THERE’S MORE TO MARKETS THAN TARIFFS AND AI

The View in Short

Policy Shifts and Market Dynamics

2025 was a year of headline comebacks and resilience. Despite significant disruption and a deepening trade conflict, global markets and economies displayed remarkable resilience. Feared recessions and inflationary surges did not materialise, and most markets made progress.

Narrow Leadership, Broader Risks

Equities delivered another strong year, led by surging AI data centre investment. However, market performance was narrow. Fewer than one in three US stocks outperformed the S&P 500 while quality stocks saw their sharpest underperformance in decades. Yet there are good reasons to expect a broader range of opportunities ahead.

Governments Turn Up the Heat

Western governments have responded to electoral dissatisfaction and political challenges by upping fiscal stimulus. The One Big Beautiful Bill Act will inject $200-300bn into the US economy, benefiting consumers and businesses. Trade policy uncertainty is easing, deregulation is boosting banking activity and interest rates are falling across most developed economies.

International Opportunities

For the first time in years, international markets outperformed the US. Europe is loosening fiscal policy, especially in Germany, and encouraging defence spending. Japan is pursuing aggressive stimulus under new leadership. The World Bank forecasts global growth of around 3%, with potential upside.

Broader Earnings Growth

Given supportive fiscal and monetary policy, corporate earnings growth is expected to exceed 10% across major regions. Technology will continue to lead, but wider market participation is expected.

Emerging Markets and Asia

Asia and emerging markets were the best performers in 2025, shrugging off trade turmoil to post strong gains. The region benefits from attractive demographics, a huge potential consumer base and a shift toward intra-Asian trade. Valuations remain attractive.

Artificial Intelligence – Still Centre Stage

AI continues to shape market dynamics, especially in the US, where the largest companies now represent over 40% of the index. While concerns about overvaluation persist, investors are becoming more discerning. The sector’s scale and investment level remain the key risk to markets, especially should Nvidia or OpenAI disappoint.

Central Banks, Inflation, and Gold

2026 will see the end of Jerome Powell’s tenure as Fed Chair. With the next appointee expected to favour lower rates as the president wants, further cuts into a buoyant economy could reignite inflation, which remains above target. Against this backdrop, gold has delivered extraordinary performance, rising over 60% in 2025 and outperforming even tech-heavy indices.

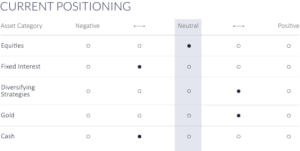

Outlook and Portfolio Positioning

Fiscal stimulus, stable inflation and falling interest rates supportive for company earnings and the outlook for equities. After several years of narrow returns we expect both company earnings and market performance to broaden across sectors and regions. However, with valuations elevated markets will remain vulnerable to shocks, especially in the short term. Balancing and diversifying assets, such as high-quality, short-maturity bonds and gold, look best placed to provide protection against market risks.

DON’T LOOK BACK IN ANGER – AT LEAST NOT TODAY

2025 was defined by two hotly anticipated comebacks, both featuring headliners renowned for their uncompromising and confrontational styles.

Whether the focus was on the return of Oasis to global stadiums or of Donald Trump to the global stage, expectations were for a blockbuster year. Neither comeback disappointed.

The real drama was of course in US policy, with the incoming administration providing a level of market theatre that matched the scale of any world tour. For investors and spectators alike, 2025 proved that in both politics and rock-and-roll, the appetite for a high-stakes revival remains undiminished.

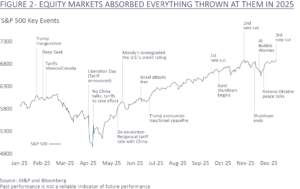

In amongst the upheaval of ”Liberation Day” and the upending of conventional international relationships, perhaps the most remarkable outcome was the resilience of the global economy. Asset markets remained strikingly robust in the face of this bull market in uncertainty and disruption. All major asset classes rising, with the exception of the US dollar which has proven the escape valve for international concerns about the US.

As we move into 2026, we anticipate more of the same. Reasons for caution abound, including bubble risks in AI, simmering geopolitical tensions fuelled by imperialist ambitions and markets trading near historic peaks both of price and valuation. However, there are equally compelling grounds for optimism. Historically, major market reversals rarely occur in the absence of a recession, rising rates or a credit crisis. There are few signs of any of these today.

