordinary disruption of Covid proved the foundation for many bubbles to build and burst. Perceived lockdown winners such as Zoom Communications and Peloton, crypto currencies and vaccine developers saw values rise precipitously as a narrative grabbed hold only to come crashing down again.

The Rise of the Few

Emotions can drive markets in the short-term. But over a longer stretch, the market will reflect the profitability and prospects of the underlying businesses it represents. Warren Buffett captured this in his 1987 letter to Berkshire Hathaway shareholders, “in the short run, the market is a voting machine, but in the long run it is a weighing machine”. Knowing which way humans will vote in the next 6 months or one year is nearly impossible. Having an idea of which businesses have a good chance of growing in scale and delivering attractive returns for shareholders in the next five years is more achievable.

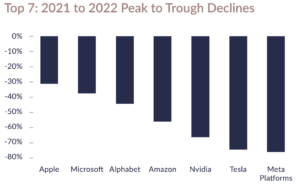

Today the market is embroiled in a new fixation. So far this year the global market, as measured by the MSCI World Index, is up 8% in sterling terms. The return of this index is weighted by the relative size of the constituent companies, with the larger businesses having a greater impact. In 2023 the entirety of the index return is accounted for by the seven largest companies1. Strip out the impact of these companies and the world equity market would be down for the year.

1Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla, Meta Platforms

Source: Bloomberg.

This is due in no small part to the explosion of enthusiasm around Artificial Intelligence (Al) such as OpenAl’s ChatGPT. But we would also argue it reflects a rebound from the extreme lows of 2022, a very difficult year with share prices of the same seven companies falling by 40% in aggregate.

2022 – A Year to Forget For Technology

Source: Bloomberg

There is no doubt that Al will open new avenues and has the potential to give a significant boost to productivity. We are working hard to analyse its impacts and already have exposure through Microsoft and Alphabet.

But if history is a guide, such a narrow stock market rarely lasts. Ominously, the last time market returns were this concentrated was 1999, the peak in the Dot-com bubble.2 While the hype and valuations are not as extreme today, the average valuation for those seven companies, at 30x profits, is double the average of the rest at 15x. For context, the fabled Nasdaq (the leading index of US technology companies) is on 26x.3

2 The Dot-com bubble is a reference to the rise in internet related company share prices in 1999 and the subsequent crash in the following years.

3 Bloomberg data using current price divided by consensus estimates for earnings per share in the next twelve months.

Source: Bloomberg.

BETTER THAN AVERAGE

The most important question is not “How can I earn the highest returns?” It’s this: “What are the best returns I can sustain for the longest period of time?” Morgan Housel.

When performance is measured in months and quarters there is a determination to strive for ways to excel and stand out over every period. But what sets the most successful investors apart is not simply the level of return but the consistency and longevity of their track records. High growth strategies are hard to sustain. They require the ability to recognise when enough is enough and the skill to skip to the next big thing. High growth businesses can also be very risky. They attract a lot of attention as competitors move in, they have many internal pressures that can become self-destructive, and the valuation demanded is often not reflective of the risks investors are taking.

In his latest memo, Howard Marks hits on a point that we have long held core to our philosophy.4

4 Howard Marks is the founder and Chairman of Oaktree Capital Management.

“I feel strongly that attempting to achieve a superior long term record by stringing together a run of top-decile years is unlikely to succeed. Rather, striving to do a little better than average every year – and through discipline to have highly superior relative results in bad times – is: less likely to produce extreme volatility, less likely to produce huge losses which can’t be recouped and, most importantly, more likely to work (given the fact that all of us are only human).”

While it doesn’t sound exciting, a strategy focused on being consistently better than average can over time lead to a significantly better than average outcome. Moreover, it is a strategy that carries a much higher probability of success.

Betting on Sameness

Rather than obsessing over themes or chasing stories, our strategy is based on a rigorous and repeatable process. We look for business models that have stood up to the test of time, for management teams and cultures that create an environment of adaptability and opportunism. As Charlie Munger said, “positive and negative surprises are not equally distributed across good and bad companies. Good things tend to happen to good companies”. Our view is that too much of the investing world is preoccupied with trying to work out what is going to change; we are just as concerned with what is going to stay the same.

“Show me the incentive and I’ll show you the outcome”

Understanding the culture of a business is key to building confidence in its potential for continued success. This includes both the alignment of key individuals’ interests with shareholders and the organisational structure. This often leads us to companies which have a higher level of owner or founder management. These individuals run their companies with a different mindset to the typical CEO. They also tend to have a level of decentralisation that pushes control to the coal face where employees are incentivised to make decisions for their customers as they see fit. Companies are complicated; their organisation matters for long-term success.

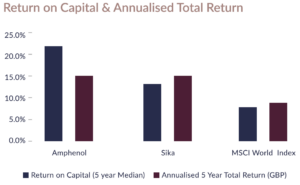

Amphenol is a good example. They are a leader in sensors (which detect physical signals such as light, heat or pressure) and connectors (connecting electronic components). The proliferation of electronic devices will underpin revenue growth for years. However, we are equally interested in their operating model and incentives that align management with shareholders. We have met Adam Norwitt, the CEO, regularly. He has been CEO for 15 years and owns more than $100m of company shares. The business is managed in a decentralised fashion where each individual business unit is given the freedom and flexibility to operate in their niche. Through this structure, Amphenol’s entrepreneurialism supports consistently higher growth than their competitors.

