01.06.2020

Nobody said it was easy – Coronavirus update

Dan Zegleman, Portfolio Manager

Daniel Zegleman, Portfolio Manager

Not many would have included a global pandemic, the lockdown of over half the world’s population and a shut-down of large sections of the economy as realistic risk factors to be considered entering 2020. A 50%+ drop in the oil price following a breakdown in negotiations between Saudi Arabia and Russia added further fuel to the fire. Cue one of the fastest bear markets of all time, the worst quarter for equities in over 30 years and daily market moves reminiscent of the depths of the financial crisis in 2008.

Given elevated market valuations and record-high index price levels as recently as mid-February, in many respects the market reaction could have been much worse. With lessons learnt from prior crises, central banks and governments worldwide have responded with support policies of commendable size and scope. Once the immediate health crisis is brought under greater control these measures should help limit the second-order effects such as job losses and corporate defaults while providing a powerful support for a return to growth after restrictions to daily life are lifted. Indeed, signs that we are passing the apex of COVID-19 transmission has been enough to trigger a 20% rebound in world equity markets from the lows reached in late March.

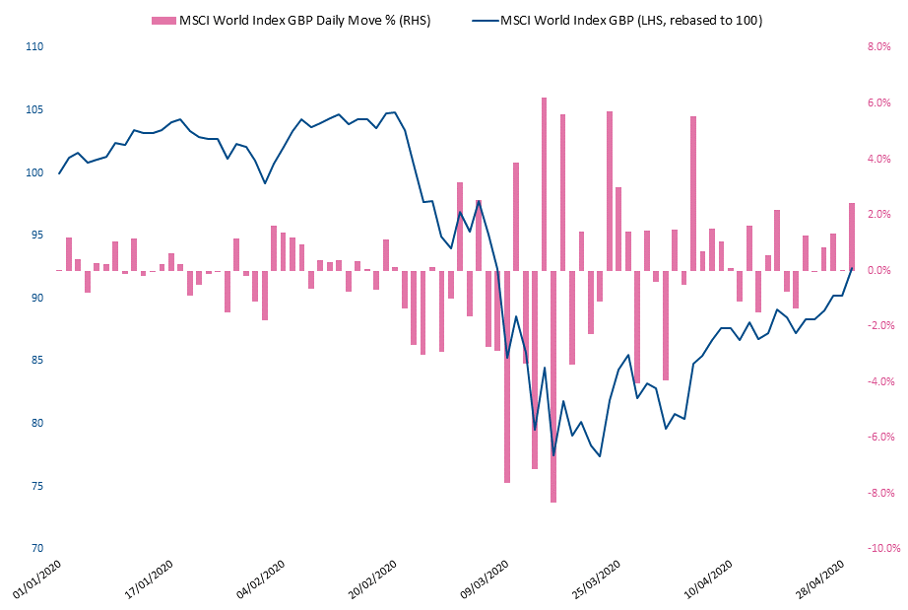

Over the 50 trading days from the market peak to the end of April, the absolute daily move has averaged almost 2.5%. Not even during the throes of 1929 or 2008 have equities served up such a sustained diet of day-to-day volatility.

Figure 1: Daily and cumulative world equity returns 2020 YTD. Source: Bloomberg, all figures in GBP

Reasonable vs. Rational

“’Be greedy when others are fearful, and fearful when others are greedy,’ is rational, but hard. ‘Be fearful before others are fearful and less greedy in general.’ That’s more reasonable.” Morgan Housel, The Collaborative Fund

Faced with an uncertain world, our investment approach deliberately looks for companies that can deliver sustainable growth from selling essential products or services that are recurring or predictable in nature. Businesses with these attributes form the bedrock of our portfolios; many are found in the software & services, consumer staples and healthcare sectors, and have to date proved relatively insulated to the lockdown and broader economic slowdown. Some may even benefit from changing consumer habits and business processes brought about by the crisis, such as a shift of more activities online, increased demand for hygiene products and a longer-term step-up in investment across healthcare services. ‘Microsoft Teams’, the company’s video-calling solution, nearly doubled the number of active users to 75 million in March alone, while Nestle and Unilever reported their strongest sales growth in North America in decades as consumers rushed to stock up on Nescafe and Domestos.

However, not all our businesses have proved so defensive, particularly those with more economically sensitive end markets, such as industrial production, retail or other discretionary consumer spending. Here, we have taken comfort in the financial and balance-sheet strength that we require across all our individual company investments. As part of our investment research, we ask ourselves a series of questions around a business’s financial model with the very purpose of protecting us should economic conditions deteriorate, or our conclusions prove wrong.

The financial flexibility brought about by appropriately prudent debt levels, low reinvestment requirements and high initial profitability provides a company with an ‘ability to suffer’ through the tough times, allowing them to take advantage of a crisis to emerge an even stronger business than peers in the recovery. We have undertaken a series of stress tests across our more exposed names to ensure that they have the liquidity and solvency headroom to weather a prolonged period of significant disruption.

