DÉJÀ VU ALL OVER AGAIN

The View in Short

A Familiar Shock to a Constructive Backdrop

The year began with improving economic momentum. Falling interest rates, sustained AI related capital spending and early signs of industrial recovery were setting the stage for a broadening of market returns. This outlook was abruptly disrupted at the end of February by US and Israeli airstrikes on Iran, reviving geopolitical uncertainty and refocusing attention on energy markets.

OIL IS THE TRANSMISSION MECHANISM

The most immediate risk from the conflict is oil. Sustained prices above $100 would weigh on global growth, although futures markets continue to imply any disruption will be temporary. The longer flows through the Strait of Hormuz remain constrained, the greater the risk of knock on effects across fertilisers, plastics and wider supply chains, particularly for energy dependent Asian economies.

NOT 2022, BUT MORE FRAGILE THAN IT LOOKS

Concerns of a repeat of 2022 are understandable but overstated. Monetary policy is more restrictive, labour markets are softer and household financial buffers are far smaller than four years ago. These differences suggest slower growth rather than an inflation shock is the more likely outcome, though the margin for error is slim.

POLITICS MATTER AS MUCH AS ECONOMICS

Markets have stabilised on the belief that political incentives will limit escalation. With US midterm elections approaching and public support for intervention weak, sustained high oil prices are politically unattractive. Trump’s familiar pattern of reverse, delay and soften remains plausible, but uncertainty also remains elevated.

A SUPPLY-SHOCK WORLD HAS CHANGED PORTFOLIOS

Covid, Ukraine, tariffs and now Iran underline that supply shocks are no longer exceptional. These tend to weaken growth while fuelling inflation — a difficult mix for traditional portfolios. Bonds, once a reliable hedge, have repeatedly failed to diversify equity risk this decade.

DIVERSIFICATION NEEDS TO LOOK DIFFERENT

With bonds offering less protection, resilience increasingly comes from diversification across assets, sectors and geographies. Short dated and selectively inflation linked bonds retain a role, but defence is now found in real assets, gold, alternative strategies and careful equity composition.

THE RETURN OF THE REAL ECONOMY

Equity leadership is broadening. Capital intensive and asset heavy sectors, long neglected during the era of cheap money, are regaining relevance. Industrial automation, electrification, energy infrastructure and reshoring are driving a multi year investment cycle. International markets, with greater exposure to these areas, are increasingly well positioned.

CONSTRUCTIVE, BUT NOT COMPLACENT

The most likely outcome remains a prolonged ceasefire and limited lasting economic damage. However, today’s economy is more fragile than in recent years, and portfolios must reflect that. Over the past year we have adapted positioning to balance participation in long term structural growth with greater emphasis on resilience in an increasingly volatile world.

DÉJÀ VU ALL OVER AGAIN

The first few months of the year played out largely as hoped.

Last year’s supportive pillars such as heavy capital investment related to Artificial Intelligence (AI) and falling interest rates remained firmly in place, while headwinds like tariffs, fiscal drags and inflation were beginning to reverse. Economic data improved, interest rate expectations eased and industrial activity showed signs of recovery.

The US midterm elections later this year suggested the Trump administration would use all the tools at their disposal to maintain momentum, paving the way for a broadening of returns after several years of unusually narrow market performance.

This changed suddenly on 28th February, when US and Israeli airstrikes on Iran created a new round of geopolitical uncertainty. The immediate market concern has been higher oil prices which, if sustained, could slow the global economy potentially to the point of recession. Portfolios need to account for a more fragile outlook.

We have been here before. Early 2025 saw a similar combination of solid growth, lower interest rates and green shoots of cyclical recovery upended by President Trump’s ‘Liberation Day’ tariffs. Much like last year, unexpected, unpopular and seemingly ill-conceived Trump policy threatens to derail the previously constructive outlook.

That said, today’s environment shares several of the strengths that helped markets absorb previous shocks. Fiscal policy remains supportive, industrial activity is showing broader signs of recovery and a multi-year capital investment cycle is increasingly evident across energy, infrastructure and manufacturing. As we set out later, while geopolitics may yet dictate the path of markets in the short term, the longer-term drivers of portfolio returns remain firmly intact.

