OUTLOOK 2024: APPROACHING THE FINISHING STRAIGHT?

2023 defied gloomy predictions as markets bounced back from a terrible 2022. Central banks kept to their task, hiking interest rates to over 5% in the UK and US. The continued tightening in financial conditions did not lead to either a much-anticipated recession or much-feared financial accident. To date, March’s failures in the US regional banking system have proven little more than a bump in the road.

Recent communications from the Federal Reserve, Bank of England and European Central Bank suggest that interest rates have not only peaked but will be cut through 2024. Having appeared unlikely for much of the past two years, with inflation continuing to fall and jobs markets robust, Central Bankers appear tantalisingly close to completing a successful slowing of the economy without causing significant collateral damage. This set the stage for a broad-based rise in almost all assets in the final months of the year.

Even following these strong moves, valuations look much more reasonable than two years ago and provide us with a broader set of opportunities across asset classes than for much of the post financial crisis period. With rising tensions between superpowers driving the realignment of global supply chains and a prioritisation of resilience over efficiency the world is more vulnerable to shorter and more volatile economic cycles; a wider range of investments will be essential to smoothly navigate future markets.

Thus far inflation has fallen without higher interest rates crashing the economy. However, the finishing line hasn’t been reached and with inflation still above central banks targets victory has yet to be declared. The last mile is traditionally the hardest and there is plenty of scope for surprises before we chest the finishing tape.

Our view in short

- The first 9 months of 2023 saw economies wrestling with stubborn inflation and rising rates whilst facing hurdles of regional banking failures and a looming debt ceiling crisis in the US.

- Falling energy prices, strong jobs markets and consumers willing to get out and spend kept western economies going even as the manufacturing sector proved moribund. Initial gloomy growth expectations were steadily revised higher through the year.

- Asset markets were in limbo with only a narrow leadership of the largest seven technology companies making headway as enthusiasm for growth, especially in Artificial Intelligence, captured the imagination.

- Outside of technology the broader market and bonds struggled to make headway. Cash was king as rising allocations to money market funds topped $6 trillion,

a record. - Markets shifted gear in the autumn as inflation began to decisively roll over in major markets even as economic growth held firm in the face of higher rates.

- With the peak in rates declared and looming recessionary fears dissipating, confidence returned. Almost all asset markets performed strongly to finish the year in positive territory.

- Commodities, oil and the dollar were the chief laggards, despite tensions in the Middle East.

- Markets are now anticipating a soft economic landing comprising falling inflation, falling rates and resilient growth. Economic growth expectations are low but positive. Companies expect to make steady progress in such a scenario.

- Both bond and equity valuations look reasonable when compared to history and should do well in the softlanding scenario.

- We expect a continuation of the broadening out of equity market performance. Sectors including healthcare and industrials look well placed to benefit.

- The experience of recent years favours optimism but cautions against complacency. The world has proven vulnerable to shocks and both inflation and interest rates are still above the levels of the last 15 years.

- In a bumper year for elections, the polarising nature of candidates will increase uncertainty. However, outcomes are likely to prove more consequential for policy beyond this year.

- We retain a preference for higher quality companies, with balance sheets that afford them resilience and flexibility, in portfolios that are broadly balanced. Many of the structural trends supporting infrastructure renewal and re-shoring of supply chains provide investment opportunities that will transcend whoever leads the next political administrations.

2023 In Review – A sprint to the finish

The final quarter of 2023 saw all asset classes buoyed by the heady combination of resilient growth, falling inflation and a clear signal from Central Banks that the next move in interest rates would be lower. Equities as measured by the MSCI All Companies World Index rose by over 9% in US dollars, although a weaker dollar reduced this return to 6% in sterling terms. The fourth quarter corporate reporting season was broadly supportive and CEOs displayed increasing optimism with mentions of recession at the lowest level in two years.

The shift in direction on interest rates also set bonds moving, with the UK gilt index rallying by 8% over the final three months, taking it into positive territory for the year. The experience was similar in the US Treasury market. In what was a positive environment for equities and animal spirits it was notable that diversifying assets such as gold and hedge funds also made progress; gold reaching a new all-time high in US dollar terms.

