12.10.2018

Market commentary Q3 2018

John Langrish, Chief Investment Officer

“Let’s Make America Great Again“ – Ronald Reagan’s presidential campaign slogan, 1980

By John Langrish, Chief Investment Officer

Ronald Reagan was elected in November 1980, after conducting his campaign against a backdrop of domestic economic malaise, the Iranian hostage crisis and a deteriorating relationship with the Soviet Union. After a series of energy crises during the 1970s, America was suffering from low growth, high interest rates and rising unemployment, whilst attempting to maintain its global hegemony. Reagan implemented a series of sweeping tax cuts and initiatives, to stimulate the economy, as well as reigning back government intervention and increasing military expenditure by over 40%, under his ‘peace through strength’ doctrine. The ‘Reagan Revolution’ between 1981-1989 saw US annual economic growth accelerate to average 7.5%, unemployment drop to 5.4% from a peak of 10.8% and interest rates fall dramatically, after reaching a scarcely credible 20% in the early 1980’s.

Reagan was the first President since Dwight Eisenhower to serve consecutive terms and by the end of his tenure he had re-invigorated US pride and morale, restored faith in the ‘American Dream’ and overseen the imminent collapse of the Soviet Bloc, while following an ideology of American exceptionalism: the belief that the US has a unique role to play in world events. Despite almost tripling the national debt through budget deficits and overseeing an increase of wealth inequality, his approval rating when he left office was only previously matched by Franklin Roosevelt.

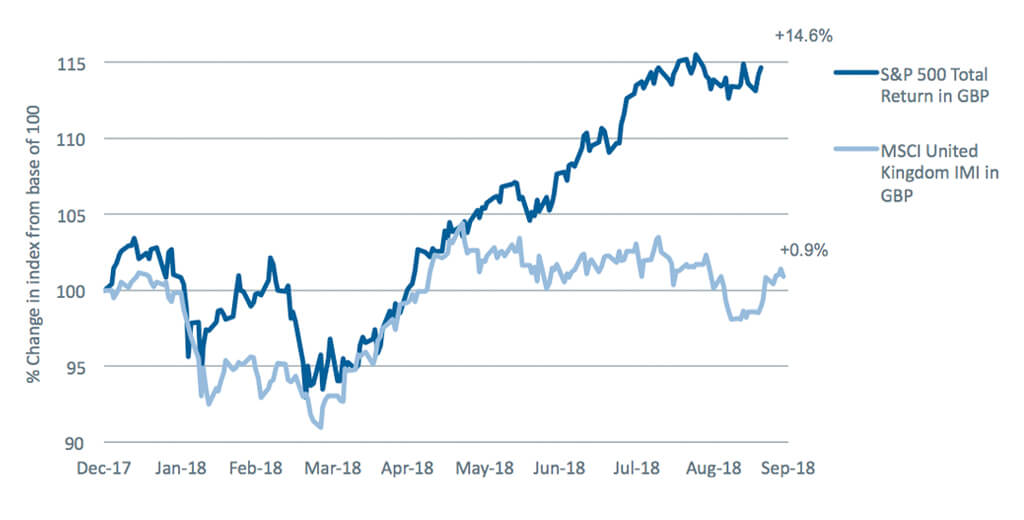

Current US President Donald Trump adapted Reagan’s campaign slogan to a shortened ‘Make America Great Again’, and often cites the current strength of both the US economy and stock market as vindicating his policy-making prowess. The S&P 500 equity index has just delivered its best quarterly return since the final quarter of 2013, rising by 8% in dollar terms, bolstered by surging company results, and is ahead by 10.5% in the current calendar year to the end of September. This strong performance is even more pronounced for a UK-based investor, boosted by a weaker Pound, as Figure 1, below shows. The dark blue line signifies the leading S&P 500 equity index, up by almost 15% in sterling terms this year, whereas the light blue line shows the UK stock market has returned less than 1% in the year to end-September. Even before Trump’s election, we had long regarded the US as representing the best fully-functioning developed economy, but the 2017 tax cuts and one-off repatriation of overseas earnings have accelerated the upward trajectory, encouraging company management to re-invest into their businesses and increase share buy-backs; there have been 4.4 trillion dollars of these since the Great Financial Crisis and they now exceed the value the Federal Reserve’s asset purchases. Revisions to US corporate earnings have been stronger than rest of the world’s, leading to a more optimistic view of the underlying American economy and reinforcing a favourable outlook for the dollar.

