Jamie Hambro, Chairman, James Hambro & Partners

Some generations are lucky enough to be born in times of relative political peace and a benign economic environment.

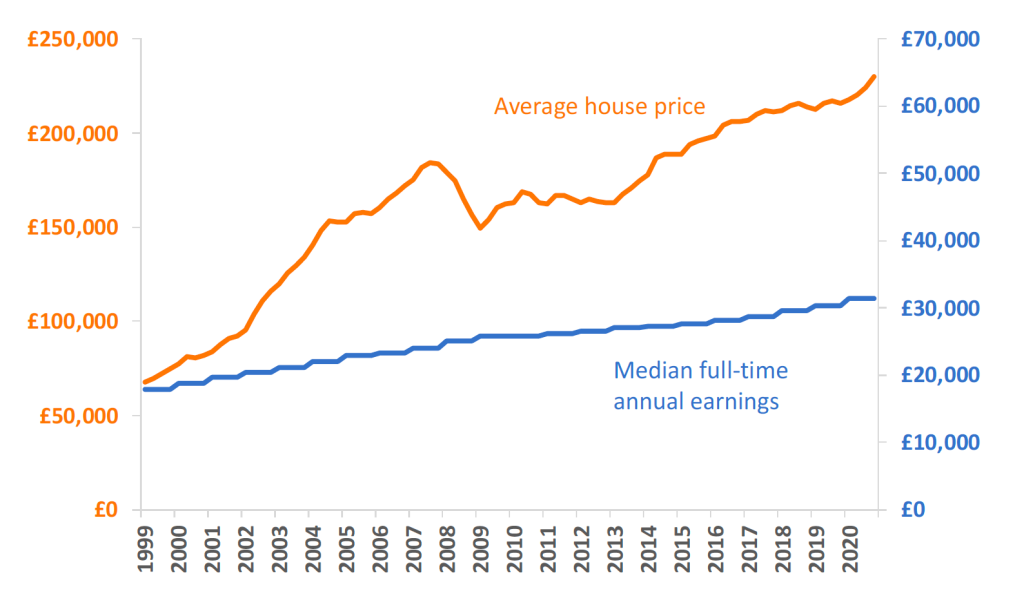

Those of us who boarded the housing ladder in the ’70s and ’80s have seen our property investments rise dramatically (as our charts show), far outstripping inflation and salary growth. The 1980 Housing Act enabled more than two million council house tenants to buy their homes at discounts of around 50 per cent[1]. Mortgage interest tax relief and ready capital through the ’90s until the financial crisis then made it easy for many people to build buy-to-let property portfolios on little equity.

House price rises have significantly outstripped increases in earnings over the last 20 years

Source: James Hambro & Partners Average price according to Nationwide and median full-time annual gross earning from ONS Annual Survey for Hours and Earnings

Generation X, as it is called, has been a lot less lucky. The average home now costs around seven times the average median full-time salary[2]. This generation will bear the brunt of the massive debts incurred by the cost of the 2020 virus, while the baby boomers sit comfortably in their smart houses with their final-salary pensions and equity ISAs that have been boosted by quantitative easing.

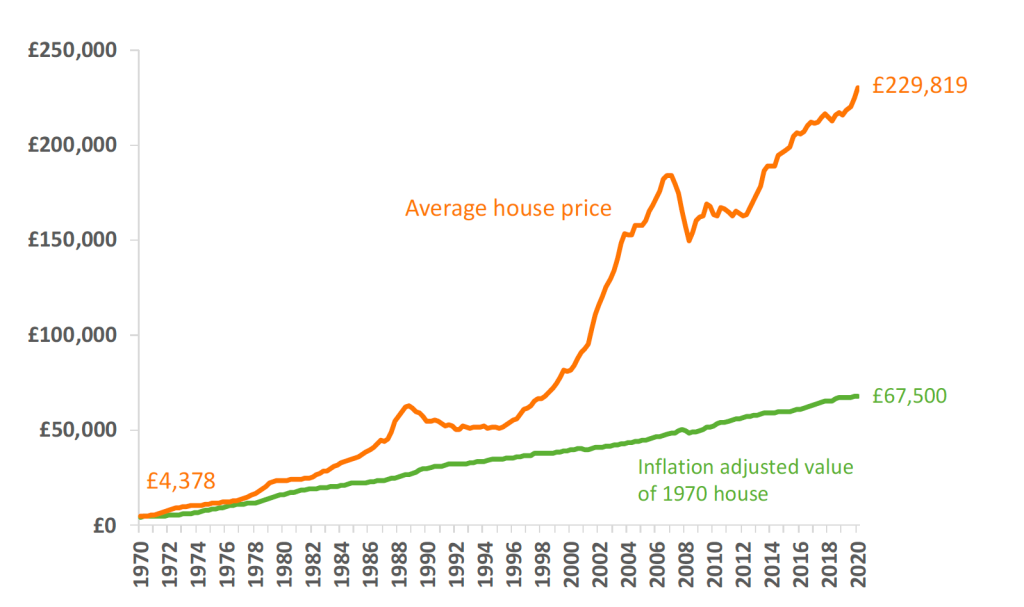

House price have outpaced inflation more than threefold since 1970

Source: James Hambro & Partners Average price according to Nationwide and inflation adjusted prices calculated using ONS Retail Price Index