There were very few exceptions given the wave of positivity. The most notable being the price of oil, which fell by almost 20% in dollar terms in Q4 despite elevated conflict in the Middle East. Prices fell by more than 10% over the year, providing a fillip to consumers whilst supporting the continued cooling of inflation. The US dollar was the other prominent faller, with the tradeweighted dollar index down 5% as the more dovish signalling from the Fed combined with risk-on sentiment. Dollar weakness this year has been a modest headwind for sterling investors, having been a haven in the turbulence of 2022.

Peering beneath the surface of equity returns the US technology-focused Nasdaq Index led the way, rising by nearly 45% given the dominant returns of the largest seven tech companies from Microsoft to Tesla. Undoubtedly a remarkable year, yet this return merely reversed the rout that saw the index lose a third of its value in 2022.

At the back of the pack, China limped behind broad-based rises across most regional indices – the country’s headline CSI 300 index fell by 9%. A tepid economic re-opening, a rolling property crisis and ongoing tensions with the US weighed on confidence whilst foreign capital and investment continued to exit China at a rapid rate. The UK too lagged given the weakness in oil and the market’s modest exposure to growth sectors such as technology.

Source: Bloomberg/James Ham bro & Partners January 2024. Equities: Global is MSCI AC World Index, US is S&P 500, UK is FTSE All-Share. Bonds: US Govt is BB US Government Conventional Index, UK Govt is FTSE Actuaries All Gilt Index, US Index-Linked is BB US Government Inflation-Linked Index, UK Index-Linked is

FTSE Actuaries UK Index Linked Index. Alternatives: Hedge Funds is HFRX Equal Weight Strategies. Past performance is not a reliable indicator of future performance. Where an investment is denominated in a currency other than the currency of your portfolio, the return may increase or decrease as a result of currency fluctuations.

Economic backdrop – Going for Gold(ilocks)

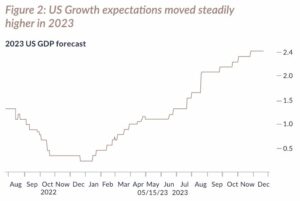

US GDP forecasts troughed in December 2022 and steadily moved higher through the year as pessimism entering the year proved ill-founded. Live estimates forecast that the US economy will have grown by 2.5% in the last three months of the year, slower than in Q3 but still ahead of what most consider its long-term trend potential.

Source: Bloomberg.

With financial accidents having been contained and a recession notable by its absence even as inflation has fallen, confidence has built that policy makers may bring inflation back to their 2% target without causing major damage to the economy. An economic soft landing is increasingly seen as a probability rather than a possibility.

This shift in emphasis is understandable. Inflation has fallen markedly across the US, UK and Eurozone, albeit it is still above long-term targets of 2%. Economic demand, by comparison, has held up surprisingly well in the face of interest rates 5% higher than two years ago. The US economy in particular has proven resilient. Unemployment is low, real wages are rising and there are precious few signs of slowdown let alone recession. Growth in Europe and the United Kingdom has been less impressive but still been better than anticipated as lower energy prices have provided relief to consumers, business and inflation rates.

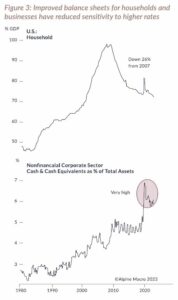

A surprise of this cycle is that both consumers and businesses have proven less sensitive to interest rates than in the past and certainly than during the financial crisis of 2008.

Following a decade of deleveraging, consumer balance sheets are far healthier now, with savings and government handouts accumulated during lockdown providing a further opportunity for people to save or pay down debt. Lower borrowing has meant that higher rates and inflation have not crimped spending power with jobs plentiful and rising wages. Additionally, the US mortgage market offers fixed rates for 30 years and most homeowners took the opportunity post-covid to lock in attractive deals, meaning rising mortgage rates have had little impact on discretionary spending let alone defaults or repossessions.

However, unlike in the UK, US mortgages are not portable. Few are willing to trade a 3% mortgage for an 8% one, so people have simply stopped moving. This has created an unbalanced housing market where existing home sales have slumped to near recessionary lows, leaving those in need of property reliant on a supply-constrained new build market and exposed to ever-rising house prices.

