Sean Jones, Financial Planner

It’s one of the most complex tax charges on the records – you virtually need a degree in financial planning to understand it. And it’s slowly creeping up on more people. The Lifetime Allowance is the amount you can accumulate in pension savings over your lifetime without incurring any punitive tax charges.

The standard Lifetime Allowance is currently £1, 073,100 and, in the wake of the budget, will remain frozen at that level until 2026 at least. If you go above that, you face a penalty.

The government wants us to save for retirement so we don’t turn to the state for benefits when we stop working. It offers us generous tax perks to encourage that – effectively paying us back all our income tax on earnings saved into a pension. The chancellor thinks that once you’ve got £1,073,100 in your pension, you don’t need these benefits, and he would like the money back on the excess. You pay 25% on any money you withdraw as income, and 55% on any lump sum.[i]

You aren’t actually tested for the charge until one of the following three events occur:

- You take money from your pension that is above your remaining Lifetime Allowance – either as a lump sum or income (this is known as ‘crystallising’ your pension).[ii]

- You die before 75.[iii]

- When you get to 75.[iv]

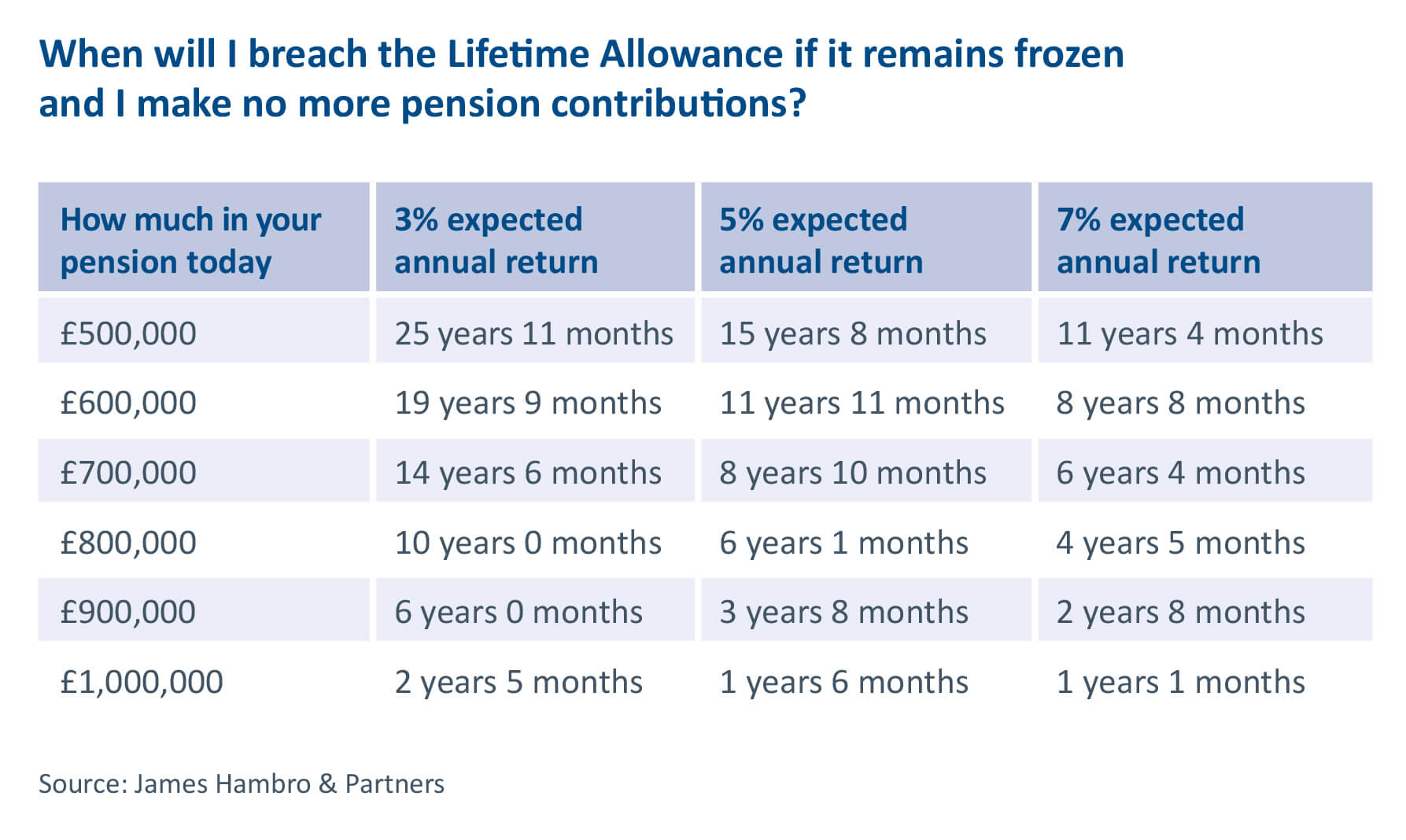

Creeping up on people

Lots of people are likely to reach this limit, simply through growth. Anyone with an uncommuted final salary pension of over £53,655 is in this territory because HMRC calculates the value of these pensions by multiplying the defined benefit by 20. Our table below shows just how quickly you might find yourself breaching the Lifetime Allowance.

So should I stop putting money in my pension?

Many people looking at these figures will be tempted to stop saving into their pension. If you are in this scenario it is worth taking advice.

I would say be careful about stopping too soon. You may find that illness forces you to retire early and so you have needlessly stopped saving tax efficiently. Money in your pension grows free of all taxes and is free of Inheritance Tax (IHT) when you die. These can be substantial benefits.