With both fiscal and monetary policy now calibrated to provide further economic stimulus, conditions are in place to allow market gains to broaden beyond the narrow technology leadership of recent years. The main risk for the year ahead may not be one of economic cooling, but of overheating. Should economies run too hot, we may see a resurgence of inflationary concerns as we approach the latter part of 2026.

THE STATUS QUO ROCKED ALL OVER THE WORLD

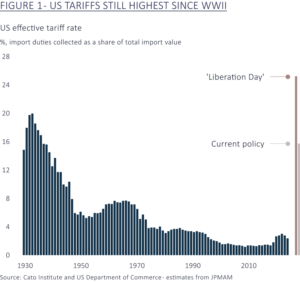

The global reverberations of the Trump Presidency have been profound, arguably unmatched outside of wartime. The shock announcement of Liberation Day’s reciprocal tariffs and the reassessment of NATO obligations forced an immediate revision of defence strategies, trade routes and fiscal frameworks. While initial tariffs have since moderated, they remain at levels not seen since the pre-war era.

The introduction of DOGE, expansion of ICE mandates and a pivot toward transactional foreign policy have dismantled conventions that had underpinned US policy for decades. In many respects, the shift toward governing by decree has surpassed even the most radical forecasts.

Given this context the most notable feature of 2025 was what didn’t happen. Despite colossal disruption and a deepening trade conflict between the world’s leading economic powers, global markets and economies displayed remarkable resilience. The year was not without trauma – April saw a visceral reaction to US tariffs and Beijing’s uncompromising response – yet most markets made respectable progress by year end. Crucially, the world avoided both the recessions and inflationary surges that many feared tariffs would prompt.

A GOOD YEAR, BUT NOT FOR DIVERSIFICATION

Equities delivered another strong year, supported by corporate earnings growth of nearly 10%. At the vanguard, the US hyperscalers (Microsoft, Meta, Alphabet, Amazon and Oracle) remained largely insulated from the tariff chaos. Their profits continued to climb, as did their spending.

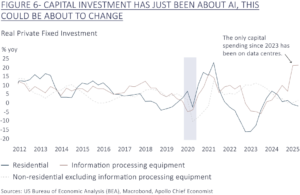

Investment in data centres and artificial intelligence surged from $250 billion in 2024 to $400 billion in 2025. It could exceed $600 billion for 2026. This spending provided valuable economic fuel, contributing nearly half of US growth.

With AI and tariffs the dominant narratives, the US equity market was characterised by increasing concentration and narrow performance. For the third consecutive calendar year, fewer than one in three US stocks outperformed the S&P 500. When considering cumulative returns over the past three years that figure drops to only one in five. These are levels not seen since the dot-com era. This dynamic has tested disciplined active investors; sensible portfolio diversification and risk management has offered few rewards in the short term.

This narrow dominance was not purely a US phenomenon, though the drivers differed sharply across the Atlantic.

Whilst the US market was propelled by the AI capex explosion, in Europe defence and banks led returns. In a world beset by confusion investors latched onto what they thought they knew for sure. Spending on defence in Europe and data centres in the US looked likely whatever the political weather, whilst higher rates have helped banks after a decade in the sin bin.

As a result, many companies and sectors have been either ignored or filed in the ”too difficult” drawer. Software companies have swung from AI winners to AI losers.

Manufacturing and industrial firms not tied to the data centre supply chain have effectively been in recession for three years, with any nascent signs of recovery snuffed out by the uncertainty of tariffs. Healthcare, still digesting a post-pandemic overhang, was forced to grapple with the unpredictable decisions of a US Health Secretary who appeared determined to denounce science. Meanwhile, consumer stocks have found themselves squeezed on one side by new obesity treatments curbing appetites and on the other by low-income consumers facing an affordability crisis more acute than headline inflation suggests.

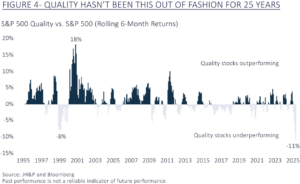

Most notably, ‘Quality’ as an investment style has struggled. These businesses, typically core portfolio holdings, are characterised by high returns on capital, robust balance sheets and an ability to provide resilience and growth throughout the economic cycle. In 2025, they experienced their sharpest underperformance in two decades.

