Thomas Allsup, Portfolio Manager

For many investors, meeting company management has become unfashionable. Slickly choreographed executives are viewed as sticking so closely to the script that they leave no room to read between the lines. Worse still, sceptics fear that meetings can allow emotions to overrule ‘the facts’, with unwary investors sucked into ill-fated ventures based on nothing more than body language and the firmness of a chief executive’s handshake.

At JH&P, we have always thought differently. A 10-hour journey to Omaha, Nebraska, and a copy of William Thorndike’s 2012 classic, The Outsiders, provided a clear reminder of why.

Mirror, mirror, on the wall…

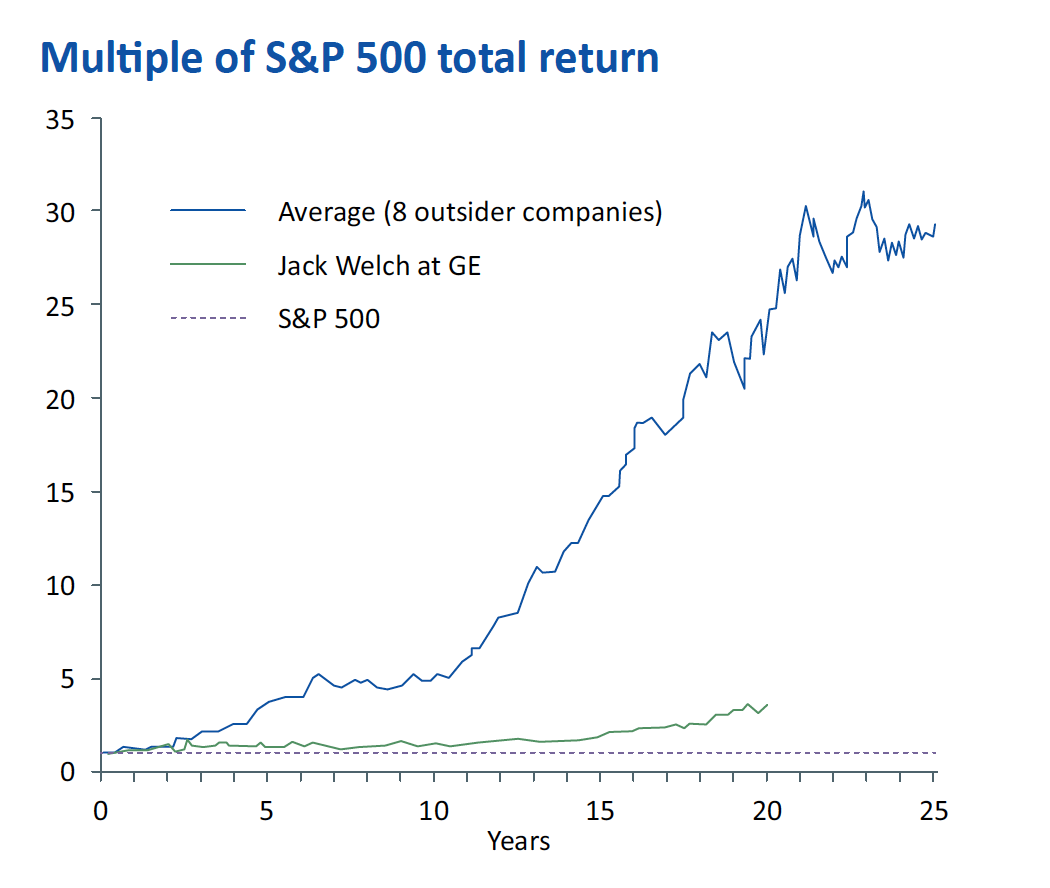

Ask experienced investors to name the best chief executive officer (CEO) of the past 50 years and many will nominate Jack Welch, of technology and financial services behemoth General Electric (GE).

Having started as an entry-level engineer, Welch was GE’s youngest-ever chief executive upon his appointment at the age of 46. Over his 20-year reign he earned a reputation for hard-hitting strategies, gaining the moniker ‘Neutron Jack’ for his policy of regularly firing the bottom 10% of staff. With expansive growth and rising profitability, GE vaulted up the corporate rankings.