IRAN CONFLICT: IMPLICATIONS FOR OIL, INFLATION AND MARKETS

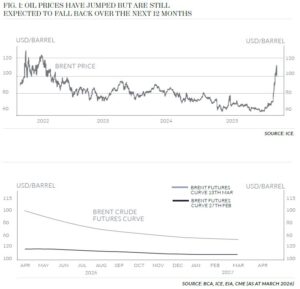

The oil market remains the most immediate focus for the global economy. Economists estimate that a Brent Crude price sustained over $100 is needed to materially slow the US economy, with the global economy’s sensitivity to oil prices much lower than in the 1970s.

At the time of writing prices sit around those levels, having increased by over 50% since the start of the war, albeit futures markets imply that prices should fall back over the next year, suggesting investors don’t expect a prolonged supply disruption (Fig. 1). However, each successive day of conflict threatens months of impact on the global economy – it can take several years to rebuild what is destroyed in only a few days.

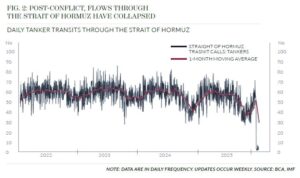

The biggest risk for markets is that the Strait of Hormuz, a chokepoint through which 20-30% of global oil and gas supply typically flows, remains closed for much longer than is currently expected (Fig. 2). If disruption persists, the impact will extend beyond the energy market. Hydrocarbons are not only used as energy sources but also as vital inputs for other materials, most notably plastics and fertiliser.

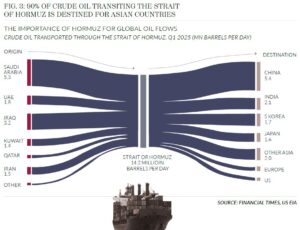

Asia faces the greatest vulnerability to supply-chain disruptions, given its outsized dependence on Middle Eastern energy (Fig. 3). The response across the continent has been swift and defensive: China has mandated a freeze on fuel exports, South Korea has implemented its first fuel price caps in three decades and Bangladesh has resorted to closing universities to curb energy consumption.

Donald Trump’s unpredictable announcements and inconsistent hyperbolic messaging have further clouded the outlook, albeit markets have been stabilised by growing confidence that Trump is indeed looking for an off-ramp.

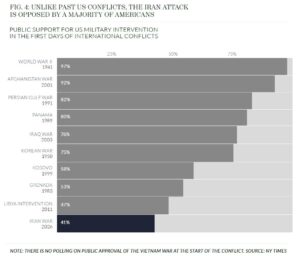

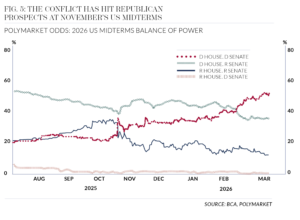

With the upcoming mid-term elections likely to be fought on the topic of affordability and his approval ratings falling, the US President has little appetite for persistently high oil prices driven by an unpopular foreign policy intervention (Fig. 4). It won’t escape Republican attention that since the onset of the conflict a Democratic sweep of both the House of Representatives and the Senate has become the most likely outcome in November (Fig. 5). Political realities would suggest the President’s historic policy pattern of ‘reverse, delay, soften’ remains a likely blueprint.

2022 REDUX?

Although there is ongoing optimism for a diplomatic solution, recent attacks on production facilities throughout the Gulf have heightened the potential for sustained disruption to supply and with it a more sustained rise in energy prices.

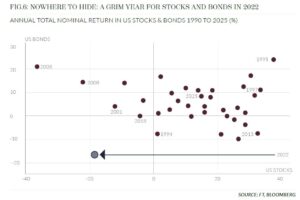

The last bout of geopolitically driven energy price inflation in 2022 left balanced portfolios nursing steep losses with both equities and bonds falling in tandem (Fig. 6). Inflation surged as the post-pandemic reopening mixed with Russia’s invasion of Ukraine. Concentrating on ‘transitory’ supply issues, central bankers were slow to respond, keeping policy too loose and arguably contributing to the higher peak and settling level of inflation we still wrestle with today. Four years on, geopolitical turmoil playing out through energy markets naturally raises worries we are headed for a repeat.

