07.07.2020

Will the next black swan be green?

Sarah Goose, Portfolio Manager, Responsible Investment Lead

The Covid-19 pandemic is arguably one of those ‘Black Swan’ events that spring upon us unexpectedly. As governments and central banks scrabble to address the extraordinary impact the virus is having on humanity, societies and economies, we continue to be reminded of another impending threat – climate change. Will the next black swan be green?

Sarah Goose, Assistant Portfolio Manager

It was scholar and statistician Nassim Nicholas Taleb who first used the term ‘black swan’ to describe a rare, unforeseen event that has extreme consequences – such as the 2008/9 financial crisis. With the benefit of hindsight, we can see these events as entirely predictable, but at the time they come as a shock.[1]

In January the Bank for International Settlements (BIS), the ‘central bank for central banks’, produced a book[2]warning that the next global financial crisis could be triggered by climate change – a green swan rather than a black one.

Here we look at just a few of the many issues shaping the investment aspects of the climate agenda and consider how they will influence our portfolio decisions in the coming months and years.

The regulatory challenge

We hear a lot about the risks that the changing planet brings to our ecosystem, nature and mankind. BIS’s publication frames the seriousness of the issue in terms of financial markets.

The authors warn that new policies needed to fight climate change and mitigate its effects will require unparalleled international coordination – incorporating governments, the private sector, civil society and the global community.

The authors warn that new policies needed to fight climate change and mitigate its effects will require unparalleled international coordination – incorporating governments, the private sector, civil society and the global community.

“Climate change represents a colossal and potentially irreversible risk of staggering complexity.” – BIS

They highlight the danger of ‘transition risks’– the problems caused by ‘potentially disorderly mitigation strategies’ that can increase systemic financial risk. In other words, policymaker errors.

We are already seeing significant regulatory change, much of which we believe is positive. We are now in what has been referred to as the ‘decade of delivery’ – the United Nations’ Sustainable Development Goals (SDGs) Summit in September last year concluded with world leaders calling for action to deliver the 17 SDGs by 2030.

In December, Europe proposed ambitious plans to join the UK’s pledge for carbon neutrality by 2050. The Green Deal for Europe outlines a multitude of policies to meet its target, with particular sections of the policy to be finalised in various stages throughout the next two years. Ursula von der Leyen, fresh into her new role as President of the European Commission, has described the deal as “Europe’s man on the Moon moment”.

This regulation requires drastic change at all levels of society – investors will need to be one step ahead and nimble in anticipating how companies will be affected, adversely and beneficially.

Alongside the Green Deal, the EU has announced new non-financial reporting regulations and a taxonomy for reporting sustainable activities. The importance of this latter proposal cannot be stressed enough. It requires financial market participants to classify environment-focused activities, products and objectives in a consistent way.

This seeks to address ‘greenwashing’ accusations, making it harder for firms to boast great environmental targets without a timeline or plan of action. This flexing of regulatory muscle will drive a big change in corporate philosophy and raise levels of disclosure, making it easier for investors to see which firms are genuinely addressing climate issues.

The UK’s Green Finance Strategy was announced prior to the EU’s proposals, in July 2019, and establishes a joint force with regulators, overseen by the government, to ensure a coordinated approach on climate-related financial issues. Disclosure is a fundamental principle of EU and UK plans alike. Companies can either be on the front foot with this or find it becomes an enormous headwind to growth.

The role of Covid-19 in accelerating ESG[3]

The past few years have seen company management teams begin to depart from the philosophy promulgated by economist Milton Friedman in the 1960s that their sole responsibility is the maximisation of shareholder value. We are seeing moves to incorporate a greater environmental and societal focus. Covid-19 has accelerated that shift.

Many companies have demonstrated their commitment to the S and G of the ESG triumvirate as they prioritise employees, customers and society over dividends and shareholder returns.

Covid-19 and lockdown have also boosted the move to decarbonisation and digitisation. As we emerge from lockdown, there is a powerful hope among many to ‘build back better’.

Enormous government spending is required to revitalise the economy. This presents a real opportunity to target money towards projects and businesses that help decarbonise the world. Calls for ‘green stimulus’ echo louder and louder throughout Europe, with the Green Deal hailed as central to Europe’s recovery strategy.

What will happen in the US?

The US has been an outlier among developed economies in its responses to climate change. Covid-19 has further widened the gap between what the US federal government and the EU are doing. Increasingly in the US, states have taken environmental matters into their own hands; indeed, companies and individuals have broken rank with the Presidential decree to produce their own ESG pledges.

