A YEAR FOR TREADING CAREFULLY

“My only question is who is our bigger enemy, Jay Powell or Chairman Xi” President Donald J Trump

In 2022, Central Bankers didn’t simply cool the party by taking away the punch bowl. Faced with inflation rising to 40-year highs, they turned off the music, flicked on the lights and threw everyone out onto the street.

The Fed Put became well and truly kaput as fighting inflation and supporting the wider economy superseded any desire to stabilise financial markets.

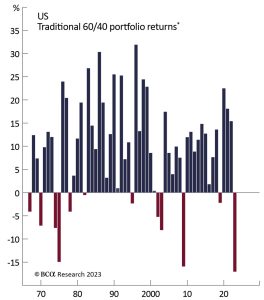

As growth decelerated there was more than a whiff of stagflation about asset returns. World equities delivered their worst year since the depths of the financial crisis whilst bond markets collapsed. A 60/40 portfolio (60% equities, 40% bonds) – the traditional balanced strategy’s North Star – lost 17% in US dollar terms in 2022, the worst performance in 50 years. Commodities and the dollar were the only assets to hold up in a year when the end of zero interest rates and the death of free money meant the deflation of asset prices across the world.

Entering 2023, inflation remains high but looks to have peaked in most regions. Central banks have set out their stall to beat inflation at the expense of growth. That resolve will be challenged as the effects of the rapid increase in rates begin to reach the economy and recessions loom. With valuations having reset lower the scale and composition of the slowdown will determine the direction of policy and ultimately investment returns this year.

Looking further out, events of the last few years, from President Trump’s sanctions to COVID to the return of military conflict in Europe, have catalysed a strategic change in which nations and companies have begun to prioritise resilience and security over maximising efficiency. This will have more enduring implications for portfolio construction and the foundations of the next cycle.

The shockwaves of the pandemic continue to reverberate whilst the full impacts of the highest interest rates in over a decade have yet to be revealed. The blow-ups in cryptocurrencies will not be the last landmines of this cycle, caution and resilience are the watchwords in what will be a year for treading carefully.

Worst year in 50 for a balanced portfolio

*Portfolio composed of 60% S&P 500 and 40% 10 year treasury bonds. Past performance is not a reliable indicator of future results.

2022 – one of the toughest in an investment generation

“This is what it sounds like when doves cry” – Prince

2022 proved to be a year of extremes, with financial literature littered with hyperbole and references to the “highest since”, “biggest since” and “fastest since”.

Inflation reached forty-year highs, bonds suffered their biggest falls since the Second World War and US interest rates rose at their fastest rate since the early 1980s when the 6’7’ Paul Volcker towered over the Federal Reserve – a time when inflation was 14.8%. Alongside these highs were considerable lows, as UK consumer confidence hit rock bottom levels not recorded since measurement began in 1974 and investor sentiment fell to the trough of the great financial crisis.

The inflationary foundations were well set coming into the year. Supply chains, still gummed up by residual pandemic restrictions, were unable to satisfy the surging demand from liberated western consumers armed to the teeth with savings accumulated during incarceration.

With central bankers too sanguine as to the building threat, the energy price shock following Russia’s invasion of Ukraine in February propelled inflation higher. Brent crude had risen by 50% in June, peaking at over $120 per barrel. A squeeze on disposable incomes followed. The rising cost of living infected consumer psyches, becoming embedded in rising wage demands as electorates felt the pinch.

One of the challenges of inflation is this psychological component. It drives expectations and ultimately fostered the wage-price spirals of the seventies. Once inflation becomes embedded in expectations it can escape policy makers’ control. Only extremely painful action can break the cycle; witness the early 1980s. This explains the belated and aggressive tightening across the world.

Central bankers have told us that they are not done yet but the scale and pace of rises will slow this year. Whilst inflation remains in focus, the narrative of 2023 is likely to be dictated by the impacts of the full throttle rise in interest rates on economic growth and corporate earnings rather than prices.