Figure 1. 2018 US and UK equity market performance, total return in GBP

Source: Bloomberg, 04/10/2018

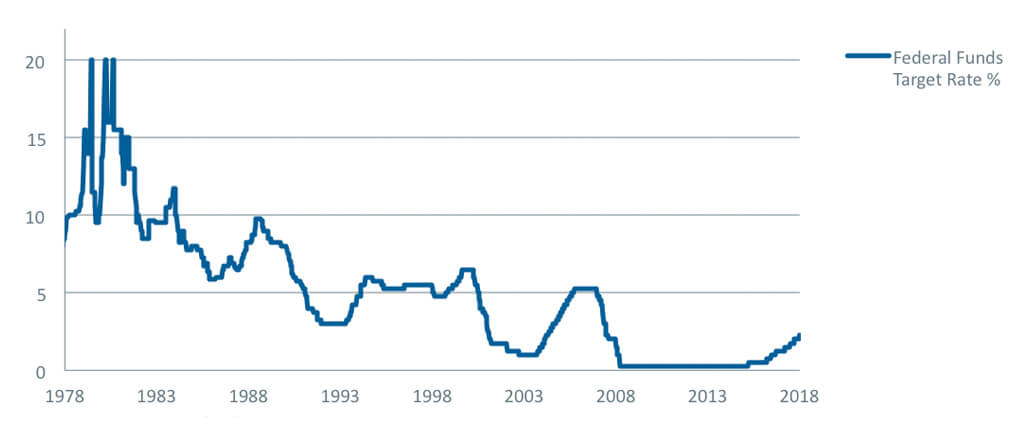

Politics have become a key determinant of investment returns. Aside from America, equity returns in 2018 have been fairly lacklustre, with Japan an exception. The Japanese market has returned 5% this year for a sterling based investor, but much of this was post Shinzo Abe’s re-election in September as the ruling Liberal Democratic party’s leader. By extending his term by another three years, he will be the longest ever serving Prime Minister of Japan and investors have welcomed the political stability and continuation of reform. Meanwhile, there have been negative returns this year from Asia Pacific excluding Japan and emerging markets that have borne the brunt of escalating trade wars and capital flight from countries overburdened by dollar debt. It has certainly become more expensive to service this debt, with the US Federal Reserve recently increasing interest rates for the eighth time this cycle, albeit only to 2.25%, way below the levels witnessed during the Reagan era (see Figure 2). Some commentators have even talked of a ‘weaponised dollar’ being utilised to inflict punishment on countries that have run up large trade surpluses with the US. Propping up the table of investment returns this year are Continental Europe and the UK, depressed by relatively weaker economies, corporate earnings and the continuing confusion around the Brexit end-game. The latter is a significant headache for us and other investors, due to the highly uncertain outcome, so our preference has been to avoid companies that are too highly dependent on the domestic economies of mainland Europe and UK. We will communicate more on our thinking soon.

In China, President Trump arguably faces a much tougher competitor to US leadership than the Soviet Union did to Reagan. Whereas the Soviet economy was fatally weakened by the significant escalation in Cold War military expenditure, China today is in a far better shape to withstand pressure from the US, both militarily and economically. It has responded to recently imposed trade tariffs by a classic policy response of allowing competitive currency depreciation and already exports twice as much to its immediate trading partners than it does to the US. We are watching for further Chinese stimulus measures. For now, America may be satisfied with a moderation of its Asian rival’s growth, but it seems difficult to imagine any long term setback to China’s increasing ambitions on the geopolitical stage.

Near-term, any increased rhetoric and retaliation could slow global growth, just as the Federal Reserve continues to hike interest rates and inflationary pressures gradually mount. These are not just a reflection of rude economic health and quickening wage growth, but also due rising energy prices, with Iran and its oil supplies also firmly in Trump’s cross-hairs, just as they were for Ronald Reagan during his presidency.

Figure 2. US Interest rates 1978 – 2018

Source: Bloomberg, 04/10/2018

Posted on 12 October 2018

You should not act on the content of this market commentary without taking professional advice. Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made of given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions.

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. Fluctuations in interest rates may affect the value of your investment. The levels of taxations and tax reliefs depend on individual circumstances and may change. You should be aware that past performance is no guarantee of future performance.

Image: iStock