In short, it has been a challenging period for investment approaches built on the principles of quality and diversification. We are confident the rationale and principles that underpin an approach of owning a portfolio broadly diversified by company, sector and region will endure, even if they failed to be captured by the zeitgeist of 2025.

We see compelling reasons why earnings and sentiment towards neglected market areas can improve this year and lead to a much broader range of opportunities. The policies and foundations are already in place.

GOVERNMENTS ARE DIALLING UP THE TEMPERATURE

“populus… duas tantum res anxius optat, panem et circenses” (the public… longs eagerly for just two things, bread and circuses) – Juvenal

Much as the emperors did in the fading days of the Roman Empire, Western governments have responded to post-pandemic inflation and populist unrest with short-term fixes and direct fiscal interventions. The era of austerity has decisively ended to be replaced by one of fiscal activism and largesse more suited to an age of populism. Nowhere is this more evident than in the US, where mid-term elections in November create every incentive for the Trump administration to ”juice” the economy.

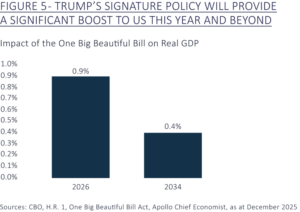

Trump’s signature One Big Beautiful Bill Act (OBBBA) is set to inject an estimated $200-300bn of stimulus into the economy through 2026. The Congressional Budget Office estimate it could add nearly 1% to US growth in 2026 and sustainably raise growth projections for future years.

Measures within the OBBBA targeting lower earners, such as removing taxes on tips or overtime, alongside White House proposals to send cheques of as much as $2,000 directly to consumers as a ”tariff dividend” could help address the increasingly uneven consumer spending picture in the US. Tax rebates of up to $150 billion should hit consumers’ pockets from February.

Businesses are set to benefit from policy changes intended to lower taxes and incentivise capital investment. With trade policy uncertainty easing and interest rates falling, broadening corporate capex should begin to share the load alongside still robust AI-related spending.

Deregulation is also set to boost business activity and reduce economic friction. Treasury Secretary Scott Bessent is keen to liberate US banks to increase lending, mortgage reform is touted to reinvigorate housing and a more relaxed attitude to dealmaking has unleashed corporate animal spirits. The value of mergers and acquisitions (M&A) rose by 50% to $4.5 trillion in 2025, with nearly 70 deals valued at $10 billion or above; good news for sentiment, investment and Wall Street bankers.

Finally, US interest rates have fallen by almost 2% since September 2024. Lower borrowing costs should feed through to the wider economy, amplifying the impact of other pro-cyclical measures. The overall picture looks good.

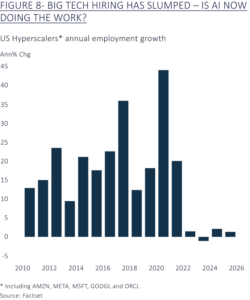

The main challenge to this bullish backdrop is employment, which has looked fragile since the middle of last year. For now, this reflects cautious hiring rather than widespread layoffs. Many companies have put expansion on hold given the crosswinds of tariffs whilst the rate of hiring by big tech companies has materially slowed – perhaps indicating a ground zero for the productivity-based gains expected from AI. With government employment also undermined by the legacy of Elon Musk’s DOGE and November’s shutdown, recent employment weakness still looks more specific than systemic. It will be closely watched.

IT’S NO LONGER JUST ABOUT AMERICA

While US technology giants underpinned continued stock market momentum, for the first time in years returns across Europe, Japan, and Asia outpaced those of the S&P 500, driven by attractive relative valuations, regional stimulus and low investor exposure.

The story of fiscal activism, lower rates and deregulation extends beyond the Stars and Stripes. Germany has committed to breaking its self-imposed shackles of fiscal conservatism in the face of the threat of rising militarism to the east, a manufacturing and automotive base under sustained assault from China and swelling support for the brazenly right wing AFD. Its construction sector grew in December for the first time in four years.