The US presidential election could change that. We now know that Joe Biden is the Democratic challenger to the incumbent President, and the environment is a key focus in his campaign, emphasised by the recent release of the Democrats’ climate crisis action plan. A change of political stance within the White House on the environment could herald an inflection point that will reverberate through corporate America.

JH&P view – rising to the regulatory challenge

Unsurprisingly, the complexity surrounding the environmental challenge is already being reflected in financial markets. Fast-moving capital allocation decisions have led to sectoral divestment at one end and crowding at the other.

Sustainability sits at the core of our fundamental analysis of investments – we seek companies with sustainable business models and sustainability of returns. We believe we can have a beneficial impact through ownership of companies that are driving positive change, where demand is strong and consistent. We believe many of these companies will enjoy a tailwind from changing regulation and consumer preference. The companies of the future will surely be the ones that contribute to the future.

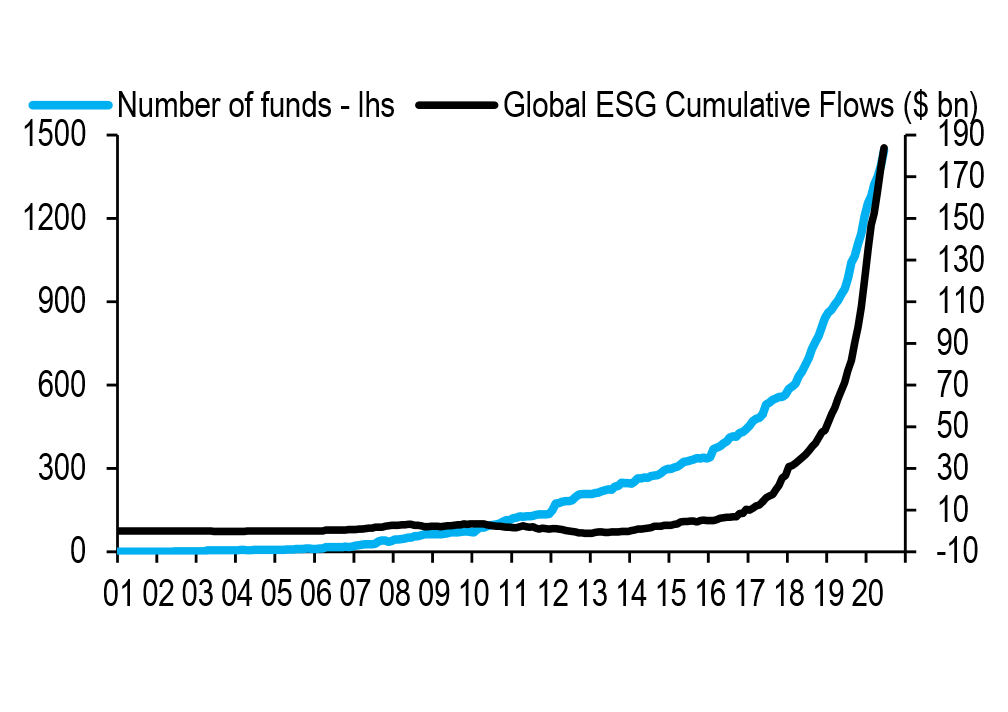

The flow into ESG strategies and stocks, particularly over the past 18 months and throughout the Covid-19 correction, highlights how individuals are taking action via their investments – an extension to other populist movements experienced across the world in politics and culture.

Global ESG funds have recorded record inflows in recent years.

It can be easy to be lured into areas of the market that are particularly ‘hot’, such as those playing into the more obvious ESG themes. However, we increasingly see value in ‘picks and shovels’ businesses – those mission-critical companies in the value chain that are perhaps further away from the ESG limelight but nonetheless crucial to the advancement of environmental targets. We find Europe particularly attractive for these types of investment.

The end of ESG

2020 is already a remarkable year. With so much regulatory change on the horizon, it may prove a turning point for the environment – and for investors. It is no longer enough just to avoid sin stocks. Sustainability must now be core to investment strategy for everyone. There may come a time soon when ‘ESG investing’ becomes simply ‘investing’.

James Hambro & Partners is a signatory to the Principles of Responsible Investment, the leading global network for investors who are committed to integrating ESG considerations into their investment practices and ownership policies.

By Sarah Goose

Posted on 7 July 2020

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.

[1] Taleb outlined the principles in his book. The Black Swan: The impact of the highly improbable. For centuries ‘black swan’ was used as a term – like ‘hens’ teeth’ – to describe something deemed impossible. The only swans known by Europeans were white. But in 1697 Dutch explorer Willem de Vlamingh discovered black swans on a river in Western Australia.

[2] See The Green Swan: Central banking and financial stability in the age of climate change, by the Bank of International Settlements.

[3] ESG = Environmental, Social and Governance.