04.05.2021

Market timing and life after lockdown – Q1 report

James Beck, Partner, Head of Investments

“When it comes to market timing there are only two sorts of people: those who can’t do it, and those who know they can’t do it. It is safer and more profitable to be in the latter camp.” Terry Smith, Fundsmith

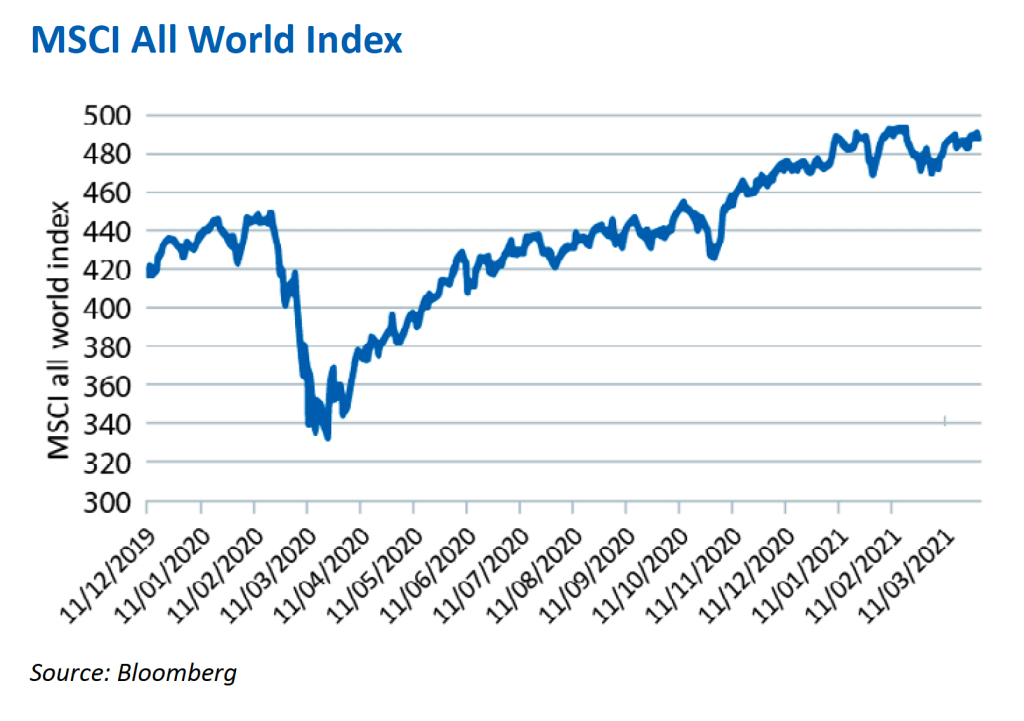

Market returns in the last 12 months are evidence enough of the cruelties they can inflict in short periods of time and the dangers of trying to time investments. It was on 23rd March 2020 that Boris Johnson announced, “from this evening I must give the British people a very simple instruction – you must stay at home”. Remarkably, it also proved the day that the equity market bottomed having fallen 33% from the peak of 12th February just five weeks earlier; beginning a 76% recovery, and taking markets 16% above pre-Covid highs.[1] Never has the saying “buy the rumour, sell the news” been more appropriate, or perhaps in this case “sell the rumour, buy the news”.

Market timing

Making consistent long-term returns in the stock market is predicated on a required level of patience; shorten your investment horizon and lower your chances of success. As the legendary investor Sir John Templeton said, “Ninety-nine percent of investors shouldn’t try to get rich too quickly; it’s too risky. Try to get rich slowly.” As stewards of our clients’ capital, it is our responsibility to ensure our clients’ expectations are aligned with the realities of investing in markets. “The historical odds of making money in the US markets are c. 50/50 over one-day periods, 68% in one-year periods, and 88% in 10-year periods, and (so far) 100% in 20-year periods”.[2] We stress the importance of time horizon because it matters – reduce your time horizon and investing turns to speculating.

Focusing on the fundamentals

This point is especially relevant today. The implications of a Coronavirus-induced collapse in economic activity followed by unprecedented levels of fiscal and monetary support have led to gyrations in asset values and shifts in preference across the investment spectrum. At the start of 2020, the market continued to prefer the companies of tomorrow – the internet platforms, the digital enablers, and more recently the environmental champions. Aided by persistently low inflation and the determination of central banks to keep interest rates low, valuations in these companies were high by historical standards. On the flip side, businesses considered to be of the old world – capital intensive, polluting, physical rather than digital – continued to lag. Fast forward 12 months, and with accelerating economic growth and burgeoning inflation the situation has reversed.