Market Returns – the bond bubble bursts causing plenty of collateral damage

The vertical climb in interest rates saw the US risk-free rate move from 0.25% to 4.5% in just nine months. This lit the touchpaper for a material repricing of assets that had been buoyed by the zero rates policy and monetary generosity of central banks for over a decade.

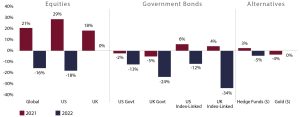

Following a strong 2021 – few places to hide in 2022

Asset class returns in local currency

Source: Bloomberg/James Hambro & Partners. December 2022. Equities: Global is MSCI AC World Index, US is S&P 500, UK is FTSE All-Share. Bonds: US Govt is BB US Government Conventional Index, UK Govt is FTSE Actuaries All Gilt Index, US Index-Linked is BB US Government Inflation-Linked Index, UK Index-Linked is FTSE Actuaries UK Index Linked Index. Alternatives: Hedge Funds is HFRX Equal Weight Strategies. Past performance is not a reliable indicator of future results.

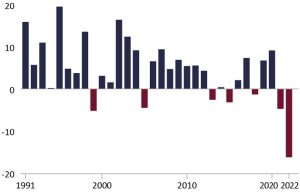

A historic sell-off for bonds

Annual return of Bloomberg global aggregate index (%)

Source: Bloomberg. Past performance is not a reliable indicator of future results.

Equity market valuations reset in a flash. The MSCI All Company World Index fell by 16% in local currency terms, its biggest fall since 2008 and the third biggest drawdown this millennium. The more expensive areas of the market were hit the hardest. This meant the US, the more technology-focused Nasdaq index declined by over 30%. China too was weak given the stubborn adherence to zero-COVID policies, a deflating property sector and concerns over the ramifications of President Xi’s consolidation of power.

UK equities provided a rare shard of light. The FTSE All Share closing flat given its heavy weighting towards energy, commodities, and defensive sectors together with a cheap valuation.

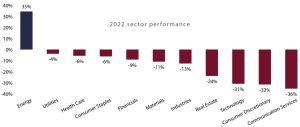

Underlying these headline returns, the dispersion in sector performance was extreme with a 70% spread between the best and the worst. There was only one place to hide, with the energy sector up 35%. All other sectors fell. Facebook (Meta) and Tesla, bellwethers of the tech boom, fell by 70% as the big tech companies lost $5 trillion in market value alone – total UK GDP in 2021 was only $3.2 trillion.

Equities usually fall in more difficult economic environments. However, for years investors have been able to rely on bonds providing insulation in those tougher times. In 2022 they singularly failed to ride to equities’ rescue. Government bonds, previously a paragon of stability, suffered some of the biggest falls of all asset classes. Conventional UK Gilts fell by 24% and US Treasuries were 13% lower.

Commodities provided most of the gains for the year as the Russian military attack on Ukraine and subsequent sanctions spurred energy and agricultural prices. Brent Crude surged before a combination of weaker global growth and a mild winter in Europe allowed prices to fall back but still ended the year 10% up. Industrial metals fared less well with Chinese demand weakened by COVID restrictions. Copper prices fell 11% and aluminium 16%.

Gold and the US dollar burnished their protective credentials with the former flat on the year whilst the trade weighted dollar rose 8%.

For equities energy was the only game in town

Source: Bloomberg/James Hambro & Partners. December 2022. MSCI All Country World sector index returns shown on total return basis in local currency. This chart provides a year-to-date snapshot of market performance. This graph provides a limited snapshot of market performance. Past performance is not a reliable indicator of future results.

The year ahead – the most predicted recession in history?

Consensus amongst strategists, commentators and economists over the prospects for the US economy is unusually high even for this time of year – a recession is coming, the question is when. A record 70% of economists polled by Bloomberg in December expect the US economy to enter a slowdown in the next twelve months, up from only 30% last June. It is easy to see why.

Financial conditions in the US have tightened at warp speed, moving from being looser than ever before to being extremely restrictive in a matter of months. Such a move has almost always precipitated an economic downturn.

