Sean Jones, Financial Planner

We know the government is racking up a huge debt for its response to Covid-19. We weren’t expecting the bill to land in the Budget, but we know it’s coming. Today Rishi Sunak began to flag up who will pay for it and how.

First, let’s look at the debt. Borrowing is at its highest outside wartime. The budget deficit is likely to be £280 billion this year, and public sector net debt is forecast to rise to £2.8 trillion by 2025/26.

The government had little option but to spend as it has. The economy shrank by 10% last year – the largest fall in 300 years; 700,000 people have lost their jobs since March.

But recovery is coming. The OBR expects the economy to return to pre-Covid levels by the middle of next year.

The Chancellor has a difficult job in building the momentum behind that recovery. Today he announced a raft of extensions to support schemes that can keep businesses hanging on in there until we are all vaccinated and some sense of normality has resumed.

And so to that bill. There were two key announcements that might affect clients significantly.

The freezing of allowances until 2025/26

The income tax threshold will rise in April to £12,570. The 40% higher-rate tax will kick in at £50,270 and then both will remain frozen there till the end of this Parliament in 2025/26. That is expected to generate the Treasury £1.5 billion next year but will rise to £8.1 billion a year by the next election, demonstrating just how many people will be caught by this freeze.

Inheritance tax thresholds will remain at today’s level, generating £445 million a year by 2025/26. The Capital Gains Tax Annual Exempt Allowance freeze, at £12,300, will raise just £30 million a year. Junior ISAs and ISA allowances, unsurprisingly, have also been frozen.