Sika has a similar cultural bedrock. As the market leader in the chemical additives that are used in concrete, mortars and other building materials, Sika provides the critical characteristic like quick drying, viscosity or waterproofing that are essential to their customers. They are structurally positioned to benefit as buildings are decarbonised and infrastructure is rebuilt. In addition, they sell high performance adhesives into the auto market that is seeing strong growth from the shift to electric vehicles.

Equally important is the way that Sika has aligned itself with shareholders. Group management are required to hold more than 200% of their base salary in shares (the CEO is 500%) and their long-term incentive plan is based on return on capital employed rather than the more traditional and malleable metrics such as earnings growth.

Again, the organisational structure of Sika is important; the business is decentralised with key individuals in regions and specialties owning the customer relationship and maintaining the responsibility of decision making. Over half of their salespeople are engineers who position themselves on-site alongside their construction customers, providing consultation and solutions in real time. These engineers feed their insights back to Sika’s innovation centres where new products are invented. These are high barriers for other companies to overcome.

Both Sika and Amphenol, as market leaders, are well placed to grow on the back of several thematic trends. Yet it is their organisation and culture that gives us the confidence to hold these businesses with conviction.

Good businesses with strong culture and alignment of interests should deliver better returns

Source: Return on Capital, Holt Credit Suisse (Holt’s return on capital or ‘cash flow returns on invested capital’ is a measure of the cash profits a business generates relative to the total amount of capital invested). Annualised Return, Bloomberg. Past performance is not a reliable indicator of future performance.

Mission Critical

We are drawn to companies that sit at the heart of their customers’ daily activities. Where their products are a relatively small cost compared to the value they provide, are often sold via a subscription creating a recurring stream of revenue, and where their embedded nature means the cost of moving to another solution is high.

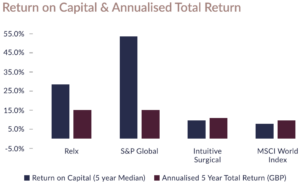

Relx is a diversified business operating in four key markets: legal, scientific research, insurance and exhibitions. The first three account for most of the group’s profits and share a common theme in providing digitised data and software tools that bring productivity and functionality to the customer. Today more than 80% of their revenues in legal and scientific research are under a subscription contract. As an owner of proprietary data, Relx is at the forefront of using Al models that interrogate and interpret data so that researchers, lawyers, and underwriters can make faster and more accurate decisions. We find similar characteristics at S&P Global and Intuitive Surgical.

S&P Global is a leader in providing financial data across capital markets. Many of their divisions are a fundamental part of the day-to-day operations of their customers. Platts, their commodities pricing platform, provides prices that are embedded into the contracts of two counterparties. S&P Ratings issues a rating on nearly every piece of corporate and government debt that is issued. Without an S&P rating companies and governments would be subject to interest costs significantly higher than the cost of the rating over the lifetime of the security.

Intuitive Surgical is the leader in robotic surgery having entered the market with the da Vinci machine in 2000. Hospitals have built their operating theatres and processes around these machines, and they are now the standard on which surgeons are trained. Guys and St Thomas’ Hospital in London has just completed the 10,000th operation using their original surgical robot. The chance of a competitor breaking this ecosystem looks low.

Intuitive Surgical do not know how Al is going to develop but have collected data on more than 10 million procedures. This proprietary information is now helping the machines to better assist surgeons, avoiding errors and improving patient outcomes. Patients spending less time in hospital benefits creaking health services and outweighs the initial cost of a da Vinci.

None of these three companies are subject to an unsustainable bout of investor interest but are steadily growing, taking market share and providing above average outcomes for shareholders.

Source: Holt Credit Suisse and Bloomberg. Past performance is not a reliable indicator of future performance.

Cost Leadership

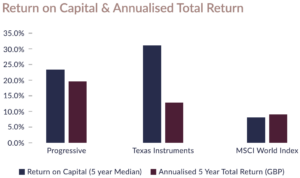

Progressive is a US-based auto insurance provider. Auto insurance is an attractive marketplace – cars are a necessity, they must by law be insured and the complexity of fifty states with fifty separate regulators makes for high barriers to entry.

Progressive is often described as a technology company operating in the insurance market. Their leadership in the use of telematics to monitor driving habits and their in house systems used for risk assessment and claims handling mean that Progressive is the lowest cost underwriter. The auto insurance market is competitive and commoditised so being the lowest cost producer provides an advantage that can lead to durable and sustainable returns.

Texas Instruments, a semiconductor manufacturer, is in a very different market to Progressive but we see echoes in their competitive advantage. Texas has the leanest and most efficient manufacturing capacity amongst peers as proven by the highest profit margins. Over the past two decades Texas has invested counter to the cyclical winds and built a scale that is hard to replicate.

The semiconductors they manufacture are required for thousands of applications across industries and are typically low cost to the customer. They are designed into the product making it hard to swap to another chip.

The electrification of all things means that their semiconductors are proliferating across consumer, industrial and automobile products. The growth in demand for semiconductors is attractive but the decision to own Texas Instruments was built on an understanding of their durable competitive advantages that will, over time, accrue to shareholders.

Source: Holt Credit Suisse and Bloomberg. Past performance is not a reliable indicator of future performance.

In the modern world news travels fast and the digitalisation of the equity markets means that investors can chase the next story or theme with relative ease. Many banks have evolved to sell investors thematic baskets designed to satisfy their short-term needs. More sugar for a higher high.

Our investment strategy is deliberately built on more durable foundations and is designed to help us navigate through the noise. If we can own a collection of above average businesses that generate above-average returns and hold them for a meaningful timeframe we are confident that our clients will do much better than average in the long run.

Article written by Mark Leach

For illustrative purposes only and should not be construed or relied upon as advice.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.