Source: Alpine Macro Research.

Companies, too, took advantage of the ultra-low interest rate environment through COVID to lock in low borrowing costs and extend maturities. This has enabled them to weather the higher rate environment as their interest costs have yet to follow rates higher. With funding costs contained, companies have retained staff and kept unemployment rates near multi-decade lows, providing something of a virtuous circle. Resilient retail spending by consumers continues to confound the doom-mongers.

The other piece of the economic resilience puzzle has been Big Government. We have been writing about the shift from fiscal austerity to fiscal support that has been bubbling under the surface since Trump took the White House in 2016. Tax cuts favoured by the Republicans have since given way to increased spending under President Biden. Having provided emergency COVID support equivalent to more than 20% GDP the US economy has further benefitted from President Biden’s three marquee infrastructure acts and their $2 Trillion of combined spending over the next 10 years. The duration and impact of these policies has been underestimated.

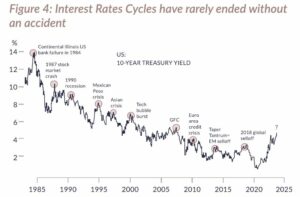

So far so good. Yet it is still too early for a victory lap. Economic wisdom tells us that monetary policy acts with long and variable lags as the impact of higher rates takes time to work its way through the economy; the same could also be said for the fiscal support handed out in 2020 and 2021. It is rare for an interest rate cycle to pass without some form of accident (see frgure 4) even more so given the recent steep trajectory of rate increases on the heels of a decade of cheap financing.

Source: BCA. Past performance is not a reliable indicator of future performance.

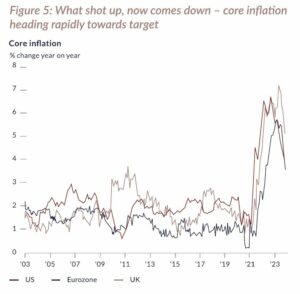

Inflation – Starting to flag

The continued moderation in inflation has emboldened the Federal Reserve to suggest that they will begin to reduce interest rates by 0.75% over the course of this year, aiming to land the economy smoothly having piloted through quite some turbulence.

Source: BLS, Eurostat, LSEG Datastream, ONS, J.P. Morgan Asset Management.

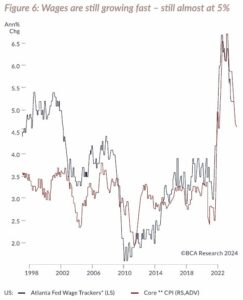

Plenty of progress has been made, but the last mile is likely to be the hardest. US wage inflation is still running above 5% and bringing this down whilst keeping the economy buoyant is the next challenge. Given the blunt tool that is interest rates, to achieve that without raising unemployment will require skilful threading of the needle.

Source: Federal Reserve Bank of Atlanta; shown as a 3-month moving average.

We also know through recent experience that prices are vulnerable to supply shocks and so any surprises, say escalation in the Middle East and with it a broadening out of disruption both to shipping and oil production, could see inflation jump once more. This would leave central banks in an unenviable position where they must keep rates high, increasing the risk of damage to the economy.

Whilst the path to 2% inflation without an economic accident is there, it is narrow. The nature of the postpandemic business cycle has caused forecasters plenty of trouble. The impulse from this year’s surprises will fade. Consumer excess savings are not bottomless, recent fiscal largesse will not be repeated in an election year and economic growth in the major western economies is slowing. With inflation still not beaten, we think it is unwise to go “all in” on a soft landing.

Off to the election races

2024 will be a big year for national elections with 40 nations set to go to the polls, accounting for 40% of the world’s population and a similar proportion of GDP. Throw in the European Council elections and we get to over 50%. While some results look like a slam dunk (anybody think that Vladimir Putin will lose?), others remain firmly in the balance with the US Presidential election looming large in November. With the UK also set to go to the polls by January 2025 at the latest, politics is sure to dominate the news cycle and the minds of shorter-term traders as the year progresses.