2021 has also been punctuated by an increase in unconventional and, in some cases, alarming behaviour. Volumes of initial public offerings and the proliferation of Special Purpose Acquisition Companies (SPACs) raise concerns that excess liquidity and low interest rates are driving higher levels of speculation. Additionally, with consumers feeling flush with cash and little opportunity to spend, retail activity is fuelling bubble-like prices in certain pockets of the market. Prices of some companies look to have decoupled from underlying fundamentals driven by rumour and momentum, as the urge to participate is driven more by greed and the fear of missing out than any genuine understanding of the asset in question.

It is during these times that we can take advantage of having an investment horizon beyond that of the average market participant. Over the past six months, the market’s preference to chase low-quality cyclicals has left many of the fundamentally more attractive companies out of favour. For us these companies are more likely to exit the pandemic stronger than they entered it, underpinning an even more attractive investment case. Equally, it is easy to feel we are missing out on those companies that are currently in fashion. Here we must remain patient and ensure that we are ready to act should gravity, as it inevitably does in investing, start to pull these shares back towards levels more reflective of their true intrinsic value.

The policy of war

The pandemic’s immediate impact on the world has been profound. In a little more than 12 months, known infections total 120 million and deaths greater than 2.7 million.[3] This compares to the 290,000 to 650,000 that die each year from influenza.[4]With populations placed into lockdown, GDP around the world collapsed, falling 9.8% in the OECD countries in the second quarter of 2020; the UK alone fell 21.7%. But it was the colossal policy reaction of politicians and central bankers, on a scale not seen since the Second World War, that shaped the investment environment we are in today. On Sunday 22nd March, the day before the market bottomed, the US Federal Reserve unleashed unprecedented levels of liquidity. As Jim Bianco of Bianco Research wrote at the time, “At first blush, it looks like they are nationalizing the financial markets.” Using money ‘printed’ on a digital screen, central banks financed loans and pushed interest rates in the US down from 1.6% to 0.5%. In unison, governments used fiscal policies that provided cash to those who couldn’t work and bridging loans to companies forced into hibernation. Incomes were protected, and debt obligations put on hold.

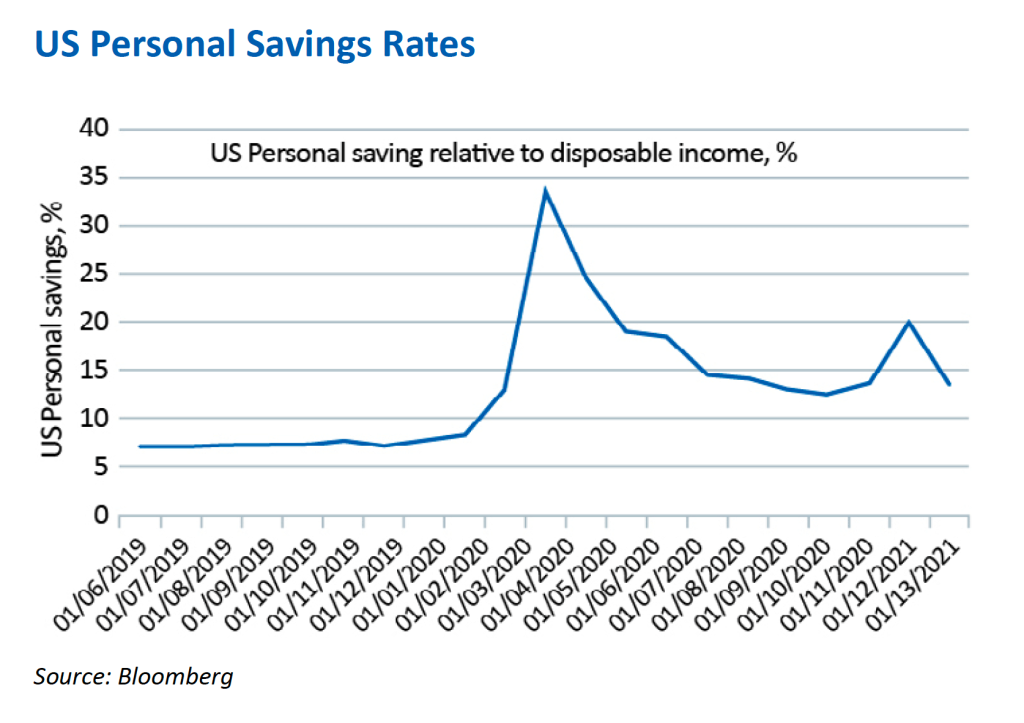

Digitalisation meant that the majority continued to work from home. With the ability to spend suppressed, consumer borrowing collapsed, savings rates rose, and consumer finances improved – an outcome hitherto unheard of during a recession.

