19.11.2021

November investment update

James Beck, Partner, Head of Investments

Strong earnings helped keep markets buoyant in October, but the contrast with negative returns in September demonstrated the importance of managing risks effectively.

October saw a revival in markets after a more subdued September. The MSCI AC World Index returned 4.7%, compared with -3.4% the month before. This sharp reversal in fortunes could have left investors with a case of whiplash: September was the first monthly fall in the index since November 2020, and then October the best return since the same date.

So, what changed? Last month, news flow had an impact on investor sentiment. Debt levels of Chinese property companies, uncertainty over how quickly the US Federal reserve would reduce its bond buying programme and headlines about squeezed supply chains all weighed on investors’ minds. Combined with high valuations after the extended bull market since late 2020, this led to some profit-taking and realigning of assets into less affected areas, all of which acted as a drag on markets.

None of these issues has gone away exactly, although there is now much more clarity over the US Fed’s intention on asset purchases. Markets can often overreact to bad news in the short-term, and spring back quickly once the initial shock wears off. After the knee-jerk, investors have an opportunity to digest what the changes really mean, adjust portfolios and refocus on fundamentals.

At present, the overall background is accommodating for equities and liquidity is high. Economic growth is likely to remain positive well in to 2022, albeit slower than after the post-lockdown surge. Consumers are still nurturing post-lockdown bank balances, which should continue to power economic activity, and they may soon be joined by corporates who look ready to invest. Combine these factors with rising inflation expectations – that favour companies with pricing power – and equities still look attractive particularly when compared to other options.

An alternative approach to risk

However, the fluctuation in returns between September and October supports our view that we’re likely to see choppier markets in the coming months. Inflationary pressures and central bank responses are just one factor that could disrupt markets as economies readjust after the long period of fiscal and monetary support.

In this environment, it’s crucial to find investments that will provide a positive return that isn’t linked to the direction of equity markets. That’s why we’ve decided to increase our allocation to the ‘alternatives’ basket within our client portfolios.

‘Alternatives’ covers a range of assets with characteristics that help us diversify portfolio risk. It’s a mix of funds that invest in real assets – things like property and infrastructure projects – and absolute return funds, that focus on generating a positive return in all market conditions.

They are especially important when cash and bonds are under strain. While we are keeping some bond exposure to protect against market surprises, real returns in most developed government bonds are negative. And with the CPI set to hit 4% or more over the next few months, investing in cash now provides a very material loss once the corrosive impact of inflation on spending power is accounted for.

Earnings season boosts markets

In October, companies report on sales and after-tax income (or ‘earnings’) over the third quarter of the year. As well as providing insight into how well an individual company is doing, the overall trends are an important indicator of the health of the corporate world. Absolute numbers are less important than relative performance – relative to the previous year, and to analysts’ estimates of how well they would do.

This quarter, results have left markets in an upbeat mood. Sales and earnings are up, and a large proportion of companies have returned numbers ahead of expectations. While the data is a little lower than the previous quarter, it’s still well ahead of historical averages showing companies are in good shape.

By the time reporting season was over, overall sales growth was 19% and earnings were up by 42% over the previous year. This is 3% ahead of expectations on sales and 9% ahead on earnings. Overall, around 80% of companies beat analysts’ expectations.

In Europe, revenues were up 16% and earnings up 42% – similar levels of growth to the S&P 500, but because expectations were higher, this was just 4% ahead of expectations on sales and 8% on earnings.

Inflation on everybody’s mind

Inflation has been grabbing headlines over the quarter, and it should come as no surprise that companies are worried about the impact it could have on their profits. Analysis by the Bank of America showed a massive increase in inflation-related discussion in earnings results this quarter compared to Q2.