Market volatility will increase in the run up to elections but once the results are in the attention turns to the detail. As already noted, government intervention has been on the rise as austerity has given way to fiscal expansion. We do not expect that to change although with debt burdens high there is little room for shock-andawe spending irrespective of who enters Number Ten and the White House.

Whatever the outcome in the US many of the structural themes and spending policies we have been writing about in recent years will remain; they have bipartisan support. Reshoring, deglobalisation and increased strategic competition between China and the US will exert a more material influence on investment returns beyond even the next administration.

As a final thought, data over the last 40 years cautions against placing too much weight on the impact of politics. There has been little correlation between which party has been in power and equity market returns. More meaningful drivers have tended to be the major market or exogenous events such as the GFC, technology bubble or COVID rather than political policy and so it is likely the ultimate path of inflation, interest rates and growth that determine portfolio returns.

Source: FTSE, LSEG Datastream, S&P Global, JP Morgan Asset Management. The shading represents who was in power for the majority of each year. Past performance is not a reliable indicator of future performance.

Bonds – Finding the second wind

A soft-landing scenario would be fine for bonds. Falling interest rates due to falling inflation should modestly push up bond prices and bring down yields (which move inversely to the price). Current yields, which sit above both short- and long-term expectations for inflation, now offer a real return to investors and a reasonable lower risk building block for diversified portfolios. In the unlikely event of a dull year then bonds should deliver us a similarly dull cash-like return. Such an outcome would

be welcome.

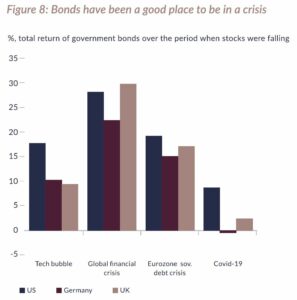

Whilst bonds should do fine in a benign environment, they will do quite well if soft landing turns to recession. Government bonds have a track record of providing investors with good returns in tough economic periods and when financial accidents begin to multiply (See Figure 8). They benefit both from being a safe harbour in choppy seas and an increasingly attractive lower risk

return as policy makers rush to cut interest rates.

Source: Bloomberg & JP Morgan Asset Management. Past performance is not a reliable indicator of future performance.

For much of the past decade the traditional dual attractions of bonds – income and diversification in the event of a deteriorating economy – have steadily diminished. After the challenges of the past two years, we believe the role of bonds in multi-asset portfolios has been restored and once again deserves its place within a diversified portfolio.

Equities – A broadening field of potential winners

The prevailing economic consensus of inflation under control, falling interest rates and continuing economic growth would provide a fertile environment for equities to continue their recent run; particularly those companies of a more cyclical persuasion.

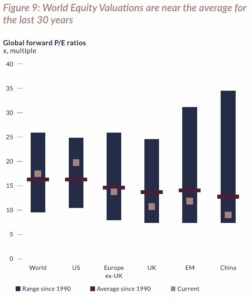

Economic progress would support earnings whilst falling rates provide support to starting valuations that already look reasonable, being at or near the average over the last thirty years or so (Figure 9). The US is the only major market that looks a little on the expensive side, due in large part to the drivers of the market growth last year.

Source: FTSE, IBES, LSEG Datastream, MSCI, S&P Global, J.P. Morgan Asset Management. MSCI indices are used for World, Europe ex-UK, EM and China. UK is FTSE All-Share and US is S&P 500. Earnings data is based on 12-month forward estimates. Past performance is not a reliable indicator of future performance.

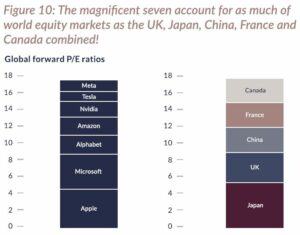

As has been well reported by us and others, market leadership was narrow in 2023. Returns were dominated by the ‘magnificent seven’ technology companies: Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta and Tesla.

Whilst these are excellent businesses that are exposed to many of the most exciting growth opportunities (we own several of them and have done so for years), we do not expect a similar level of outperformance in 2024. The forward Price to Earnings ratio (a measure of valuation) of this group moved from 18x at the start of 2023 to 31x at the end. In contrast to 12 months ago expectations are high leaving little room for error.