“What we are witnessing is the dawn of a second wave of digital transformation sweeping every company and every industry. Digital capability is key to both resilience and growth. It’s no longer enough to just adopt technology. Businesses need to build their own technology to compete and grow.”

Satya Nadella, CEO of Microsoft at the second quarter 2021 conference call

And they thought it couldn’t get any better

After the initial ‘sell everything’ collapse in March 2020, it became clear that the policy of lockdown would favour a particular group of companies. The inability to leave home forced a reimagination of how we work, how we spend and even how our children learn. Trends towards digitalisation in the home and in the workplace accelerated, bringing forward levels of adoption and penetration that would have taken years to occur otherwise. Technology companies that were already in the ascendancy, couldn’t have asked for more.

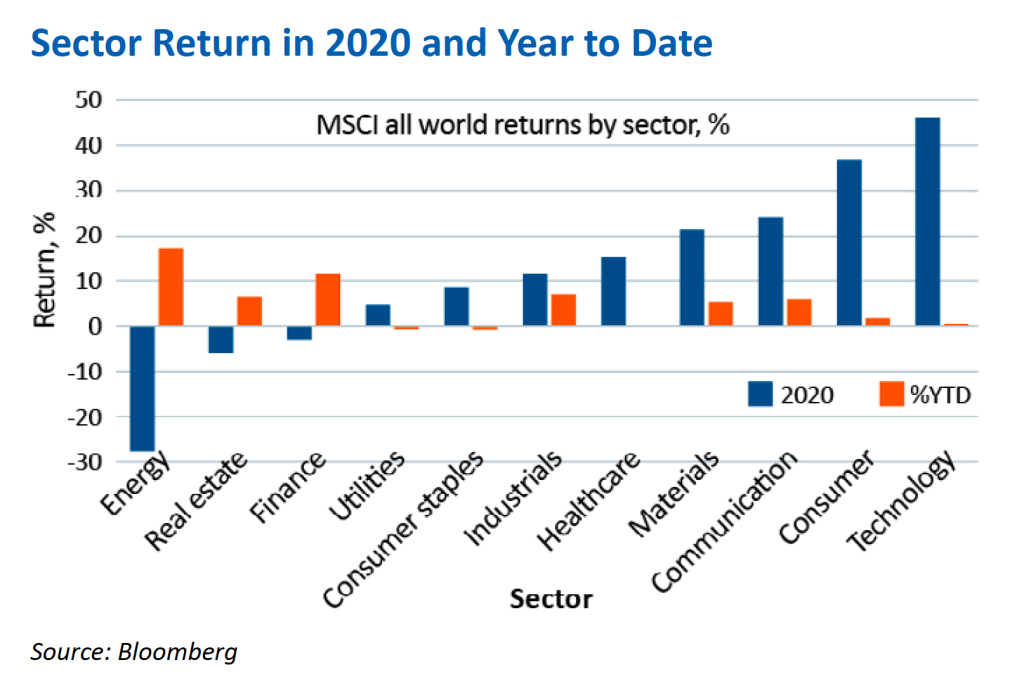

Netflix, the video streaming giant, added 37m new subscribers in 2020, 33% more than the year before. Amazon’s online sales growth accelerated from 15% in 2019 to 40%, and Zoom’s revenue increased three-fold; the video conferencing application has gone from near obscurity to the status of its name being used as a verb. Microsoft’s sales, driven by the need for corporates to build flexible/cloud-based IT infrastructure, never skipped a beat growing at 15% in each quarter of fiscal 2020, faster than the 14% growth of 2019. In contrast, banks, energy, and companies dependent on social interaction for their revenues all suffered. Of course, some of this will revert as restrictions lift but the world after lockdown will in many ways have changed for good.