Finally, like most investors, we didn’t predict or plan for a scenario where international travel would cease almost overnight. The structural growth in air travel and leisure spend had been a powerful theme in portfolios for several years, during which we made investments across the aerospace, hotels, trade exhibitions and travel retail industries. The companies we targeted were fairly resilient to economic conditions in any normal environment and a rational analysis might suggest that their share prices will rebound quickly as travel returns post-crisis, supported by rising wealth in emerging markets and the expansion of low-cost airlines bringing new consumers into the flying population over the coming decades.

However, a reasonable counter would point to an unknowable period of near-zero revenues, psychological scars slowing any recovery and longer-term impacts on business travel and face-to-face events. Almost two-thirds of hotel and airline profits are tied to corporate customers – for the likes of Intercontinental Hotels, Airbus and SSP the facts have undoubtedly changed. In such extraordinary circumstances, previously strong balance sheets can become weak almost overnight. With infection numbers rising and any potential vaccine still some way off, in February and March given the heightened level of uncertainty we sold holdings most obviously at risk from lockdown policies and plummeting commodity prices.

The world after COVID

There is a growing consensus that one of the consequences of the crisis will be an acceleration in the recent reversal of globalisation and the reorganisation of complex global supply chains. For companies relying on lower-cost labour or components from far-flung corners of the world, the longer-term implications are rising costs of business and lower profitability.

It also seems likely that we will see ever-greater government control of our economies (ironically in response to a dislocation created by government interference in the first place). For more regulation, subsidies and surveillance, read higher costs, lower growth and reduced enterprise. Those companies that can withstand the current environment without outside assistance and that offer exposure to secular growth in a new low-return world seem likely to be rewarded with an even greater premium.

“As Covid-19 impacts every aspect of our work and life, we’ve seen two years’ worth of digital transformation in two months.” Satya Nadella, Microsoft CEO

At a more company-specific level, the necessary response to the pandemic is validating many already powerful digital trends that have been in train for a number of years. Thanks to superior digital technologies in areas such as remote working, online shopping, payments, home entertainment and telemedicine, many parts of the economy have been able to continue with some semblance of normality.

Recessions also have a way of forcing the pace of change for the parts that can’t – inertia in the good times is giving way to rapid digital adoption, particularly across industries that have resisted technological change in the past such as healthcare, banking, retail or the government. Shoppers will go back to stores, employees will return to offices, and not all new users of Zoom will stick, but new habits are being formed and the transition towards a more digital economy will continue to accelerate.

One of the first questions we ask ourselves of every company we consider is: Is this company benefitting from technological change? Ecommerce champions, digital payments leaders, business software and analytics providers, online advertising giants – have all just found lots more potential customers.

The more things change…

“I very frequently get the question: ‘What’s going to change in the next 10 years?’ That’s a very interesting question. I almost never get the question: ‘What’s not going to change in the next 10 years?’ And I submit to you that the second question is actually the more important of the two. Jeff Bezos, Amazon founder and CEO

Notwithstanding the trends discussed above, it is also likely that in many ways life will return to normal, with some of the more far-fetched predictions of a new world order following the crisis proving wide of the mark.

Change undoubtedly brings investment opportunities, but often it is easier and more rewarding to remember that some strategies are timeless. We know people will not stop caring about Amazon’s lower prices, Spotify’s wider choice or innovations that give them greater control of their time. Technological advances may have allowed Netflix to build their business, but it is the ability to watch what you want, when you want, with greater choice at better value that has enabled it to be successful. It is a superior product.

Likewise, businesses will always be willing to pay for more efficient solutions to their problems or tools that give them greater insight into their customers or analysis of their operations. Successful companies don’t sell ‘technology’ or ‘structural change’, they sell convenience, cost savings, increased speed to market, improved productivity and greater flexibility. Trust, increased confidence and the promise of higher social standing never go out of fashion.

Understanding change is important, particularly when accelerated by a crisis. But structural shifts don’t happen for their own sake; the legacy of this crisis may well be more video calls over yet another business trip, online shopping rather than a traffic-filled drive to supermarkets, or a further shift to digital payments instead of ‘dirty’ coins and banknotes, but the underlying reason for their success will be the same as it ever was. It’s an improvement.

By Daniel Zegleman

Posted on 1 June 2020

Opinions and views expressed are personal and subject to change. Mention of any stock by name is not a recommendation to buy that stock. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.

James Hambro & Partners LLP is a Limited Liability Partnership incorporated in England and Wales under the Limited Liability Partnerships Act 2000 under Partnership No: OC350134. James Hambro & Partners LLP is authorised & regulated by the Financial Conduct Authority and is an SEC Registered Investment Adviser. Registered office: 45 Pall Mall, London, SW1Y 5JG. A full list of partners is available at the Partnership’s Registered Office.