Remember, markets can go down, too. We may have a couple of years where there is “negative growth” and your pension could fall.

The general advice is that it is sensible to stop paying contributions into your pension if you’re nearing the limit. However, there are a number of scenarios where that would not necessarily be wise.

Scenarios where you might carry on paying into your pension, even if you are approaching or over the LTA

- Free money from your employer: If your employer is paying into your pension and will not give you the benefit any other way, then you might as well continue to take it, even though you may be taxed punitively. It’s better than nothing! But do ask your employer if they will pay it as taxable income instead.

- If you are a higher-rate tax payer and salary sacrificing: If you salary sacrifice your pension contribution, the money goes straight into your pension pot without you seeing it. This means you do not pay the 40% income tax, and you do not pay National Insurance (NI), at 2%. So you are enjoying a 42% benefit. If you salary sacrifice your employer saves 13.8% in NI too and some of them will add this to your pension, bringing the tax saving to over 55% in this scenario. This money is exempt from IHT so you may prefer to have it in a SIPP.

- If your salary is between £100,000 and £125,000: For every two pounds you earn above £100,000 you lose one pound of your tax-free benefit. That means earnings in this bracket are effectively being taxed at 60%. So if your taxable income, after allowing for charitable donations, is over £100,000 you might consider paying this element into your pension.

- If you own your own company and are a higher rate taxpayer: Contributions that are salary sacrificed into your pension come off the company profits, so they reduce your corporation tax bill, making it an effective way to take profits tax efficiently. This is an additional factor to include within any calculations.

- If you’ve earmarked your pension savings for your children: If you don’t need your pension income, and see that pot as earmarked for the next generation, you can be growing it tax efficiently. At 75 if you have any uncrystallised benefits you will pay a 25% charge on anything over the LTA. The money then passes to them on your death IHT-free and they pay tax on it at their marginal rate of tax.

What can I do to mitigate or reduce the risk of breaching the Lifetime Allowance?

It’s worth pointing out that there are various forms of Lifetime Allowance protection which mean you may be entitled to a higher personal Lifetime Allowance than the standard rate. If you (or anybody on your behalf) have not made any contributions to a pension since 5th April 2016, you may be able to claim a personal Lifetime Allowance (LTA) of £1,250,000 in the form of Fixed Protection 2016.

There are some steps you may want to talk through with your adviser.

Taking the tax-free lump sum: Before you breach the LTA, if you are 55 or over, you might consider taking your 25% tax-free lump sum in one go. So if you had £1 million in your pension and did that, you would have £250,000 tax-free cash and £750,000 in your pension. You are considered to have crystallised £1m. You would have £73,100 LTA left. You can invest the £250,000 elsewhere, feeding £20,000 a year into your ISA, perhaps, or investing it and using your capital gains tax allowance each year through careful annual disposals and reinvestments. You will lose the IHT benefits on this £250,000, but the growth on this portion of your savings will no longer be liable for an LTA charge.

Taking income: If you manage your pension carefully and are old enough to crystallise it, you can take taxable income from your pension each year to prevent it from breaching the LTA, or at least mitigate any final LTA bill. Once you take income, you are restricted as to how much you can contribute in to money purchase pensions each year to just £4,000.

Take advice

As you can see this is fiendishly complex. There are so many factors to take into consideration – like your age, how much savings you have elsewhere or whether you’re married or in a civil partnership. You might well ask why any Chancellor ever thought such a charge sensible. It is surely simpler to limit how much people put into their pension, rather than penalising their success at investing their money wisely.

If he really wanted to clobber pension savings he could just remove the IHT benefits. Lots of us would be upset by that, but at least we would be able to understand it.

If you are affected by the LTA it is wise to take advice. Unfortunately, the rules on pensions keep changing, so this is something many people will have to keep an eye on – at least until someone has the sense to scrap it.

By Sean Jones, Financial Planner

Posted on 3 March 2021

[i] So if you are £10,000 over the lifetime allowance and take that money in one go, HMRC will charge you 55% and you’ll be left with £4,500. If you take it as income, you are charged 25% on the money as you withdraw it, and then income tax at your current rate. If you are a higher rate (40%) taxpayer, you’ll be left with the same amount – £4,500. If you can keep your retirement income within the 20% basic rate taxpayer threshold (which is below £50,000), you are better taking the money as income. You’ll pay 25% = £7,500, then 20% income tax (£1,500), leaving you with £6,000. This is where higher-rate taxpayers would have been if they had not had the 40% uplift when they were saving money into their pension. That sounds vaguely plausible, doesn’t it? But what a complicated way to get there! Accepting the 25% charge is usually the best thing to do.

[ii] At this point you are charged on the proportion of the fund that is over the LTA (after you’ve accounted for your 25% tax free allowance, which is generally 25% of the LTA – currently £268,275). So if you crystallise £100,000 and you are £30,000 over the LTA, the charge is applied on the £30,000.

[iii]At this point any uncrystallised pension over the LTA is taxed at 55%, so it may be worth crystallising the pot early to ensure this does not happen. If the pension is already in a drawdown contract when the member dies, or can be designated to drawdown, then the 25% tax charge can apply to any excess above the member’s remaining LTA.

[iv] At this point any uncrystallised pension is charged at 25%. You are also tested on growth on any drawdown contract.

Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made or given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions (but so that nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently).

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. You should be aware that past performance is not a reliable indicator of future results. Tax benefits may vary as a result of statutory changes and their value will depend on individual circumstances.