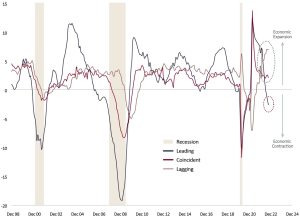

Leading economic indicators are pointing convincingly to a recession, whilst coincident real-time indicators have also begun to roll over. Lagging indicators are still on an uptrend but, as the name suggests, these will not turn negative until well into any slowdown.

The challenge for policy makers is that whilst everyone expects a recession, actual signs in the consumer-driven US economy are thin on the ground. The Atlanta Fed Nowcast of current economic growth suggests the US economy grew at an annual rate of 3.9% in Q4 2022, an acceleration from the 3.2%

recorded in Q3. Consumer confidence has started recovering from the lows.

US Conference board’s indices of leading, coincident, and lagging economic indicators

% Change on year ago

Source: Bloomberg/James Hambro & Partners. December 2022. Equities: Global is MSCI AC World Index, US is S&P 500, UK is FTSE All-Share. Bonds: US Govt is BB US Government Conventional Index, UK Govt is FTSE Actuaries All Gilt Index, US Index-Linked is BB US Government Inflation-Linked Index, UK Index-Linked is FTSE Actuaries UK Index Linked Index. Alternatives: Hedge Funds is HFRX Equal Weight Strategies. Past performance is not a reliable indicator of future results.

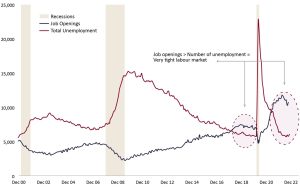

US labour market is extremely tight

Sources: Bureau of Labour Statistics, William Blair Equity Research.

Most of all, the US job market remains robust. The unemployment rate in December fell back to 3.5% and shows few signs of softening with the demand for labour high and many more job openings than applicants. Unsurprisingly wages continue to rise given the imbalance.

“Restoring price stability will likely require maintaining a restrictive policy stance for some time…and a sustained period of below-trend growth”

Federal Reserve Chair, Jerome Powell

With the US consumer proving resilient for now, the Fed is firmly focussed on bringing inflation down. Headline inflation at 6.5% and core services inflation of 5.7%, whilst falling, are well above the official target of 2%. The message from central bankers is clear: rates are going to rise further and stay there until the job is done.

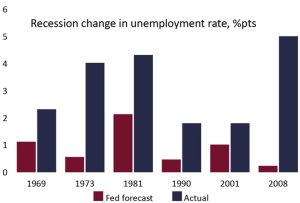

Yet any good student of economics will tell you, monetary policy works with ‘long and variable’ lags. The implications of one of the fastest rate hike cycles in history will take time to reveal themselves as the butterfly effects flutter their way through the US economy. Unemployment, once it begins to rise, has a habit of forming a negative feedback loop for the economy and the Fed does not have a great track record of either predicting or controlling moves in unemployment.

The fed has a lousy record of predicting unemployment

Source: Federal Reserve and Bloomberg.

Recession risks high but not pre-ordained

After a horrible 2022 this may feel like a gloomy hangover. However, whilst the odds are in favour of slowdown in the US, this is not pre-ordained and there are potential silver linings.

Inflation is falling, and, if it continues, this could take the pressure off rates allowing a smoother glide path to an elusive “soft landing”, a phrase only whispered in corners but one that would be good for most asset classes, particularly equities.

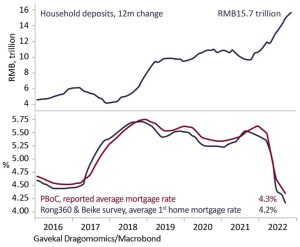

China, having been a headwind for growth, may become a tailwind and counterbalance the anticipated slowing of the US. The change in covid policy and priorities in China could see an economic acceleration led by the consumer as the population emerge from confinement. Europe too may benefit, given its economic ties and allure for tourists who have spent 1,016 days unable to leave the People’s Republic.

Just like western consumers in 2021, Chinese citizens have accumulated a financial war chest during confinement. They are well placed to unleash this monetary arsenal in a similar frenzy of “revenge spending”.