The members of Generation X may be the first people since the Second World War to experience a worse standard of living than their parents. Is it enough to say “Tough luck”? Should there be some “rebalancing” between the old and the young? How should the Covid debt be paid for and by whom?

Though the Chancellor, Rishi Sunak, ruled out a wealth tax last July, the idea of a one-off tax is attracting growing interest in the press and within academia. Surveys suggest the public mood is changing towards such a tax – though generally on the assumption that someone else will have to pay it.

A recent report by the Wealth Tax Commission argued that the predicted deficit as a result of Covid-19 has doubled since July. It calculated that a one-off wealth tax on all individual wealth above £500,000 and charged at 1 per cent a year for five years would raise £260 billion (our deficit in 2020 was expected to be £394 billion[3]). At a threshold of £2 million it would raise £80 billion.

The report also suggested the Chancellor should assess wealth on the day he announces the tax. This would give the wealthy no chance to take steps to avoid it.

“One-off” taxes

I have difficulty thinking of a wealth tax as a one-off if it is repeated for five consecutive years. And I doubt it will end after five years. William Pitt introduced Income Tax in 1799 as a one-off tax to help pay the costs of the Napoleonic Wars (this after a wealth tax on houses, horses and carriages and servants and another new tax – inheritance tax – failed to raise enough[4]).

The principle of rebalancing wealth is a worthy aspiration if it creates more opportunities for the next generation. But there are serious issues with a wealth tax.

The first is collection. Many people are cash-poor and asset-rich. Will this mean evicting the elderly from their homes? How do you value assets? The French have an annual wealth tax on property, with a revaluation every four years (it helps explain why there are so many crumbling French châteaux). The administrative processes are in place there.

There is no system in the UK, so it will be a massive logistical exercise for us, involving lawyers, accountants, estate agents, investment managers, district valuers and the like.

The ever-expanding Tolley’s Tax Guide – most recent edition 45 chapters and a thousand pages – underlines how previous attempts to simplify Britain’s creaking tax system have failed. How many more pages will we need for the wealth tax?

Tax alternatives

So what is the alternative? There are easier ways to tax the wealthy. “Voluntary taxes”, like Inheritance Tax (IHT) and Capital Gains Tax (CGT), could be increased and loopholes tightened. But neither will make much of a dent in the massive borrowing under way by the government. So a small increase in VAT and/or income tax would be required in 2022/3 onwards if the economy has recovered by then[5].

Clearly, a priority has to be growth in the economy, with more personal spending in the short term and incentives to improve productivity and innovation in the longer term. If the UK is to be the Singapore of Europe then there must be incentives to create non-property wealth.

Never waste a crisis

Critically, any tax reform must be accompanied by a reduction in government expenditure. Boris Johnson likes to scatter cash – it is in his nature, as he wants to please everyone. He is not only spending a lot, but much of it is in the wrong places – such as on ego projects like HS2. Do we still need this in a working-from-home economy?

I believe a 10-15 per cent reduction in expenditure is possible over the lifetime of this government, if there is the political will to do it, without reducing essential services provided. The red tape created by endless well-meaning legislation is endemic. Look at the forms retired doctors and nurses were asked to complete to give the Covid vaccination. What an opportunity to slim it down.

It is right to think creatively about taxation, but we should think creatively about public expenditure as well. And we should not expect a silver-bullet solution to this problem. The answer lies in a complex balance of often radical initiatives.

Jamie Hambro is Chairman of wealth manager James Hambro & Partners.

This article first appeared in the Daily Telegraph.

[1] Joseph Rowntree Foundation: https://www.jrf.org.uk/sites/default/files/jrf/migrated/files/HRD28.pdf.

[2] The average median salary for a full-time worker in April 2019, according to the ONS, was £30,420 (or £585 per week). The average UK house price, according to the Nationwide house price index in Q1 2019, was £212,694. It has subsequently risen to £229,819.

[3] Office for Budget Responsibility: November 2020 Economic and fiscal outlook.

[4] UK Parliament: War and the coming of income tax.

[5] The Institute of Fiscal Studies estimates that a 1p increase in all rates of income tax, all National Insurance contribution rates or the main rate of VAT would each raise £6-7bn. A 1p increase in higher-rate income tax would raise about £1.3bn.

Posted on 19 January 2021

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.