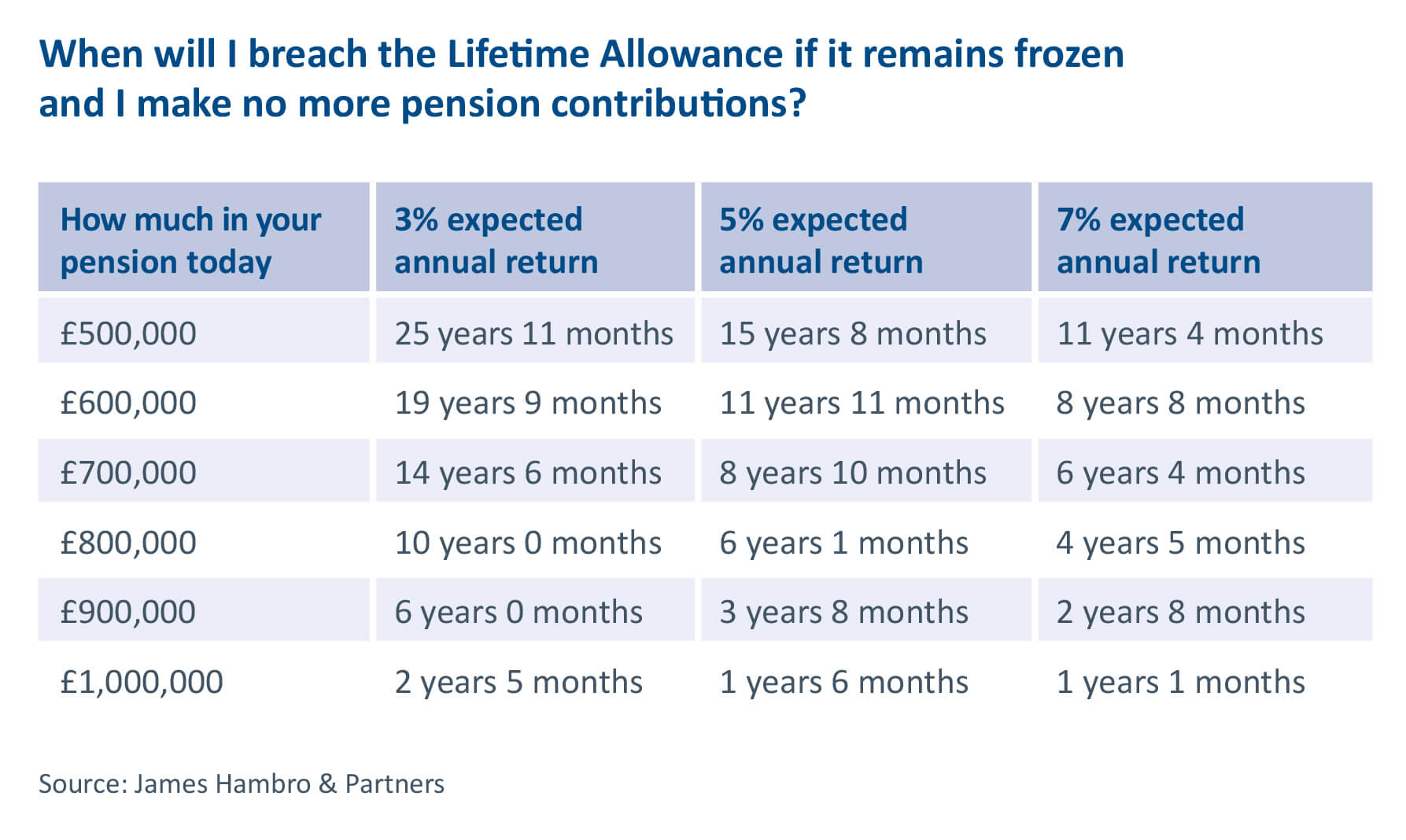

The freezing of the Pensions Lifetime Allowance at today’s rate of £1,073,100 – remember it used to be £1.8 million – will generate £300 million a year for the Treasury by 2025/26. It really doesn’t seem worth it, given how complex this charge is to understand and administer.

Over time, though, this may come to be a major earner for the Chancellor. As our table below shows, it won’t just hit the super-rich. In the coming years it’s going to affect many ordinary people, including teachers and civil servants, who have worked for a long time in skilled jobs with final salary pension schemes.

A growing number of people are going to have to think about this in their retirement planning. We have written elsewhere about whether you should worry about this charge. You should certainly think about it and discuss it with your adviser.

Though he didn’t use these words, the Chancellor was keen to stress that these tax freezes aren’t a stealth tax. He was being explicit about them. “We are not hiding it, I am here, explaining it to the House and it is in the Budget document in black and white. It is a tax policy that is progressive and fair.”

Corporation tax increases

The other big tax increase is in corporation tax. This will rise from 19% to 25%. Small businesses with £50,000 or less of profits will be taxed at 19%, and it will be tapered up. Only those with £250,000 of profits will be taxed at the full rate. The Chancellor was keen to point out that this is just one in 10 companies.

Of course, this will affect nearly all of us who have pensions and who rely on these companies to either reinvest their profits in further growth or distribute them as dividends, but we shall overlook that.

The rise in corporation tax is expected to generate £17 billion in revenue by 2025/26. The new rate is still lower than that paid by companies in other G7 countries, and there’s no sense that cutting corporation tax did much to stimulate inward investment in the UK.

Balancing the books

The thing that strikes you when you look at these headline numbers is that these tax rises and freezing allowances don’t generate that much when compared with the £280 billion budget deficit and the £2.8 trillion debt.

The hope is that other measures mentioned today to stimulate the economy will also generate plenty of tax revenue. Certainly there were some interesting initiatives announced, like the free ports and the ‘super deductor’, which allows businesses to reduce their tax bill by 130% of their investment in new qualifying plant and machinery – part of a drive to improve Britain’s productivity.

The Chancellor also flagged up some interesting environmental initiatives, like a voluntary carbon offsetting scheme. We look forward to seeing more on that.

If these initiatives don’t kick-start a vibrant, low-carbon British economy then we can expect more tax rises and public spending cuts. You can’t help feeling that what we heard today, unpleasant as it might be for some people, was just a taster of what’s to come. But how else do we pay for Covid?

The key takeaway is that good tax planning will become more important than ever. There are ways to mitigate some of these creeping taxes, and the sooner you address these issues the better. Do call your financial planner if you have any concerns.

By Sean Jones, Financial Planner

Posted on 3 March 2021

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.

Image: Guy Corbishley/Alamy