20.04.2018

Trade wars and technology – market commentary Q1 2018

Mark Leach, Partner, Portfolio Manager

“The way to prosperity for all nations is rejecting protectionist legislation and promoting fair and free competition”, Ronald Reagan in a radio address to the nation, 25 April 1987

By Mark Leach

Free market economists have long espoused the risks that protectionist policies bring to the global economy; as each state responds the collective result is to lower global trade to the detriment of all parties. Historically, politicians have worked hard to promote their free market credentials but in reality, their policies have often fallen short of this utopian expectation. Ronald Reagan is perhaps one of the more controversial figures in this debate, having publicly called for more free trade while at the same time justifying policies that attacked the ‘dumping’ of Japanese cars on US consumers to the disadvantage of domestic industry.

In recent weeks, President Trump has reignited this debate with his attack on China in an attempt to rebalance the US trade deficit (see figure 1) and in theory revive US industry. Such populist policy is at odds with modern economic theory, but politicians are incentivised to think in the short term, focusing on protecting the jobs of their electorate thus creating a natural conflict between philosophy and reality. In this regard there is likely to be some truth to the US Commerce Secretary, Wilbur Ross’ recent comment that, “the EU, China and Japan, all talk free trade, and they all practice protectionism”.

The New Year began with all OECD countries seeing positive GDP expansion and economic indicators signalling further growth to come. Economic strength coupled with lower taxes, following sweeping reforms in the US, added fuel to corporate earnings momentum to drive stock prices higher with the MSCI All World Index up 4% in January, having risen significantly in 2017. Technology remained the leader of the pack with the Nasdaq[i]rising 7.5%.

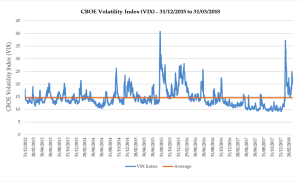

A confluence of factors, including extremely easy monetary conditions through persistently low interest rates and steady job growth with low inflation, had contrived to bring volatility of asset prices to historically low levels. These benign conditions created an environment of investor complacency that snapped in early February on the back of a marginally higher than expected wage inflation print in the US. A significant pullback ensued bringing with it an increase in market volatility (see figure 2[ii]).

Figure 1

Source: Bloomberg, 04/04/2018

The market quickly recovered only for the cracks to re-emerge in March as Trump revealed his protectionist intentions. This coincided with a correction in technology companies, triggered in part by the scandal surrounding Facebook, placing it and other consumer facing platforms in the crosshairs both of politicians and regulators. Technology has been a strong theme in our portfolios for some years with a focus on businesses that continue to disrupt incumbent markets and use network effects to build high barriers to entry and strong cash flows. However, while many of these companies remain well placed longer term, we recognise the risks that lie in a sector that has been the primary driver of index returns. As an illustration, at the start of 2017, Facebook, Amazon, Apple, Microsoft and Google, combined, accounted for 11% of the S&P 500 Index; by the end of year the ‘FAAMG’ stocks had risen 44% in aggregate and accounted for a fifth of the increase in the index taking their index weight to 13.4%.

With the onset of the sharp decline in early February, we took further equity risk out of the portfolios, adding the proceeds to already above-benchmark cash and short-term money market funds. So long as economic fundamentals remained robust, driving higher earnings growth, our preference for equities relative to bonds has remained consistent; serving portfolios well in recent years. However, we have written extensively on the burgeoning risks to equities as valuations have risen and the cycle has evolved. With global trade relations deteriorating we have, more recently, rationalised our technology exposure, aware that trade barriers are likely to benefit no-one. With excess liquidity at a time when political grandstanding is building, our preference is to maintain a heightened level of caution in the portfolios until equity valuations improve and a more settled environment emerges.

Figure 2

Source: Bloomberg, 04/04/2018

Mark Leach

[i]The Nasdaq is a stock market index of the companies listed on the Nasdaq Stock Exchange in the US with a heavy bias to technology companies.

[ii]The VIX is the Chicago Board Options Exchange Volatility index. It is a forward looking measure that estimates how volatile options contracts on the S&P 500 will be between the current date and the option’s expiration date. It is more commonly known as the ‘fear index’.

Posted 20 April 2018

You should not act on the content of this market commentary without taking professional advice. Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made of given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions.

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. Fluctuations in interest rates may affect the value of your investment. The levels of taxations and tax reliefs depend on individual circumstances and may change. You should be aware that past performance is no guarantee of future performance.

Image: iStock