Chinese households are cashed up, and mortgage rates are down

Source: Gavekal Research.

In the UK employment is one of the few bright spots with the unemployment rate of 3.7% the lowest since 1973 and well below the average of 6.7% for the last 50 years. But that is where the good news ends with inflation higher than in the EU or US, the economy likely already in a recession, and public sector borrowing this financial year set to be £177 billion – nearly twice expectations as recently as March.

With the most recent UK government resorting to fiscal conservatism and any giveaways likely to target keeping vital public services afloat rather than stimulating growth there must be questions as to how much further rates can rise. If one economy is to be snared by stagflation, then the UK looks a reasonable bet. This would not seem to make a strong case for sterling.

Outlook for markets – a much better starting point

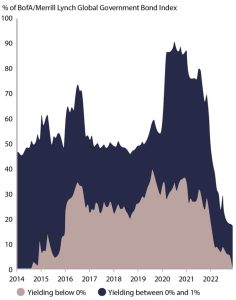

Only 18 months ago 90% of government bonds yielded less than 1%; $18 trillion paid less than 0%. Now a 10-year US treasury will deliver nearly 4%, a rate of return not seen for 14 years. Even cash now offers a respectable nominal return. There is now an alternative to equities.

The era of negative bond yields is over

Source: JP Morgan Asset Management. Past performance is not a reliable indicator of future results.

Further rises in interest rates could see modest pressure on bonds in the earlier part of the year. But with government bond yields nearing the 4% to 5% range that persisted in the early 2000s, these traditional safe havens are much more attractive, offering income, a long term positive real yield and diversification to portfolios in the event of a recession. Having long been cautious on bonds, after a 25% fall the time has come to begin adding back.

Nominal 10 year government bond yields providing a return again

Source: JP Morgan Asset Management. Past performance is not a reliable indicator of future results.

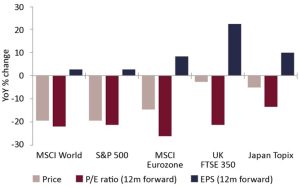

Equities too have seen a major reset in valuations. Last year’s drawdowns were not due to any contraction in earnings, which in most major geographies actually increased over the year. The falls in prices simply represented markets getting cheaper.

2022 returns were driven by valuation de-rating, earnings expectations barely moved

Source: SG Cross Asset Research/Equity Quant, Factset, I/B/E/S. Past performance is not a reliable indicator of future results.

This has left the MSCI world equity index trading fractionally below its thirty-year average. Valuations are rarely a signpost of the short-term direction of markets but provide a good starting point in assessing longer-term potential. Whilst by no means a bargain, those buying stocks today do so at a price that has historically delivered good returns over the next decade.

Global equities are not expensive

Source: Bloomberg. Past performance is not a reliable indicator of future results.

However, we are not yet convinced that equities are out of the woods. Although markets have adjusted to the reality of higher rates, earnings expectations do not yet reflect the risks and potential reality of a recession. Nor have we yet seen the sort of capitulation event that has previously characterised the end of bear periods.

Profit margins are high against all comparisons but will come under pressure from rising input costs. In the face of a slowing economy there will be a limit to how far businesses can raise prices to offset the squeeze. Earnings could fall even if top line revenues hold firm.

Profit margins vulnerable to a squeeze

Source: JP Morgan Asset Management. Past performance is not a reliable indicator of future results.

While the near-term outlook for earnings looks uncertain, given the material reset in valuations and cautious positioning amongst institutional investors, we do not see now as a time for us to become more defensive from our current cautious positioning.

We spent much of 2022 adapting portfolios to be more resilient in the face of a more difficult market. We therefore enter the year excited about the long-term prospects for the businesses and holdings we own on our clients’ behalf. The heavy lifting in portfolios has been done.

Looking ahead – prioritising resilience over efficiency

The tumultuous events of last year (or three!) have forced us to be more active than usual in adapting portfolios. This work has been aimed at strengthening our foundations and building resilience in the face of a broader set of potential outcomes. This is the role an active approach is designed to play. It enabled us to move quickly following a difficult start in 2022 to deliver a much stronger second half of the year.

