13.02.2017

Is it time to invest in Japan?

Rosie Bullard, Partner, Portfolio Manager

Equity markets are difficult to judge at the moment, with many on record highs, but one which stands out as more compelling than most is Japan, where the price/earning ratio is at its lowest for almost a decade and Prime Minister Shinzo Abe’s stimulus measures continue to underpin the economy. Is it time to invest in Japan?

In late January, the Bank of Japan forecast that GDP growth would accelerate and remain above trend into 2019 on the back of Abe’s three-pronged programme of economic reforms and expectations of a weakening Yen and improving exports.

Abenomics, which began in 2012 and is characterised by Abe’s so-called ‘three arrows’ of fiscal stimulus, monetary easing and structural reform, has resulted in the lowering of interest rates and bond yields (accompanied by Yen depreciation of over 40% against the dollar since late 2012). This has been good for equities – in Yen terms the Nikkei returned 129% from October 2012 to the end of January 2017, while the 10 year Japanese Government bond yield, which was around 0.8% in October 2012, has dropped closer to 0.1% today.

Meanwhile, structural reforms are transforming Japan’s long stagnant corporate sector and supporting growth in equity ownership.

Japanese companies are being encouraged to improve efficiency, productivity and return on equity – to invest for growth, distribute surplus cash and become more shareholder-friendly. New equity indices are being created that rank corporates for capital efficiency, dividends and management performance. Businesses are responding by making more regular and consistent dividend payments, operating share buybacks and being more transparent, responsive and performance-driven.

Structural reforms are transforming Japan’s long stagnant corporate sector

One of the outcomes of these changes is that many Japanese equities are now yielding more than European and US stocks and becoming increasingly attractive to income-hungry investors. This is all in stark contrast to days gone by, when companies were largely unaccountable to shareholders and tended to hoard cash, providing little incentive for foreign investors and helping to fuel the deflationary spiral that bedevilled the Japanese economy for decades.

These developments are making Japanese equities more attractive to own. Institutional investors, foreign and domestic – including the world’s largest institutional investor, Japan’s Government Pension Investment Fund – are investing in Japanese companies far more significantly than they have ever done in the past, generating real momentum behind Japan’s equity market.

These developments are making Japanese equities more attractive to own. Institutional investors, foreign and domestic – including the world’s largest institutional investor, Japan’s Government Pension Investment Fund – are investing in Japanese companies far more significantly than they have ever done in the past, generating real momentum behind Japan’s equity market.

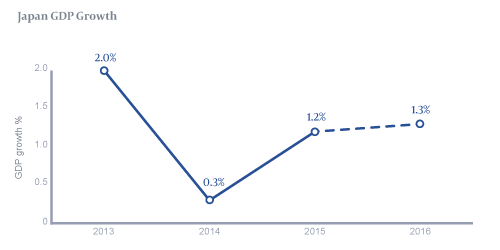

Yet Abenomics has not been an unqualified success. GDP growth has fluctuated, from 2.0% in 2013, to 0.3% in 2014,1.2% in 2015 and is estimated at 1.3% for 2016. Creating a consistent and positive inflationary trend to arrest Japan’s deflationary tendencies is proving tricky, and the feat has so far largely eluded policymakers.

Inflation rose year-on-year from 2013 to 2015, but fell in 2016. The Bank of Japan is currently forecasting 1.5% inflation for the next fiscal year – a figure that some believe is conservative given Japan’s growth prospects.

Even if the jury remains out on Abenomics’ overall efficacy, what really makes Japan stand out for us right now – and the reason we have been investing in Japan more heavily within our global portfolio – is valuation. While many developed markets around the world look fully, perhaps even over-valued, the current Japanese PE ratio of 15.5x is well below its 17x historic average, while the dividend yield of 1.95% is significantly higher than the 1.53% average. The relatively low valuations mean there is ample scope for stock prices to improve during the next twelve months.

In particular – after many years of being neglected by international and local investors – relatively cheap small and mid-cap Japanese equities in more economically sensitive, domestic sectors offer appeal. A risk to the Japanese equity outlook is President Trump’s threatened trade wars with countries he has accused of manipulating their currencies to boost exports, the alleged culprits of which include Japan. However, even if trade wars were to break out, the undervalued domestically-focused small and mid cap stocks in which we have been investing would arguably be more insulated from harm than Japan’s large cap exporting sector, to which we have limited exposure.

With Japan you always have to consider currency risk. We were unhedged throughout most of last year, which was of benefit as GBP fell with Brexit and Yen strengthened from a weak base. We decided to lock in our profits late last year and are now hedged again.

Rosie Bullard, Partner and Portfolio Manager at James Hambro & Partners

There have been many times in recent years when investors have thought Japanese equity markets were going to emerge from the gloom. After many false dawns, the land of the rising sun may finally deliver on its promise.

Rosie Bullard

You should not act on this content without taking professional advice. Opinions and views expressed are personal and subject to change. No representation or warranty, express or implied, is made of given by or on behalf of the Firm or its partners or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this document, and no responsibility or liability is accepted for any such information or opinions.

The value of an investment and the income from it can go down as well as up and investors may not get back the amount invested. This may be partly the result of exchange rate fluctuations in investments which have an exposure to foreign currencies. Fluctuations in interest rates may affect the value of your investment. The levels of taxations and tax reliefs depend on individual circumstances and may change. You should be aware that past performance is no guarantee of future performance.