Much of the rest of Europe remains burdened by stricter fiscal and political constraints, but governments are doing all they can to avoid tightening fiscal policy at the very least, as was even evident in the much maligned Labour Budget late last year. Increased defence spending could have a wider economic halo effect that inspires research and development and passes through to other industries.

European interest rates have fallen to 2%, and banks are being encouraged to rationalise domestically. Were this to be allowed to extend beyond national borders then we could see a further boost for the EU. Progress in Ukraine and a resurgence in consumer and infrastructure spending would further support growth.

Japan, under new leadership, is embarking on an aggressively stimulative approach to drive private sector growth and invest in strategic sectors. Whilst this has implications for inflation, Japanese rates and the Yen, it provides a clear driver of reflationary growth.

The IMF and World Bank expect the world economy to grow at a rate of around 3%, consistent with that seen in 2024 and 2025. They have underestimated the world in recent years and so, barring another helping of foreign policy shocks, it could easily surprise to the upside.

A RISING TIDE AT LAST FOR MOST BOATS?

With both fiscal and monetary policy set in growth mode, prospects for corporate earnings look promising. Data from JPMorgan Asset Management points to a global acceleration in earnings, with growth forecast to exceed 10% in all major geographies this year. The acceleration will be most pronounced in Asia and Europe.

A similar picture is emerging at a sector level. Technology companies are expected to continue growing profits at a healthy clip of near 20%, but the wider market should begin to catch up as a broader range of companies benefits from improved economic conditions and reduced trade uncertainty. With many of these companies looking cheaper than the technology sector and investors looking to diversify beyond AI, this bodes well for share prices.

Alongside a resurgence in more cyclical areas, we see increasing opportunities in some sectors with more defensive credentials, particularly the healthcare space. The sector’s attractions are clear. With structural growth drivers of ageing societies and growing wealth in emerging markets combining with the industry’s long history of harnessing research and technology, AI offers obvious opportunities. Following post-Covid sector struggles, valuations are appealing just as many of the headwinds are diminishing. We are reviewing several potential investments across the space, given the attractive balance of growth and economic resilience.

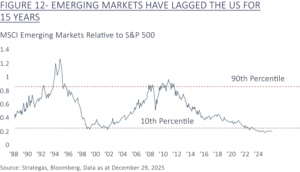

THE EMERGING OPPORTUNITY

Asia and Emerging Markets surprised many by proving the best performing equity regions in 2025, shrugging off trade turmoil to post strong gains. We added steadily to the region from mid-April and still see substantial opportunity, especially compared to Europe where the political and structural challenges are more complex. There are both cyclical and structural reasons to be more constructive on the region.

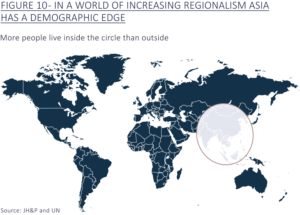

As the world continues to polarise into spheres of influence, Asia and Emerging Markets possess structural advantages: attractive demographics, a huge potential consumer base with over 800 million millennials, plentiful resources and a vibrant mercantilist culture. Their populations are less encumbered by regulation which provides a dynamism and willingness to embrace technological progress (where they can afford it) without the weight of legacy embedded systems and infrastructure.

China’s push up the industrial and technological value chain is reducing Asian reliance on US leading edge innovation. This is increasingly evident in its dominance of clean energy and Electric Vehicles, where BYD has surpassed the auto sales of Tesla, alongside enormous progress in advanced industrial automation and chip manufacturing. Not forgetting AI where DeepSeek was no flash in the pan and where we have seen animal spirits alive in the Hong Kong market, with app developers such as Minimax and Zhipu floating in Hong Kong this year. Asia could be the ultimate AI winner!

Intra-Asian trade is growing and will become increasingly important in a multi-polar world, making Asia less reliant on the fortune of Europe and the US. Indeed, should the West re-industrialise as Trump wishes, Asia could become more important to the US than the US is to Asia.

In the near term, the cyclical opportunity has been boosted by a weaker US dollar, low oil prices and falling rates. These trends look set to continue, while tariff noise is diminishing and reliance on the west moderating as trade is becoming increasingly regional. When set alongside more reasonable valuations and modest ownership amongst global investors Asia offers attractive balance against the US.