However, the events of the last few years could mark a step change in the regime that persisted following the deflationary bust of the Global Financial Crisis. They have already brought the end of free money and the bear market in cash (at least for now). This requires a more strategic review of how the next five years or more may differ and what that means for longer-term planning. There are a few things on our mind.

A New World Order?

“And you’d better start swimming, or you’ll sink like a stone for the times they are a-changin’” – Robert Zimmerman

Journalists and investment writers are always quick to reach for the fin de siècle narrative and all that it encompasses. The reality is that trends evolve and emerge over years built on multiple events and transitions.

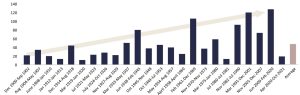

The US economic expansion from the end of the banking crisis to the start of the covid crisis was the longest in over a century at over 120 months. The average since 1900 is 45 months. Cycles had been getting longer since the early 1980s as falling inflation and rates coincided with the peace dividend of the thawing Cold War. However, several trends that have been gathering momentum under the surface were brought into the open by recent crises. This may mean that we see a return to the shorter and more volatile cycles of the past.

U.S. economic expansions had been trending longer, especially since the 1960s…

U.S. economic expansions without recessions, number of months trough-to-peak, 1990 – 2022

Source: National Bureau of Economic Research, Bureau of Economic Analysis. Data as of June 2022.

Globalisation stalled, now shifting into reverse

Just as it heralded the extreme period of zero interest rate policy, quantitative easing and an era of secular stagnation (low growth and productivity), the 2008 financial crisis marked the zenith of global co-operation. Surging protectionism, economic populism and nationalism were variably rewarded at the ballot box. Autocracies were emboldened to retrench and harden their stances rather than move towards democracy.

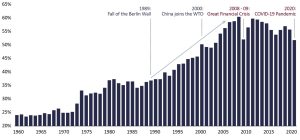

Trade as a percentage of Global Gross Domestic Product peaked in 2009 at 65% and it had fallen by 10% even before the pandemic and last year’s events in Europe. The primary reason is clear.

The end of 20 years of Hyper-Globalisation

Trade as a proportion of world GDP

Source: World Bank. As of December 2020. For illustrative purposes only.

The most important economic relationship underpinning globalisation, that between the US and China, has come under strain. A relationship once based on mutual economic benefit has become fractious as China’s growth and development has seen it evolve from outsourced manufacturing hub to economic rival. Technology theft, Trumpian sanctions and data security have marked staged escalations in an economic proxy war. Add in the strategic tensions around spheres of influence and geopolitical ambition and the chances of globalisation reaching new heights look minimal.

The pandemic raised profound concerns around the fragility of global just-in-time supply chains, whilst Russia’s invasion of Ukraine revealed the risks on relying on others for vital resources. National and corporate behaviour is changing. Prioritising security over cost suggests that costs will rise as companies and governments support the reshoring of key processes and industries.

Labour is back in fashion

This is not a comment on the sartorial attractions of Keir Starmer, rather that dynamics in the labour markets are changing. After decades of ceding share of GDP to companies and business owners, labour is striking back.

Demographics mean that working age populations are shrinking, particularly in the developed world but also in China where the one child policy is coming home to roost. In Europe the share of the population retiring in the next 5 years (those aged 60-64) is 6.5%, a whole percent more than the 5.2% aged 15–19-year-olds that should be filling their shoes – put another way Europe will need to find another 4.5 million willing workers.

The pandemic accelerated the natural shrinkage of the labour force as many older workers embraced the “life’s too short” principal, retiring early. Participation rates have fallen and barely recovered, part of the reason demand for workers continues to outstrip supply in the US with the inevitable repercussions.

Just as the supply side is shrinking so trends around reshoring and the care of an older society will boost demand for workers in jobs not easily automated.

The pendulum is swinging back just as costs of living are colliding with populism and militancy, as reflected in the storming of capital building in Washington and Brasilia and the industrial action in the UK this winter. This will have implications for companies, particularly those that rely heavily on labour, supporting our view that the next few years may be very different from the past.