The comparison is understandable but imperfect.

Today, most agree interest rates worldwide are mildly restrictive, a far cry from the ultra-loose policy entering 2022. Recent history hangs heavy too. At their March meeting, US Federal Reserve (the US central bank often referred to as ‘the Fed’) Chair Jerome Powell’s lukewarm support for looking through upcoming energy price impacts suggests that five years of missing their inflation targets is clearly bothering the Federal Reserve Board. It may take signs of genuine economic weakness before the Bank is willing to provide the interest rate cuts most had expected entering the year.

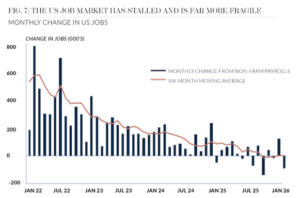

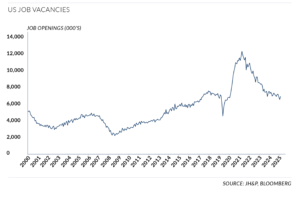

Labour markets also look very different. In 2022, the employment market was booming and companies were struggling to hire, with real wages surging. In contrast, the last 12 months have seen jobs growth stall and workers worry about AI related disruption, while there is a much smaller pool of vacancies to mitigate a slowdown before actual job losses occur (Fig. 7).

Household finances are also in a weaker position. Excess savings and government hand-outs built up during the pandemic have largely been spent, meaning consumers have less ability to absorb higher prices.

The buffers between the US economy and a recession look less robust today than four years ago, suggesting the bigger risk of the oil shock is slower growth rather than a repeat of the 2022 inflation surge. We still expect the most likely outcome to be a prolonged ceasefire and limited lasting global economic damage, but portfolios need to account for a more fragile outlook and heightened uncertainty.

A SUPPLY SHOCK WORLD NEEDS DIFFERENT LINES OF DEFENCE

The investment environment has shifted meaningfully. Over the past five years, investors have faced a series of supply shocks from Covid to Ukraine, tariffs, immigration pressures and now Iran. As we wrote last year, tariffs, labour shortages and geopolitical fallouts have a nasty habit of both weighing on growth (which is bad for equities) and stoking inflation (which is bad for bonds).

After presiding over five years of higher-than-targeted inflation central bankers are both less able to look through these shocks and less likely to respond pre-emptively to signs of faltering demand.

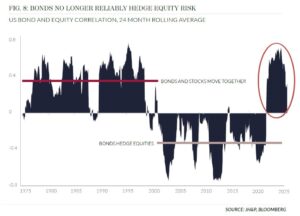

This matters because for most of the past two decades, bonds reliably provided diversification when equities fell. This decade however, that relationship has reversed (Fig. 8).

With bonds no longer as reliable a source of insurance, portfolios need to have exposure to a wider range of holdings across sector, geography and asset class to build resilience.

We have retained our long-held cautious view on bonds, with selective holdings focused on shorter-term issues and those with cheaply priced inflation-linked characteristics. Instead, we continue to look for portfolio diversification and defence in different areas, such as hedge funds, gold and real assets with inflation linked cash flows. Equity allocations fall in this latter group, and we have been more active than usual in adjusting the underlying composition as we adapt to an investment environment that is markedly different to the pre-covid world. The rapidly shifting sands and increasing influence of policy on markets means we expect that we will need to continue to be nimble and dynamic in portfolios.

REVENGE OF THE REAL ECONOMY: WHY ‘OLD ECONOMY’ SECTORS ARE REGAINING LEADERSHIP

2025 marked a pivotal shift in equity markets. For many years, US equity markets and technology stocks dominated returns.

For over a decade following the 2008 Financial Crisis, a combination of low interest rates, low inflation and low growth burnished the credentials of companies with dependable growth not reliant on either economic acceleration or substantial capital investment. Such ‘quality’ or ‘capital-light’ companies formed the core of JH&P portfolios and benefited from twin tailwinds of increasing earnings and rising valuations.

In contrast, across more capital-intensive industries, zero interest rate policy allowed weaker competitors to survive, delaying consolidation and suppressing pricing power. With governments firmly in austerity mode following the 2008 financial crisis there was little investment into infrastructure and capital. While many of these companies traded at cheaper valuations, the low capital returns generated across much of the period meant they stayed just that.