Saved by science

Gradually, during the summer months, the levels of fiscal and monetary support coupled with growing optimism around a vaccine began to fuel higher levels of confidence in an economic rebound. The wave of announcements of vaccine efficacy in November triggered a greater confidence in the narrative of normalisation. Vaccines provide the crucial ingredient to exiting lockdown. Efficacy in preventing infection is high in all variants but more importantly all have a 100% success rate in preventing death or hospitalisation. When the political narrative for lockdown has been predicated on the prevention of overwhelming healthcare systems, then the argument for continued enforced social distancing surely weakens once the majority of the population has received the jab. These vaccine announcements triggered a sharp rotation in market leadership as lockdown winners were sold and companies more sensitive to a sharp economic rebound were bought.

Higher demand will lead to higher prices

Despite much of the world experiencing another wave of infections, hospitalisations and deaths over the winter months, the optimistic trends of late 2020 have continued into 2021. The market remains firmly focused on the roll-out of the vaccine and an imminent re-opening of economies. But this is not a normal recovery. High levels of consumer confidence after a year of artificially suppressed demand are likely to lead to high levels of activity once lockdown ends.

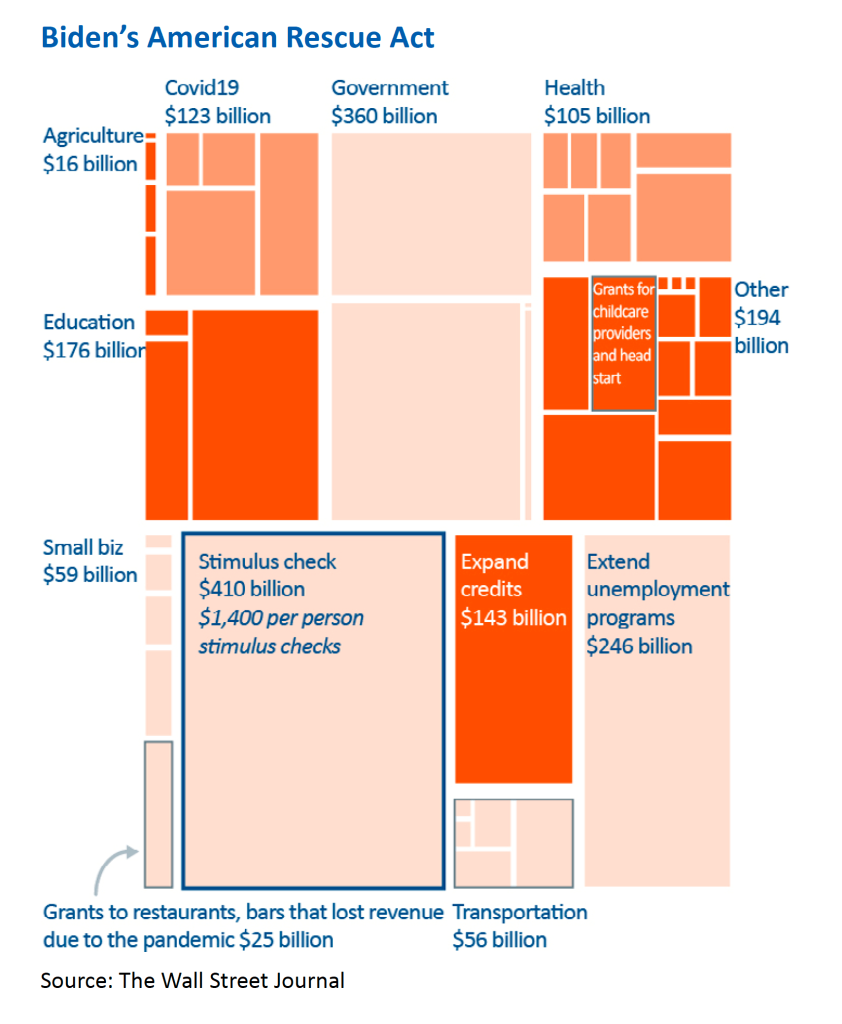

To add fuel to the fire, Congress has recently agreed another round of stimulus, passing President Biden’s $1.9tn American Rescue Act, the second-largest spending package in history and putting another $1,400 of cash in the hands of American households. This is despite the expectation of GDP growth in the US of 6.5% in 2021.