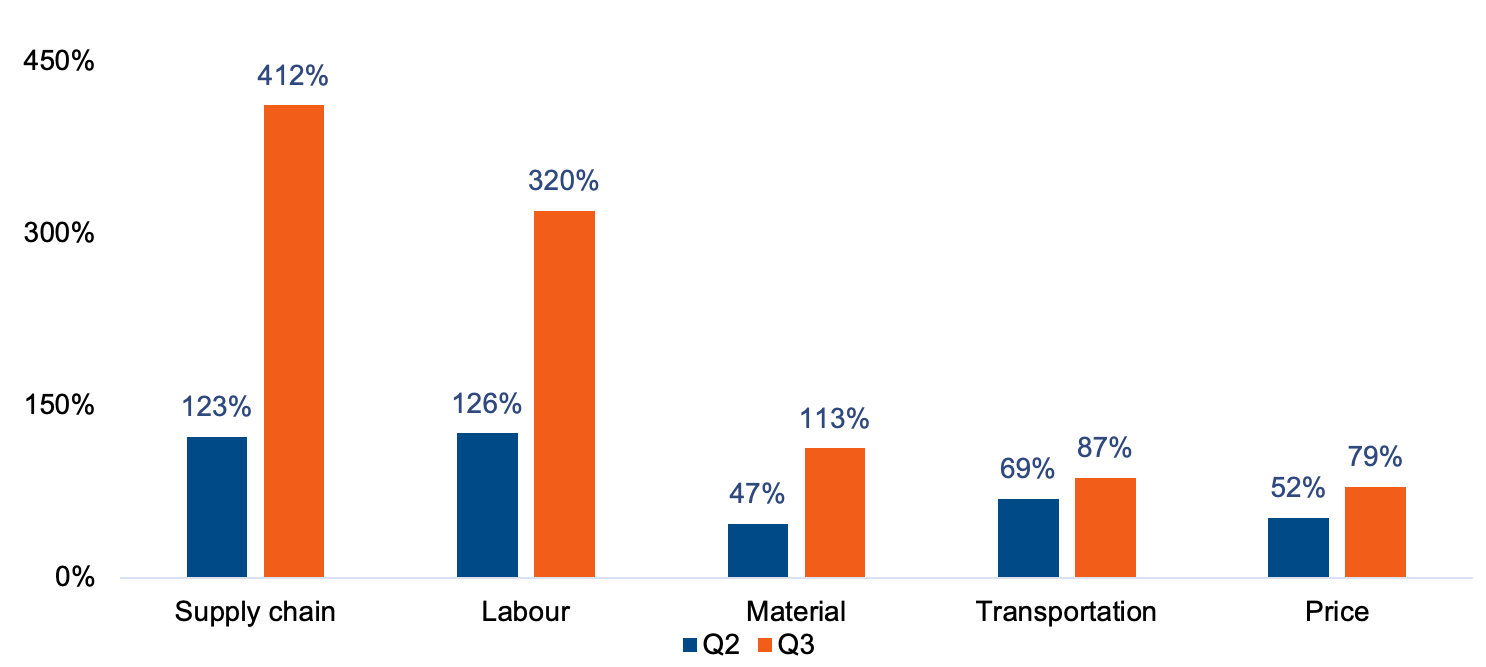

Growing concerns

Companies in the S&P 500 were much more likely to talk about inflation during the earnings announcements than last quarter.

Represents the number of times inflation-related words were mentioned as a percentage of the number of companies reporting. Words included: price: ‘price’, ‘pricing’; materials: ‘material’, ‘commodities’; transportation: ‘transportation’, ‘shipping’, ‘freight’, ‘logistic’, ‘fuel’; Labout: ‘wage’, ‘worker’, ‘personnel’; supply chain: ‘supply chain’

Labour costs are on the rise, as rising demand has seen more positions opening and the supply of unemployed workers fall. In fact, there’s been a notable trend of workers being nudged into early retirement – partly a result of post-pandemic lifestyle reassessment and partly thanks to retirement plans accelerated by stimulus checks and the effect of rising markets on pensions.

The lag in getting basic materials moving is also having an impact, with semi-conductors particularly hard-it. As everything is a computer these days it’s had knock-on effects across many industries from autos to consumer electronics to heavy engineering.

But the results themselves provide evidence that rising inflation hasn’t damaged company returns. Price increases have been passed along to the consumer fairly easy, reflecting the fact that many consumers are still sitting on lockdown savings or money from stimulus payments, in the case of the US.

This underlines the importance of pricing power, one of the key characteristics we look for in companies. Having a product that’s essential and embedded in consumers’ lives, and that’s not easily replaced by competitors, means customers are more willing to absorb price rises. With inflation set to be a factor in economies for a while to come, it’s likely that these are the companies that will outperform.