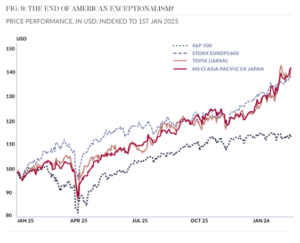

Yet last year the US market underperformed compared to other major markets in both local and dollar terms despite rising 15% (Fig. 9). While technology stocks performed well, they were outdone by many old economy sectors, particularly outside of the US.

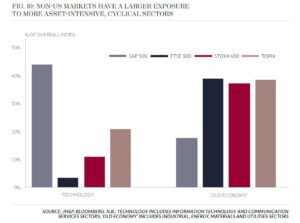

These dynamics appear to be strengthening in 2026. ‘Big Tech’ has stalled as spiraling investment plans are being met with increasing investor scepticism. Near daily announcements from AI model leaders Anthropic and OpenAI have dented share prices across software and professional services sectors. Meanwhile, investors are rotating from ‘AI losers’ to ‘real asset’ winners. The happy recipients of data centre capex are powering higher, while physical-asset-heavy businesses deemed less at risk of imminent AI-driven disruption have provided refuge as governments seek to tempt industry onshore and embark on fiscal priming of core infrastructure. For once, the more traditional composition of international markets is proving an advantage (Fig. 10).

Atoms over bits, steel over software, megawatts over megabytes. This shifting market zeitgeist reinforces the theme of industrial renaissance we have highlighted for several years. From a structural perspective, multiple pieces are falling into place.

Labour shortages are encouraging companies to invest in automation. Spending on AI infrastructure is expanding into power stations and the electricity grid, policymakers are incentivising housing and infrastructure development due to political imperatives, and heightened global tensions are focusing a rethink on energy resilience and leading to the local reconstruction of supply chains. This has the potential to reverse decades of increasing competitive intensity across asset-heavy sectors, protecting local champions and leading to an inflection in future returns for many perceived ‘commodity’ providers.

Our expectation of a sustained period of industrial and technology investment has become one of the key themes across client portfolios, offering a broad swathe of attractive opportunities across the industrial, materials and technology sectors. We have been investing in and reviewing a broad range of potential beneficiaries.

For example, Amphenol’s market leading portfolio of advanced interconnect systems, sensors and antennas provide the roads, power lines and plumbing a data centre needs to move massive amounts of information between servers at lightning speed. As AI chips and servers become more computationally intensive and power hungry, the connector and cable requirements become increasingly complex. This directly benefits Amphenol’s content per site and has been the driving force behind the company’s recent explosive growth. While data centres provide the excitement today, our recent meeting with management emphasised that Amphenol is far from a one-trick pony. The modernisation of physical assets has the potential to drive incremental connector and sensor demand throughout the manufacturing industry, and the company is exposed to rising electronic content across industrial, automotive, aerospace and defence systems which could continue even when the AI hype has subsided.

In aerospace, Safran remains supported by structurally rising engine aftermarket volumes. Supply chain interruptions during the pandemic and multi-year backlogs at Airbus and Boeing have forced airlines to defer retirement of existing planes. Fleets are being stretched with higher engine utilisation tying directly to lucrative servicing revenues for engine manufacturers like Safran. Rising geopolitical tensions have also transformed the outlook for the group’s defence division.

Meanwhile, Emerson is enjoying robust demand for automation and process control upgrades as companies attempt to offset labour scarcity through productivity enhancing tools, while AMETEK has seen a broadening recovery in its test, measurement and automation franchises as customers reinvest in safety critical and compliance driven equipment after years of deferrals.

The industrial upturn also extends into semiconductors. Texas Instruments, with its growing domestic manufacturing footprint and exposure to power management, sensing and embedded processing, is positioned at the intersection of onshoring, electrification and equipment modernisation. At the same time, Linde should continue to demonstrate that industrial gases remain a royalty on progress. Demand for high purity hydrogen, nitrogen and specialty gases is strengthening across semiconductors, advanced manufacturing, clean energy projects and chemicals. Linde’s long term, contract based model provides visibility across multiple industrial end markets and should be a natural beneficiary of a capital investment cycle that is becoming more structural, more global and more sustained.