As we lap the anniversary of the depths of the crisis and collapse in energy prices, higher inflation seems a mathematical certainty in the near term. Central banks, led by the Federal Reserve, are unperturbed. Chairman Jerome Powell has signalled a belief that any short-term spikes in inflation will ease as supply constraints normalise. The bond markets are unconvinced, testing the central bank’s resolve to keep rates low. Since the start of the year the US 10-year treasury yield has risen from 0.9% to 1.7%, recapturing all the downdraft caused by the pandemic. On average, US bonds have fallen -3.2% in dollar terms and UK Gilts -4.2%.

Our conservative allocation to fixed income assets has reduced the impact of this sharp decline in bonds in recent months. Our exposure is concentrated in index-linked bonds that provide some protection against higher inflation, particularly any surprise increase, but even these have not been immune from the moves this year and are down -1.2% in the US and -1.8% in the UK year to date.

A store of value

With bond prices falling at historic rates and inflation threatening to breakout, we continue to see gold as having a role in portfolio construction. However, as an asset with a zero-income return, gold’s relative attractiveness diminishes as real interest rates (interest rates adjusted for inflation) rise. In recent months, bond yields have risen faster than inflation expectations, which has pushed real interest rates up and contributed to gold falling 10% during the quarter.

Interest in gold may also have been hampered by the levels of speculation in Bitcoin. Its rise from financial obscurity to the financial mainstream is remarkable. In the past year Bitcoin has increased eight-fold and has doubled in 2021. We have given it much consideration. It shares many characteristics with gold: limited supply assets that should provide protection from the devaluation of fiat currencies.

Currently, we remain on the side-lines. The extreme volatility in Bitcoin and other cryptocurrencies due to excess speculation and limited liquidity make this an extremely difficult asset class to hold, while serious questions around the environmental impact of Bitcoin and the potential for regulatory interference continue to be at the forefront of our concerns.

We continue to hold our position in gold for two reasons. First, as protection should inflation rise faster than expectations, pushing real interest rates down. The second, is as a store of value in periods of heightened market stress when all other assets are sold. The current environment is not one where we would expect a relative outperformance of gold, but it remains an asset that can provide valuable protection when the unexpected strikes, just as it did in 2020.

“The urge to buy an investment because its price went up means you probably don’t know why the price has gone up. And if you don’t know why the price has gone up, you’re more likely to bail when it goes down.” Morgan Housel, The Collaborative Fund

Story Stocks & SPACs

There is no doubt that Bitcoin’s recent rise is partly driven by the fear of missing out or FOMO as it is often called. FOMO tends to build as cycles accelerate and assets rise in value. The gamification of investment platforms and the digitalisation of investing in recent years has provided the tools for retail investors to participate in markets like never before. Add this to low interest rates, strong consumer finances and a lack of anything else to do, and there is the potential for assets to enter bubble territory.