High inflation might be part of the solution for governments

The returning power of labour and populism is being reflected in governments’ policies. China’s common prosperity policy is the command economy’s clear articulation of what many more democratic regimes are stiving for.

Austerity has been jettisoned to provide recue remedies to shuttered economies. Having opened the pandora’s box of fiscal spending it has become very easy for that to become the ‘go to’ solution for any crisis.

The UK government’s response to protect consumers from rising energy costs means that they will now need to borrow £177 billion this year; the OBR forecast was £99 billion nine months ago. Even fiscally conservative Germany will issue more debt in 2023 to counter the energy crisis than they did to protect their economy through COVID.

This means that debt to GDP ratios in many countries have reached levels over 100%, not seen since the aftermath of World War II.

With higher interest rates raising financing costs these levels will need to come down. There are two ways this might happen. The first is to repay debt either by cutting spending or raising taxes. Both look politically difficult wherever you are.

The other is to take a leaf out of the post war playbook and inflate its away through financial repression. The theory here is that inflation means an increase in the headline nominal value of the economy even if real standards of living stagnate. By growing the bottom part of the debt/GDP equation then the ratio mathematically comes down.

Given the options available we suspect that governments will view higher inflation as the lesser of two evils.

Long-term inflation expectations in the US are still anchored near the 2% levels that have persisted since 2008; we think the risks are skewed to the upside. Companies with pricing power, resource stocks, gold and inflation protected bonds all remain attractive.

Structural Changes bring new opportunities

The 2010s was the era of big tech and big ideas, with valuation concerns taking a back seat to stories of disruption, rapid growth and massive addressable markets as smartphone adoption exploded.

The pendulum of market leadership swings each decade

Source: Gavekal Research

We are now in a different environment where the cost of capital is higher than at any time since the financial crisis. Profits today rather than promises about tomorrow are back in fashion. The past tells us that few companies remain market leaders over the very long term.

While decade-long predictions should be treated with a healthy dose of scepticism, we would not be surprised if market leadership passed from the technology sector to the industrial sector and have made several changes to portfolios over the past 12 months to reflect this potential changing of the tide. After a long period of underinvestment, many of the post-pandemic themes are supportive of a resurgence in industrial activity, particularly in the US.

Conflict vs co-operation, resilience vs efficiency, populism vs planning. These seismic shifts are driving the re-shoring of supply chains, investments in energy security and decarbonisation, and broad-

based infrastructure upgrades to kick-start economic growth and create new jobs.

The Biden administration has already flashed the cash to support its strategic imperatives around energy transition, strategic industries and re-industrialisation. The Infrastructure Investment and Jobs Act, Inflation Reduction Act and Chips and Science Act passed over the last 18 months provide over $2 trillion of spending.

At the corporate level, companies are responding to consumer, government and regulator demand to clean up their acts. Energy transition agendas are for the many, not the few. Against the backdrop of tight labour markets, we are amid a significant transformation in how goods are produced thanks to the digitisation of manufacturing. Technological advancements have made the smart factory a reality, with the adoption of data and machine learning powering autonomous systems making processes more efficient, more productive, and less wasteful.

While the drivers might be different, the characteristics we are looking for remain the same. Competitively advantaged companies, exposed to growing markets, with aligned management teams, bought and held at reasonable valuations. The opportunity set is broader than it has been for some time.

We will delve deeper into this in next quarter’s update given the scale of the opportunities.

2022 – Goodbye and Good Riddance

There will be few tears shed by the investment community over the passing of 2022 and even fewer fond memories. But for all the turmoil it provided a reminder of the need to be adaptable, to build portfolios with resilience and to expect change.

Markets and portfolios begin this year on firmer footing and, while the immediate outlook remains murky, we are confident about longer term returns.

The environment may be changing, we think that the chances are that it is. Even if the new regime proves similar to the old, the opportunities today provide plenty to excite us about the future.

For illustrative purposes only and should not be construed or relied upon as advice.