With Asia alone accounting for half the world’s people, nearly 50% of world GDP but only 10% of the MSCI World Index, we would expect that gap to narrow. The opportunity for emerging markets to catch up is clear.

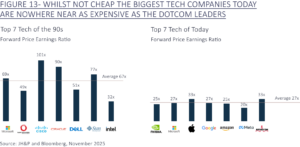

ARTIFICIAL INTELLIGENCE – STILL HOGGING THE HEADLINES

AI’s sheer scale means it is impossible to ignore. Last quarter, our view was that while sentiment and valuations appeared stretched, a setback seemed more likely than a full-blown bubble bursting. So far, that assessment has held true.

Alongside the recent cooling of the AI narrative, we have noticed a growing differentiation in how technology companies and those exposed to AI are treated by the market. Investors appear increasingly discerning about relative risks. Last quarter’s results saw a very different response from Alphabet and Meta, the former rising 3% and the latter falling by more than 10% despite both growing sales by over 15% on the previous year.

Debate now centres on the scale of capital expenditure, the means of financing such spending, and the prospects for meaningful returns. There is also a degree of caution around the circular nature of contracts and the spectre of vendor financing, with OpenAI at the heart of the ecosystem. Scepticism is building as to when (if?) OpenAI will become profitable.

This is understandable given the bold predictions from OpenAI’s CEO Sam Altman and the company’s staggering capital spending commitments of over $1 trillion into the next decade. With 2025 revenues estimated at $13 billion and projected losses of $9 billion, the road ahead is long. Transparency remains limited, though a potential stock market flotation could shed more light. Having been valued at $500 billion in October, OpenAI is rumoured to be seeking a valuation closer to $1 trillion later this year.

The memories of the dot-com bubble still loom over investment markets, even if for many the lessons are gleaned from history books rather than early-career PTSD. This alone may keep broad stock market enthusiasm contained. Scepticism about OpenAI is, in many ways, a healthy sign that sentiment has not detached from reality as it did at the peak of previous bubbles.

Whilst both valuations and leverage are far below the extremes of 1999/2000, borrowing is on the rise, and those taking on more debt, such as Oracle and Meta, have fared less well.

The question of returns on all this investment remains unresolved. Recent research cited in the Financial Times suggests annual revenue of $650 billion would be needed to deliver a 10% return on current announced AI investment. This is a huge sum but not impossible in the context of $1.6 trillion of revenues earned by Microsoft, Alphabet, Amazon Meta and Oracle, which have grown at 14% per annum over the last decade.

As with any technological revolution, it is impossible to predict who will ultimately profit from AI. The sector is still in its early stages, and the landscape is evolving rapidly. There is a strong argument that companies harnessing AI within their existing businesses may derive longer-term benefits in productivity and profitability than the AI labs building and training the models. Machine learning and AI could have profound implications for industry if applied alongside robotics and automation – with only 177 industrial robots for every 10,000 employees there looks to be huge scope for growth and efficiency.

WE NEED TO TALK ABOUT KEVIN(S)

May 2026 will bring the end of an era as Jerome ”Jay” Powell’s likely tenure as Chair of the Federal Reserve draws to a close. Originally appointed by Donald Trump, Chair Powell has in recent years become a subject of the President’s ire for not cutting interest rates quickly enough.

What might once have been a routine transition of interest only to economists and market wonks (such as us), in true Trumpian fashion has acquired a new sense of jeopardy and spectacle.

The two frontrunners are both Kevins: Kevin Warsh, a seasoned Fed insider and former adviser to President George W. Bush, and Kevin Hassett, who served on the National Economic Council and advised Trump during his first administration. Regardless of their pedigrees, the principal qualification for the role appears to be a willingness to deliver what the President wants: lower interest rates, at least in the near term.

This creates two risks. First, markets are aware of the brief of the incoming Chair and are likely to test their resolve and challenge their independence. This could lead to turbulence in bond markets over the summer. Second, and perhaps more importantly, is the risk of stoking inflation.

Since the post-COVID spike, inflation has settled at a higher resting heart rate than we saw in the previous decade. A year ago, consensus expected inflation to have drifted back towards 2% by now, yet it remains stubbornly close to 3%, even with oil prices subdued. Despite this, longer-term inflation expectations remain anchored, with market pricing only just above the Fed’s 2% target. The Federal Reserve’s own projections see inflation falling back in 2026 and reaching target in 2027.