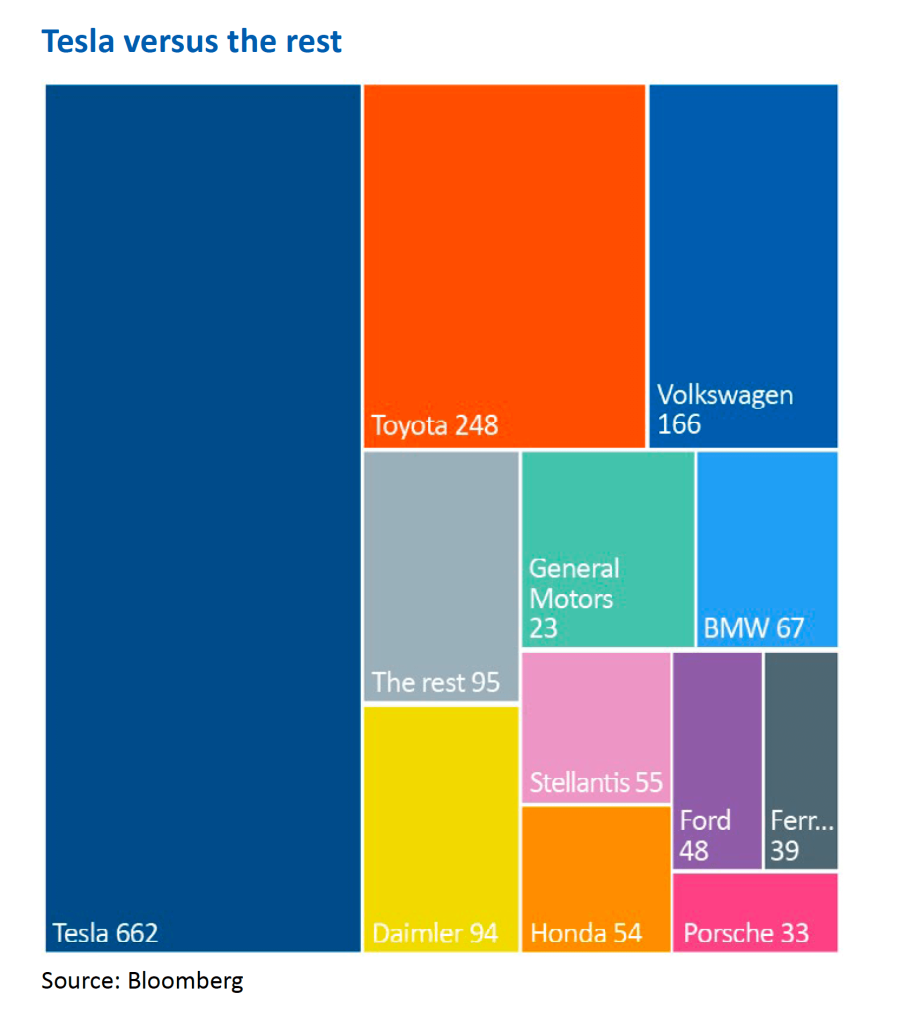

Story stocks have been the largest beneficiaries – companies that tell a great story about their potential but where today’s share price appears far removed from the realities of their profit potential. Tesla might be the poster child for this phenomenon, but it is just one of many. Largely down to the cult-like status of the CEO, Elon Musk, the share price of Tesla has risen from $75 at the start of 2020 to $900 at its recent peak ($670 at the time of writing). We are not disputing the potential for Tesla to be one of the world’s largest car companies in time but at a market cap of $662bn it is already nearly three times larger than the next largest company, Toyota, and larger than all the rest combined. Putting this into context, in 2020 Tesla delivered 500,000 vehicles compared to Toyota’s 2.1 million.

If prices can rise irrationally on the way up, then what happens when confidence subsides, and prices begin to fall? Tesla shares have already fallen 25% from the recent peak and similar moves have occurred in other stocks where retail activity is high, and valuations stretched.

