Thousands of retirees in final salary pension schemes are making costly decisions on whether to take up their option of a 25% tax-free lump sum because of poor information and lack of advice.

From the age of 55 pension savers can take 25% of their pension pot in tax-free cash. For those on ‘defined contribution’ schemes, this is easy to calculate. It is simply a quarter of whatever they have saved into their pension pot over a working lifetime.

But for those in ‘defined benefit’ schemes – better known as ‘final salary’ schemes – it is much more complex. Their pension is based on their length of service and final or average lifetime salary.

To access their tax-free pension allowance (the “pension commencement lump sum”), holders must forego a proportion of regular pension. The scheme administrator calculates the size of the up-front lump sum compensation using a ‘commutation’ factor. This is determined by scheme rules and can be set by the trustees or the sponsoring company. Public sector schemes are among the meanest, typically using commutation factors of 12. Elsewhere the factor varies widely between schemes.

Research among private sector pensions schemes from James Hambro & Partners has shown final salary schemes offering commutation multipliers ranging from 14 to 36.

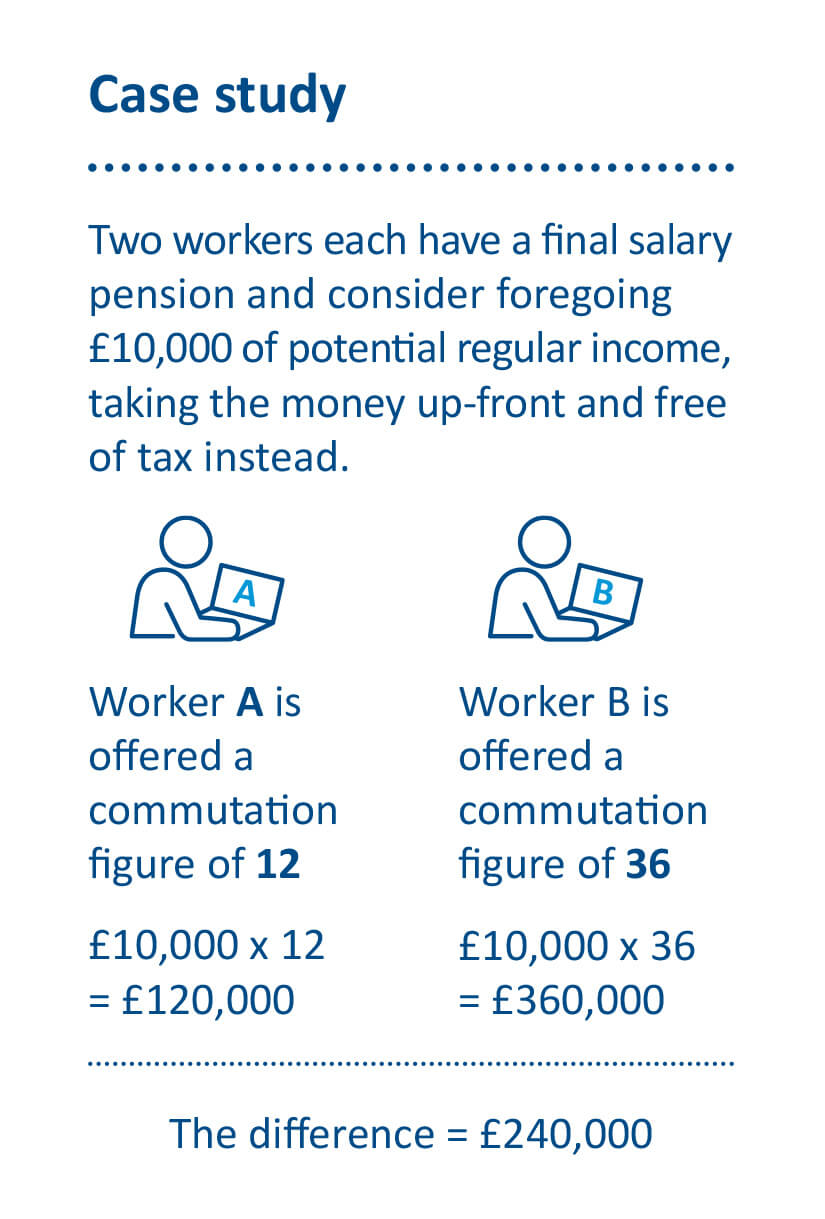

It is a shocking disparity. For someone looking to forgo £10,000 of annual pension it could mean the difference between them receiving a tax-free lump sum of £120,000 or £360,000 – a difference of nearly quarter of a million pounds.

Across the industry 20 is considered about the point at which commutation begins to be considered worthwhile. But many people see this as tax-free cash and take whatever they are offered by default. They assume – because it is tax free – that it is the sensible option. Some need the cash to pay off their mortgage and others to fulfil a dream, like buying a motor home. But in a lot of cases people do not really need the lump sum. If they took advice and reviewed the numbers carefully they would see they were better taking the money as income. The key thing is to take professional advice.

One James Hambro & Partners client offered a commutation figure of 14 declined to take the tax-free lump sum after we ran a number of calculations for her. She will pay more income tax. But she and her husband – who will get half the pension if she dies before him – are both in good health. They are having to pay tax on a proportion of their pension that should be tax-free, however, they will generally enjoy index-linked growth on the pension income. There is a strong likelihood of them living beyond the breakeven point, though basic rate tax payers achieve this sooner than higher rate payers.

Defined benefit drawbacks

Generally, defined benefits schemes are regarded as valuable because they offer an assured income through retirement. But they are less flexible and do have drawbacks. Once you take a tax-free lump sum in a defined benefit scheme you must start taking the pension, even if still working. If you opt to take the tax-free lump sum benefit you have to take it in one go. Those in defined contribution schemes can take it in small regular chunks over their retirement, which can be very tax-efficient.

Finally, if you have a defined benefit pension and die, your spouse or civil partner will usually get 50% of your pension. There may be benefits for children who are still minors, too. Holders of defined contribution schemes, however, can pass on everything left in their pension pots to loved ones or favoured charities on death.

Think before you switch

Some may be tempted to try to access the benefits of the defined contribution scheme by moving the pension prior to retirement out of a defined benefit scheme to a defined contribution scheme. But there is a wide variation between schemes on what is known as the “cash equivalent transfer value” (CETV) of pots, as well. Two 60-year olds from different schemes with the same normal retirement age of 60 may be offered different CETVs. One could be 27 times the pension given up, the other 40 times.

Anyone wanting to transfer a defined benefit scheme to a defined contribution scheme will usually be required to take professional advice. This can be expensive because it is a specialised area subject to intense scrutiny from the financial regulator, whose assumption is that it is almost always better to be in a defined benefit scheme. The regulator is right. The defined benefit scheme has its flaws, but there is huge upside to having a generous, guaranteed, index-linked, pension for life. The only question for most people is whether to take the tax-free lump sum. This is where advice can come in useful.

By Sean Jones

Posted 19 October 2020

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document. And no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.