In infrastructure, Siemens Energy has twin tailwinds of AI data centre power demand and the multi year rebuilding, hardening and digitalisation of electricity grids as governments prioritise energy security and system resilience. CRH, one of the largest integrated construction materials and infrastructure solutions providers, is seeing tailwinds from US federal spending, state level transportation programmes and the early stages of private sector reshoring investment. Its exposure spans roads, data centre foundations, warehousing, commercial buildings and critical infrastructure, making it a useful bellwether for the breadth of the construction led capex cycle now taking shape.

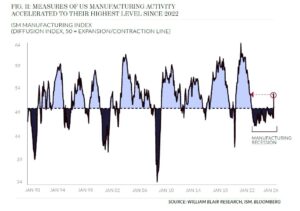

To date, many of these trends have been offset by higher interest rates and the lingering effects of the post pandemic surge in demand. However, after three years of recession-like conditions, broader manufacturing and industrial activity finally looks to have reached an inflection point, supported by rising orders, low inventories and improving upstream indicators (Fig. 11).

This manufacturing revival is not without hurdles, the most significant being the reliance on affordable energy and secure supply of raw materials. Against this backdrop, events in the Middle East are of even greater significance. Historic underinvestment in grid capacity and broader infrastructure underpin the need for long-term investment but also limit the pace of progress. Yet while these constraints may cap the speed and scale of the industrial expansion, they are unlikely to derail it over the decade ahead.

HOW WE ARE POSITIONED

We have been more active than usual over the past year in response to the rising political and market volatility.

Recent additions have focused on AI-enablers such as ASML, Polar Capital Global Technology and Siemens Energy, industrial capex cycle beneficiaries like Safran, CRH and Emerson, as well historically more pedestrian businesses like Lloyds and US drug distributor McKesson where relative competitive positions and growth outlooks are improving. Alongside our direct stock changes, additions to third-party funds have bolstered exposure to Asian markets and more capital-intensive, cheaper old-economy sectors that look both more protected from AI disruption and well-placed to benefit from faster, more industrial-led, economic growth.

These changes have resulted in stronger, more resilient portfolios with greater diversification across regions, sectors and investment style, reflecting an evolving investment environment that offers a greater range of growth opportunities albeit one in which many industries are undergoing rapid change and the threat of technological change. Pleasingly, the adjustments have not come at the cost of valuation. The look-through valuation of portfolios has rarely been lower in absolute terms and sits at its smallest premium relative to the world market in a decade. Current consensus estimates from Bloomberg suggest our companies should be capable of delivering earnings growth in the high teens over the next two years, well ahead of the wider market. If the companies can deliver, portfolio performance should follow too.

Despite the recent rise in geopolitical uncertainty, we believe today’s risks are manageable. While more fragile to shocks, the US economy entered this period on a sound footing. Fiscal policy is supportive following the new US tax bill, the global industrial sector is showing broader signs of recovery as part of a multi year capital investment cycle, and productivity growth appears to be picking up. We expect these forces to reassert themselves if there is a near term resolution in the Middle East which allows for the prospect of supply chains to reopen. The underlying drivers of these forces have not been undermined by recent events and the experience of last year’s trade shock highlighted markets and the global economy’s ability to absorb and rebound from self-inflicted policy crises.

Article written by Dan Zegleman, Portfolio Manager.

This document is a Financial Promotion for UK regulatory purposes and is directed only at investors resident in the United Kingdom.

This document does not constitute investment advice or a recommendation.

Past performance is not a reliable indicator of future performance. The value of investments, and the income from them, may go down as well as up, so you could get back less than you invested.

This material has been issued and approved in the UK by James Hambro & Partners LLP, which is authorised and regulated by the Financial Conduct Authority and is a registered investment adviser of the Securities and Exchange Commission. It is listed in the Financial Services Register with reference number 513246. James Hambro & Partners LLP is a limited liability partnership registered in England & Wales with number OC350134 and registered office at 45 Pall Mall, London SW1Y 5JG. A list of members is available on request. The registered mark James Hambro® is the property of Mr J D Hambro and is used under licence.