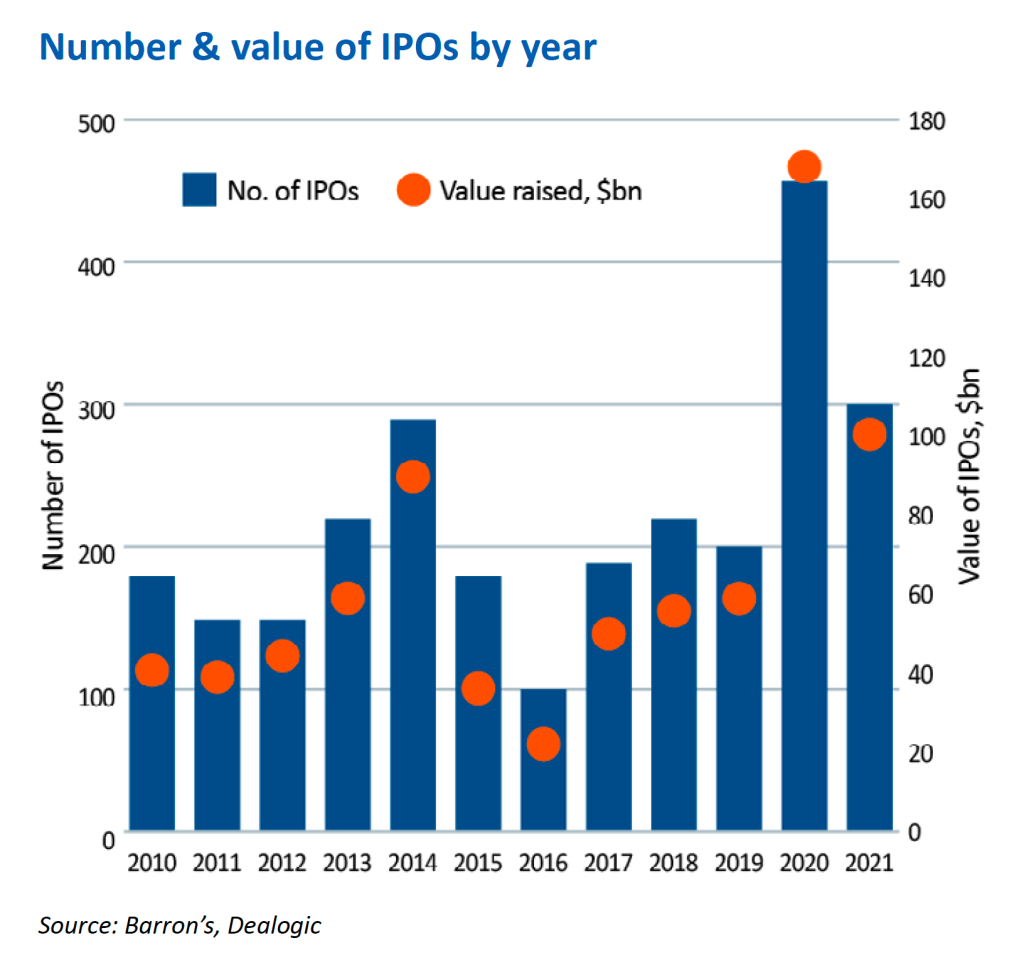

The spate of initial public offerings (IPOs) this year is also worth noting. At 302 to the beginning of March, the number of IPOs is already close to overtaking the 457 new company listings of 2020. Even more alarming is the number of these IPOs that are so-called Special Purpose Acquisition Companies (SPACs). These are blank cheque structures whereby investors buy a share of a shell company, whose sole purpose is to go out and buy private companies, for which the managers clip a hefty fee for the privilege. To date, of the 302 IPOs, 80% have been SPACs. Many of these companies are yet to make a profit. This is nothing new; young companies that are aggressively investing to grow rarely make a profit, but the number of IPOs that are in the red stands at around 80% today compared to averages closer to 50–60% in the past; further evidence that speculation and excess liquidity are powering markets over and above rational analysis.

Adjusting the tiller

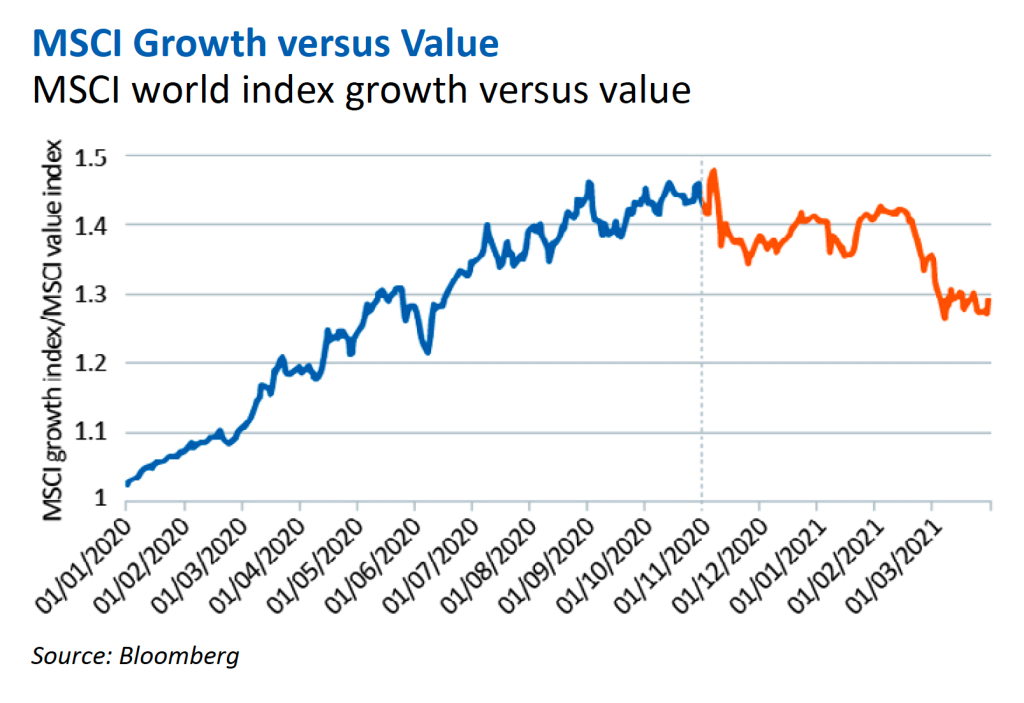

We continue to see plenty of opportunity in equity markets and our investments, although they have lagged the broader market index this year. Our preference for businesses with dependable profitability and limited volatility has been out of favour in the early cycle ‘dash for trash’. While at an aggregate level the MSCI World Index rose 4% in local currency terms, splitting the underlying constituents into baskets of growth, quality, and value shows the returns are markedly different at 0.1%, 2.9%, and 8.9% respectively. As can be seen from the following chart, it was the advent of the vaccine that drove a shift in leadership from growth and quality to value.