However, with policy firmly set to growth mode and the prospect of further rate cuts under new leadership, there is a real risk that inflation could begin to inflect upwards once again. With the economy already performing robustly, and expected to heat up further, additional monetary easing could pour fuel on the fire and ultimately lead to much higher interest rates down the line. There is a strong argument that policy is already more accommodative than warranted.

Given the backdrop of government deficits and elevated asset prices, a return to the rising inflation, rising interest rate dynamics of 2022 is the most meaningful risk for multi-asset investors to monitor.

GOLD – NOW THE EVERYTHING HEDGE?

Once seen as a relic of the past, gold’s performance over the past few years has been extraordinary. Following a 60% rise in 2025, the yellow metal has now returned over 30% annualised since the start of 2023, outperforming even the US tech-heavy NASDAQ equity index during an AI investment boom.

Gold’s attractions are clear. With inflation proving stickier than expected and policymakers seemingly content to err on the side of stimulus, the risk of a renewed inflationary pulse looms large. At the same time, ballooning government deficits and the prospect of further monetary easing have cast a shadow over the reliability of government bonds as a hedge against market stress. The old certainties, where bonds reliably offset equity risk, have been called into question, leaving investors searching for alternatives.

Geopolitical tensions, too, have added to gold’s lustre. In a world where alliances are shifting and the rules of engagement are being rewritten, gold’s status as a store of value and a hedge against uncertainty has rarely looked more relevant. For investors seeking resilience in the face of the unknown, gold’s recent performance is a timely reminder that sometimes, the oldest solutions are still the best. It remains a core holding across multi-asset portfolios.

DIFFICULT NOT TO BE CONSTRUCTIVE, IMPOSSIBLE NOT TO WORRY.

So where does this leave us? The economic conditions and expectations for corporate profit growth continue to look supportive. Given a mix of solid economic prospects, stable inflation and falling interest rates, allied to a generational technological advance, the case for further growth from equity markets looks well supported.

What is more, with the drivers of markets in 2025 having been incredibly narrow there is a compelling reason to believe that a wider range of businesses and industries will deliver attractive earnings growth and stock returns this year. With investors prepared to consider and reward opportunities outside of the US, we see conditions as ripe for a far more balanced portfolio return.

Technology will remain an important component for markets. There are pockets of excess in AI and capital will be destroyed but we do not view the conditions in place that characterise an extreme bubble. We will see ongoing profit expansion from the largest names but there is scope for attention to move towards those who harness machine learning and artificial intelligence from the current focus on those helping to build the infrastructure. We expect to hear a lot more about robotics, automation and productivity in 2026.

Tempering this enthusiasm are valuations which have marched higher in recent years and are undoubtedly expensive as compared to historical averages. This leaves markets vulnerable to shocks, which could come from a wealth of sources given the step change in global tensions and unpredictable nature of policy. A resurgence in inflation sits high on our watch list, not because of its likelihood but because of its capacity to create widespread disruption across geographies and asset classes.

The best way to balance these tensions is not to reduce our exposure to growth, where we are maintaining strategic exposure to equities. It is to ensure that our balancing and diversifying assets are truly capable of providing protection against market risks. That is why we are keeping our bond exposure both of the highest quality and short maturity and is why gold remains an important asset in portfolios even after its substantial moves in recent years.

Article written by James Beck, Partner, Head of Investments.

This document is a Financial Promotion for UK regulatory purposes and is directed only at investors resident in the United Kingdom.

This document does not constitute investment advice or a recommendation.

Past performance is not a reliable indicator of future performance. The value of investments, and the income from them, may go down as well as up, so you could get back less than you invested.

This material has been issued and approved in the UK by James Hambro & Partners LLP, which is authorised and regulated by the Financial Conduct Authority and is a registered investment adviser of the Securities and Exchange Commission. It is listed in the Financial Services Register with reference number 513246. James Hambro & Partners LLP is a limited liability partnership registered in England & Wales with number OC350134 and registered office at 45 Pall Mall, London SW1Y 5JG. A list of members is available on request. The registered mark James Hambro® is the property of Mr J D Hambro and is used under licence.