While controversial, Welch’s leadership was highly rewarding for shareholders. Under his tenure from 1981 to 2001, $1 invested in GE stock would have grown into $48, a compound annual return of 21% during a period when the S&P 500 (the measure of the performance of the 500 largest US companies) averaged a 14% annual return.

Close but no cigar

However, Thorndike offers us eight chief executives, ranging from Katherine Graham of the Washington Post to Henry Singleton of Teledyne, who topped even the formidable Welch. In the process, he asks what there is to learn for those seeking managerial success or, like us, looking to identify future winners.

“It is impossible to produce superior performance unless you do something different.” – John Templeton

Lessons to be learnt

The eclectic group were all first-time CEOs, typically far younger than their peers and with little prior managerial experience. More of them had engineering degrees than MBAs. One, Bill Anders of General Dynamics, piloted the 1968 Apollo 8 lunar module and flew fighter jets in his spare time.

Operating out of bare-bones offices, they were united by their attention to detail and frugality. Legend has it that when Tom Murphy of media business Capital Cities was asked to paint his WTEN radio station in Albany to project a smarter image to advertisers, he painted only the two sides facing the road.

“Leadership is analysis.” – Bill Stirritz, Ralston Purina

All eight were analytical and independent, preferring their own thinking to the outside advice of management consultants and investment bankers. When Bill Stirritz’s Ralston Purina, the packaged goods company, was making a bid for RJR Nabisco, Stirritz arrived alone at one late-night due diligence session in Goldman Sachs’s offices, armed only with a yellow legal pad. He walked through his key operating assumptions one by one before making a final offer and going to bed.

However, these were no megalomaniacs. They operated highly decentralised operations, staying focused on deciding which promising new business shoots to water with further investment of time and money and which formerly prize-winning stalks to cut. They planned for the long term and paid attention to cash generation rather than the fickle quarterly earnings loved by Wall Street.

This required a remarkable ability to sit patiently and wait for the right opportunity. In the 1980s, Graham at the Washington Post refused to compromise on her returns discipline and made no acquisitions for nearly a decade when all her rivals were spending fast and loose. When her rivals’ over-reaching laid them low, Graham’s Post was left able to acquire the best assets at lower prices. Nearly all the CEOs shared this mix of patience and occasional boldness, with each making at least one acquisition or investment that equalled 25% or more of their own firm’s entire value.

“The goal is not to have the longest train, but to arrive at the station first using the least fuel.” – Tom Murphy, Capital Cities

Finally, they all recognised that size was not success. It is per sharevalue that matters, not increased revenues or earnings. If maximising per share value required the divestment of a once-cherished division, or the favouring of share buybacks over a showy acquisition, they didn’t hesitate.

The ‘who’ of business matters as much as the ‘what’

The Outsiders is a reminder that those at the top carry two of the greatest responsibilities: the efficient management of operations and the effective deployment of cash. Solely running numbers is insufficient when selecting companies for potential investment in portfolios.

The Berkshire Hathaway Annual Meeting

Meeting senior management allows us to test how well they understand their role and whether they have a credible plan to create long-term value for minority shareholders. Repeated meetings combined with repeated analysis enables us to check whether managements’ words are borne out in reality. And, finally, these meetings help us decide whether we are giving your money to people we trust.

Warren Buffett

We always try to hold these meetings before making an investment. In the case of my trip to Nebraska, the order had to be reversed – only by purchasing shares a year ago could I attend the Berkshire Hathaway annual meeting to listen to the CEO, Warren Buffett, perhaps the most effective capital allocator of all time and the subject of chapter eight of Thorndike’s book.

Reading about history’s greatest CEOs is a useful way of learning what qualities to look for in senior management. Meeting them is even better.

Posted on 10 July 2019

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made of given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions.

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. Fluctuations in interest rates may affect the value of your investment. The levels of taxations and tax reliefs depend on individual circumstances and may change. You should be aware that past performance is no guarantee of future performance.