Aware of our portfolio biases and the strength of the trends in front of us, we have been adjusting the portfolios since Autumn 2020. Funded by a reduction in the allocation to bonds, we have added to equities – focusing on companies and funds with higher sensitivity to an opening-up of the economy and acceleration in the economic cycle, but only where we have confidence in longer-term sustainable growth and our quality thresholds are met.

Examples include Compass Group in the UK, which provides catering services to businesses, hospitals, universities, and entertainment venues. While Compass’ activity levels remain understandably low, there is evidence that there will be greater demand for outsourcing post the pandemic as the complexities of managing catering in-house rise. Another example is Vinci. As the operator of road concessions and airports, Vinci is a natural beneficiary of rising economic momentum with limited competition. Finally, we have increased exposure to companies we already own that will benefit from current market dynamics. These include Rio Tinto, the miner; JPMorgan, the bank; and Amphenol, a specialist in sensors and connectors used throughout the industrial and technology supply chain. All three are market leaders in their field, with higher returns on capital and lower indebtedness than their peers. All should prove beneficiaries of enduring trends as well as near-term momentum.

Despite the respective 17% and 12% rise in the energy and financial sectors year to date, we have not been tempted to sacrifice the quality of our portfolios to chase short-term returns. Even if we could have timed our entry here, making a profit in cyclical low-quality markets is predicated on timing the exit too – an outcome more often determined by luck than skill in our experience.

Focusing on the fundamentals of their respective markets, both sectors remain unattractive to us. In the energy sector, even leaving the environmental debate to one side, oil and gas companies operate within a market where 40% of global oil supply is dictated by national oil companies ordinarily controlled by authoritarian regimes. These companies do not have the same cost of capital or shareholder constraints as their listed peers. At the same time, the oil majors, through shareholder activism, are being forced to reallocate capital into alternative markets such as wind power generation, where barriers to entry are low and returns, already significantly below their legacy businesses, are falling. An industry with rising costs of capital and falling returns does not offer great prospects for sustainable growth.

In the financial sector, banks have risen this year on the back of a steepening yield curve. As discussed above we see this is a short-term cyclical dynamic. In the longer term, after bringing the global financial system to its knees in 2008, banks have become heavily regulated with limits on leverage and high levels of capital requirement constraining profitability (we doubt the recent controversy around the family office Archegos will do anything but increase regulatory oversight). In addition, the sector remains extremely competitive while smaller, nimbler financial technology companies continue to disrupt their markets and raid their profit pools.

“Even if one knew what the stock market was going to do, it would be more profitable to forget it and concentrate on trying to find the right stock to buy.”

Warren Buffett

Building resilience, sticking with quality

While the market has focused on value at one end and extreme speculation at the other, we firmly have an eye on the horizon and how the world might look beyond the next 12 months. After a fantastic year in 2020, we believe many of our companies and the themes we are exposed to through our funds, stand on stronger foundations today than they did before the pandemic. As investors chase the rebound trade, it is our resolve to not do too much. The short-term market direction is impossible for us to predict but by maintaining our focus on companies that offer genuine long-term sustainable growth, these periods of higher volatility and market rotation should be seen as periods of opportunity rather than threat.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.

James Hambro & Partners LLP is a Limited Liability Partnership incorporated in England and Wales under the Limited Liability Partnerships Act 2000 under Partnership No: OC350134. James Hambro & Partners LLP is authorised & regulated by the Financial Conduct Authority and is a SEC Registered Investment Adviser. Registered office: 45 Pall Mall, London, SW1Y 5JG. A full list of partners is available at the Partnership’s Registered Office.

[1] MSCI ACWI data used in market references

[2] Morgan Housel, Collaborative Fund

[3] https://www.worldometers.info/coronavirus/

[4] World Health Organization estimates