These seven stocks now account for over 30% of the S&P 500 and have a combined market capitalisation that exceeds that of markets representing five of the largest economies outside of the US.

Source: LSEG Datastream, Schroders. Past performance is not a reliable indicator of future performance.

Whilst this in itself does not mean these companies are destined to disappoint, it does point to the likelihood that a wider group of companies and industries will assume the running this year, particularly those more sensitive to benign economics and interest rates.

Previous precedents of highly concentrated markets suggest the current levels of crowding are rarely sustained (Figure 11). Given the prospective economic climate, we think 2024 will see successful returns from a broader selection of companies than those that led last year.

Source: Kenneth R. French Data Library and the Center for Research in Security Prices (CRSP).

With the rolling impacts of COVID fading, we see exciting opportunities in companies and industries exposed to the range of structural trends that we have written about in previous quarterly letters.

Healthcare companies have suffered from a hangover following the revenue bonanza created by COVID. However, with supply and demand returning back to trend, we can now return to the clear structural drivers propelling the industry. Ageing populations in the developed world and increasing spending on healthcare in developing countries provide strong foundations for the industry. Innovation, analysis, data and Al are opening new frontiers which provide a wealth of opportunities for growth. Having been at the bottom of the pile in 2023, we expect to see our investments in life sciences, medical technology and drug discovery prosper. The industry has the added attraction of being insulated against the vagaries of economic cycles.

Alongside the current fiscal impulse, the established trends towards re-shoring, a strategic imperative to strengthen the resilience of supply chains and investment in creaking core infrastructure will continue to support long-term growth across industrial end markets. We expect to see further spending on capital and renewal that is long overdue after decades of underinvestment. Al cannot build roads, semiconductor factories or renew the energy infrastructure (although it could make it

more efficient).

Which brings us to last year’s runaway winner? Artificial intelligence and machine learning are real and being embraced by businesses; they have the power to expedite digital transformations that have been underway for years, to enhance productivity and efficiency whilst opening potential new opportunities. Al will move beyond those directly manufacturing the equipment to those that can effectively harness and embed the power of this technology in their businesses. The most forward looking and dynamic management teams will lead the way.

Source: Bloomberg/James Ham bro & Partners. Data as at January 2024. MSCI ACWI Sectors. Past performance is not a reliable indicator of future performance. Where an investment is denominated in a currency other than the currency of your portfolio, the return may increase or decrease as a result of currency fluctuations.

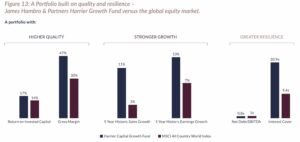

Long the strong – Form is temporary, quality is permanent

With the shifting tectonic plates of geopolitics having reversed the trend for global co-operation, there has been a tangible shift in national and corporate priorities. The increasingly unpredictable nature of cycles and growing vulnerability to external shocks has meant that security and resilience are now prized ahead of efficiency. Forecasting the outlook is tougher than ever. The best defence in such an environment is a relentless focus on quality in everything we own and diversification across a broader range of asset classes and sectors than for many years.

High quality businesses, those that earn high returns, benefit from competitive moats and have the balance sheets to keep going whatever the economic gods throw at them will win out in the end. Aligning that inherent quality with sensible diversification provides the resilience to stay in the race and make sure that we are there competing for medals as we approach the finishing line.

Harrier Capital Growth Fund holdings based upon the underlying companies owned as at 30th November 2023 which represented over 0.1% of the Fund’s equity allocation. The data is inclusive of both direct exposure from individual equities help and indirect exposure from third-party investment funds held. Figures shown are the weighted average of the relevant companies within the Fund or MSCI AC World Index, except ND/EDITDA and Interest Cover which are median figures. Where company data is unavailable, those companies have been excluded from the relevant calculation. MSCI AC World Index sales and earnings growth is on a calendar year trailing basis. Past performance is not a reliable indicator of future performance.

Article written by James Beck, Head of Investments

For illustrative purposes only and should not be construed or relied upon as advice.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.